APPLEGREEN PLC 2019 ANNUAL REPORT + FINANCIAL STATEMENTS Applegreen Spalding, UK 2 APPLEGREEN PLC ANNUAL REPORT and FINANCIAL STATEMENTS 2019 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Store Store Name Store Postcode Asda Great Bridge DY4 7HW Asda

Store Store Name Store Postcode Asda Great Bridge DY4 7HW Asda PARK ROYAL NEW NW10 7LW Asda Ashford, GB TN24 0SE Asda Roehampton SW15 3DT Asda Eastleigh SO53 3YJ Asda Dagenham RM9 6SJ Asda Bridge of Dee Aberdeen AB10 7QA Asda Kings Hill (West Malling) ME19 4SZ Asda Milton Keynes MK1 1SA Asda Killingbeck LS14 6UT Asda Havant PO9 3QW Asda Watford WD18 8AD Asda Roehampton SW15 3DT Asda Govan G51 3HR Asda Lower Earley RG6 5TT Asda Wigan WN5 0XA Asda WAKEFIELD DURKAR WF2 7EQ Asda Wallington CR0 4XS Asda Pudsey LS28 6AN Asda Colindale NW9 0AS Euro Garages Frontier Park - Flagstaff BB1 2HR Euro Garages The Gateway WV10 7ER Euro Garages Bolton - Blackburn Road BL1 7LR Euro Garages Armada B23 7PG Euro Garages Cannock WS11 9NA Morrisons Sutton Cheam Road SM1 1DD Morrisons Wood Green N22 6BH Morrisons Hatch End HA5 4QT Morrisons Holloway N7 6PL Morrisons Preston Riversway PR2 2YN Morrisons BANGOR HOLYHEAD RD LL57 2ED Morrisons Rochdale OL16 4AT Morrisons Bradford - Victoria BD8 9TP Morrisons Queensbury NW9 6RN Morrisons Bolton BL1 1PQ Morrisons Maidstone Sutton Rd ME15 9NN Morrisons Stamford PE9 2FT Morrisons Reading Rose Kiln Way RG2 0HB Morrisons WELWYN GARDEN CITY BLACK FAN RD AL7 1RY Morrisons Farnborough Southwood GU14 0NA Morrisons Dagenham wood lane RM10 7RA Morrisons Enfield EN1 1TW Morrisons Swindon SN3 3TX Morrisons Aldershot GU11 1NX Morrisons Basingstoke RG21 8BJ Morrisons Bracknell RG12 1EN Morrisons REIGATE BELL ST RH2 7BA Morrisons LONDON ACTON W3 9LA Morrisons Watford WD18 8AD Morrisons ST ALBANS HATFIELD RD AL1 4SU Morrisons Gravesend -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Morning Wrap

Morning Wrap Today ’s Newsflow Equity Research 16 Nov 2020 08:34 GMT Upcoming Events Select headline to navigate to article Kingspan FY20 to be a year of profit growth Company Events 16-Nov Kainos Group; Q221 Results Irish Banks EU banks should focus on cost cutting and Kingspan; Q320 Trading Update need a more discerning regulator 17-Nov easyJet; FY20 Results 18-Nov Breedon Group; Q320 Trading Update UK Housebuilders Rightmove asking prices fall 0.5% in British Land Company; Half Year Results 2021 Origin Enterprises; Q121 Trading Update November SSP Group; Full year results Supermarket Income REIT Accretive acquisitions add to 20-Nov Mitchells & Butlers; Full year results 23-Nov Codemasters Group; Q221 Results occupier mix Hibernia REIT Preview ahead of Tuesday’s HY21 Results Economic Events Ireland United Kingdom United States Europe This document is intended for the sole use of Goodbody Investment Banking and its affiliates Goodbody Capital Markets Equity Research +353 1 6419221 Equity Sales +353 1 6670222 Bloomberg GDSE<GO> Goodbody Stockbrokers UC, trading as “Goodbody”, is regulated by the Central Bank of Ireland. In the UK, Goodbody is authorised and subject to limited regulation by the Financial Conduct Authority. Goodbody is a member of Euronext Dublin and the London Stock Exchange. Goodbody is a member of the FEXCO group of companies. For the attention of US clients of Goodbody Securities Inc, this third-party research report has been produced by our affiliate, Goodbody Stockbrokers Goodbody Morning Wrap Kingspan FY20 to be a year of profit growth Kingspan has released a trading update for Q320. -

Driver's Guide

Driver’s Guide Downloadable version last updated: 19/07/19 Download ‘intruck’ and locate Truck Parks on your smart phone +44 (0)1603 777242 www.snapacc.com #DrivingEfficiency Parking Map Overview PAGE 16 PAGE 25 PAGE 12 PAGE 4 PAGE 24 PAGE 23 PAGE 8 PAGE 26 PAGE 22 2 3 South East Parking Map & Listing Red Lion Truck Stop, NN7 4DE Caenby Corner LN8 2AR 47 M1 J16, Upper Heyford, 01604 248 Transport Ltd., A15, 01673 Please note that all green parking sites must be pre-booked online, by calling Northampton. 831914 M180 J4, Glentham. 878866 +44 (0)1603 777242 or through our partner app intruck, where you can also see real time The Fox Inn A1, A1, Great NG33 5LN Chris’s Cafe, A40, M40 HP14 3XB availability of spaces. 51 North Rd, Colsterworth, 01572 250 J5, Wycombe Road, 01494 If you wish to cancel a booking, it must be done by 4pm or you will still be charged. Grantham. 767697 Stokenchurch. 482121 To call these numbers from outside of the UK, please add +44 before dialling the number. Jacks Hill Café, A5, M1 NN12 8ET Airport Cafe, A20, M20 TN25 6DA Please be aware you cannot use SNAP for parking at Welcome Break, Moto, or Roadchef 54 J15a, Watling Street, 01327 262 J11, Main Road, Sellindge, 01303 Motorway Service Areas. Towcester. 351350 Ashford, Kent. 813185 Junction 29 Truckstop, S42 5SA Portsmouth Truckstop, PO6 1UJ Service Key 94 A6175, M1 J29, Hardwick 01246 326 A27, M27 J12, Railway 02392 View Road, Chesterfield. 599600 Triangle, Walton Road. 376000 Truck Parking Extra Services Baldock, SG7 5TR Havant Lorry Park, A27, PO9 1JW Truck Parking and Washing 189 A1(M) J10, Radwell, 07703 331 A3(M), Southmoor Lane, 02392 Baldock, Hertfordshire. -

Growth Company Index 2019

JUNE 2019 Restaurants, Hospitality & Leisure GROWTH COMPANY INDEX 2019 The AlixPartners Growth Company Index, now in its eighth year, has become a beacon for the UK’s very best restaurant, pub and bar companies, highlighting excellent financial performance. This year’s list highlights that both fledgling and its biggest site to date in Chelsea. The company also established businesses can thrive, through offering a operates sites in its homeland Denmark and launched strong customer experience and an innovative approach, in Berlin last year, and has a further opening lined up in allied to operational discipline and robust management— central London, in Beak Street. That would take its total despite the ongoing headwinds buffeting the eating and estate to 22 sites, including nine in the UK. The company drinking out sector. says this culture of what it calls ‘measured expansion’ allows them to fully focus on giving guests a great New entrant Sticks‘n’Sushi, the Copenhagen-based experience alongside a great product restaurant group backed by Maj Invest Equity and specialising in premium sushi and yakitori sticks, topped A look at the 2019 index shows that all parts of the diverse this year’s list, generating a compound annual growth eating and drinking out sector are represented; from rate (CAGR) of 129.2%. Its position at the summit follows the fast-growing trend of experiential and competitive an impressive recent performance from the company, socialising formats to traditional family brewers; from founded in 1994 by the Danish-Japanese brothers Jens exciting new entrants to the long-established perennials of and Kim Rahbek Hansen. -

Store List For

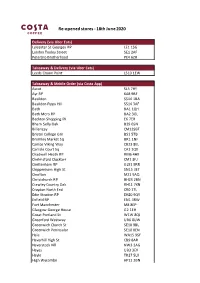

Re-opened stores - 18th June 2020 Delivery (via Uber Eats) Leicester St Georges RP LE1 1SG London Tooley Street SE1 2AF Peterbro Brotherhood PE4 6ZR Takeaway & Delivery (via Uber Eats) Leeds Crown Point LS10 1EW Takeaway & Mobile Order (via Costa App) Ascot SL5 7HY Ayr RP KA8 9BF Basildon SS14 1BA Basildon Pipps Hill SS14 3AF Bath BA1 1QH Bath Mero RP BA2 3GL Beckton Shopping Pk E6 7ER Bham Selly Oak B29 6SN Billericay CM129BT Bristol College Grn BS1 5TB Bromley Market Sq BR1 1NF Cambs Viking Way CB23 8EL Carlisle CoUrt Sq CA1 1QX Chadwell Heath RP RM6 4HX Chelmsford Clocktwr CM1 3FJ Cheltenham RP GL51 9RR Chippenham High St SN15 3ET Chorlton M21 9AQ ChristchUrch RP BH23 2BN Crawley CoUntry Oak RH11 7XN Croydon North End CR0 1TL Edin Straiton RP EH20 9QY Enfield RP EN1 3RW Fort Manchester M8 8EP Glasgow George HoUse G2 1EH Great Portland St W1W 8QJ Greenford Westway UB6 0UW Greenwich ChUrch St SE10 9BL Greenwich PeninsUlar SE10 0EN Hale WA15 9SF Haverhill High St CB9 8AR Haverstock Hill NW3 2AG Hayes UB3 3EX Hayle TR27 5LX High Wycombe HP11 2BN Holloway Road N7 6PN Kingston KT1 1JH Leeds Merrion LS2 8BT Leicester Haymarket LE1 3YR Leigh on Sea SS9 1PA Lon Brent Cross Sth NW2 1LS Lon Charlton SE7 7AJ Lon Friern Bridge RP N11 3PW Lon Leyton Mills RP E10 5NH Lon SoUthampton St WC2E 7HG Lon SoUthwark SE1 8LP Lon Staples CornerRP NW2 6LW Lon Wembley Central HA9 7AJ LoUghton IG10 1EZ Manchester Market St M1 1WA Manchester Portland M60 1HR Milton Keynes Kingst MK10 0BA NewqUay TR7 1DH Northampton NN1 2AJ Orpington BR5 3RP Perth Inveralmond RP -

Glanbia Reports Improving Trends in Q3 2020

THIRD QUARTER 2020 INTERIM MANAGEMENT STATEMENT Glanbia reports improving trends in Q3 2020 29 October 2020 – Glanbia plc, the global nutrition group (‘Glanbia’ or the ‘Group’), is issuing this Interim Management Statement for the nine month trading period ended 3 October 2020 (“Q3 YTD” or “first nine months of 2020”). Summary Improving trends in Q3 2020 while navigating the challenges resulting from the Covid-19 pandemic; Q3 YTD wholly owned revenues up 1.0% reported. On a like-for-like* basis up 3.1% versus prior year; Good performance from Glanbia Nutritionals (“GN”) maintaining growth trajectory, Q3 YTD like-for-like revenues up 10.9% versus prior year; Foodarom acquisition closed in the third quarter; Improving trends in Glanbia Performance Nutrition (“GPN”) in the third quarter. Q3 2020 like-for-like branded revenue down 2.3% versus Q3 2019 with positive pricing. Q3 2020 EBITA margin in double digits; GPN transformation programme on track and delivering margin improvements; Joint Ventures (“JVs”) continue to deliver a robust performance; Group is in a strong financial position, net debt at Q3 period end improved by €187.7 million versus the prior year with a net debt to EBITDA ratio of 1.95 times; Glanbia announces intention to launch a share buy-back programme of up to €50 million; and In Q4 2020, notwithstanding continued Covid-19 related uncertainty, Glanbia expects GN and JVs to continue to deliver a resilient earnings performance in addition to further sequential improvement in GPN. Commenting today, Siobhán Talbot, Group Managing Director said: “I would like to again acknowledge the tremendous efforts of all my Glanbia colleagues as well as our supplier and customer partners as we navigate the challenges of 2020. -

Global Equity Fund Description Plan 3S DCP & JRA MICROSOFT CORP

Global Equity Fund June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA MICROSOFT CORP 2.5289% 2.5289% APPLE INC 2.4756% 2.4756% AMAZON COM INC 1.9411% 1.9411% FACEBOOK CLASS A INC 0.9048% 0.9048% ALPHABET INC CLASS A 0.7033% 0.7033% ALPHABET INC CLASS C 0.6978% 0.6978% ALIBABA GROUP HOLDING ADR REPRESEN 0.6724% 0.6724% JOHNSON & JOHNSON 0.6151% 0.6151% TENCENT HOLDINGS LTD 0.6124% 0.6124% BERKSHIRE HATHAWAY INC CLASS B 0.5765% 0.5765% NESTLE SA 0.5428% 0.5428% VISA INC CLASS A 0.5408% 0.5408% PROCTER & GAMBLE 0.4838% 0.4838% JPMORGAN CHASE & CO 0.4730% 0.4730% UNITEDHEALTH GROUP INC 0.4619% 0.4619% ISHARES RUSSELL 3000 ETF 0.4525% 0.4525% HOME DEPOT INC 0.4463% 0.4463% TAIWAN SEMICONDUCTOR MANUFACTURING 0.4337% 0.4337% MASTERCARD INC CLASS A 0.4325% 0.4325% INTEL CORPORATION CORP 0.4207% 0.4207% SHORT-TERM INVESTMENT FUND 0.4158% 0.4158% ROCHE HOLDING PAR AG 0.4017% 0.4017% VERIZON COMMUNICATIONS INC 0.3792% 0.3792% NVIDIA CORP 0.3721% 0.3721% AT&T INC 0.3583% 0.3583% SAMSUNG ELECTRONICS LTD 0.3483% 0.3483% ADOBE INC 0.3473% 0.3473% PAYPAL HOLDINGS INC 0.3395% 0.3395% WALT DISNEY 0.3342% 0.3342% CISCO SYSTEMS INC 0.3283% 0.3283% MERCK & CO INC 0.3242% 0.3242% NETFLIX INC 0.3213% 0.3213% EXXON MOBIL CORP 0.3138% 0.3138% NOVARTIS AG 0.3084% 0.3084% BANK OF AMERICA CORP 0.3046% 0.3046% PEPSICO INC 0.3036% 0.3036% PFIZER INC 0.3020% 0.3020% COMCAST CORP CLASS A 0.2929% 0.2929% COCA-COLA 0.2872% 0.2872% ABBVIE INC 0.2870% 0.2870% CHEVRON CORP 0.2767% 0.2767% WALMART INC 0.2767% -

Sr No. Zone Restaurant Name Address of the Restaurant City of the Restaurant Offer Details Offer Exclusions End Date

Sr No. Zone Restaurant Name Address of the restaurant City of the restaurant Offer Details Offer Exclusions End Date 1 South 1947 296, Ram Towers, 100 Feet Ring Road, Banashankari, Bangalore Bangalore 15% off on Total Bill Not Valid on Buffet 31st May 2019 62, The High Street Building, 5th Floor, Opposite Vijaya College, 2 South 1947 Bangalore 15% off on Total Bill Not Valid on Buffet 31st May 2019 4th Block, Jayanagar, Bangalore 5, 4th Floor, Above GIRIAS, 15th Cross, Malleshwaram, 3 South 1947 Bangalore 15% off on Total Bill Not Valid on Buffet 31st May 2019 Bangalore 5, Ground Floor, Number 2, First Main, Industrial Town, West of 4 South 1947 Bangalore 15% off on Total Bill Not Valid on Buffet 31st May 2019 Chord Road, Rajajinagar, Bangalore 292/A, 12th Cross, Ideal Homes Township, Rajarajeshwari 5 South 1947 Bangalore 15% off on Total Bill Not Valid on Buffet 31st May 2019 Nagar, Bangalore 6 South 18 Degree North - Clarion Hotel Clarion Hotel, 25, Dr. Radhakrishnan Salai, Mylapore, Chennai Chennai 20% off on Total Bill Not Valid on Buffet 31st October 2019 31, 1st Floor, Santhome Inn, High Road, Basha Garden, 7 South AKI BAY Chennai 15% off on Total Bill Not Valid on Buffet 14th June 2019 Mylapore, Chennai 6, Seetharam Main Road, Tambaram Main Road, Velachery, 8 South AKI BAY Chennai 15% off on Total Bill Not Valid on Buffet 14th June 2019 Chennai 7/3, ASK Tower, Next to Bata Showroom, Kundanahalli Gate, 9 South Amanthrana Gardenia Bangalore 15% off on Total Bill Not Valid on Buffet 15th June 2019 AECS Layout, Brookefield, Bangalore -

England's Motorway Services Show Star Quality

England’s Motorway Services show star quality 9 March 2015: Top 5* star ratings have been awarded to seven Motorway Service Stations from across the country as part of VisitEngland’s Motorway Service Area Quality Scheme. Whether travelling for business or leisure, Service Stations provide important stopping points for people visiting an area and this experience can add to the overall enjoyment of the trip. As National Tourist Board for England, VisitEngland assesses the quality of service and customer experience at service stations across the country to help encourage a high quality experience for all travellers. Five leading operators took part in this year’s quality scheme - Extra, Moto, Welcome Break, Roadchef and Westmorland, who collectively own 107 sites across England. A further 42 services will received a 4 Star rating and the remaining 58 services are rated as 3 Star. As part of the Scheme, VisitEngland Assessors anonymously visited all the operators’ individual sites twice over the last 12 months and completed a thorough quality report. On each visit, the Assessor looks at the whole of the customer journey, from initial arrival right through to the use of facilities, retail and catering outlets, to departure. The sites’ service stations are assessed on the quality of catering, cleanliness, staff, food, forecourt, retail, service, toilet facilities and overall site – which can include anything from the baby changing, coach parking space or facilities for dogs. Top 5* ratings have been awarded to the following Motorway Service stations: Beaconsfield, Buckinghamshire, Beaconsfield achieved an overall score of 90 per cent which means that Junction 2 of M40, Extra the services has now progressed from 4* to 5* in the last 12 months. -

The Utility Warehouse Cashback Card

The Utility Warehouse CashBack Card Participating Retailer Terms & Conditions Transactions made using a Utility Warehouse CashBack card will attract a saving of between 3% and 10% (based on the price paid at the till) payable as CashBack on your Utility Warehouse monthly bill, at the following Participating Retailers. Please note that all CashBack is subject to the terms and conditions below: Participating Retailer CashBack Sainsbury’s (groceries and fuel) 3% American Golf 5% Argos 5% ASK Italian 5% B&Q 5% Belgo 5% Bella Italia 5% Body Shop 5% Boots 5% Burton 5% Café Rouge 5% Caffè Nero 5% Carpetright 5% Clarks 5% Debenhams 5% Dorothy Perkins 5% Evans 5% Evans Cycles 5% Feel Unique 5% GAP 5% Halfords 5% Hotel Voucher Shop 5% House of Fraser 5% Knowledge is King 5% Laithwaite’s Wine 5% Miss Selfridge 5% Mappin & Webb 5% Marks and Spencer 5% Moss Bros. 5% National Express 5% Outfit 5% Printwell 5% Pizza Hut 5% Spafinder 5% The White Company 5% The Works 5% TopShop 5% TopMan 5% Tunetribe 5% Wallis 5% Waterstones 5% Wilko 5% Wyevale Garden Centres 5% YO! Sushi 5% Zizzi 5% Mothercare 6% New Look 6% Pizza Express 6% River Island 6% Ernest Jones 7% Goldsmiths 7% H Samuel 7% Leslie Davis 7% Papa John’s Pizza 7% TGI Fridays 7% Thorntons 7% Virgin Experience 7% Utility Warehouse, Network HQ, 508 Edgware Road, The Hyde, London NW9 5AB May 2018 Participating Retailer Terms & Conditions 1. Savings only apply to purchases made from the listed Participating Retailers at stores located within the UK and online using their UK website. -

Transforming Dublin

Hibernia REIT plc Annual Report 2018 Annual Report Transforming Dublin Annual Report 2018 About us Hibernia is a Dublin- focused REIT, listed on Euronext Dublin and the London Stock Exchange, which owns and develops Irish property. All of our €1.3bn portfolio is in Dublin and we specialise in city centre offices. We aim to use our knowledge and experience of the Dublin property market, together with modest levels of leverage, to generate above average long-term returns for our shareholders. We focus on improving buildings at appropriate times in the property cycle and growing income: our portfolio is mainly a mix of regenerated properties and assets held for future repositioning. Clockwise from top left: 1SJRQ under construction 1WML 2WML (CGI) 2DC Clanwilliam Court 1 Cumberland Place Phase II (CGI) Hibernia’s Management Team at 1SJRQ Hibernia REIT plc Annual Report 2018 Strategic report Governance Financial statements Contents Strategic report IFC About us 02 Our business at a glance 03 Our portfolio 04 Why Dublin? 06 Chairman’s statement 08 CEO’s statement 12 Market review 14 Business model 16 Strategic priorities 18 Key performance indicators 19 Operational metrics 20 Strategy in action 24 Operational review 24 – Portfolio overview 26 – Acquisitions and disposals 28 – Developments and refurbishments 31 – Asset management 33 – Financial results and position 36 Risk management 40 Principal risks and uncertainties 48 Sustainability Governance 68 Chairman’s corporate governance statement 72 Board of Directors 74 Our Management Team 77 Corporate