Evaluation of Environmental Tax Reforms: International Experiences

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Innovative Sources of Development Finance

Discussion Paper No. 2002/98 Innovative Sources of Development Finance Global Cooperation in the Twenty-first Century Raghbendra Jha* October 2002 Abstract This paper argues that in view of the resource crunch confronting many developing countries and the fall in overseas development aid flows to them, new sources of development finance need to be found. We consider international taxes, fees and levies that could considerably augment aid flows to developing countries and some of which may have coincident beneficial effects. Estimates of the revenue yield from such taxes and levies are also presented. The paper proposes the establishment of a ‘world development organization’ to coordinate such effort. A formula for voting within the organization and another for disbursal of such aid are suggested. Keywords: global taxes, fees and charges, world development organization JEL classification: F02, F35, H23, H87 Copyright UNU/WIDER 2002 * Australia South Asia Research Centre, Research School of Pacific and Asian Studies, Australian National University; email: [email protected] This study has been prepared within the UNU/WIDER project on the Sustainability of External Development Financing, which is directed by Matthew Odedokun. UNU/WIDER gratefully acknowledges the financial contribution to the project by the Ministry for Foreign Affairs of Finland. Acknowledgement I would like to thank Matthew Odedokun and mark McGillivrary for helpful comments and Anurga Sharms for research assistance. All opinions and any errors are mine. UNU World Institute for Development Economics Research (UNU/WIDER) was established by the United Nations University as its first research and training centre and started work in Helsinki, Finland in 1985. -

Oc Undeliverable Refunds Final.Pdf

Sample article for organizations to use to reach customers (288 word count) Customize and post the following article on your websites and/or other communication vehicles to help your customers who may be looking for their federal tax refund. _____________________________________________________________________________________ The IRS may have a refund check waiting for you Thousands of tax refund checks go undelivered every year because people forget to tell the IRS or post office that their address changed. This year, more than 99,000 people are due refund checks averaging $1,547. Could one of them be you? If you think your refund check may have been returned to the IRS as undelivered, you should use the Where’s My Refund? tool on IRS.gov. This tool provides the status of your refund and, in some cases, instructions on how to resolve delivery problems. You can put an end to lost, stolen or undelivered checks by choosing direct deposit when you file either paper or electronic returns. Last year, more than 78.4 million people chose to receive their refund through direct deposit. You can receive refunds directly into your bank account, split a tax refund into two or three financial accounts or even buy a savings bond. You can also file your tax return electronically. E-file eliminates the risk of lost paper returns, reduces errors on tax returns and speeds up refunds. Nearly 8 out of 10 taxpayers chose e-file last year. E-file combined with direct deposit is the best option for avoiding refund problems. Plus, it’s easy, fast and safe. -

Itep Guide to Fair State and Local Taxes: About Iii

THE GUIDE TO Fair State and Local Taxes 2011 Institute on Taxation and Economic Policy 1616 P Street, NW, Suite 201, Washington, DC 20036 | 202-299-1066 | www.itepnet.org | [email protected] THE ITEP GUIDE TO FAIR STATE AND LOCAL TAXES: ABOUT III About the Guide The ITEP Guide to Fair State and Local Taxes is designed to provide a basic overview of the most important issues in state and local tax policy, in simple and straightforward language. The Guide is also available to read or download on ITEP’s website at www.itepnet.org. The web version of the Guide includes a series of appendices for each chapter with regularly updated state-by-state data on selected state and local tax policies. Additionally, ITEP has published a series of policy briefs that provide supplementary information to the topics discussed in the Guide. These briefs are also available on ITEP’s website. The Guide is the result of the diligent work of many ITEP staffers. Those primarily responsible for the guide are Carl Davis, Kelly Davis, Matthew Gardner, Jeff McLynch, and Meg Wiehe. The Guide also benefitted from the valuable feedback of researchers and advocates around the nation. Special thanks to Michael Mazerov at the Center on Budget and Policy Priorities. About ITEP Founded in 1980, the Institute on Taxation and Economic Policy (ITEP) is a non-profit, non-partisan research organization, based in Washington, DC, that focuses on federal and state tax policy. ITEP’s mission is to inform policymakers and the public of the effects of current and proposed tax policies on tax fairness, government budgets, and sound economic policy. -

Income Tax Basics

International Student Taxes Information compiled by International Student Services International Student Taxes • The Basics • Specific Tax Scenarios • What You Can Do Now • Resolving Tax Issues • Top Ten Tax Myths • Tax Resources THE BASICS Tax Basics • Taxes – What are they? – A financial charge imposed by a governing body upon a taxpayer in order to collect funds – Collected funds are used to carry out a variety of functions – There are many types of taxes • Income Tax – A financial charge imposed on income earned by an individual or business – Income can be taxed at the local, state and federal (i.e. national) level. – This session primarily focuses on Federal Income Taxes • Internal Revenue Service (IRS) – The unit of the U.S. federal government responsible for administering and enforcing tax laws – www.irs.gov • Tax Year – January 1 – December 31 • Why should you care about taxes? – Paying income taxes and filing the appropriate paperwork with the IRS is required by law in the U.S. – Failure to comply can result in serious immigration, financial, and legal consequences Income Tax Basics • How are Income Taxes paid? – It is the taxpayer’s (i.e. YOUR) responsibility to pay tax obligation to IRS – Most common process: 1. Portion of your income is withheld from each paycheck throughout the year by your employer 2. Employer pays the withheld income to IRS on your behalf during the year 3. Each year, you file tax return to summarize tax obligations and payments for the prior tax year • What is a tax return? – A report that YOU file with the IRS to… 1. -

Investment in Panama 2019

Investment in Panama 2019 KPMG in Panama Investment in Panama | 1 © 2019 by KPMG © 2012 by KPMG © 2009 by KPMG © 2006 by KPMG © 2000 by KPMG © 1996 by KPMG © 1992 by KPMG Peat Marwick © 1984 by Peat Marwick Mitchell & Co. All rights reserved KPMG, a Panamanian civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. Images of the Panama-Pacific Special Economic Area are courtesy of London and Regional Panama. Investment in Panama | 2 Contents Chapter 1 ...................................................................................................................................................... 9 Panama at a Glance .................................................................................................................................... 9 Geography and Climate ............................................................................................................................ 9 History ....................................................................................................................................................... 9 Government ............................................................................................................................................ 10 Population, Languages and Religion ...................................................................................................... 10 General State Budget ............................................................................................................................. -

Tax Design for Inclusive Economic Growth

OECD Taxation Working Papers No. 26 Bert Brys, Tax Design for Inclusive Sarah Perret, Economic Growth Alastair Thomas, Pierce O’Reilly https://dx.doi.org/10.1787/5jlv74ggk0g7-en OECD CENTRE FOR TAX POLICY AND ADMINISTRATION OECD TAXATION WORKING PAPERS SERIES This series is designed to make available to a wider readership selected studies drawing on the work of the OECD Centre for Tax Policy and Administration. Authorship is usually collective, but principal writers are named. The papers are generally available only in their original language (English or French) with a short summary available in the other. OECD Working Papers should not be reported as representing the official views of the OECD or of its member countries. The opinions expressed and arguments employed are those of the author(s). Working Papers describe preliminary results or research in progress by the author(s) and are published to stimulate discussion on a broad range of issues on which the OECD works. Comments on Working Papers are welcomed, and may be sent to the Centre for Tax Policy and Administration, OECD, 2 rue André-Pascal, 75775 Paris Cedex 16, France. This working paper has been authorised for release by the Director of the Centre for Tax Policy and Administration, Pascal Saint-Amans. Comments on the series are welcome, and should be sent to either [email protected] or the Centre for Tax Policy and Administration, 2, rue André Pascal, 75775 PARIS CEDEX 16, France. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. -

Use IRS Withholding Calculator to Adjust Your Withholding

Sample article for organizations to use to reach customers (320 word count) Customize and post the following article on your websites and/or use in other communication vehicles to inform your readers about how to adjust their withholding. ____________________________________________________________________________ Use IRS Withholding Calculator to Adjust Your Withholding When your federal tax return is completed, you may discover that you’ll either receive a tax refund or owe money. If either of these amounts is substantial, it’s probably time for you to review your withholding election. If you owe a substantial amount of tax, you may need to increase the amount of taxes being withheld from each paycheck you receive. If you are receiving a substantial refund, you may elect to reduce the amount of taxes being withheld from your paychecks. In both cases, the ultimate goal is to get as close to a zero balance at the end of the year as possible. If you find that you owe a significant amount of tax at the end of the year, adjusting your Form W-4 for additional withholding will mean a little less take home pay in each paycheck, but it will eliminate the need to pay taxes at the end of the year. And if you receive a very large refund, a reduction in the amount withheld will mean a little more take home pay in each paycheck to help with day-to-day living expenses. Examples of events that can have a significant impact on your tax liability and require an adjustment to withholding or the number of allowances that you claim on your Form W-4 include: • Change in marital status • Loss of a dependent • Birth or adoption of a child Regardless of your reasons for choosing to review or change your withholdings, IRS provides an excellent interactive online tool to help you make the most informed decision. -

Publication 517, Social Security

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print AH XSL/XML Fileid: … tions/P517/2020/A/XML/Cycle03/source (Init. & Date) _______ Page 1 of 18 11:42 - 2-Mar-2021 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. Publication 517 Cat. No. 15021X Contents Future Developments ............ 1 Department of the Social Security What's New .................. 1 Treasury Internal Reminders ................... 2 Revenue and Other Service Introduction .................. 2 Information for Social Security Coverage .......... 3 Members of the Ministerial Services ............. 4 Exemption From Self-Employment Clergy and (SE) Tax ................. 6 Self-Employment Tax: Figuring Net Religious Earnings ................. 7 Income Tax: Income and Expenses .... 9 Workers Filing Your Return ............. 11 Retirement Savings Arrangements ... 11 For use in preparing Earned Income Credit (EIC) ....... 12 Worksheets ................. 14 2020 Returns How To Get Tax Help ........... 15 Index ..................... 18 Future Developments For the latest information about developments related to Pub. 517, such as legislation enacted after this publication was published, go to IRS.gov/Pub517. What's New Tax relief legislation. Recent legislation pro- vided certain tax-related benefits, including the election to use your 2019 earned income to fig- ure your 2020 earned income credit. See Elec- tion to use prior-year earned income for more information. Credits for self-employed individuals. New refundable credits are available to certain self-employed individuals impacted by the coro- navirus. See the Instructions for Form 7202 for more information. Deferral of self-employment tax payments under the CARES Act. The CARES Act al- lows certain self-employed individuals who were affected by the coronavirus and file Schedule SE (Form 1040), to defer a portion of their 2020 self-employment tax payments until 2021 and 2022. -

Anti-Avoidance and Tax Laws: a Case of Fiji

International Journal of Business and Social Research Volume 09, Issue 03, 2019: 01-20 Article Received: 03-07-2019 Accepted: 28-04-2019 Available Online: 22-07-2019 ISSN 2164-2540 (Print), ISSN 2164-2559 (Online) DOI: http://dx.doi.org/10.18533/ijbsr.v9i3.1165 Anti-Avoidance and Tax Laws: A Case of Fiji Shivneil Kumar Raj1, Mohammed Riaz Azam2 ABSTRACT The pervasiveness of tax avoidance is undoubtedly linked to the tax policies of any country. In Fiji, residents for tax purpose have to disclose income from all sources within and outside Fiji whereas non- resident has to disclose income derived from sources in Fiji. Fiji has a comprehensive tax system put in place with tax laws continued to be amended to curb any loopholes in the system so that everyone pays their fair share of tax. Thus, this research paper applied document analysis methodology. The objective of this research was to highlight Fiji’s position on tax avoidance and how has Fiji addressed such issues identified in Base Erosion Profit Shifting (BEPS). Furthermore, the paper has discussed, Fiji’s tax laws relating to anti-avoidance and provide recommendations to further strengthen and protect Fiji’s tax base from being eroded away through various schemes or arrangements that taxpayer’s might indulge into for the purpose of paying less tax or avoiding tax. The findings indicated that Fiji’s position on tax avoidance issues has remained firm, pro-active and have made substantial progress in regulatory framework and in tax compliance culture. Keywords: Tax, Tax Avoidance, Tax Evasion, Anti-Avoidance, BEPS and Fiji Income Tax Act. -

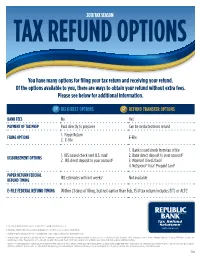

You Have Many Options for Filing Your Tax Return and Receiving Your Refund

2018 TAX SEASON TAX REFUND OPTIONS You have many options for filing your tax return and receiving your refund. Of the options available to you, there are ways to obtain your refund without extra fees. Please see below for additional information. IRS DIRECT OPTIONS REFUND TRANSFER OPTIONS BANK FEES No Yes1 PAYMENT OF TAX PREP Paid directly to preparer Can be deducted from refund 1. Paper Return FILING OPTIONS E-File 2. E-File 1. Bank issued check from tax office 1. IRS issued check sent U.S. mail2 2. Bank direct deposit to your account2 DISBURSEMENT OPTIONS 2. IRS direct deposit to your account2 3. Walmart Direct2Cash3 4. Netspend® Visa® Prepaid Card4 PAPER RETURN FEDERAL IRS estimates within 6 weeks5 Not available REFUND TIMING E-FILE FEDERAL REFUND TIMING Within 21 days of filing, but not earlier than Feb. 15 if tax return includes EITC or ACTC5 1. Consult your tax preparer for the specific amount of this fee and when it will be assessed. 2. It may take additional time for your financial institution to post the refund to your account or for mail delivery. 3. Available at participating Walmart locations for disbursements up to $7,500. An additional one-time $7.00 fee applies. 4. Available at participating tax offices. The Netspend® Visa® Prepaid Card is issued by Republic Bank & Trust Company, member FDIC pursuant to a license from Visa U.S.A. Inc. Netspend®, a TSYS® Company, is a registered agent of Republic Bank & Trust Company. A $5 Monthly Fee will begin upon first load of funds. -

The Economic Effects of a Tax Shift from Direct to Indirect Taxation in France

6 ISSN 2443-8022 (online) The Economic Effects of a Tax Shift from Direct to Indirect Taxation in France Francisco de Castro Fernández, Marion Perelle and Romanos Priftis DISCUSSION PAPER 077 | MARS 2018 EUROPEAN ECONOMY Economic and EUROPEAN Financial Affairs ECONOMY European Economy Discussion Papers are written by the staff of the European Commission’s Directorate-General for Economic and Financial Affairs, or by experts working in association with them, to inform discussion on economic policy and to stimulate debate. The views expressed in this document are solely those of the author(s) and do not necessarily represent the official views of the European Commission. Authorised for publication by Carlos Martínez Mongay, Director for Economies of the Member States II. LEGAL NOTICE Neither the European Commission nor any person acting on behalf of the European Commission is responsible for the use that might be made of the information contained in this publication. This paper exists in English only and can be downloaded from https://ec.europa.eu/info/publications/economic-and-financial-affairs-publications_en. Luxembourg: Publications Office of the European Union, 2018 PDF ISBN 978-92-79-77414-0 ISSN 2443-8022 doi:10.2765/610397 KC-BD-18-004-EN-N © European Union, 2018 Non-commercial reproduction is authorised provided the source is acknowledged. For any use or reproduction of material that is not under the EU copyright, permission must be sought directly from the copyright holders. European Commission Directorate-General for Economic and Financial Affairs The Economic Effects of a Tax Shift from Direct to Indirect Taxation in France Francisco de Castro Fernández, Marion Perelle, Romanos Priftis Abstract This paper uses the European Commission's DSGE model QUEST to investigate the impact of alternative tax reforms shifting the tax burden away from labour or corporates, making the French tax system more growth friendly. -

Capital Gains Withholding

Capital Gains Withholding Emmanuel Saez, Danny Yagan, and Gabriel Zucman1 University of California Berkeley January 2021 Abstract Capital gains income currently escapes taxation for decades and often forever, as the wealthy wait to sell their stock and other assets. We propose capital gains tax withholding as a friendly amendment to existing reform proposals. Under withholding, the very wealthy – the 0.05% with wealth above $50 million – would have to prepay capital gains taxes over a ten-year period. Illiquid entrepreneurs could prepay their cash taxes using a no-risk government loan. Withheld amounts would be credited toward standard capital gains taxes due upon asset sale so that there is no double tax. Withholding improves mark-to-market proposals because valuation uncertainty and price swings do not impact ultimate tax liability under withholding and because illiquid taxpayers can pay cash taxes without liquidation. Withholding complements realization-at-death proposals because withholding generates large revenue from the living, so a future Congress cannot spare the wealthy without giving them obscenely large refunds. An analysis by the Penn Wharton Budget Model estimates that capital gains withholding would enable Congress to raise $2 trillion over the years 2021-2030 even without raising capital gains tax rates. 1 We thank Alan Auerbach, David Gamage, David Kamin, Greg Leiserson, Zach Liscow, Darien Shanske, Joel Slemrod, and numerous conference participants for helpful discussions and comments. Funding from the Center for Equitable Growth and the Stone Center at UC Berkeley is thankfully acknowledged. This document develops an idea briefly mentioned in Saez, Emmanuel and Gabriel Zucman. 2019. “Progressive Wealth Taxation”, Brookings Papers on Economic Activity.