Sandstorm Gold Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rhodochrosite Gems Unstable Colouration of Padparadscha-Like

Volume 36 / No. 4 / 2018 Effect of Blue Fluorescence on the Colour Appearance of Diamonds Rhodochrosite Gems The Hope Diamond Unstable Colouration of in London Padparadscha-like Sapphires Volume 36 / No. 4 / 2018 Cover photo: Rhodochrosite is prized as both mineral specimens and faceted stones, which are represented here by ‘The Snail’ (5.5 × 8.6 cm, COLUMNS from N’Chwaning, South Africa) and a 40.14 ct square-cut gemstone from the Sweet Home mine, Colorado, USA. For more on rhodochrosite, see What’s New 275 the article on pp. 332–345 of this issue. Specimens courtesy of Bill Larson J-Smart | SciAps Handheld (Pala International/The Collector, Fallbrook, California, USA); photo by LIBS Unit | SYNTHdetect XL | Ben DeCamp. Bursztynisko, The Amber Magazine | CIBJO 2018 Special Reports | De Beers Diamond ARTICLES Insight Report 2018 | Diamonds — Source to Use 2018 The Effect of Blue Fluorescence on the Colour 298 Proceedings | Gem Testing Appearance of Round-Brilliant-Cut Diamonds Laboratory (Jaipur, India) By Marleen Bouman, Ans Anthonis, John Chapman, Newsletter | IMA List of Gem Stefan Smans and Katrien De Corte Materials Updated | Journal of Jewellery Research | ‘The Curse Out of the Blue: The Hope Diamond in London 316 of the Hope Diamond’ Podcast | By Jack M. Ogden New Diamond Museum in Antwerp Rhodochrosite Gems: Properties and Provenance 332 278 By J. C. (Hanco) Zwaan, Regina Mertz-Kraus, Nathan D. Renfro, Shane F. McClure and Brendan M. Laurs Unstable Colouration of Padparadscha-like Sapphires 346 By Michael S. Krzemnicki, Alexander Klumb and Judith Braun 323 333 © DIVA, Antwerp Home of Diamonds Gem Notes 280 W. -

Page 1 of 2 Reporting Issuer List - Cover Page

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page Reporting Issuers Default When a reporting issuer is noted in default, standardized codes (a number and, if applicable a letter, described in the legend below) will be appear in the column 'Nature of Default'. Every effort is made to ensure the accuracy of this list. A reporting issuer that does not appear on this list or that has inappropriately been noted in default should contact the Alberta Securities Commission (ASC) promptly. A reporting issuer’s management or insiders may be subject to a Management Cease Trade Order, but that order will NOT be shown on the list. Legend 1. The reporting issuer has failed to file the following continuous disclosure document prescribed by Alberta securities laws: (a) annual financial statements; (b) an interim financial report; (c) an annual or interim management's discussion and analysis (MD&A) or an annual or interim management report of fund performance (MRFP); (d) an annual information form; (AIF); (e) a certification of annual or interim filings under National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109); (f) proxy materials or a required information circular; (g) an issuer profile supplement on the System for Electronic Disclosure By Insiders (SEDI); (h) a material change report; (i) a written update as required after filing a confidential report of a material change; (j) a business acquisition report; (k) the annual oil and gas disclosure prescribed by National Instrument -

Minerals of the San Luis Valley and Adjacent Areas of Colorado Charles F

New Mexico Geological Society Downloaded from: http://nmgs.nmt.edu/publications/guidebooks/22 Minerals of the San Luis Valley and adjacent areas of Colorado Charles F. Bauer, 1971, pp. 231-234 in: San Luis Basin (Colorado), James, H. L.; [ed.], New Mexico Geological Society 22nd Annual Fall Field Conference Guidebook, 340 p. This is one of many related papers that were included in the 1971 NMGS Fall Field Conference Guidebook. Annual NMGS Fall Field Conference Guidebooks Every fall since 1950, the New Mexico Geological Society (NMGS) has held an annual Fall Field Conference that explores some region of New Mexico (or surrounding states). Always well attended, these conferences provide a guidebook to participants. Besides detailed road logs, the guidebooks contain many well written, edited, and peer-reviewed geoscience papers. These books have set the national standard for geologic guidebooks and are an essential geologic reference for anyone working in or around New Mexico. Free Downloads NMGS has decided to make peer-reviewed papers from our Fall Field Conference guidebooks available for free download. Non-members will have access to guidebook papers two years after publication. Members have access to all papers. This is in keeping with our mission of promoting interest, research, and cooperation regarding geology in New Mexico. However, guidebook sales represent a significant proportion of our operating budget. Therefore, only research papers are available for download. Road logs, mini-papers, maps, stratigraphic charts, and other selected content are available only in the printed guidebooks. Copyright Information Publications of the New Mexico Geological Society, printed and electronic, are protected by the copyright laws of the United States. -

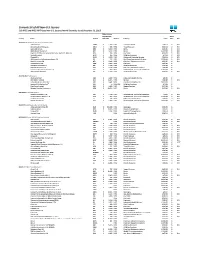

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Lower Applegate Area

... (26) ELDER MANGANESE LOWER APPLEGATE AREA Rhodonite ore with some rhodochrosite and hard manganese oxides in fracture planes occurs in a black, siliceous, metamorphosed sediment. The rock may be cobbed to show fairly large pieces of deep pink rhodonite. From the standpoint of metallurgical manganese ore, the prospect shows little promise. Authority: FWL (?) Department report Owner: J. R. Elder(?) Location: Sec. 6, T. 39 S., R. 5 W., south of Mungers Creek. Geology: "The rocks of the locality are old, highly metamorphosed sediments." n'l'he only opening -~he deposit is an opencut about 10 ft. long with a face about 8 ft. high, all in a black, siliceous, metamorphosed sediment, into which eydrothermal solutions have penetrated, depositing quartz, rhodonite and a small amount of rhodochrosite in irregular small seams and lenses. A thin\. coating of hard manganese oxides covers some fracture planes, and a little soft black oxide occurs in joint cracks near the surface." "The rock may be cobbed to show fairly large pieces of deep pink rhodonite, and several hundred pounds has been sold to collectors and lapidaries. The work done on the deposit has been to obtain rhodonite for this purpose". "The surface indicttes a considerable area of similar country rock, and probably trenching would show a greuter extent of the rhodonite oc currence. From the standpoint of producing a metallurgical manganese ore, however, the prospect shows little promise." SITE NP.ME: ELDER MANGANESE COUNTY: JOSEPHINE SYNONYMS: OWNER: LOCATION: MINING DIS:LOWER APPLEGATE BLM FS DIS: QUADl: GR.ANTS PASS SCALE: 100000 TOWNSHIP:039S QUAD2: OREGON CAVES SCALE: 62500 R.ANGE:005W RIVER BASIN:17 SECTION:06 PHYSIOG: 13 KLAMATH MOUNTAINS SECT FRACT:S USGS NUM: M013351 LAT:42-12-22N DOGAMI MLR: LONG:123-20-21W REPORTER: LEE, W UTM N:4672500 AFFILIATION: USGS UTM E:472000 REP DATE: 74 01 UTM Z:+10 UPDATE BY: FERNS, MARK L. -

Characterisation of Carbonate Minerals from Hyperspectral TIR Scanning Using Features at 14 000 and 11 300 Nm

Australian Journal of Earth Sciences An International Geoscience Journal of the Geological Society of Australia ISSN: 0812-0099 (Print) 1440-0952 (Online) Journal homepage: http://www.tandfonline.com/loi/taje20 Characterisation of carbonate minerals from hyperspectral TIR scanning using features at 14 000 and 11 300 nm D. Green & M. Schodlok To cite this article: D. Green & M. Schodlok (2016): Characterisation of carbonate minerals from hyperspectral TIR scanning using features at 14 000 and 11 300 nm, Australian Journal of Earth Sciences, DOI: 10.1080/08120099.2016.1225601 To link to this article: http://dx.doi.org/10.1080/08120099.2016.1225601 Published online: 13 Nov 2016. Submit your article to this journal Article views: 13 View related articles View Crossmark data Full Terms & Conditions of access and use can be found at http://www.tandfonline.com/action/journalInformation?journalCode=taje20 Download by: [Bundesstalt Fuer Geowissenschaften] Date: 21 November 2016, At: 02:06 AUSTRALIAN JOURNAL OF EARTH SCIENCES, 2016 http://dx.doi.org/10.1080/08120099.2016.1225601 Characterisation of carbonate minerals from hyperspectral TIR scanning using features at 14 000 and 11 300 nm D. Greena and M. Schodlokb aMineral Resources Tasmania, Department of State Growth, Hobart, Australia; bBundesanstalt fur€ Geowissenschaften und Rohstoffe (Federal Institute for Geosciences and Natural Resources), Hannover, Germany ABSTRACT ARTICLE HISTORY Rapid characterisation of carbonate phases in hyperspectral reflectance spectra acquired from drill Received 11 February 2016 core material has important implications for mineral exploration and resource modelling. Major Accepted 9 August 2016 infrared active features of carbonates lie in the thermal region around 6500 nm, 11 300 nm and KEYWORDS 14 000 nm, with the latter two features being most useful for differentiating mineral species. -

Dissolution and Solubility of Calcite-Rhodochrosite Solid Solutions

Zhu et al. Geochem Trans (2021) 22:1 https://doi.org/10.1186/s12932-021-00075-1 Geochemical Transactions RESEARCH ARTICLE Open Access Dissolution and solubility of calcite-rhodochrosite solid solutions [(Ca1-xMnx)CO3] at 25 °C Yinian Zhu1* , Peijie Nong1, Nan Mo1, Zongqiang Zhu2,3*, Huan Deng1, Shen Tang2, Hongqu Yang1, Lihao Zhang2 and Xingxing Wang1 Abstract A complete series of calcite-rhodochrosite solid solutions [(Ca1-xMnx)CO3] are prepared, and their dissolution pro- cesses in various water samples are experimentally investigated. The crystal morphologies of the solid solutions vary from blocky spherical crystal aggregates to smaller spheres with an increasing incorporation of Mn in the solids. Regarding dissolution in N2-degassed water, air-saturated water and CO2-saturated water at 25 °C, the aqueous Ca and Mn concentrations reach their highest values after 1240–2400 h, 6–12 h and < 1 h, respectively, and then decrease gradually to a steady state; additionally, the ion activity products (log_IAP) at the fnal steady state ( solubil- ity products in log_K ) are estimated to be 8.46 0.06, 8.44 0.10 and 8.59 0.10 for calcite [CaCO ], ≈respec- sp − ± − ± − ± 3 tively, and 10.25 0.08, 10.26 0.10 and 10.28 0.03, for rhodochrosite [MnCO3], respectively. As XMn increases, the log_IAP− values ±decrease− from ± 8.44 ~ 8.59− for calcite± to 10.25 ~ 10.28 for rhodochrosite. The aqueous Mn − − − − concentrations increase with an increasing Mn/(Ca Mn) molar ratio (XMn) of the (Ca1-xMnx)CO3 solid solutions, while the aqueous Ca concentrations show the highest values+ at X 0.53–0.63. -

Geological Setting and Genesis of Coticules (Spessartine Metapelites) in the Lower Ordovician of the Stavelot Massif, Belgium

Journal of the Geological Society, London, Vol. 143, 1986, pp. 253-258, 8 figs, 2 tables Printed in Northern Ireland Geological setting and genesis of coticules (spessartine metapelites) in the Lower Ordovician of the Stavelot Massif, Belgium J. LAMENS’, F. GEUKENS’ & W. VIAENE2 Instituut voor Aardwetenschappen, Katholieke Universiteit Leuven, Redingenstraat 16, B-3000 Leuven, Belgium ’Afdeling Fysico-Chemische Geologie, Katholieke Universiteit Leuven, Celestijnenlaan 200C, B-3030 Heverlee, Belgium Abstract: The LowerOrdovician in the CaledonianStavelot Massif (Belgium) containsa coticule member, probablyArenig in age, composed of redhematite-rich shales alternating with thin yellowish coticulebeds. These coticules are fine-grained highly manganiferousmetamorphic rocks mainly composed of spessartine garnet, mica and quartz. Similar rocks of about the same age occur in several localities along the Appalachian and Caledonian fold belts. The Belgian coticules are thought to haveoriginated from marly sediments which had beendeposited rapidly, probably by density currents, and in which CaCO, had been diagenetically replaced by MnCO,. During metamorphism, spessartine garnets- were formed from this MnCO, and mica. Manganese and iron are thought to have originated from volcanic-exhalative processes. The Stavelot Massif is one of the five Caledonian Massifs in could be used as a key lithology for correlation along the Belgium. It consists of MiddleCambrian to Lower Appalachian and Caledonian fold belts. Similar rocks have Ordovician strata (Fig. 1, Table 1). The southeastern partof also been described from older (Precambrian) and younger the Stavelot Massifis at a low metamorphicgrade. The strata(Roy & Purkait 1968; Vearncombe 1983; Minnigh LowerOrdovician of the Stavelot Massifis called 1979). Most of these spessartine-rich rocks, however, have “Salmian”.It has been subdivided into Salmian 1 (Sml), morequartz and less mica than the Belgian coticules. -

Alphabetical Listing by Company Name

FOREIGN COMPANIES REGISTERED AND REPORTING WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION December 31, 2015 Alphabetical Listing by Company Name COMPANY COUNTRY MARKET 21 Vianet Group Inc. Cayman Islands Global Market 37 Capital Inc. Canada OTC 500.com Ltd. Cayman Islands NYSE 51Job, Inc. Cayman Islands Global Market 58.com Inc. Cayman Islands NYSE ABB Ltd. Switzerland NYSE Abbey National Treasury Services plc United Kingdom NYSE - Debt Abengoa S.A. Spain Global Market Abengoa Yield Ltd. United Kingdom Global Market Acasti Pharma Inc. Canada Capital Market Acorn International, Inc. Cayman Islands NYSE Actions Semiconductor Co. Ltd. Cayman Islands Global Market Adaptimmune Ltd. United Kingdom Global Market Adecoagro S.A. Luxembourg NYSE Adira Energy Ltd. Canada OTC Advanced Accelerator Applications SA France Global Market Advanced Semiconductor Engineering, Inc. Taiwan NYSE Advantage Oil & Gas Ltd. Canada NYSE Advantest Corp. Japan NYSE Aegean Marine Petroleum Network Inc. Marshall Islands NYSE AEGON N.V. Netherlands NYSE AerCap Holdings N.V. Netherlands NYSE Aeterna Zentaris Inc. Canada Capital Market Affimed N.V. Netherlands Global Market Agave Silver Corp. Canada OTC Agnico Eagle Mines Ltd. Canada NYSE Agria Corp. Cayman Islands NYSE Agrium Inc. Canada NYSE AirMedia Group Inc. Cayman Islands Global Market Aixtron SE Germany Global Market Alamos Gold Inc. Canada NYSE Alcatel-Lucent France NYSE Alcobra Ltd. Israel Global Market Alexandra Capital Corp. Canada OTC Alexco Resource Corp. Canada NYSE MKT Algae Dynamics Corp. Canada OTC Algonquin Power & Utilities Corp. Canada OTC Alianza Minerals Ltd. Canada OTC Alibaba Group Holding Ltd. Cayman Islands NYSE Allot Communications Ltd. Israel Global Market Almaden Minerals Ltd. -

Mineralization of the Luis Lopez Epithermal Manganese Deposits in Light of Fluid Inclusion and Geologic Studies David I

New Mexico Geological Society Downloaded from: http://nmgs.nmt.edu/publications/guidebooks/34 Mineralization of the Luis Lopez epithermal manganese deposits in light of fluid inclusion and geologic studies David I. Norman, Khosrow Bazrafshan, and Ted L. Eggleston, 1983, pp. 247-251 in: Socorro Region II, Chapin, C. E.; Callender, J. F.; [eds.], New Mexico Geological Society 34th Annual Fall Field Conference Guidebook, 344 p. This is one of many related papers that were included in the 1983 NMGS Fall Field Conference Guidebook. Annual NMGS Fall Field Conference Guidebooks Every fall since 1950, the New Mexico Geological Society (NMGS) has held an annual Fall Field Conference that explores some region of New Mexico (or surrounding states). Always well attended, these conferences provide a guidebook to participants. Besides detailed road logs, the guidebooks contain many well written, edited, and peer-reviewed geoscience papers. These books have set the national standard for geologic guidebooks and are an essential geologic reference for anyone working in or around New Mexico. Free Downloads NMGS has decided to make peer-reviewed papers from our Fall Field Conference guidebooks available for free download. Non-members will have access to guidebook papers two years after publication. Members have access to all papers. This is in keeping with our mission of promoting interest, research, and cooperation regarding geology in New Mexico. However, guidebook sales represent a significant proportion of our operating budget. Therefore, only research papers are available for download. Road logs, mini-papers, maps, stratigraphic charts, and other selected content are available only in the printed guidebooks. Copyright Information Publications of the New Mexico Geological Society, printed and electronic, are protected by the copyright laws of the United States. -

STABLE ISOTOPES of HYDROTHERMAL CARBONATE MINERALS in the BUTTE PORPHYRY-LODE DEPOSITS, MONTANA Ryan Stevenson Montana Tech of the University of Montana

Montana Tech Library Digital Commons @ Montana Tech Graduate Theses & Non-Theses Student Scholarship Summer 2015 STABLE ISOTOPES OF HYDROTHERMAL CARBONATE MINERALS IN THE BUTTE PORPHYRY-LODE DEPOSITS, MONTANA Ryan Stevenson Montana Tech of the University of Montana Follow this and additional works at: http://digitalcommons.mtech.edu/grad_rsch Part of the Biogeochemistry Commons, Geology Commons, and the Geophysics and Seismology Commons Recommended Citation Stevenson, Ryan, "STABLE ISOTOPES OF HYDROTHERMAL CARBONATE MINERALS IN THE BUTTE PORPHYRY-LODE DEPOSITS, MONTANA" (2015). Graduate Theses & Non-Theses. 44. http://digitalcommons.mtech.edu/grad_rsch/44 This Thesis is brought to you for free and open access by the Student Scholarship at Digital Commons @ Montana Tech. It has been accepted for inclusion in Graduate Theses & Non-Theses by an authorized administrator of Digital Commons @ Montana Tech. For more information, please contact [email protected]. STABLE ISOTOPES OF HYDROTHERMAL CARBONATE MINERALS IN THE BUTTE PORPHYRY-LODE DEPOSITS, MONTANA by Ryan Stevenson A thesis submitted in partial fulfillment of the requirements for the degree of Master of Science in Geosciences Montana Tech 2015 ii Abstract The stable isotopic compositions of over 90 hydrothermal carbonate minerals in the Butte porphyry-lode system were analyzed. These samples came from the underground workings as well as the active Continental Pit area. Most material came from polymetallic “Main Stage” veins which post-date the porphyry Cu-Mo mineralization of Butte. Some samples from late calcite-stellerite veins were also included in the study. Rhodochrosite 13C and 18O values range from -8.3 to -2.9‰ (average of -6.7±1.0‰) and -1.8 to 12.8‰ (average of 3.6 ±3.4‰) respectively, while calcite 13C and 18O values range from -9.0 to -2.6‰ (average of -5.4 ± 1.5‰) and -4.4 to 12.3‰ (average of 6.2±2.8‰) respectively. -

Current List of All Non-U.S. Issuers 515 NYSE and NYSE MKT-Listed Non-U.S

Current List of All Non-U.S. Issuers 515 NYSE and NYSE MKT-listed non-U.S. Issuers from 46 Countries (as of December 31, 2015) Global Market Capitalization Share Country Issuer † Symbol ($M USD) Market Industry Listed Type IPO #N/A 12/31/2015 ARGENTINA (10 ADR Issuers and 4 non-ADR Issuers ) Adecoagro S.A. AGRO $ 1,487 NYSE Consumer Goods 1/28/11 O IPO Arcos Dorados Holdings Inc. ARCO $ 655 NYSE Travel & Leisure 4/14/11 O IPO Banco Marco S.A. BMA $ 3,339 NYSE Banks 3/24/06 A IPO BBVA Banco Francés S.A. BFR $ 3,414 NYSE Banks 11/24/93 A IPO Empresa Distribuidora y Comercializadora Norte S.A. (Edenor) EDN $ 795 NYSE Electricity 4/26/07 A IPO GeoPark Limited GPRK $ 155 NYSE Oil & Gas Producers 2/7/14 O IPO Globant S.A. GLOB $ 1,276 NYSE Software & Computer Services 7/18/14 O IPO IRSA-Inversiones y Representaciones, S.A. IRS $ 712 NYSE Real Estate Investment & Services 12/20/94 A IPO Nortel Inversora S.A. NTL $ 2,032 NYSE Fixed Line Telecommunications 6/17/97 A IPO Pampa Energia S.A. PAM $ 1,394 NYSE Electricity 10/9/09 A Petrobras Argentina S.A. PZE $ 1,119 NYSE Oil & Gas Producers 1/26/00 A Telecom Argentina S.A. TEO $ 3,115 NYSE Fixed Line Telecommunications 12/9/94 A Transportadora de Gas del Sur, S.A. TGS $ 968 NYSE Oil Equipment, Services & Distribution 11/17/94 A YPF Sociedad Anónima YPF $ 6,183 NYSE Oil & Gas Producers 6/29/93 A IPO AUSTRALIA (6 ADR Issuers ) Alumina Limited AWC $ 2,420 NYSE Industrial Metals & Mining 1/2/90 A BHP Billiton Limited BHP $ 65,005 NYSE Mining 5/28/87 A IPO James Hardie Industries N.V.