New Association's Aspiration

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Financial Services Clipsheet October 27, 2004

AQUBANC ClipSheet 2004 James Cowen, Vice President of Sales, AQUBANC, LLC , , 800.350.4720 [email protected] www.aqubanc.com Financial Services Clipsheet October 27, 2004 Check 21 Aqubanc Check 21 offering PRWEB 10/27 Aqubanc, LLC, Buffalo Grove IL, a provider of Payment, Check, & Form Processing Solutions announces the Check 21 Pass™ for processing check transactions. Every check transaction which can physically move through a check or page image scanner is imaged with the checks first & always before any other documents in the transaction. Check 21 Pass documents do not need or require any OCR scan lines or barcodes. Eliminating OCR scan lines or barcodes means more real estate is available on each document for use by marketing, sales & business development in soliciting & to convey information. In the Check 21 Pass, document recognition, data field capture & data excellence are performed on multiple fonts in multiple sizes on multiple documents within each batch. This makes it easier for operations to open/sort mail, post transactions & submit electronic deposits to meet ARC & Check 21 conversion needs. Will imaging prompt Fed to exit from clearing? 10/27 AB Many believe that as banks start using electronic images to clear checks they will switch from the Federal Reserve Banks’ check processing service to private systems. Nobody expects an instant transformation Thursday, when Check 21 will take effect. The law will merely make banks accept printouts of check images as substitute checks. But Thursday will be a symbolic kickoff to full-scale image clearing, & a number of companies are poised to offer image-based clearing & settlement, which would divert business from the Fed. -

Primer Podjetja Paypal

UNIVERZA V LJUBLJANI EKONOMSKA FAKULTETA DIPLOMSKO DELO KONKURENCA NA TRGU PLAČILNIH STORITEV S STRANI NEBANČNIH PODJETIJ: PRIMER PODJETJA PAYPAL Ljubljana, maj 2013 MATEJ ŠKRINJAR IZJAVA O AVTORSTVU Spodaj podpisani Matej Škrinjar, študent Ekonomske fakultete Univerze v Ljubljani, izjavljam, da sem avtor diplomskega dela z naslovom Konkurenca na trgu plačilnih storitev s strani nebančnih podjetij: primer podjetja PayPal, pripravljenega v sodelovanju s svetovalcem doc. dr. Matejem Marinčem. Izrecno izjavljam, da v skladu z določili Zakona o avtorski in sorodnih pravicah (Ur. l. RS, št. 21/1995 s spremembami) dovolim objavo diplomskega dela na fakultetnih spletnih straneh. S svojim podpisom zagotavljam, da je predloženo besedilo rezultat izključno mojega lastnega raziskovalnega dela; je predloženo besedilo jezikovno korektno in tehnično pripravljeno v skladu z Navodili za izdelavo zaključnih nalog Ekonomske fakultete Univerze v Ljubljani, kar pomeni, da sem o poskrbel, da so dela in mnenja drugih avtorjev oziroma avtoric, ki jih uporabljam v diplomskem delu, citirana oziroma navedena v skladu z Navodili za izdelavo zaključnih nalog Ekonomske fakultete Univerze v Ljubljani, in o pridobil vsa dovoljenja za uporabo avtorskih del, ki so v celoti (v pisni ali grafični obliki) uporabljena v tekstu, in sem to v besedilu tudi jasno zapisal; se zavedam, da je plagiatorstvo – predstavljanje tujih del (v pisni ali grafični obliki) kot mojih lastnih – kaznivo po Kazenskem zakoniku (Ur. l. RS, št. 55/2008 s spremembami); se zavedam posledic, ki bi jih na osnovi predloženega diplomskega dela dokazano plagiatorstvo lahko predstavljalo za moj status na Ekonomski fakulteti Univerze v Ljubljani v skladu z relevantnim pravilnikom. V Ljubljani, dne 22.5.2013 Podpis avtorja:__________________ KAZALO UVOD .................................................................................................................. -

Nordic M&A Tech Refresh

Nordic M&A Tech Refresh Selected deals: Updated 09.05/2021 Updated every Monday morning, here 1 | 88 Nordic M&A Tech Refresh Contents Selected deals: 2021 Week 18 (03 may – 09 may) 4 Selected deals: 2021 Week 17 (26 apr – 02 may) 5 Selected deals: 2021 Week 16 (19 apr – 25 apr) 7 Selected deals: 2021 Week 15 (12 apr – 18 apr) 9 Selected deals: 2021 Week 14 (5 apr – 11 apr) 11 Selected deals: 2021 Week 12-13 (22 mar – 4 apr) 13 Selected deals: 2021 Week 11 (15 mar – 21 mar) 15 Selected deals: 2021 Week 10 (08 mar – 14 mar) 17 Selected deals: 2021 Week 09 (01 mar – 07 mar) 18 Selected deals: 2021 Week 08 (22 feb – 28 feb) 20 Selected deals: 2021 Week 06-07 (08 feb – 21 feb) 21 Selected deals: 2021 Week 05 (01 feb – 07 feb) 23 Selected deals: 2021 Week 04 (25 jan – 31 jan) 24 Selected deals: 2021 Week 03 (18 jan – 24 jan) 26 Selected deals: 2021 Week 02 (11 jan – 17 jan) 28 Selected deals: 2021 Week 01 (01 jan – 10 jan) 29 Selected deals: 2020 Week 51-53 (14 dec – 31 dec) 31 Selected deals: 2020 Week 50 (07 dec – 13 dec) 33 Selected deals: 2020 Week 49 (30 nov – 06 dec) 35 Selected deals: 2020 Week 48 (23 nov – 29 nov) 37 Selected deals: 2020 Week 47 (16 nov – 22 nov) 38 Selected deals: 2020 Week 46 (09 nov – 15 nov) 40 Selected deals: 2020 Week 45 (02 nov – 08 nov) 41 Selected deals: 2020 Week 44 (26 oct – 01 nov) 42 Selected deals: 2020 Week 43 (19 oct – 25 oct) 44 Selected deals: 2020 Week 42 (12 oct – 18 oct) 46 Selected deals: 2020 Week 41 (05 oct – 11 oct) 47 Selected deals: 2020 Week 40 (28 sep – 04 oct) 49 Selected deals: 2020 Week -

March of Mobile Money: the Future of Lifestyle Management

The March of Mobile Money THE FUTURE OF LIFESTYLE MANAGEMENT SAM PITRODA & MEHUL DESAI The March of Mobile Money THE FUTURE OF LIFESTYLE MANAGEMENT SAM PITRODA & MEHUL DESAI First published in India in 2010 by Collins Business An imprint of HarperCollins Publishers a joint venture with The India Today Group Copyright © Sam Pitroda and Mehul Desai 2010 ISBN: 978-81-7223-865-0 2 4 6 8 10 9 7 5 3 Sam Pitroda and Mehul Desai assert the moral right to be identified as the authors of this work. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publishers. HarperCollins Publishers A-53, Sector 57, Noida 201301, India 77-85 Fulham Palace Road, London W6 8JB, United Kingdom Hazelton Lanes, 55 Avenue Road, Suite 2900, Toronto, Ontario M5R 3L2 and 1995 Markham Road, Scarborough, Ontario M1B 5M8, Canada 25 Ryde Road, Pymble, Sydney, NSW 2073, Australia 31 View Road, Glenfield, Auckland 10, New Zealand 10 East 53rd Street, New York NY 10022, USA Typeset in 12/18.3 Dante MT Std InoSoft Systems Printed and bound at Thomson Press (India) Ltd We would like to thank the entire C-SAM family and its well-wishers, without whom this journey would not be as enriching. We would like to thank Mayank Chhaya, without whom we would not have been able to complete this book. We would like to thank our better halves, Anu and Malavika, without whose companionship this journey and book would not be as meaningful. -

Paypal Prospectus.Pdf

SUBJECT TO COMPLETION, DATED JANUARY 18, 2002 P R O S P E C T U S 5,400,000 Shares Common Stock statement filed with the Securities and Exchange $ per share e securities in any state where the offer or sale is not permitted. We are selling 5,400,000 shares of our common stock. We have granted the underwriters an option to purchase up to 810,000 additional shares of common stock to cover over-allotments. This is the initial public offering of our common stock. We currently expect the initial public offering price to be between $12.00 and $14.00 per share. We have applied to have our common stock included for quotation on the Nasdaq National Market under the symbol ``PYPL.'' Investing in our common stock involves risks. See ``Risk Factors'' beginning on page 8. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. Per Share Total Public Offering Price $ $ Underwriting Discount $ $ Proceeds to PayPal (before expenses) $ $ The underwriters expect to deliver the shares to purchasers on or about , 2002. Salomon Smith Barney Bear, Stearns & Co. Inc. William Blair & Company SunTrust Robinson Humphrey Friedman Billings Ramsey The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration The information in this prospectus is not complete and may be changed. We Commission is effective. This prospectus not an offer to sell these securities and it soliciting buy thes , 2002 You should rely only on the information contained in this prospectus. -

Survey of Developments in Electronic Money and Internet and Mobile Payments

Committee on Payment and Settlement Systems Survey of developments in electronic money and internet and mobile payments March 2004 Copies of publications are available from: Bank for International Settlements Press & Communications CH-4002 Basel, Switzerland E-mail: [email protected] Fax: +41 61 280 9100 and +41 61 280 8100 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2004. All rights reserved. Brief excerpts may be reproduced or translated provided the source is cited. ISBN 92-9131-667-9 (print) ISBN 92-9197-667-9 (online) Foreword A number of innovative products for making payments have been developed in recent years, taking advantage of rapid technological progress and financial market development. Transactions made using these innovative products are accounting for an increasing proportion of the volume and value of domestic and cross-border retail payments. The possibility of electronic money taking over from physical cash for most small-value payments continues to evoke considerable interest among both the public and the various authorities concerned, including central banks. Although e-money has not been a very dynamic area in the field of retail payments recently, its development raises policy issues for central banks as regards payment system oversight, the possible implications for central banks’ revenues and the implementation of monetary policy. In view of these potential policy concerns, in 1996 the G10 central bank Governors announced their intention to closely monitor the evolution of electronic money schemes and products and, while respecting competition and innovation, to take any appropriate action if necessary. The Governors asked the BIS to monitor the developments of these new products on a regular and, as far as possible, global basis. -

Diáriodoco Gresso

ESTADOS UNIDOS DO BRASiL DIÁRIO•. • ~'" < *~', .,;' ,,DO• . CO. GRESSO'·. -, ..•.'. lei SEÇAO iLL ""'" ANO XII - N,' 194 CAPITAL FEDERAL QUINTA-F~IRA, 24 DE OUTUBRO DE 1957 ... NACIONAl~ CONGRESSO., -. • ~ - ; l-' ' • .~ Presídêneía .~ ... Transferêllcia d@~pr.eciação de "veto" .presidencial que cU.spõe sõbre créditos orçamentários destinad~s !J.. cJefc.a contra ~. secas do- Nordeste, regula a forma de pagamento de ,ll'CClUU. vela cúUAooo O Presidente do senado Federal, atendene'o à ímpcssibílídade .de se trução de açudes em cooperação e dá outrus providênclae. ~calizar no dia 22 do corrente, conrcrme rôra estabelecido, a. uprecíação elo Veto presidencial D.O Projeto de Li:! .n.> 1.181. de 1958, na Câmara e SeMdo Federal, em 9 de Outubro de 1957. n.« 82, de 1957, no senaãc, que reol':;aniza as Secretarias do MiIUstérlo Senador I,polônia Sales Público da União ju:ito à Justiça do Trabalho, cria o respectivo QUadro VIce-Presidente, no exercicío da Presidêx;clll. de Pessoal e dá outras provídêncías, em virtUI;!·" de ser ti sessão conjunta. dessa data necessárla o. ultimação do estudo do veto presídeneíal ao Pro jeto de Lei que dispõe sõbre a reforma da Tanfa das Alfândegas, resolve Convocação de sessão conjunta .para apreciação transrert-la paro. o dia '24, também do mês em curso, às 21 horas, no do "veto" presidencial ;L"aacio da Câmara dos Deputados. O Presidente do Senc.do Federal, nos têrmas do aMigo 70, ~ da Senado Federal, 11 de Outubro de 1957. 3.°, ConstltUiçúo Federal, e do artigo 45 do Regimento comum, convoca aa Senador Apo/ónio Salle~ duas Casas ,do Congresso Nacional para, em .sessâo conjunta. -

University of Jammu

University of Jammu The Business School MBA 106: Computer Applications In Management Online Payment Protocols Submitted To: Submitted By: Mrs. Versha Mehta Kartik Gupta (18) Faculty Varun Kumar (39) TBS, JU MBA, 1st Sem E-commerce payment system An e-commerce payment system facilitates the acceptance of electronic payment for online transactions. Also known as Electronic Data Interchange (EDI), e-commerce payment systems have become increasingly popular due to the widespread use of the internet-based shopping and banking. In the early years of B2C transactions, many consumers were apprehensive of using their credit and debit cards over the internet because of the perceived increased risk of fraud. Recent research shows that 30% of people in the United Kingdom still do not shop online because they do not trust online payment systems. However, 54% do believe that it is safe to shop online which is an increase from 26% in 2006. There are numerous different payments systems available for online merchants. These include the traditional credit, debit and charge card but also new technologies such as digital wallets, e-cash, mobile payment and e-checks. Another form of payment system is allowing a 3rd party to complete the online transaction for you. These companies are called Payment Service Providers (PSP), a good example is Paypal or WorldPay. Credit Cards and Smart Cards Over the years, credit cards have become one of the most common forms of payment for e- commerce transactions. In North America almost 90% of online B2C transactions were made with this payment type. Turban et al. goes on to explain that it would be difficult for an online retailer to operate without supporting credit and debit cards due to its widespread use. -

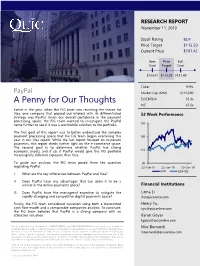

A Penny for Our Thoughts

RESEARCHNovember REPORT11, 2019 A NovemberPenny for Our11, 2019 Thoughts Stock Rating BUY Insert Picture in Master View Price Target $115.29 Current Price $101.42 Bear Price Bull Case Target Case $103.41 $115.29 $131.49 Ticker PYPL PayPal Market Cap (MM) $119,090 A Penny for Our Thoughts EV/EBITDA 35.3x P/E 47.6x Earlier in the year, when the FIG team was revisiting the theses for Visa, one company that piqued our interest with its differentiated 52 Week Performance strategy was PayPal. Given our overall confidence in the payment processing space, the FIG team wanted to investigate the PayPal name further to see if it was a worthwhile addition to the portfolio. 150 The first goal of this report was to better understand the complex payment processing space that the FIG team began examining this 130 year in our Visa report. While the last report focused on in-person payments, this report sheds further light on the e-commerce space. The second goal is to determine whether PayPal has strong economic moats and if so, if PayPal would give the FIG portfolio 110 meaningfully different exposure than Visa. To guide our analysis, the FIG team posed three key question 90 regarding PayPal: 22-Feb-19 22-Jun-19 20-Oct-19 PYPL S&P100 I. What are the key differences between PayPal and Visa? II. Does PayPal have any advantages that can allow it to be a winner in the online payments space? Financial Institutions III. Does PayPal have the managerial expertise to navigate the Linna Li rapidly changing and competitive digital payments space? [email protected] Finally, the FIG team considered valuation using both a discounted Henry Yu cash flow model and a comparable companies analysis. -

Nordic M&A Tech Refresh

Nordic M&A Tech Refresh Selected deals: Updated 10.01/2021 Updated every Monday morning, here 1 | 63 Nordic M&A Tech Refresh Contents Selected deals: 2021 Week 01-02 (01 jan – 10 jan) 4 Selected deals: 2020 Week 51-53 (14 dec – 31 dec) 6 Selected deals: 2020 Week 50 (07 dec – 13 dec) 8 Selected deals: 2020 Week 49 (30 nov – 06 dec) 10 Selected deals: 2020 Week 48 (23 nov – 29 nov) 12 Selected deals: 2020 Week 47 (16 nov – 22 nov) 13 Selected deals: 2020 Week 46 (09 nov – 15 nov) 15 Selected deals: 2020 Week 45 (02 nov – 08 nov) 16 Selected deals: 2020 Week 44 (26 oct – 01 nov) 17 Selected deals: 2020 Week 43 (19 oct – 25 oct) 19 Selected deals: 2020 Week 42 (12 oct – 18 oct) 21 Selected deals: 2020 Week 41 (05 oct – 11 oct) 22 Selected deals: 2020 Week 40 (28 sep – 04 oct) 24 Selected deals: 2020 Week 39 (21 sep – 27 sep) 25 Selected deals: 2020 Week 38 (14 sep – 20 sep) 26 Selected deals: 2020 Week 37 (07 sep – 13 sep) 27 Selected deals: 2020 Week 36 (31 aug – 06 sep) 28 Selected deals: 2020 Week 35 (24 aug – 30 aug) 30 Selected deals: 2020 Week 34 (17 aug – 23 aug) 32 Selected deals: 2020 Week 33 (10 aug – 16 aug) 34 Selected deals: 2020 Week 32 (03 aug – 09 aug) 35 Selected deals: 2020 Week 31 (27 july – 02 aug) 36 Selected deals: 2020 Week 30 (20 july – 26 july) 37 Selected deals: 2020 Week 29 (13 july – 19 july) 38 Selected deals: 2020 Week 28 (06 july – 12 july) 39 Selected deals: 2020 Week 27 (29 june – 05 july) 40 Selected deals: 2020 Week 26 (22 june – 28 june) 41 Selected deals: 2020 Week 25 (15 june – 21 june) 42 Selected deals: -

Why Payments Startups Fail

STRATEGIES May 2012 digitaltransactions Why Payments Startups Fail Eric Grover Low acceptance costs, convenience, and security aren’t enough. As compelling, economics to anybody in this global review of would-be PayPals and Visas shows, startups the value chain. Much-ballyhooed Revolution Mon- need a clear path to a mass of users. ey launched in 2007 and wooed retail- ers with a 0.5% merchant discount and ith the advent of mobile it comes to payments, consumers and superior fraud prophylactics. It boasted payments, we read almost merchants are creatures of habit. To as its chief executive Jason Hogg, son W daily about new payments win them over, challengers must be of a former MasterCard chief exec- startups. And this avalanche of start- compellingly better in some respect. utive, and blue-chip investors Gold- ups follows a period in the history of man Sachs, Citigroup, Morgan Stanley, electronic payments that had already A Long Way to Go Deutsche Bank, and America Online seen vigorous entrepreneurial activity. Many startups peg their ultimate suc- co-founder Steve Case. The hard truth is, very few of those cess on lower acceptance costs. U.S. However, it never had a credible startups succeeded—and only a scant Sen. Richard Durbin’s famous amend- business model, much less a business. number of those emerging now will. ment, along with merchant litigation In 2009, Hogg abandoned the dream, Retail payment networks must and lobbying, have put a spotlight on selling Revolution Money (basically deliver value, be reasonably priced this issue as never before. software and management) to Ameri- relative to value, sufficiently secure, Lower costs for everyone in the can Express Co. -

Les Cahiers De Droit

Document generated on 09/28/2021 10:53 a.m. Les Cahiers de droit Analyse de la trajectoire historique de la monnaie électronique Marc Lacoursière Volume 48, Number 3, 2007 Article abstract In its earliest economic form, money and the means for exchanging it took the URI: https://id.erudit.org/iderudit/043936ar oldest form of swapping : barter, which in time gave way to metal coins and DOI: https://doi.org/10.7202/043936ar then, much later, was replaced by ethereal electronic or “e-money”. During each evolutionary stage, the acceptance of money has rested upon the See table of contents confidence of mediating economic agents. Such confidence may be market-based or backed by government, as when money is issued by a public authority. While this diachronic profile appears at each stage in the Publisher(s) development of money, it becomes most obvious in the evolution of paper money and e-money. This paper sets forth a description of the origins of Faculté de droit de l’Université Laval e-money and analyzes the phenomenon of this specific form of monetary evolution in order to better understand and anticipate the trail that ISSN e-payments will eventually blaze over the Internet. 0007-974X (print) 1918-8218 (digital) Explore this journal Cite this article Lacoursière, M. (2007). Analyse de la trajectoire historique de la monnaie électronique. Les Cahiers de droit, 48(3), 373–448. https://doi.org/10.7202/043936ar Tous droits réservés © Faculté de droit de l’Université Laval, 2007 This document is protected by copyright law. Use of the services of Érudit (including reproduction) is subject to its terms and conditions, which can be viewed online.