Competitive Snapshot

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Country Club Plaza

KANSAS CITY — MISSOURI COUNTRY CLUB PLAZA 4750 BROADWAY, KANSAS CITY, MISSOURI 64112 CULTURAL EPICENTER SELECT TENANTS — — Country Club Plaza is the dominant upscale shopping and dining destination in Kansas City. This one-of-a- kind, 15-block open air destination also serves as an urban cultural district offering long-standing yearly events and traditions. UNIQUE-TO-MARKET — Including Eileen Fisher, Free People, Kate Spade New York, Moosejaw, Sur La Table, Tiffany & Co., Vineyard Vines, Warby Parker and West Elm. DINING — Brio Tuscan Grille, Buca Di Beppo, Chuy’s Mexican Food, Classic Cup Cafe, Cooper’s Hawk Winery, Fogo de Chao, Gram & Dun, Granfalloon Restaurant & Bar, Hogshead Kansas City, Jack Stack Barbecue, McCormick & Schmick’s, O’Dowd’s Gastrobar, P.F. Chang’s, Parkway Social, Rye, Seasons 52, Shake Shack, The Capital Grille, The Cheesecake Factory, The Melting Pot, True Food Kitchen, Zocalo Mexican Cuisine and Tequileria and more. LOCATION — The Plaza is at the heart of where people live and work, with over 20 condominium communities within walking distance and many multi-million dollar homes within five miles of the Plaza. 2019 TRADE AREA DEMOGRAPHICs – 15-MILE RADIUS (SOURCES: CLARITAS, TETRAD, ENVIRONICS, ESRI) TOURISM ll rights reserved. A — Population ______________________ 1,337,953 Households ______________________ 551,630 Kansas City welcomed a record 25.2 million visitors in and its licensors are $75K+ Households _______________ 223,970 RI 2016 who spent $3.4 billion. S $100K+ Households ______________ 155,045 E and its licensors. Daytime Population ______________ 1,522,073 RI S In its 88th year, the Plaza Art Fair, recognized as one of —— E the top five art fairs in the U.S., is held during the third MALL TENANT SPACE week of September. -

Country Club Plaza Walking Guide

7 WAYS OF LOOKING AT THE PLAZA 50 NOTABLE THINGS TO SEE BY HISTORIC KANSAS CITY COUNTRY CLUB PLAZA WALKING GUIDE PUBLISHED WITH THE SUPPORT OF THE WILLIAM T. KEMPER FOUNDATION COUNTRY CLUB PLAZA WALKING GUIDE Introduction .................................................................... 3 7 Ways of Looking at the Plaza: A few words about the history and lasting value of Kansas City’s prized shopping district. Planning ........................................................................... 4 Architecture ..................................................................... 6 Business ............................................................................ 8 Placemaking .................................................................. 10 Neighborhood .............................................................. 12 Community ................................................................... 14 Legacy ............................................................................. 16 50 Notable Things to See: A Plaza Walking Guide: Towers, tiles and tucked-away details that make up the essence of the Country Club Plaza. Maps and details .....................................................18-33 A Plaza Timeline ..........................................................34 Acknowledgments ......................................................34 Picture credits ...............................................................34 About Historic Kansas City Foundation ...............35 2 INTRODUCTION TAKE A WALK By Jonathan Kemper n addition -

1625 Watt Avenue WATT AVENUE & ARDEN WAY, SACRAMENTO, CALIFORNIA

FOR SALE OR LEASE> ±9,584 SF FREESTANDING RESTAURANT BUILDING 1625 Watt Avenue WATT AVENUE & ARDEN WAY, SACRAMENTO, CALIFORNIA Highlights > ±9,584 square foot freestanding building > ±1.21 acre site with 71 parking spaces > Recently-renovated, fully improved restaurant building > High identity location in a prime retail trade area > Heavily-trafficked intersection, over 50,000 cars per day > Highly-visible monument and building signage > Strong residential and daytime population Traffic Count > Watt Avenue @ Arden Way: 50,084 ADT > Arden Way @ Watt Avenue: 22,124 ADT Demographic Snapshot 1 Mile 3 Miles 5 Miles Population 16,610 144,257 332,104 Daytime Population 18,687 166,145 383,255 Households 6,808 60,490 130,824 Average Income $80,656 $70,554 $66,946 Pricing > Sale Price: $2,200,000 > Lease Rate: $1.50/SF NNN (Estimated Operating Expenses: ±$0.50/SF) COLLIERS INTERNATIONAL MARK ENGEMANN MICHAEL DRAEGER San Francisco Peninsula [email protected] [email protected] 203 Redwood Shores Pkwy, Ste 125 +1 916 563 3007 +1 650 486 2221 Redwood City, CA 94065 CA License No. 00865424 CA License No. 01766822 colliers.com/redwoodcity FOR SALE OR LEASE> ±9,584 SF FREESTANDING RESTAURANT BUILDING 1625 Watt Avenue WATT AVENUE & ARDEN WAY, SACRAMENTO, CALIFORNIA Market Square Country Club Centre Country Club Plaza Arden & Watt Point West Plaza Arden Plaza Arden Square 1625 WATT AVENUE Arden Watt Marketplace MARK ENGEMANN MICHAEL DRAEGER [email protected] [email protected] +1 916 563 3007 +1 650 486 2221 CA License No. 00865424 CA License No. 01766822 FOR SALE OR LEASE> ±9,584 SF FREESTANDING RESTAURANT BUILDING 1625 Watt Avenue WATT AVENUE & ARDEN WAY, SACRAMENTO, CALIFORNIA EXISTING ADJACENT SINGLE STORY OFFICE BUILDING Site Plan PROJECT SUMMARY THIS PROJECT IS A PROPOSED RENOVATION OF AN EXISTING RESTAURANT BUILDING. -

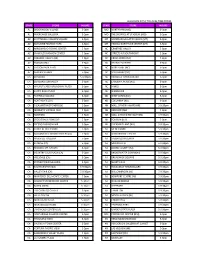

Store # Address 1 Address 2 City State 1 2837 WINCHESTER PIKE

Store # Address_1 Address_2 City State 1 2837 WINCHESTER PIKE BERWICK PLAZA COLUMBUS OH 3 PEACH ORCHARD PLAZA 2708 PEACH ORCHARD RD AUGUSTA GA 5 GREAT SOUTHERN S/C 3755 S HIGH STREET COLUMBUS OH 7 68 N WILSON ROAD GREAT WESTERN SC COLUMBUS OH 21 606 TAYWOOD ROAD NORTHMONT PLAZA ENGLEWOOD OH 29 918 EAST STATE STREET ATHENS SHOPPING CENTER ATHENS OH 30 818 S. MAIN STREET BOWLING GREEN OH 32 2800 WILMINGTON PIKE DAYTON OH 37 13 ACME STREET MARIETTA OH 39 2250 DIXIE HIGHWAY HAMILTON PLAZA HAMILTON OH 42 2523 GALLIA STREET PORTSMOUTH OH 43 3410 GLENDALE AVE. SOUTHLAND SHOPPING CENTER TOLEDO OH 45 3365 NAVARRE AVENUE OREGON OH 49 825 MAIN STREET MILFORD OH 51 1090 MILLWOOD PIKE WINCHESTER VA 57 OAKHILL PLAZA S/C 3041 MECHANICSVILLE TURNPIKE RICHMOND VA 58 370 KROGER CENTER MOREHEAD KY 61 800 14TH STREET W. HUNTINGTON WV 62 1228 COUNTRY CLUB ROAD COUNTRY CLUB PLAZA FAIRMONT WV 64 127 COMMERCE AVE COMMERCE VILLAGE S/C LAGRANGE GA 71 1400 S. ARLINGTON STREET ARLINGTON PLAZA AKRON OH 72 3013 NORTH STERLING AVE WARDCLIFFE S/C PEORIA IL 77 1615 MARION-MT. GILEAD ROAD FORUM SHOPPING CENTER MARION OH 78 3600 S DORT HIGHWAY #58 MID-AMERICA PLAZA FLINT MI 79 1140 PARK AVENUE WEST MANSFIELD OH 82 1350 STAFFORD DRIVE PRINCETON WV 83 1211 TOWER BLVD. LORAIN OH 86 ALTON SQUARE SHOPPING CTR 1751 HOMER ADAMS PARKWAY ALTON IL 91 5520 MADISON AVE INDIANAPOLIS IN 97 1900 BRICE RD BRICE POINT REYNOLDSBURG OH 98 498 CADIZ RD STEUBENVILLE OH 102 27290 EUREKA ROAD CAMBRIDGE SQUARE TAYLOR MI 109 15 E 6TH STREET BELLEVUE PLAZA BELLEVUE KY 111 5640 N. -

Store Number

Store Number STORE NAME State 0788 ANCHORAGE AK 0124 BIRMINGHAM AL 0140 RIVERCHASE GALLERIA AL 0724 HUNTSVILLE AL 0132 PINNACLE HILLS AR 0488 LITTLE ROCK AR 0016 BILTMORE AZ 0094 ARROWHEAD AZ 0168 SAN TAN VILLAGE AZ 0288 CHANDLER AZ 0364 SCOTTSDALE AZ 0480 TUCSON AZ 0736 THE QUARTER AZ 0926 PARK PLACE AZ 1258 DANA PARK AZ 1308 NORTERRA AZ 0026 SANTA MONICA CA 0028 HILLSDALE CA 0030 ANAHEIM CA 0032 HOLLYWOOD & HIGHLAND CA 0034 PASADENA CA 0036 FASHION VALLEY CA 0038 UNIVERSITY TOWNE CENTER CA 0048 STANFORD CA 0052 BURLINGAME CA 0058 POWELL STREET CA 0078 CENTURY CITY CA 0082 RANCHO CUCAMONGA CA 0088 FRESNO FASHION FAIR CA 0090 SANTA BARBARA CA 0104 BAKERSFIELD CA 0116 EMERYVILLE CA 0196 UNION STREET CA 0202 WALNUT CREEK CA 0206 NOVATO CA 0232 OTAY RANCH CA 0382 EMBARCADERO CA 0438 SAN LUIS OBISPO CA 0462 PACIFIC COMMONS CA 0484 MODESTO CA 0494 TEMECULA CA 0614 CALABASAS CA 0646 VALENCIA CA 0672 AMERICANA CA 0674 PALM DESERT CA 0740 MALIBU CA 0914 HUNTINGTON BEACH CA 0922 MARINA DEL REY CA 0928 BEVERLY DRIVE CA 0934 MONTEREY CA 0938 WESTLAKE CA 0946 THE GROVE CA 0958 SANTANA ROW CA 1118 RIVER PARK CA 1128 CORTE MADERA TOWN CENTER CA 1134 CONCORD CA 1138 UNIVERSAL CITY WALK CA 1144 STUDIO CITY CA 1150 CHINO HILLS CA 1158 TUSTIN MARKET PLACE CA 1166 PACIFIC PALISADES CA 1168 LAUREL VILLAGE CA 1172 DALY CITY CA 1176 ALISO VILLAGE CA 1190 FOLSOM CA 1192 SANTEE CA 1200 BERKELEY CA 1202 SAN FRANCISCO CENTRE CA 1218 PALM SPRINGS CA 1222 ONE PASEO CA 1230 IRVINE SPECTRUM CA 1236 REDLANDS CA 1240 BISHOP RANCH CA 1250 LONG BEACH CA 1268 SHOPPES AT -

State Store Hours State Store Hours Al Brookwood

ALL HOURS APPLY TO LOCAL TIME ZONES STATE STORE HOURS STATE STORE HOURS AL BROOKWOOD VILLAGE 5-9pm MO NORTHPARK (MO) 5-9pm AL RIVERCHASE GALLERIA 5-9pm MO THE SHOPPES AT STADIUM (MO) 5-9pm AZ SCOTTSDALE FASHION SQUARE 5-9pm MT BOZEMAN GALLATIN VALLEY (MT) 5-9pm AZ BILTMORE FASHION PARK 5-9pm MT HELENA NORTHSIDE CENTER (MT) 5-9pm AZ ARROWHEAD TOWNE CENTER 5-9pm NC CRABTREE VALLEY 5-9pm AZ CHANDLER FASHION CENTER 5-9pm NC STREETS AT SOUTHPOINT 5-9pm AZ PARADISE VALLEY (AZ) 5-9pm NC CROSS CREEK (NC) 5-9pm AZ TUCSON MALL 5-9pm NC FRIENDLY CENTER 5-9pm AZ TUCSON PARK PLACE 5-9pm NC NORTHLAKE (NC) 5-9pm AZ SANTAN VILLAGE 5-9pm NC SOUTHPARK (NC) 5-9pm CA CONCORD 5-9:30pm NC TRIANGLE TOWN CENTER 5-9pm CA CONCORD SUNVALLEY 5-9pm NC CAROLINA PLACE (NC) 5-9pm CA WALNUT CREEK BROADWAY PLAZA 5-9pm NC HANES 5-9pm CA SANTA ROSA PLAZA 5-9pm NC WENDOVER 5-9pm CA FAIRFIELD SOLANO 5-9pm ND WEST ACRES (ND) 5-9pm CA NORTHGATE (CA) 5-9pm ND COLUMBIA (ND) 5-9pm CA PLEASANTON STONERIDGE 5-9pm NH MALL OF NEW HAMPSHIRE 5-9:30pm CA MODESTO VINTAGE FAIR 5-9pm NH BEDFORD (NH) 5-9pm CA NEWPARK 5-9pm NH MALL AT ROCKINGHAM PARK 5-9:30pm CA STOCKTON SHERWOOD 5-9pm NH FOX RUN (NH) 5-9pm CA FRESNO FASHION FAIR 5-9pm NH PHEASANT LANE (NH) 5-9:30pm CA SHOPS AT RIVER PARK 5-9pm NJ MENLO PARK 5-9:30pm CA SACRAMENTO DOWNTOWN PLAZA 5-9pm NJ WOODBRIDGE CENTER 5-9:30pm CA ROSEVILLE GALLERIA 5-9pm NJ FREEHOLD RACEWAY 5-9:30pm CA SUNRISE (CA) 5-9pm NJ MONMOUTH 5-9:30pm CA REDDING MT. -

Taubman Declares Common and Preferred Dividends 9-3-15

Macerich T 310.394.6000 401 Wilshire Blvd. www.macerich.com Suite 700 Santa Monica, California 90401-1452 Taubman Centers, Inc. T 248.258.6800 200 East Long Lake Road www.taubman.com Suite 300 Bloomfield Hills, Michigan 48304 -2324 Taubman and Macerich to Acquire Country Club Plaza BLOOMFIELD HILLS, Mich., January 4, 2016 - - Taubman Centers, Inc. (NYSE: TCO) and The Macerich Company (NYSE: MAC) today announced an agreement to purchase Country Club Plaza (Kansas City, Mo.) from Highwoods Properties, Inc. (NYSE: HIW). The purchase price for the mixed-use retail and office property is $660 million cash, excluding transaction costs. Taubman and Macerich will each have a 50% interest in the center, which will be jointly managed by both companies. Concurrent with or shortly after closing, a long-term, fixed-rate loan for 50-60% of the purchase price is expected to be placed on the asset. “Taubman and Macerich are bringing our collective expertise together to continue to ensure the long-term growth and success of the iconic Country Club Plaza,” said Robert S. Taubman, chairman, president, and chief executive officer of Taubman Centers. “This purchase is consistent with our strategy to own high quality, dominant assets in great markets.” ”This investment represents the latest example of Macerich’s continuing strategy of recycling capital out of slower-growth assets, including Panorama Mall which we recently sold for $100 million, into truly irreplaceable, market-dominant centers with stronger growth prospects,” said Arthur Coppola, chairman and chief executive officer of Macerich. “Together with Taubman, we see opportunities to expand the market reach of the Plaza as well as the potential for further retail densification of this timeless asset.” The transaction has been approved by the Boards of Directors of Taubman and Macerich. -

Community Features in the Country Club District

Building Character and Distinction Community Features in the Country Club District Community features can and should be the means of giving character and distinction to your property; the things that create enthusiasm and a liking for the property by its residents; the things that cause your cli- ents and your owners in your property to enjoy living there. Community features … include the activities that bring residents … to- gether in any united purpose of pleasant or serious effort. On the other hand, it includes the character of the physical development of your property, its adornment, its characteristics — the very creation of an individual and an appealing personality in all or various parts of your property … These features may be the inspiration that causes a better Mary Rockwell Hook was Kansas City’s and more intensive development of every private lawn; an inspiration first significant female architect. Here for better architecture … the cause of the development of a greater in- she is pictured heading off to France in terest and love of one’s home … the cause for closer friendships, and a 1920 to work for the American Com- greater neighborhood and community spirit. They directly improve life mittee for Devastated France. Her work is in its noblest sense and lead to higher aspirations to obtain the things important but little known. See story on worthwhile in life — and in the end, from it all comes a greater love page 9. and respect for one’s city, a greater civic interest and pride, a better public spirit, and a greater patriotism for city and nation in the hearts of both young and old. -

Prime Locations for Lease

Prime locations for lease AVAILABLE IN URBAN MARKETS, SHOPPING CENTERS, FREESTANDING, OFFICE AND RESIDENTIAL LOCATIONS 2,400 – 3,933 sf FOR MORE INFORMATION: James Avallone Locations in: [email protected] Arkansas, Colorado, Florida, (516) 682-4224 Maryland, Missouri and Pennsylvania gordonbrothers.com/realestate Formerly operating under the DJM REAL ESTATE name since joining Gordon Brothers in 1998, we are now proudly under the Gordon Brothers name. ALL INFORMATION CONTAINED HEREIN WAS OBTAINED FROM SOURCES DEEMED RELIABLE. NO WARRANTIES OR REPRESENTATIONS, EXPRESSED OR IMPLIED, ARE MADE REGARDING THE ACCURACY OF THE INFORMATION CONTAINED HEREIN AND SUCH INFORMATION IS SUBMITTED SUBJECT TO ERRORS, OMISSIONS, PRIOR LEASE ASSIGNMENT, SUBLEASE AND/OR WITHDRAWAL WITHOUT NOTICE. ALTHOUGH THE COMPANY IS MARKETING ITS PROPERTIES INDIVIDUALLY, IT IS ALSO IN THE PROCESS OF CONSIDERING GOING CONCERN OFFERS FOR SOME OR ALL OF ITS STORES. ACCORDINGLY, THE COMPANY RESERVES THE RIGHT TO WITHDRAW ANY OR ALL OF ITS PROPERTIES FROM CONSIDERATION AND TO REJECT ANY OFFERS FOR INDIVIDUAL STORES. FOR ADDITIONAL INFORMATION CALL 516.628.4200 OR VISIT OUR WEBSITE AT WWW.GORDONBROTHERS.COM/REALESTATE Store Gross Address Local Broker Details # SF ARKANSAS 280 3,060 12900 Chenal Pkwy. Cynthia Lu Operating - Do not disturb Little Rock, AR 72211 Flake & Kelley 501-375-3200 286 3,130 Park Plaza Mall - Midtown Cynthia Lu Location Closed 6000 Markham St. Ste. 2030 Flake & Kelley Little Rock, AR 72205 501-375-3200 COLORADO 309 2,800 FlatIron Crossings Daniel M. Miller & Cameron Flint Operating - Do not disturb 1 Flatiron Crossings Dr. CBRE | Advisory Broomfield, CO 80021 303-264-1908 FLORIDA 302 2,800 Millenia Plaza (Orlando) Ross Waters Operating - Do not disturb 4723 Millenia Plaza Way Atlantic Retail Properties Orlando, FL 32839 561-424-3014 263 2,821 1670 W. -

Appendix D – Historic Properties Survey Technical Report

Environmental Assessment Appendix D – Historic Properties Survey Technical Report Kansas City Streetcar Main Street Extension Project SECTION 106 TECHNICAL REPORT MO SHPO PROJECT NUMBER 211-JA-18 Prepared for the Federal Transit Administration By Architectural & Historical Research, LLC, Kansas City, MO January 21, 2019 This page left intentionally blank TABLE OF CONTENTS Project Background 2 Introduction 3 Streetcar Description 4 Methods and Area of Potential Effect 6 Disposition of Records 9 Results 10 Mass Transit in Kansas City and The Metropolitan Area 10 The Appropriateness of Placing Light Rail on Kansas City’s Boulevards 22 Architectural and Historical Contexts 24 Main Street Development 24 West Pershing to Thirty-First Streets 27 Thirty-First Street to Thirty-Ninth Street 31 Thirty-Ninth Street to Forty-Third Street 35 Forty-Third Street to Forty-Seventh Street 38 Forty-Seventh Street to Fifty-First Street 41 Inventory of Resources Within the APE 46 Determination of Effect 65 Recommended Mitigation 66 Bibliography 67 Appendices Kansas City Downtown Streetcar Project Page | i Section 106 Historic Resources Technical Report January 21, 2019 PROJECT BACKGROUND The Kansas City Downtown Streetcar starter line began service on May 6, 2016. The 2.2-mile line has provided more than 4.9 million trips in the 2+ years since opening day (over twice the projections). Due to overwhelming support and enthusiastic public interest in extending the streetcar route, the City of Kansas City, Missouri, the Kansas City Area Transportation Authority (KCATA), and the Kansas City Streetcar Authority (KCSA) have formed a Project Team to develop Federal Transit Administration (FTA) Section 5309 Capital Investment Grant Program – New Starts project justification materials and data in support of extending the streetcar approximately 3.5 miles south from its current terminus at West Pershing Road. -

Missou St Uri Public Taff's Gas C Service S

Missouri Public Service Commission Staff’s Gas Incident Report 910 W 48th Street Kansas City, Missouri February 19, 2013 Missouri Gas Energy Case No. GS-2013-0400 Regulatory Review Division Tariff, Safety, Economic and Engineering Analysis Department Energy Infrastructure Reliability Unit February 6, 2014 Jefferson City, Missouri 1 TABLE OF CONTENTS 2 I. EXECUTIVE SUMMARY ....................................................................................................................... 1 3 II. SYNOPSIS OF INCIDENT ..................................................................................................................... 4 4 III. STAFF ANALYSIS OF INCIDENT AND CONCLUSIONS .............................................................. 9 5 A. Locating and Marking Natural Gas Main and Electric Lines .............................................................. 9 6 B. Third-Party Damage to Natural Gas Main ......................................................................................... 12 7 C. Natural Gas Escape and Migration .................................................................................................... 14 8 D. Natural Gas Entrance, Accumulation, and Ignition ........................................................................... 16 9 E. MGE’s Emergency Response and Actions Prior the Explosion ......................................................... 17 10 F. Locate Marks near the Damaged Main ............................................................................................... 25 -

Saint Luke's Patient Information & Visitor Guide

SAINT LUKE’S PATIENT INFORMATION & VISITOR GUIDE Saint Luke’s Hospital A CON Y ON NECTION YOU CAN REL s a close affiliate of Saint Luke’s Health System, you can trust Bishop Spencer Place to provide a quality continuum of care in our distinctive retirement living setting just off the Country Club Plaza. Just two blocks from Saint Luke’s Hospital, we’re in a unique position to understand your needs, maintain communications and coordinate care. What’s EDI CAR E more, our Medical Director – Dr. Peter Holt – is a board-certified 5 MA E geriatrician and member of the Saint Luke’s medical staff. - S T R Whether you or a loved one needs short-term rehab, A A R C long-term skilled nursing, assisted living or independent living, RA TE D you’ll feel confident that our faith-based, not-for-profit retirement community is well-connected to serve you. For more information, please call Mendi at (816) 595-5878 or visit us online. Our return-to-home success rate and hospital readmission rate consistently trend better than the national averages. 4301 Madison Ave. l Kansas City, MO 64111 www.BishopSpencerPlace.org For information call (816) 595-5878 THE PLACE T O BE FOR RET IREMENT LIVING TABLE OF Our Mission CONTENTS Saint Luke’s Hospital of Kansas City is a faith- Welcome........................................ 04 based, not-for-profit tertiary care hospital Patient Information......................... 05 committed to the high- est levels of excellence Parking/Valet Parking..................... 06 in providing health care and health services Your Health Care Team..................