Suffolk's Framework for Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Forest Heath District Council & St Edmundsbury Borough

PUBLIC NOTICE FOREST HEATH DISTRICT COUNCIL & ST EDMUNDSBURY BOROUGH COUNCIL Town and Country Planning (Development Management Procedure) (England) Order 2015 Planning (Listed Building and Conservation Areas) ACT 1990 Town and Country Planning (General Permitted Development) (Amendment) Order Advert types: EIA-Applications accompanied by an environmental statement; DP- Not in accordance with the Development Plan; PROW-Affecting a public right of way; M-Major development; LB-Works to a Listed Building; CLB-Within the curtilage of a Listed Building; SLB-Affecting the setting of a Listed Building; LBDC-Listed Building discharge conditions; C-Affecting a Conservation Area; TPO-Affecting trees protected by a Tree Preservation Order; LA- Local Authority Application Notice is given that Forest Heath District Council and St Edmundsbury Borough Council have received the following application(s): PLANNING AND OTHER APPLICATIONS: 1. DC/18/1812/FUL - Planning Application - Steel frame twin span agricultural machinery storage building (following demolition of existing), Home Farm The Street, Ampton (SLB)(C) 2. DC/18/1951/VAR - Planning Application - Variation of Conditions 7, 8 and 9 of DC/14/1667/FUL to enable re-wording of conditions so that they do not need to be implemented in their entirety but require them to be completed within a limited period for the change of use of woodland to Gypsy/Traveller site consisting of five pitches, Land South Of Rougham Hill Rougham Hill, Bury St Edmunds (PROW) 3. DC/18/1995/FUL - Planning Application - Change of use of open recreational space to children’s play area including installation of children’s play area equipment and multi use games area, Land East Of The Street, Ingham (SLB)(TPO) 4. -

Breckland Council Forest Heath District Council East Cambridgeshire District Council St Edmundsbury Borough Council Fenland Dist

Agenda Item 15 BRECKLAND COUNCIL FOREST HEATH DISTRICT COUNCIL EAST CAMBRIDGESHIRE DISTRICT COUNCIL ST EDMUNDSBURY BOROUGH COUNCIL FENLAND DISTRICT COUNCIL WAVENEY DISTRICT COUNCIL SUFFOLK COASTAL DISTRICT COUNCIL At a Meeting of the ANGLIA REVENUES AND BENEFITS PARTNERSHIP JOINT COMMITTEE Held on Tuesday, 25 September 2018 at 11.00 am in the Level 5 Meeting Room, Breckland House, St Nicholas Street, Thetford IP24 1BT PRESENT Mr D Ambrose Smith Mr I Houlder (Vice-Chairman) Mr P.D. Claussen Mr R Kerry Mr S. Edwards Mr C. Punt (Substitute Member) Mr M. Buckton (Substitute Member) In Attendance Nick Kahn - Strategic Director Sam Anthony - Head of HR & OD Jo Andrews - Strategic Manager (Revenues) Alison Chubbock - Chief Accountant (Deputy Section 151 Officer) (BDC) Paul Corney - Head of ARP Jill Korwin - Director (Forest Heath & St Edmundsbury) Adrian Mills - Strategic Manager (Benefits) ARP Stuart Philpot - Strategic Manager (Support Services) ARP Julie Britton - Democratic Services Officer Emma Grima - Director of Commercial Services (East Cambs District Council) Action By In the absence of the Chairman, the Vice-Chairman, Councillor Ian Houlder chaired the meeting. 27/18 MINUTES (AGENDA ITEM 1) The Minutes of the meeting held on 26 June 2018 were confirmed as a correct record. The Head of ARP pointed out that ARP Management were working together and would be putting forward a number of recommendations in relation to performance for the December meeting. 28/18 APOLOGIES (AGENDA ITEM 2) Apologies for absence were received from the Chairman, Councillor Bruce Provan, Councillor Ann Hay and Homira Javadi, Chief Finance Officer & S151 Officer for Waveney & Suffolk Coastal District Council. -

Suffolk County Council

Suffolk County Council Western Suffolk Employment Land Review Final Report May 2009 GVA Grimley Ltd 10 Stratton Street London W1J 8JR 0870 900 8990 www.gvagrimley.co.uk This report is designed to be printed double sided. Suffolk County Council Western Suffolk Employment Land Review Final Report May 2009 Reference: P:\PLANNING\621\Instruction\Clients\Suffolk County Council\Western Suffolk ELR\10.0 Reports\Final Report\Final\WesternSuffolkELRFinalReport090506.doc Contact: Michael Dall Tel: 020 7911 2127 Email: [email protected] www.gvagrimley.co.uk Suffolk County Council Western Suffolk Employment Land Review CONTENTS 1. INTRODUCTION........................................................................................................... 1 2. POLICY CONTEXT....................................................................................................... 5 3. COMMERCIAL PROPERTY MARKET ANALYSIS.................................................... 24 4. EMPLOYMENT LAND SUPPLY ANALYSIS.............................................................. 78 5. EMPLOYMENT FLOORSPACE PROJECTIONS..................................................... 107 6. BALANCING DEMAND AND SUPPLY .................................................................... 147 7. CONCLUSIONS AND RECOMMENDATIONS......................................................... 151 Suffolk County Council Western Suffolk Employment Land Review LIST OF FIGURES Figure 1 The Western Suffolk Study Area 5 Figure 2 Claydon Business Park, Claydon 26 Figure 3 Industrial Use in -

Support to Go Home Service

Information for patients, family, carers and staff Support to go home service What is this service? The Support to Go Home Service is comprised of health and care professionals working together to provide short term care provision for when you return home. Your social worker will have arranged a care package for you with a confirmed start date. When there is a delay to your start date, our service will be able to provide interim care to enable you to be discharged home. This service is hosted by West Suffolk Hospital and is provided in partnership with the West Suffolk NHS Foundation Trust and Suffolk County Council. There is no cost to you for this service for patients who are receiving a social care funded package of care. The team consists of an occupational therapist, care co-ordinator and support workers who will help you with your daily tasks, such as washing, dressing and meal preparation, within your home. They will work closely with you, your family, social care and the community teams, to ensure you experience a seamless service throughout your period of recovery. Aims of the service To enhance your recovery by not delaying your discharge, thus reducing your Source: Support To Go Home Service Reference No: 6306-2 Issue date: 29/4/19 Review date: 29/4/22 Page 1 of 3 risk of infections associated with a prolonged admission. To maximise your independence by offering early recovery support within your home. To provide advice, follow-up visits and referrals to external agencies as required. To ensure an appropriate level of care is provided according to your needs. -

Forest Heath District Council & St

PUBLIC NOTICE FOREST HEATH DISTRICT COUNCIL & ST EDMUNDSBURY BOROUGH COUNCIL Town and Country Planning (Development Management Procedure) (England) Order 2015 Planning (Listed Building and Conservation Areas) ACT 1990 Town and Country Planning (General Permitted Development) (Amendment) Order Advert types: DP-Not in accordance with the Development Plan; PROW-Affecting a public right of way; M-Major development; LB-Works to a Listed Building; CLB- Within the curtilage of a Listed Building; SLB-Affecting the setting of a Listed Building; C-Affecting a Conservation Area; TPO-Affecting trees protected by a Tree Preservation Order Notice is given that Forest Heath District Council and St Edmundsbury Borough Council have received the following application(s): PLANNING AND OTHER APPLICATIONS: 1. DC/17/0849/FUL - 1no. dwelling with new vehicular access and driveway (following demolition of existing dwelling and outbuildings), Halfway House Burwell Road, Exning (PROW) 2. DC/17/0892/FUL - Change of use and conversion from public house storage to residential dwelling, The Vine Inn High Street, Hopton (C) 3. DC/17/0895/FUL - Change of use from shop to mixed use, 128 High Street Newmarket, CB8 8JP (C, SLB) 4. DC/17/0897/FUL - 1no. dwelling, Hardwick Sharp Road, Bury St Edmunds (TPO) 5. DC/17/0902/LB - Replacement of 6no. windows, Brick Kiln Cottage Chevington Road, Horringer (LB, PROW) 6. DC/17/0928/FUL - Extension to existing building and change of use to residential (C3), The Dovecot Thurlow Hall, Bury Road (LC) 7. DC/17/0929/LB - Extension and alterations, The Dovecot Thurlow Hall, Bury Road (LC) 8. DC/17/0940/RM - Submission of details under Planning Permission DC/13/0123/OUT, Land Adjacent To Close View Aspal Lane, Beck Row (M) 9. -

September 2015

Chatsworth The Secret Garden The Felixstowe Society Newsletter Issue Number 110 September 1 2015 In this issue: Our trip to Chatsworth, Hardwick and Lincoln The Secret Garden of Westmorland Road Society News, Reviews and Research Registered Charity No. 277442 Founded 1978 The Felixstowe Society is established for the public benefit of people who either live or work in Felixstowe and Walton. Members are also very welcome from the Trimleys and the surrounding villages. The Society endeavours to: stimulate public interest in these areas promote high standards of planning and architecture and secure the improvement, protection, development and preservation of the local environment. Contents 3 Notes from the Chairman – Roger Baker 4 Calendar – September to December 2015 5 Can You Help Us? 6 Society News 8 Speaker Evening Report - An Audience with Peter Phillips 9 The Society Dinner 10 Speaker Evening Report - The Home Front in Suffolk 1914-18 11 An Evening at The Hut 12 Beach Clean 13 Society Members’ Feature 14 Felixstowe Youth Society 16 Our Three Day Trip to Derbyshire, South Yorkshire and Lincolnshire 18 Visit to Norwich and Kirstead Hall 19 Felixstowe Walkers 20 The Abbey Grove Challenge 22 Book Reviews 23 The Felixstowe Beach Hut and Chalet Association 24 News from The Felixstowe Museum 25 Research Corner 24 - Felixstowe’s Prefabs 28 Planning Applications March 21 to July 7 2015 30 If you wish to join The Society 32 More pictures from The Secret Garden Notes from the Chairman Welcome back after the summer break. I hope that you are looking forward to the new season of talks and activities – see the list of Speaker Meetings in this issue of the Newsletter. -

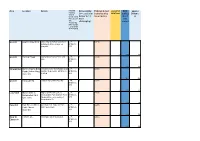

(3 = Easiest to Deliver to 1 = Most Challenging) Estimated Cost

Area Location Details Potential Deliverability Estimated Cost unweighted BCR approx Funding (3 = easiest to (calculated by MCAF total (ebike) Distance Source (Local Travel deliver to 1 = linear metre) nb 0 = m Plan, Section most not 106, challenging) scored Community Infrastructur e Levy, Dept. of Transport) Ipswich Ipswich Waterfront University of Suffolk waterfont LTP, 3 £473k building to Stoke bridge on S106/CIL, quayside DfT 5 44.1 789 Ipswich Portman Road Barrack Corner to Princes St LTP, 3 £214k junc S106/CIL, DfT 3 32.6 360 Stowmarket Chilton Way to Bury This link Lowry Way/Rugby Club LTP, 2 £495k Road (Chilton Way) junction to Bury Rd - BCR to be S106/CIL, Cycle link verified DfT 3 27.4 825 Ipswich Yarmouth Rd London Rd to Bramford Rd - LTP, 3 £327k S106/CIL, DfT 2 22.9 545 Lowestoft Higher Drive to Higher Dr/Woods Loke to LTP, 3 £432k Normanston Park Normanston Park (not incl Park S106/CIL, cycle route tracks) will need crossing of DfT Normanston Dr. 2 22.5 720 Haverhill Park Rd - A1307 to potential new route (or Park LTP, 3 £420k Castle Manor Rd?) spine route S106/CIL, Academy DfT 6 21.8 750 Bury St Cotton Lane Northgate St to Mustow St LTP, 1 £205k Edmunds S106/CIL, DfT 4 15.2 685 Ipswich Princes St link to rail station LTP, 2 £461k S106/CIL, DfT 3 14.9 770 Ipswich Belstead Rd Luther Rd to Stoke Bridge LTP, 2 £969k S106/CIL, DfT 3 13.4 1615 Ipswich Grove Ln to Civic Dr Rope Walk, Tackett St, Dogs LTP, 2 £1163k Head St S106/CIL, DfT 3 13.1 1940 Haverhill Manor Rd Ruffles Rd/Millfields Way junc, LTP, 3 £174k Manor Rd,Eringhausen -

2 Bedroom Apartments with 3 Bedroom Homes, Located in The

Akenham Spencer’s Court Tuddenham Whitton Bramford Road A14 Suffolk, IP1 5BQ Bramford Rushmere Saint Andrew Spencers Court A1214 A1156 How to find Spencer Court Valley Road Kesgrave A1214 Spencer’s Court Hadleigh Road A1214 Industrial Estate Ipswich A1071 From the A14 take junction 53 signposted A1156. Penzance Bramford Road At the roundabout take the exit signposted Ipswich A14 A1189 West and North (A1156). You will see Anglia Park A1071 London Road Suffolk, IP1 5BQ on the left and ASDA on the right. At the next A137 A1156 Felixstowe Roa roundabout take the second exit signposted Foxhall Hall ad d o town centre. You are now entering Ipswich. At the Chantry R traffic lights continue straight over into Norwich stead Wher Road (Shell petrol station on the right hand side) A137 Pinewood past the BP petrol station; continue to follow the Warren Heath A14 A12 A1189 Norwich Road through several sets of traffic lights. Copdock Just before the bridge turn right into Cromer Road. At the end of Cromer Road go straight over the crossroads into Eustace Road. Turn left into Bramford Ln A14 Brockleyr Cr Pitcairn Road and follow to the end. Turn right A1156 into Bramford Road and continue forward passing Cromer Rd Dandalan Close on the left and a new homes Hennisker Rd development on the left and right. You will see Spencers Court Bramford Rd Wallace Rd Spencers Court directly opposite the Post Office on Europe Way the fringe of Adair Road. Bramford Ln Bramford Rd Farthing Rd Sproughton Rd Sproughton Rd Hadleigh Rd Industrial Estate A1214 Yarmouth RdYarmouth High St Church Ln A14 London Rd Hadleigh Rd 2 bedroom apartments with Church Ln Hadleigh Rd Chantry Park London Rd 3 bedroom homes, located in the stunning area of Suffolk. -

Babergh and Mid Suffolk Joint Local Plan Statement of Common Ground

Babergh and Mid Suffolk Joint Local Plan Statement of Common Ground Between Babergh and Mid Suffolk District Councils and West Suffolk Council March 2021 1. Areas covered by the Statement of Common Ground The Statement of Common Ground relates to the area covered by the local planning authorities of Babergh District Council, Mid Suffolk District Council and West Suffolk Council. Page 1 of 10 2. Authorities covered by the Statement of Common Ground The signatories to this Statement of Common Ground are: • Babergh District Council, • Mid Suffolk District Council, and • West Suffolk Council. Ongoing engagement is being undertaken with Suffolk County Council, the West Suffolk Clinical Commissioning Group (CCG) and the West Suffolk NHS Foundation Trust and this Statement of Common Ground (SoCG) details the current position. An interim SoCG was published alongside the Joint Local Plan (JLP) Pre-Submission (Reg 19) Document (November 2020). 3. Purpose of Statement of Common Ground Local planning authorities have a statutory duty to co-operate with specified bodies in relation to strategic planning matters. The National Planning Policy Framework (NPPF) and accompanying Planning Practice Guidance require local authorities to produce a Statement of Common Ground as a written record on progress made for strategic planning matters across local authority boundaries and for this to be kept under review. Prior to the publication of the JLP Pre-Submission (Reg 19) Document, West Suffolk Council raised concerns to planning applications being determined in Thurston and to a lesser extent in Elmswell and Woolpit and the cumulative impact of residential development on public services, especially health, highways and leisure. -

Bury Town INT Executive Summary

Bury Town INT: Executive summary Place-Based Needs Assessment (version 1.0, 2019) Executive Summary Public Health Suffolk Page 1 of 11 Bury Town INT: Executive summary Place-Based Needs Assessment (version 1.0, 2019) Main authors Tom Delaney, Alliance JSNA Researcher Alison Matthews, Senior JSNA researcher Tess Zermanos, Health and Care Programme Manager Main editors Natacha Bines, Head of Population Insight Anna Crispe, Head of Knowledge & Intelligence Consultant reviewers Dr Padmanabhan Badrinath, Consultant in Public Health Medicine Dr Jeptepkeny Ronoh, Consultant in Public Health Medicine With many thanks to Integrated Neighbourhood Team colleagues and wider Suffolk colleagues for their input, collaboration and consultation. This is version 1 created on 25th November 2019 Public Health Suffolk Page 2 of 11 Bury Town INT: Executive summary Place-Based Needs Assessment (version 1.0, 2019) Contents Executive summary .................................................................................................................................. 5 Demographics ..................................................................................................................................... 5 Population ....................................................................................................................................... 5 Age profile ....................................................................................................................................... 5 Population projections ................................................................................................................... -

Council Size Proposal for a Future Council for West Suffolk Submitted

Council Size Proposal for a Future Council for West Suffolk Submitted on behalf of Forest Heath District Council and St Edmundsbury Borough Council In September 2017, Forest Heath District Council (FHDC) and St Edmundsbury Borough Council (SEBC) agreed a business case that supports the formation of a single district-tier Council for West Suffolk. This business case has now been submitted to the Secretary of State, who, under s.15 of the Cities and Local Government Devolution Act 2016, has the power to issue an Order to create the new Council. The business case and associated appendices is available at http://svr-mgov-01:9070/ieListDocuments.aspx?CId=172&MId=3649&Ver=4 That Order will include those ancillary matters necessary to bring the new Council into being. One of the most important aspects is the number of Councillors necessary to operate the new council. Whilst this decision will be made by the Secretary of State, we consider it important that we submit our views, as the current District and Borough Councillors for West Suffolk, on the number of Councillors we believe the future Council should have. This paper covers: - Background to West Suffolk as a place - Background to West Suffolk councils - Forming our argument for council size, including: o The governance arrangements of the council o Regulatory decision making o Scrutiny and oversight arrangements o Responsibility to outside bodies o The representational role of councillors o Views of the residents of West Suffolk o How our argument creates a council size - Conclusion About West Suffolk West Suffolk is a growing area. -

Trust-Open-Board-Meeting-Pack-26 February 2021

Board of Directors (In Public) Schedule Friday 26 February 2021, 9:15 AM — 12:15 PM GMT Venue Via video conferencing Description A meeting of the Board of Directors will take place on Friday, 26 February 2021 at 9:15. The meeting will be held virtually via video conferencing Organiser Karen McHugh Agenda AGENDA Presented by Sheila Childerhouse Agenda Open Board 2021 02 26 Feb.docx 9:15 GENERAL BUSINESS Presented by Sheila Childerhouse 1. Resolution The Trust Board is invited to adopt the following resolution: “That representatives of the press, and other members of the public, be excluded from the meeting having regard to the guidance from the Government regarding public gatherings.” For Reference - Presented by Sheila Childerhouse 2. Apologies for absence: Kate Vaughton To NOTE any apologies for the meeting and request that mobile phones are set to silent For Reference - Presented by Sheila Childerhouse 3. Declaration of interests for items on the agenda To NOTE any declarations of interest for items on the agenda For Reference - Presented by Sheila Childerhouse 4. Questions from the public relating to matters on the agenda To RECEIVE questions from members of the public of information or clarification relating only to matters on the agenda Presented by Sheila Childerhouse 5. Review of agenda To AGREE any alterations to the timing of the agenda. For Reference - Presented by Sheila Childerhouse 6. Minutes of the previous meeting To APPROVE the minutes of the meeting held on 29 January 2021 For Approval - Presented by Sheila Childerhouse Item 6 - Open Board Minutes 2021 01 29 Jan Draft.docx 7.