U.S. Customs Service

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Kowloon West Job Fair 2019

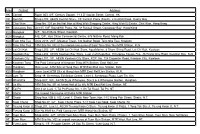

Kowloon West Job Fair Date: 15 & 16 August 2019 (Thursday and Friday) Time: 11:00 a.m. – 5:30 p.m. (Last admission at 5:00 p.m.) Venue: Atrium 1/F, Dragon Centre (37 K, Yen Chow Street, Sham Shui Po, Kowloon; MTR Sham Shui Po Station, Exit C1) Employers conduct on-the-spot recruitment of over 3 200 vacancies! Different participating organisations on each day! Free admission! Welcome to join! You can get a souvenir for joining the event while stock lasts! Subscribe for latest information on large-scale job fairs at “MyGovHK” (www.gov.hk/mygovhk/en)! 15 August 2019 (Thursday) Participating Organisation Job Vacancy Location Cheung Sha Wan , Ho Man Nixon Cleaning Company Limited Cleaner Tin , Hung Hom , Sham Shui Po Dussmann Service Hong Kong Building Attendant /Security Guard Cheung Sha Wan Limited (Night Shift) Dormitory Security Guard (Night Shift) Kennedy Town Mall Security Guard (Day/Night Shift) Kwun Tong Residential Security Guard Mid-level (Day/Night Shift) Residential Security Guard (Night Shift) Happy Valley Security Guard (Day/Night Shift) Pokfulam Hospital Cleaner Tseung Kwan O Red Cross Security Yau Ma Tei (Evening/Night Shift) Hong Kong Housing Society Senior Building Attendant Diamond Hill Senior Technician Hung Hom , To Kwa Wan Technician I Hung Hom , Tuen Mun Kwai Chung , Shatin , Yau Building Supervisor Ma Tei Technician I (plumbing & drainage) Ngau Tau Kok 1 Participating Organisation Job Vacancy Location Hong Kong Housing Society Customer Services Officer North Point (Leasing)(11-Month) Control Centre Officer North Point Personal Care Worker (11-month) Tseung Kwan O Personal Care Worker North Point Beyond Korea Limited Waiter/ Waitress (Full-time/Part-time) Anywhere in H.K. -

Public Housing Development at Lai Chi Kok Road-Tonkin Street DATE of PREPARATION June 2018

PLANNING BRIEF PROJECT NAME Public Housing Development at Lai Chi Kok Road-Tonkin Street DATE OF PREPARATION June 2018 1. Site Particulars Current Proposal Remarks 1.1 District Location Sham Shui Po 1.2 Site Location Adjoining Lai Chi Kok Road and Tonkin Street 1.3 Site Area Subject to detailed survey and Gross [ha] 2.34 finalisation of design layout. Net [ha] 2.34 A portion of the site at the junction of Lai Chi Kok Road and Tonkin Street would be carved out for construction of a public lift as agreed with TD, HyD, CEDD and LandsD. 1.4 Existing Land Use Construction site for public housing development 1.5 Existing Zoning Residential (Group A) Approved Cheung Sha Wan OZP No. S/K5/37 gazetted in Dec 2016. 1.6 Existing Land Status Government Land Held by Hong Kong Housing Authority under the Short Term Tenancy (STT) No. KX 2953. 2. Development Parameters Current Proposal Remarks 2.1 Proposed Housing Type Public Housing 2.2 Proposed No. of Flats (about) 3,859 Based on max. building height (Phase 1 - 2,545 of 120mPD. Phase 2 - 1,314) Preliminary scheme subject to detailed architectural feasibility study and ±10% variation should be allowed for design flexibility. Design population based on flat mix. 2.3 Design Population (about) 11,750 2.4 Maximum Gross Floor Area 175,134 Max. GFA calculation based (GFA) on plot ratio to be adopted. Domestic [m2] About 169,125 Non-domestic [m2] About 6,009 2. Development Parameters (Con’t) Current Proposal Remarks 2.5 Maximum Plot Ratio 7.5 overall Based on net site area. -

Office Address of the Labour Relations Division

If you wish to make enquiries or complaints or lodge claims on matters related to the Employment Ordinance, the Minimum Wage Ordinance or contracts of employment with the Labour Department, please approach, according to your place of work, the nearby branch office of the Labour Relations Division for assistance. Office address Areas covered Labour Relations Division (Hong Kong East) (Eastern side of Arsenal Street), HK Arts Centre, Wan Chai, Causeway Bay, 12/F, 14 Taikoo Wan Road, Taikoo Shing, Happy Valley, Tin Hau, Fortress Hill, North Point, Taikoo Place, Quarry Bay, Hong Kong. Shau Ki Wan, Chai Wan, Tai Tam, Stanley, Repulse Bay, Chung Hum Kok, South Bay, Deep Water Bay (east), Shek O and Po Toi Island. Labour Relations Division (Hong Kong West) (Western side of Arsenal Street including Police Headquarters), HK Academy 3/F, Western Magistracy Building, of Performing Arts, Fenwick Pier, Admiralty, Central District, Sheung Wan, 2A Pok Fu Lam Road, The Peak, Sai Ying Pun, Kennedy Town, Cyberport, Residence Bel-air, Hong Kong. Aberdeen, Wong Chuk Hang, Deep Water Bay (west), Peng Chau, Cheung Chau, Lamma Island, Shek Kwu Chau, Hei Ling Chau, Siu A Chau, Tai A Chau, Tung Lung Chau, Discovery Bay and Mui Wo of Lantau Island. Labour Relations Division (Kowloon East) To Kwa Wan, Ma Tau Wai, Hung Hom, Ho Man Tin, Kowloon City, UGF, Trade and Industry Tower, Kowloon Tong (eastern side of Waterloo Road), Wang Tau Hom, San Po 3 Concorde Road, Kowloon. Kong, Wong Tai Sin, Tsz Wan Shan, Diamond Hill, Choi Hung Estate, Ngau Chi Wan and Kowloon Bay (including Telford Gardens and Richland Gardens). -

Continuous Measurements at the Urban Roadside in an Asian

Continuous measurements at the urban roadside in an Asian megacity by Aerosol Chemical Speciation Monitor (ACSM) Particulate matter characteristics during fall and winter seasons in Hong Kong Sun, C.; Lee, B. P.; Huang, D.; Jie Li, Y.; Schurman, M. I.; Louie, P. K K; Luk, C.; Chan, C. K. Published in: Atmospheric Chemistry and Physics Published: 15/02/2016 Document Version: Final Published version, also known as Publisher’s PDF, Publisher’s Final version or Version of Record License: CC BY Publication record in CityU Scholars: Go to record Published version (DOI): 10.5194/acp-16-1713-2016 Publication details: Sun, C., Lee, B. P., Huang, D., Jie Li, Y., Schurman, M. I., Louie, P. K. K., Luk, C., & Chan, C. K. (2016). Continuous measurements at the urban roadside in an Asian megacity by Aerosol Chemical Speciation Monitor (ACSM): Particulate matter characteristics during fall and winter seasons in Hong Kong. Atmospheric Chemistry and Physics, 16(3), 1713-1728. https://doi.org/10.5194/acp-16-1713-2016 Citing this paper Please note that where the full-text provided on CityU Scholars is the Post-print version (also known as Accepted Author Manuscript, Peer-reviewed or Author Final version), it may differ from the Final Published version. When citing, ensure that you check and use the publisher's definitive version for pagination and other details. General rights Copyright for the publications made accessible via the CityU Scholars portal is retained by the author(s) and/or other copyright owners and it is a condition of accessing these publications that users recognise and abide by the legal requirements associated with these rights. -

Kowloon P P P

Branch ATM District Branch / ATM Address Voice Navigation ATM Prince Edward Branch 774 Nathan Road, Kowloon P P P Fuk Tsun Street Branch 32-40 Fuk Tsun Street, Tai Kok Tsui, Kowloon P P P P 4-4A Humphrey's Avenue, Tsim Sha Tsui, Humphrey's Avenue Branch P P Kowloon Mong Kok (Silvercorp Int'l Tower) Shop B, 707-713 Nathan Road, Mong Kok, P P P P Branch Kowloon 1/F, Sino Cheer Plaza, 23-29 Jordan Road, Jordan Road Branch P P Kowloon Mong Kok Branch 589 Nathan Road, Mong Kok, Kowloon P P Prince Edward Road West (Mong Kok) 116-118 Prince Edward Road West, Mong P P Branch Kok, Kowloon 24-28 Carnarvon Road, Tsim Sha Tsui, Tsim Sha Tsui Branch P P Kowloon Shanghai Street (Prince Edward) 689-693 Shanghai Street, Mong Kok, Kowloon P P Branch 73-77 Tai Kok Tsui Road, Tai Kok Tsui, Tai Kok Tsui Branch P P P P Kowloon Shop 19-20, 2/F, China Hong Kong City, 33 China Hong Kong City Branch P P Canton Road, Tsim Sha Tsui , Kowloon Mong Kok Road Branch 50-52 Mong Kok Road, Mong Kok, Kowloon P P P Shop 133, 1/F, Olympian City 2, 18 Hoi Ting Olympian City Branch P P Road, Kowloon Apartments A-B on G/F & 1/F, Holly Mansion, Kimberley Road Branch P P P P 37 Kimberley Road, Tsim Sha Tsui, Kowloon. Shop 1003-1004, 1/F, Elements, 1 Austin Road Elements Branch P P P West, Kowloon Mong Kok (President Commercial 608 Nathan Road, Mong Kok, Kowloon P P P Centre) Branch Yau Ma Tei Branch 471 Nathan Road, Yau Ma Tei, Kowloon P P P Shop 3,LG/F,Hilton Towers,96 Granville Tsim Sha Tsui East Branch P P Road,Tsim Sha Tsui East, Kowloon Cameron Road Wealth Management 30 -

ATM with Barrier-Free Facilities(As at 31 Mar 2021)

ATM with barrier-free facilities(As at 31 Mar 2021) adjusted Voice Region ATM Name Adress height-of-reach navigation Hong Kong West Point Branch ATM 242-244 Queen’s Road West, Sai Ying Pun, Hong Kong √ island Hong Kong West Point Personal Banking Shop 2, G/F, 345 - 345A Des Voeux Road West, Hong Kong √ island Centre ATM Hong Kong Shop F, G/F, Kai Tak Commercial Building, Sheung Wan Branch ATM √ island 317-319 Des Voeux Road Central, Sheung Wan, Hong Kong Hong Kong Basement, Ground Floor and First Floor of 122 QRC, Nos. Queen's Road Central Branch √ island 122-126 Queen's Road Central, Hong Kong Hong Kong Central Branch ATM#1 1/F., 9 Queen’s Road Central, Hong Kong √ √ island Hong Kong ICBC Tower (lobby) ATM Lobby, ICBC Tower, 3 Garden Road, Central, Hong Kong √ √ island Hong Kong Caine Road Branch ATM G/F., Caine Building, 22 Caine Road, Hong Kong √ island Hong Kong Wan Chai Branch ATM#2 117-123 Hennessy Road, Wanchai, Hong Kong ATM#2 √ island Hong Kong Wan Chai Road Branch G/F Times Media Centre, No.133 Wan Chai Road, Hong √ island ATM#2 Kong ATM#2 Hong Kong Shop 101, 1/F, China Resources Building, 26 Harbour Road, Siu Sai Wan Branch ATM √ island Wanchai, Hong Kong Hong Kong Causeway Bay Branch Shop A on G/F, 1/F, Hennessy Apartments, 488 & 490 √ √ island ATM#2 Hennessy Road, Hong Kong ATM#2 Hong Kong Causeway Bay Branch Shop A on G/F, 1/F, Hennessy Apartments, 488 & 490 √ island ATM#3 Hennessy Road, Hong Kong ATM#3 Hong Kong Happy Valley Branch ATM 23 King Kwong Street, Happy Valley, Hong Kong √ island Hong Kong Electric Road Branch -

Shop 123, 1St Floor, Peninsula Centre, 67 Mody Road, Tsim Sha Tsui East, Kowloon

NO NAME ADDRESS TELP FAX 1 A Maids Employment Services Centre Shop 123, 1st Floor, Peninsula Centre, 67 Mody Road, Tsim Sha Tsui East, Kowloon. 2111 3319 3102 9909 2 A.V.M.S Limited Shop L115, 1st floor, Metro Harbour Plaza, Tai Kok Tsui, Kowloon 3144 3367 3144 3962 3 Abadi Employment Consultant Centre Room 1108, 1st floor, Inciti Kar Shing Building, 15-19 Kau Yuk Road, Yuen Long, New Territories 3106 5716 3106 5717 4 ABNC Employment Agencies Co. Flat 79, Ground floor, Maximall, Blocks 1-3, City Garden, 233 Electric Road, North Point, Hong Kong. 25762911 25763600 5 Active Global Specialised Caregivers (HK) Pte Ltd. Unit 1703-04, 17th floor, Lucky Centre, 165-171 Wan Chai Road, Wan Chai, Hong Kong 3426 2909 3013 9815 6 Advance Court Overseas Employment Co. Shop 34B, Level 2, Waldorf Shopping Centre, Castle Peak Road, TMTL 194, Tuen Mun, New Territories 2458 1573 2452 6735 7 Advantage Consultant Co. Flat C, 12th FIoor, Kam Wah Building, 516 Nathan Road, Yau Ma Tei, Kowlon 26012708 27711420 8 AIE Employment Centre Room 1605, 16th floor, Hollywood Plaza, 610 Nathan Road, Mong Kok, Kowloon 2770 1198 2388 9057 9 Alim Prima Employment Agency Room K & L, 4th floor, Hennessy Apartments, 488 Hennessy Road, Causeway Bay, Hong Kong 25040629 27709803 10 All The Best Employment Limited. 1st floor, 92 Kam Tin Road, Yuen Long, New Territories 2807 0870 2807 0869 11 Allwin Employment Centre Limited Mezzanine floor, 408 Ma Tau Wau Road, Hung Hom, Kowloon 28668585 28669595 12 An Apple Travel & Employment Services Limited Room 907, 9th floor, Tower 2, Silvercord, -

Aeon Atm Rmb Service.Pdf

Area District Address HK Central Room 803, 8/F, Century Square, 1-13 D' Aguilar Street, Central, HK HK Kornhill Shop L108, AEON Kornhill Store, 1/F Kornhill Plaza (South), 2 Kornhill Road, Quarry Bay HK Chai Wan Shop No. 128 on the first floor of Hing Wah Shopping Centre, Hing Wah (I) Estate, Chai Wan, Hong Kong HK Causeway Bay Unit 05 10/F SoundWill Plaza, No. 38 Russell Street, Causeway Bay, Hong Kong KLN Mongkok G/F., No.43 Bute Street, Kowloon KLN Mongkok A-B, G/F, Hua Chiao Commercial Centre, 678 Nathan Road, Mong Kok KLN Tsim Sha Tsui Units 2018, 20/F, Miramar Tower, 132 Nathan Road, Tsim Sha Tsui, Kowloon KLN Tsim Sha Tsui ATM Site No. M2 at the unpaid concourse of East Tsim Sha Tsui MTR Station, KLN KLN Lai Chi Kok Shop L203, 2/F, AEON Lai Chi Kok Store, AquaMarine, 8 Sham Shing Road, Lai Chi Kok, Kowloon KLN Kowloon Bay Shop L204, AEON Kowloon Bay Store, Level 2 of Mega Box, Enterprise Square Five, 38 Wang Chiu Road, Kowloon Bay, KLN KLN Kowloon City Shop L301, 3/F, AEON Kowloon City Store, KCP, No. 128 Carpenter Road, Kowloon City, Kowloon KLN Kowloon Tong The Paid Concourse of Kowloon Tong MTR Station, East Rail Line KLN Hunghom Main Level, ATM Site at Hung Hom MTR East Rail Line Station, KLN. KLN Hunghom Lower Level,ATM Site at Hung Hom MTR East Rail Line Station, KLN. KLN Lam Tin Shop 19, Sceneway Exhibition Centre, Level 3, Sceneway Plaza, Lam Tin, Kln. -

MTR Corporation Limited Mass Transit Railway – Lai Chi Kok Station Cheung Lai Street Pedestrian Subway and Entrances Works Project Profile

MTR Corporation Limited Mass Transit Railway – Lai Chi Kok Station Cheung Lai Street Pedestrian Subway and Entrances Works Project Profile Black MTR Corporation Limited Mass Transit Railway - Lai Chi Kok Station Cheung Lai Street Pedestrian Subway and Enances Works Project Profile November 2005 Ove Arup & Partners Hong Kong Ltd Level 5, Festival Walk, 80 Tat Chee Avenue, Kowloon Tong, Kowloon, Hong Kong Tel +852 2528 3031 Fax +852 2268 www.arup.com Job number 24152 MTR Corporation Limited Mass Transit Railway – Lai Chi Kok Station Cheung Lai Street Pedestrian Subway and Entrances Works Project Profile CONTENTS Page 1. BASIC INFORMATION 1 1.1 Project Title 1 1.2 Project Description 1 1.3 Nature of the Project, and the Proposed Addition, Modification Or Alternation 1 1.4 Name of Project Proponent 2 1.5 Location of the Project 2 1.6 Name and Telephone Number of Contact Person(s) 2 1.7 Proposed Addition, Modification Or Alternation 2 1.8 Time-Table for the Addition, Modification Or Alternation 3 2. POSSIBLE IMPACT ON THE ENVIRONMENT 4 2.1 Major Elements of The Surrounding Environment 4 2.2 Noise 5 2.3 Air Quality 9 2.4 Water Quality 9 2.5 Waste Management 10 3. DESCRIPTIONS OF MITIGATION MEASURES 10 3.1 Noise 10 3.2 Air Quality 11 3.3 Water Quality 11 3.4 Waste Management 11 3.5 Environmental Monitoring and Audit (EM&A) Requirements 12 4. USE OF PREVIOUSLY APPROVED EIA REPORTS 12 5. CONCLUSIONS 12 MTR Corporation Limited Mass Transit Railway – Lai Chi Kok Station Cheung Lai Street Pedestrian Subway and Entrances Works Project Profile FIGURES -

Design and Planning of Lai Chi Kok Transfer Scheme, Hong Kong

DESIGN AND PLANNING OF LAI CHI KOK TRANSFER SCHEME, HONG KONG Alan W.C. Ip 1, Eddie W.C. Lam 1, Peter, C.W. Cheung 1 1Drainage Services Department, Government of Hong Kong SAR, China KEYWORDS drainage tunnel, TBM, risk management ABSTRACT The Lai Chi Kok Transfer Scheme comprising a 4.9m finished diameter, 3.7km long drainage tunnel with associated intake/outlet shafts and connection adits was initiated by the Government of Hong Kong Special Administrative Region to reduce flood risk in a dense urban area. The project involves construction of two TBM tunnels through hard rock stratum with a number of transverse fault zones, and mixed ground under high ground water table. Along the tunnel alignment are existing buildings, railway lines, major trunk roads and highway viaducts at a minimal clearance. This paper provides an overview of the site conditions and constraints, selection of tunnel alignment and TBMs, and resolution with stakeholders on land and technical issues. Protection of existing structures/utilities, design considerations, hybrid design-and-build contract with re-measurement provisions for control of groundwater infiltration, risk management and adoption of geotechnical baseline report will also be discussed. INTRODUCTION Rapid urbanization and changes in land use in the developed districts of Sham Shui Po, Cheung Sha Wan and Lai Chi Kok over the past decades have turned natural ground and slopes into paved and impermeable areas. During heavy rainstorms, large quantity of surface run-off from the hinterland and the overflow from Kowloon group of reservoirs will flow into the downstream urban areas and overload the existing drainage systems. -

Consumption Voucher Scheme-Locations with Drop-Box

Consumption Voucher Scheme Locations with drop-box for collection of paper registration forms The Hongkong and Shanghai Banking Corporation Number Location Bank Branch Branch Address 1 HK Causeway Bay Branch Basement 1 and Shop G08, G/F, Causeway Bay Plaza 2, 463-483 Lockhart Road, Causeway Bay, Hong Kong 2 HK Happy Valley Branch G/F, Sun & Moon Building, 45 Sing Woo Road, Happy Valley, Hong Kong 3 HK Hopewell Centre Branch Shop 2A, 2/F, Hopewell Centre, 183 Queen's Road East, Wan Chai, Hong Kong 4 HK Park Lane Branch Shops 1.09 - 1.10, 1/F, Style House, Park Lane Hotel, 310 Gloucester Road, Causeway Bay, Hong Kong 5 HK Sun Hung Kai Centre Shops 115-117 & 127-133, 1/F, Sun Hung Branch Kai Centre, 30 Harbour Road, Wan Chai, Hong Kong 6 HK Central Branch Basement, 29 Queen's Road Central, Central, Hong Kong 7 HK Exchange Square Branch Shop 102, 1/F, Exchange Square Podium, Central, Hong Kong 8 HK Hay Wah Building Branch Hay Wah Building, 71-85 Hennessy Road, Wan Chai, Hong Kong 9 HK Hong Kong Office Level 3, 1 Queen's Road Central, Central, Hong Kong 10 HK Chai Wan Branch Shop No. 1-11, Block B, G/F, Walton Estate, Chai Wan, Hong Kong 11 HK Cityplaza Branch Unit 065, Cityplaza I, Taikoo Shing, Quarry Bay, Hong Kong 12 HK Electric Road Branch Shop A2, Block A, Sea View Estate, Watson Road, North Point, Hong Kong 13 HK Island Place Branch Shop 131 - 132, Island Place, 500 King's Road, North Point, Hong Kong 14 HK North Point Branch G/F, Winner House, 306-316 King's Road, North Point, Hong Kong 15 HK Quarry Bay Branch G/F- 1/F, 971 King's Road, -

二零一七熱帶氣旋tropical Cyclones in 2017

=> TALIM TRACKS OF TROPICAL CYCLONES IN 2017 <SEP (), ! " Daily Positions at 00 UTC(08 HKT), :; SANVU the number in the symbol represents <SEP the date of the month *+ Intermediate 6-hourly Positions ,')% Super Typhoon NORU ')% *+ Severe Typhoon JUL ]^ BANYAN LAN AUG )% Typhoon OCT '(%& Severe Tropical Storm NALGAE AUG %& Tropical Storm NANMADOL JUL #$ Tropical Depression Z SAOLA( 1722) OCT KULAP JUL HAITANG JUL NORU( 1705) JUL NESAT JUL MERBOK Hong Kong / JUN PAKHAR @Q NALGAE(1711) ,- AUG ? GUCHOL AUG KULAP( 1706) HATO ROKE MAWAR <SEP JUL AUG JUL <SEP T.D. <SEP @Q GUCHOL( 1717) <SEP T.D. ,- MUIFA TALAS \ OCT ? HATO( 1713) APR JUL HAITANG( 1710) :; KHANUN MAWAR( 1716) AUG a JUL ROKE( 1707) SANVU( 1715) XZ[ OCT HAIKUI AUG JUL NANMADOL AUG NOV (1703) DOKSURI JUL <SEP T.D. *+ <SEP BANYAN( 1712) TALAS(1704) \ SONCA( 1708) JUL KHANUN( 1720) AUG SONCA JUL MERBOK (1702) => OCT JUL JUN TALIM( 1718) / <SEP T.D. PAKHAR( 1714) OCT XZ[ AUG NESAT( 1709) T.D. DOKSURI( 1719) a JUL APR <SEP _` HAIKUI( 1724) DAMREY NOV NOV de bc KAI-( TAK 1726) MUIFA (1701) KIROGI DEC APR NOV _` DAMREY( 1723) OCT T.D. APR bc T.D. KIROGI( 1725) T.D. T.D. JAN , ]^ NOV Z , NOV JAN TEMBIN( 1727) LAN( 1721) TEMBIN SAOLA( 1722) DEC OCT DEC OCT T.D. OCT de KAI- TAK DEC 更新記錄 Update Record 更新日期: 二零二零年一月 Revision Date: January 2020 頁 3 目錄 更新 頁 189 表 4.10: 二零一七年熱帶氣旋在香港所造成的損失 更新 頁 217 附件一: 超強颱風天鴿(1713)引致香港直接經濟損失的 新增 估算 Page 4 CONTENTS Update Page 189 TABLE 4.10: DAMAGE CAUSED BY TROPICAL CYCLONES IN Update HONG KONG IN 2017 Page 219 Annex 1: Estimated Direct Economic Losses in Hong Kong Add caused by Super Typhoon Hato (1713) 二零一 七 年 熱帶氣旋 TROPICAL CYCLONES IN 2017 2 二零一九年二月出版 Published February 2019 香港天文台編製 香港九龍彌敦道134A Prepared by: Hong Kong Observatory 134A Nathan Road Kowloon, Hong Kong © 版權所有。未經香港天文台台長同意,不得翻印本刊物任何部分內容。 ©Copyright reserved.