M&M 3.0: the NEW Is Coming

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Is Now Is Now Is Now Is Now Is Now Is Now

IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW ISSUE 4, 2012 IS NOW WHAT’SIS NOW INSIDE?IS NOW IS NOW IS NOW IS NOW A closer look at the Mahindra Group’s dynamic new visual identity IS NOW Swaraj Division’sIS N OWPlans for Building onI SIts SuccessNOW IS NOW IS NOW IS NOW Quanto and SsangYong Rexton launched Mahindra Logistics Clears Indian Airforce Simulator IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW A Spectrum of Awards for Excellence Mahindra Everyday IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW ISIS NOWNOWIS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW 1 IS NOW IS NOW IS NOW IS NOW IS NOW IS NOW ISSUE 4, 2012 CONTENTS AWARDS FOR COVER STORY 04 EXCELLENCE 43 The Mahindra Group has adopted a Mahindra Group companies notched up sleek new visual identity. -

Model Information News September 2017

MODEL INFORMATION NEWS SEPTEMBER 2017 CARS Light Commercial Vehicles 17 17 17 17 17 17 17 17 17 17 17 17 18 18 18 18 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Q1 Q2 Q3 Q4 AUDI Audi A5 Convertible Model 2017 Audi A8 Sedan Model 2017 Audi A8 L Sedan Model 2017 BMW BMW 2 Series Coupé Facelift Model 2017 BMW 2 Series Convertible Facelift Model 2017 BMW 1 Series 3 door Hatchback Facelift Model 2017 BMW 1 Series 5 door Hatchback Facelift Model 2017 BMW X3 Model 2017 BMW 6 Series GT Model 2017 1/72 Model Information News International Data Editorial 17 17 17 17 17 17 17 17 17 17 17 17 18 18 18 18 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Q1 Q2 Q3 Q4 CITROEN Citroen C5 Aircross Model 2018 Citroen C3 Aircross Model 2017 DACIA Dacia Logan MCV Stepway Model 2017 Dacia Duster Stationwagon Model 2018 DS DS 7 Crossback Model 2017 FERRARI Ferrari Portofino Convertible Model 2018 Ford Fiesta Active 5 door hachback Model FORD 2017 Ford Mustang Coupe Facelift Model 2018 Ford EcoSport Stationwagon Facelift Model 2018 FIAT Fiat 500L Urban Facelift Model 2017 Fiat 500L Cross Facelift Model 2017 Fiat 500L Wagon Facelift Model 2017 2/72 Model Information News International Data Editorial 17 17 17 17 17 17 17 17 17 17 17 17 18 18 18 18 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Q1 Q2 Q3 Q4 Honda Jazz 5 door Hatchback Facelift HONDA Model 2018 HYUNDAI Hyundai i30CW Model 2017 Hyundai Kona Model 2017 Hyundai i30 Sedan Model 2018 JAGUAR Jaguar I-Pace Model 2018 Jaguar E-Pace Model 2018 Jeep Compass 5 door Stationwagon JEEP Model 2017 KIA Kia Stinger -

Mahindra Everyday

ISSUE 1, 2013 ISSUE 1, 2013 WHAT’S INSIDE? Mahindra e2o Launched: Set to Redefine the Future of Mobility World Class Tractor Plant Inaugurated in Andhra Pradesh MSSSPL’s Golden Journey Of 50 Years 8th Annual Mahindra Excellence in Theatre Awards Announced Special Feature: The Mahindra Institute of Quality Mahindra Everyday 1 ISSUE 1, 2013 CONTENTS CULTURAL COVER STORY 04 OUTREACH 35 Mahindra USA’s exciting and eventful On the art and culture front, initiatives story of growth and success, from showcased old world culture, the world’s 1994 to date. best guitar and music talent, excellence in theatre and more. INTERNATIONAL AWARDS FOR OPERATIONS 11 EXCELLENCE 40 The Mahindra Group’s international A spectrum of awards, including the action stretched from Serbia to Sri first Mahindra Sustainability awards Lanka, South Africa and elsewhere recognising diverse sustainability around the globe. initiatives, was recently presented. SECTOR BRIEFS 13 SUSTAINABILITY 47 As ever there was plenty happening Efforts and initiatives towards across sectors and in all spheres of preserving, safeguarding and sustaining action – new plants, new products, our planet and its precious resources. distinguished visitors, certifications and celebrations. Please write in to [email protected] to give feedback on this issue. ME TEAM Associate Editors: Zarina Hodiwalla, Darius Lam Soumi Rao Chandrika Rodrigues Col. Abhijit Dasgupta AS, Kandivli MLDL Mahindra Management Dev. Center Asha Sabharwal Stella Rozario AS, Nashik MTWL Santosh Tandav Mahindra Partners Shirish Kulkarni Pradeep Zoting AS, Igatpuri FES, Nagpur Vrinda Pisharody Tech Mahindra & K.P. Narsimha Rao Pavitra Kamdadai Mahindra Satyam AS, Zaheerabad MNEPL Rajeev Malik Venecia Paulose Martin Cisneros Preeti Nair MVML, Chakan Mahindra USA Mahindra Navistar Edited and Published by Roma Balwani Nitin Panday Swapnil Soudagar Pooja Thawrani for Mahindra & Mahindra Limited, Gateway Mahindra Swaraj Systech Mahindra Reva Building, Apollo Bunder, Mumbai 400 001. -

Winters of Yesteryear We Take a Look Back at How

Good motoringThe magazine for members of GEM Motoring Assist Winter 2016 a luxuryWIN two-night break for two at Hartwell House. See p14 WINTERS OF YESTERYEAR SNOW ALERT! WE TAKE A LOOK BACK AT HOW BLASTS FROM THE PAST BROUGHT BRITAIN TO A STANDSTILL A cushioned ride Scottish castles Road tests On hovercraft patrol with the How to be your own VW Touran, SsangYong Tivoli, Finnish Border Guard laird for the night Seat Ateca, Kia Niro One call is all it took to sort my Home Insurance 1 YEAR’S FREE HOME EMERGENCY COVER* (worth £14.50 pa) QUOTE GEM16 Enjoy great premiums and personal service PLUS 1 year’s Free Home Emergency Cover GEM has partnered with Shield Total Insurance to bring you competitive premiums and a Optional Family Legal Cover wide choice of cover options, including: UpU tot £100,000£100 000 legal cover against ✔ Up to £1 million buildings cover disputes on the sale & purchase of your ✔ Up to £150,000 contents cover home, personal ✔ All policies on a New for Old basis injury or disputes with neighbours. Just £17.50 pa ✔ Cover for garages and outbuildings on your land ✔ Optional Key Protection from £11 pa Make More Of Your Membership Call now and quote GEM16 01277 243 010 *Offer closes 31/12/16. Terms & Conditions apply: Customer must purchase a household insurance policy with Shield Total Insurance. One free Home Emergency cover per policy. You must be a UK resident. Free Home Emergency cover is available for 1 year only and is non-refundable. Cancelling your household insurance policy mid-term will automatically discontinue Home Emergency cover. -

Annual Report 2013 MOVING AHEAD

Moving Ahead Annual Report 2013 MOVING AHEAD // Contents SOLLERS: MOVING AHEAD 06 Chairman’s Statement 08 CEO’s Statement 12 About the Company 14 Project Mapping 16 Key Performance Indicators Business & Strategy 20 Market Overview and Sollers’ Product Portfolio 29 Our Strategy 34 Our Business Model 36 Business Projects and Key Assets Corporate Governance 48 What does Corporate Governance Mean to Sollers? 50 The Profiles of Sollers’ Directors 54 Board of Directors’ Meetings 55 Board Committee Reports 60 The Profiles of Sollers’ Managers 62 Risk Management and Principal Risks Corporate Social Responsibility 68 Responsible Business Principles in All Our Operations 69 Increasing the Company’s Shareholder Value 70 Growth Through Long-Term Partnerships 71 Continuing Development 73 Improving the Quality of Our Products and Services 74 Improving Employee Competences 75 Contributing to the Social and Economic Development 75 Increasing Operating Safety and Monitoring RUB 61.3 bln >20 76 Reducing Our Impact on the Environment consolidated revenue in 2013 new products were launched by Shareholders’ Equity & Securities 80 Share Capital SOLLERS together with its partners 80 Major Shareholders’ 80 Market Share Price & GDR 81 Investor Relations Calendar 2014 81 Investor Relations Department For more info... SOLLERS is one of the leading Russian automotive Financial Reporting 86 Independent Auditor’s Report This Annual Report is also 87 Sollers Group Consolidated Financial Statements available on our website, companies and works in partnership with global -

Miami1177598932.Pdf (567.64

MIAMI UNIVERSITY The Graduate School CERTIFICATE FOR APPROVING THE DISSERTATION We hereby approve the Dissertation Of Irina Aervitz Candidate for the Degree: Doctor of Philosophy Director (Dr. John M. Rothgeb) Reader (Dr. Walter Arnold) Reader (Dr. Venelin I. Ganev) Graduate School Representative (Dr. Margaret Ziolkowski) ABSTRACT THE DRIVING FORCE BEHIND THE AUTOMOTIVE SECTOR IN CHINA AND RUSSIA: THE ROLE OF THE STATE IN TECHNOLOGY APPROPRIATION by Irina Aervitz The focus of this study is automobile industry in China and Russia. Specifically I am looking at the state attempts to encourage technology development in the automobile sector. My goal is to look for variations in the overall policy environment created by the state with regard to technology enhancement in the automobile industry in China and Russia and particularly focus on policy implementations at the enterprise level by observing the way enterprises appropriate technology by using various sources of technology appropriation provided by the state policies. I believe that this research is important because it reviews the literature on the role of the state in industrial development and introduces the concept of “technology appropriation.” Technology appropriation lies in the heart of the companies’ technological competitiveness and is based on the sources of technology made available to companies by the regulatory environment created by the state. Most importantly, this project offers analysis of the empirical data collected during a series of interviews in the domestic and foreign enterprises operating in both countries. This analysis attempts to lift the “curtain” over the companies’ technology-oriented strategies and the way they take advantage of the existent state policies affecting the process of technology appropriation. -

Approval Car Price Issued As of 30Th June 2019

APPROVAL CAR PRICE ISSUED AS OF 30TH JUNE 2019 DATE SHOWROOM PASSENGER MOTOR VEHICLES BRAND PASSENGER MOTOR VEHICLES MODEL /TYPE DATE ISSUED PRICE (SRP) EFFECTIVE EXPIRY ALFA ROMEO ALFA ROMEO GIULIA 620 QV V6 (G.H.K MOTORS SDN BHD) ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $139,973.00 ALFA ROMEO GIULIA 620 GME ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $63,353.00 AUDI AUDI A3 TFSI S-TRONIC (T. C. Y. MOTORS SDN BHD) AUDI A3 1.2L TFSI S-TRONIC AUTO SEDAN PETROL 22-Jan-19 31-Dec-18 30-Dec-19 $43,631.00 AUDI A3 TFSI S-TRONIC SPORTBACK AUDI A3 1.2L TFSI S-TRONIC AUTO SPORTBACK PETROL 6-Sep-18 11-Sep-18 10-Sep-19 $46,803.00 AUDI A4 TFSI S-TRONIC BLACK EDITION AUDI A4 2.0L TFSI S-TRONIC AUTO SEDAN PETROL - BLACK EDITION 19-Jun-19 3-Jun-19 2-Jun-20 $55,068.00 AUDI A4 TFSI QUATTRO S-TRONIC AUDI A4 2.0L TFSI QUATTRO S-TRONIC AUTO AWD SEDAN PETROL 19-Jun-19 3-Jun-19 2-Jun-20 $67,560.00 AUDI A4 TFSI ULTRA S-TRONIC AUDI A4 2.0L TFSI ULTRA S-TRONIC AUTO S-LINE BLACK STYLING SEDAN PETROL 31-Dec-18 31-Dec-18 30-Dec-19 $58,515.00 (MODEL CODE: 8W2BDG) AUDI A4 TFSI ULTRA QUATTRO S-TRONIC AUDI A4 2.0L TFSI ULTRA QUATTRO AWD S-TRONIC AUTO SEDAN PETROL 25-Feb-19 11-Feb-19 10-Feb-20 $68,676.00 AUDI A5 TFSI QUATTRO S-TRONIC COUPE AUDI A5 2.0L TFSI QUATTRO S-TRONIC AUTO COUPE PETROL 8-Aug-18 14-Aug-18 13-Aug-19 $79,952.00 AUDI A5 TFSI QUATTRO S-TRONIC SPORTBACK AUDI A5 2.0L TFSI QUATTRO S-TRONIC AUTO SPORTBACK PETROL 8-Aug-18 14-Aug-18 13-Aug-19 $83,042.00 AUDI Q2 AUDI Q2 1.0L TFSi S-TRONIC -

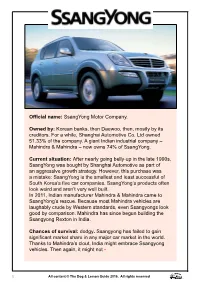

Official Name: Ssangyong Motor Company. Owned By: Korean Banks, Then Daewoo, Then, Mostly by Its Creditors. for a While, Shangha

Official name: SsangYong Motor Company. Owned by: Korean banks, then Daewoo, then, mostly by its creditors. For a while, Shanghai Automotive Co. Ltd owned 51.33% of the company. A giant Indian industrial company – Mahindra & Mahindra – now owns 74% of SsangYong. Current situation: After nearly going belly-up in the late 1990s, SsangYong was bought by Shanghai Automotive as part of an aggressive growth strategy. However, this purchase was a mistake: SsangYong is the smallest and least successful of South Korea’s five car companies. SsangYong’s products often look weird and aren’t very well built. In 2011, Indian manufacturer Mahindra & Mahindra came to SsangYong’s rescue. Because most Mahindra vehicles are laughably crude by Western standards, even Ssangyongs look good by comparison. Mahindra has since begun building the Ssangyong Rexton in India. Chances of survival: dodgy. Ssangyong has failed to gain significant market share in any major car market in the world. Thanks to Mahindra’s clout, India might embrace Ssangyong vehicles. Then again, it might not • 1 All content © The Dog & Lemon Guide 2016. All rights reserved A brief commentary on Ssangyong sangYong means ‘twin dragons’ and refers to a Korean legend in which two dragons waited 1000 years to fly to dragon heaven. SFinally, a single cintamani (magic jewel), which was necessary for the journey, was released. Each dragon encouraged the other to take it and make the trip. This display of courtesy went on for so long that both dragons missed the opportunity. The king of heaven was so touched by the dragons’ generous display that he released a second cintamani and thus the two dragons entered heaven to- gether. -

Approval Car Price Issued As of 15Th June 2020

APPROVAL CAR PRICE ISSUED AS OF 15TH JUNE 2020 DATE SHOWROOM PASSENGER MOTOR VEHICLES BRAND PASSENGER MOTOR VEHICLES MODEL /TYPE DATE ISSUED PRICE (SRP) EFFECTIVE EXPIRY ALFA ROMEO ALFA ROMEO GIULIA 620 QV V6 (G.H.K MOTORS SDN BHD) ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL 4-Apr-20 21-Apr-20 20-Apr-21 $139,973.00 ALFA ROMEO GIULIA 620 GME ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL 4-Apr-20 21-Apr-20 20-Apr-21 $64,485.00 ALFA ROMEO GIULIA VELOCE 620 GME 2000 ALFA ROMEO GIULIA VELOCE 620 2.0L AUTO GME 2000 SEDAN PETROL 21-May-20 3-Nov-19 2-Nov-20 $69,094.00 ALFA ROMEO STELVIO ALFA ROMEO STELVIO 2.0L 8-SPEED AUTOMATIC TRANSMISSION AWD SUV 7-Jan-20 1-Dec-19 30-Nov-20 $75,262.00 PETROL (SOLID PAINT) ALFA ROMEO STELVIO 2.0L 8-SPEED AUTOMATIC TRANSMISSION AWD SUV 7-Jan-20 1-Dec-19 30-Nov-20 $77,538.00 PETROL (SPECIAL PAINT) AUDI AUDI A3 TFSI S-TRONIC (T. C. Y. MOTORS SDN BHD) AUDI A3 1.2L TFSI S-TRONIC AUTO SEDAN PETROL 26-Dec-19 31-Dec-19 30-Dec-20 $43,631.00 AUDI A3 TFSI S-TRONIC SPORTBACK AUDI A3 1.2L TFSI S-TRONIC AUTO SPORTBACK PETROL 7-Sep-19 11-Sep-19 10-Sep-20 $46,803.00 AUDI A4 TFSI ULTRA QUATTRO S-TRONIC AUDI A4 2.0L TFSI ULTRA QUATTRO AWD S-TRONIC AUTO SEDAN PETROL 20-Feb-20 11-Feb-20 10-Feb-21 $68,676.00 AUDI A5 TFSI QUATTRO S-TRONIC COUPE AUDI A5 2.0L TFSI QUATTRO S-TRONIC AUTO COUPE PETROL 13-Aug-19 14-Aug-19 13-Aug-20 $79,952.00 AUDI A5 TFSI QUATTRO S-TRONIC SPORTBACK AUDI A5 2.0L TFSI QUATTRO S-TRONIC AUTO SPORTBACK PETROL 13-Aug-19 14-Aug-19 13-Aug-20 $83,402.00 AUDI A6 TFSI S-TRONIC SEDAN AUDI A6 2.0L TFSI S-TRONIC -

Electric Vehicles— Concepts

www.autotechreview.com April 2013 | Volume 2 | Issue 4 NOW, ALSO AVAILABLE ON It’s on 14 INTERVIEW Nalin Mehta, Managing Director Mahindra Navistar Automotives Ltd 18 TECHNOLOGY FORESIGHT Ultra-Capacitors for Electric Vehicles: Future Perspetives 60 NEW VEHICLE Honda CR-V — Flexible, Practical & Better ELECTRIC VEHICLES— CONCEPTS, SOLUTIONS & COMPETENCE POWERED BY Complete solutions in precision metallic coil springs I N S T Compression Springs T U T Static and Dynamic E of These are coiled helical SP RING TECHNOLOGY springs made from spring steel wire, that can resist compressive load. Extension Springs 1. Suspension Springs - These are normally close Torsion Springs Front Fork & Shock coil springs of circular These resist an applied Wire Forms Absorber cross sections, with the torque when the ends are These are made on forming 2. Engine Valve Springs end usually a hook or subjected to angular machines, in different shapes, 3. Clutch Springs loop, used in computers, displacement, used in adaptable to required 4. Rebound Springs brakes, etc. transmission, etc. applications. Seat Belt Springs Used for operation of Seat Belts of 4-Wheelers, made out of textured rolled hardened and tempered high carbon steel strips in various sizes. A to Z product range as per Customer’s designs, applications, sizes and Internationals standards Regd. Office & Works Manufacturing Unit-II Plot No. 192 A, Sector-4, E-56, Industrial Area, Haridwar-249 401 IMT Manesar-122050 Gurgaon, Haryana, India Uttarakhand, India Tel.: +91-124-4763200 Fax: +91-124-4365189 Tel.: +91-1334-221301 Fax: +91-1334-220128 E-mail: [email protected] E-mail : [email protected] ISO 9001 EDITORIAL E-VIABILITY? Dear reader, To question the viability of electric vehicles, at a time when Mahindra Reva has launched its latest bet, the e2o, might sound a little preposterous. -

Sustainability Review 2014-15

Sustainability Review 2014-15 From embedding sustainability as a business driver across the Group to empowering individual businesses to drive sustainability, within eight years, we have successfully cascaded sustainability from a boardroom vision to a shop oor reality. Powered by Alternative Thinking - our bespoke approach to sustainability, we enhanced awareness, expounded a strong business case to employees, institutionalised frameworks, invested in capacity building plus rewarded and recognised outstanding performers. The road to sustainability is fraught with obstacles - some have to be overcome with innovation, some with determination, and some simply by perseverance. But as we overcome each obstacle, we come across doors of opportunities with multiple outcomes that take us to the next level. This thought is graphically represented in this design theme. The upward moving transverse lines represent the Group's ambitions. The pillars of myriad colours are the roadmaps of individual businesses. While the ones in red are symbolic of Mahindra's Rise for Good philosophy that continues to guide them all. BUSINESSWISE is the next phase in our sustainability journey. In it, every individual business is driving the sustainability agenda on issues material to their stakeholders and aiming to set new benchmarks within their sector and geographies. It is like pursuing the sustainability agenda with independent teams who are not only committed but capable and experienced. This enlarged team, new vigour, focus and greater ownership has created -

Download Rexton Quintra Operating Instructions

Download rexton quintra operating instructions REXTON BTE USER MANUAL Pdf Download. rexton quintra operating instructions View and Download Rexton BTE user manual online. BTE Hearing Aid pdf manual download. Rexton Hearing Aid User Manuals Download - ManualsLib rexton quintra operating instructions Download 3 Rexton Hearing Aid PDF manuals. User manuals, Rexton Hearing aid Operating guides and Service manuals. [PDF] Rexton mini blu rcu user guide - read & download rexton quintra operating instructions If you are looking for the ebook Rexton mini blu rcu user guide in pdf format, in that case you come on to the faithful website. ... read/download rexton strata 18 manual; read/download rexton quintra manual . copyright 2014. ... Download or Read Online eBook user manual rexton mini blu rcu in PDF Format From . Welcome to Rexton Hearing Aids - Rexton rexton quintra operating instructions Our products offer superior speech understanding, durability, and personalization to deliver unprecedented wearing comfort. Our tenured, passionate people are empowered to provide solution-driven service to meet each individual’s needs. That is why Rexton is the smart choice. About our products. Guide, Repair Manual Yamaha Zuma, 2000 Yamaha Yz80 Owners ... rexton quintra operating instructions pdf book displaying 17201 to 17300 of 462266 products 2003 honda crv manual ... window wiring diagram focus economics grade 12 caps rexton quintra manual ... repair shop manual download workshop manual victa motorola droid a855 user manual Piano Manual - Ebook List