Income Tax Basics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Oc Undeliverable Refunds Final.Pdf

Sample article for organizations to use to reach customers (288 word count) Customize and post the following article on your websites and/or other communication vehicles to help your customers who may be looking for their federal tax refund. _____________________________________________________________________________________ The IRS may have a refund check waiting for you Thousands of tax refund checks go undelivered every year because people forget to tell the IRS or post office that their address changed. This year, more than 99,000 people are due refund checks averaging $1,547. Could one of them be you? If you think your refund check may have been returned to the IRS as undelivered, you should use the Where’s My Refund? tool on IRS.gov. This tool provides the status of your refund and, in some cases, instructions on how to resolve delivery problems. You can put an end to lost, stolen or undelivered checks by choosing direct deposit when you file either paper or electronic returns. Last year, more than 78.4 million people chose to receive their refund through direct deposit. You can receive refunds directly into your bank account, split a tax refund into two or three financial accounts or even buy a savings bond. You can also file your tax return electronically. E-file eliminates the risk of lost paper returns, reduces errors on tax returns and speeds up refunds. Nearly 8 out of 10 taxpayers chose e-file last year. E-file combined with direct deposit is the best option for avoiding refund problems. Plus, it’s easy, fast and safe. -

Form IT-399:2020:New York Depreciation Schedule:It399

Department of Taxation and Finance New York State Depreciation Schedule IT-399 Name(s) as shown on return Identifying number as shown on return Mark an X in one box to show the income tax return you are filing and submit this form with that return. IT-201, Resident IT-203, Nonresident and part-year resident IT-204, Partnership IT-205, Fiduciary Part 1 – Depreciation information for property (except for Internal Revenue Code (IRC) section 280F property) placed in service inside or outside New York State in tax years beginning after December 31, 1980, but before January 1, 1985, and if you elect to continue using IRC section 167 depreciation for property placed in service outside New York State in tax years beginning after December 31, 1984, but before January 1, 1994 (see instructions) A B C D E F G Description of property Date placed Depreciable Depr. Life or New York Federal ACRS (submit schedule if needed) in service basis method rate depreciation deduction (mmddyyyy) .00 .00 .00 .00 .00 .00 .00 .00 .00 1 Enter column F and column G totals ................................................................ 1 .00 .00 Transfer the column F total to: Transfer the column G total to: Form IT-225, line 10, Total amount column and enter Form IT-225, line 1, Total amount column and enter subtraction modification S-210 in the Number column. addition modification A-205 in the Number column. Estates and trusts: If the amount computed is attributable to items reflected in the federal distributable net income, transfer the amounts as stated above. If the amount is not reflected in federal distributable net income, see instructions. -

Evaluation of Environmental Tax Reforms: International Experiences

EVALUATION OF ENVIRONMENTAL TAX REFORMS: INTERNATIONAL EXPERIENCES Final Report Prepared by: Institute for European Environmental Policy (IEEP) 55 Quai au Foin 1000 Brussels Belgium 21 June 2013 Disclaimer: The arguments expressed in this report are solely those of the authors, and do not reflect the opinion of any other party. This report should be cited as follows: Withana, S., ten Brink, P., Kretschmer, B., Mazza, L., Hjerp, P., Sauter, R., (2013) Evaluation of environmental tax reforms: International experiences , A report by the Institute for European Environmental Policy (IEEP) for the State Secretariat for Economic Affairs (SECO) and the Federal Finance Administration (FFA) of Switzerland. Final Report. Brussels. 2013. Citation for report annexes: Withana, S., ten Brink, P., Kretschmer, B., Mazza, L., Hjerp, P., Sauter, R., Malou, A., and Illes, A., (2013) Annexes to Final Report - Evaluation of environmental tax reforms: International experiences . A report by the Institute for European Environmental Policy (IEEP) for the State Secretariat for Economic Affairs (SECO) and the Federal Finance Administration (FFA) of Switzerland. Brussels. 2013. Acknowledgements The authors would like to thank the following for their contributions to the study: Kai Schlegelmilch (Green Budget Europe); Stefan Speck (European Environment Agency - EEA); Herman Vollebergh (PBL – Netherlands Environmental Assessment Agency); Hans Vos (Independent); Mikael Skou Andersen (European Environment Agency – EEA); Frank Convery (University College Dublin); Aldo Ravazzi (Ministry of Environment, Italy); Vladislav Rezek (Ministry of Finance, Czech Republic); Frans Oosterhuis (Institute for Environmental Studies - Vrije Universiteit - IVM); Constanze Adolf (Green Budget Europe); and Janne Stene (Bellona). The authors would also like to thank the members of the Working Group accompanying the study: Carsten Colombier (Leiter) (EFV); Marianne Abt (SECO); Fabian Mahnig (EDA MAHFA); Nicole Mathys (BFE); Reto Stroh (EZV); Michel Tschirren (BAFU); and Martina Zahno (EFV). -

Form 309 Instructions

Arizona Form 2018 Credit for Taxes Paid to Another State or Country 309 For information or help, call one of the numbers listed: those taxes that qualify for a credit under Internal Phoenix (602) 255-3381 Revenue Code (IRC) §§ 901 and 903. From area codes 520 and 928, toll-free (800) 352-4090 NOTE: To claim a credit for taxes paid to a foreign country, Tax forms, instructions, and other tax information you must complete Form 309. You must complete Form 309 If you need tax forms, instructions, and other tax information, even if you did not have to complete federal Form 1116 to go to the department’s website at www.azdor.gov. claim a credit on your federal return. Income Tax Procedures and Rulings You may not claim this credit for the following: These instructions may refer to the department’s income tax • income taxes paid to any city or county, and procedures and rulings for more information. To view or print • interest or penalties paid to another state or country. these, go to our website and click on Reports and Legal NOTE: If you file an amended return after you claim this Research then click on Legal Research and select a document and category type from the drop down menus. credit, be sure to recalculate the credit, if required. Publications Application of Credit To view or print the department’s publications, go to our Claim this credit only if the income was subject to tax in both website and click on Reports and Legal Research then click Arizona and the other state or country in the same tax year. -

Investment in Panama 2019

Investment in Panama 2019 KPMG in Panama Investment in Panama | 1 © 2019 by KPMG © 2012 by KPMG © 2009 by KPMG © 2006 by KPMG © 2000 by KPMG © 1996 by KPMG © 1992 by KPMG Peat Marwick © 1984 by Peat Marwick Mitchell & Co. All rights reserved KPMG, a Panamanian civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. Images of the Panama-Pacific Special Economic Area are courtesy of London and Regional Panama. Investment in Panama | 2 Contents Chapter 1 ...................................................................................................................................................... 9 Panama at a Glance .................................................................................................................................... 9 Geography and Climate ............................................................................................................................ 9 History ....................................................................................................................................................... 9 Government ............................................................................................................................................ 10 Population, Languages and Religion ...................................................................................................... 10 General State Budget ............................................................................................................................. -

State Individual Income Tax Federal Starting Points

STATE PERSONAL INCOME TAXES: FEDERAL STARTING POINTS (as of January 1, 2021) Federal Tax Base Used as Relation to Federal Starting Point to Calculate STATE Internal Revenue Code State Taxable Income ALABAMA --- --- ALASKA no state income tax --- ARIZONA 1/1/20 adjusted gross income ARKANSAS --- --- CALIFORNIA 1/1/15 adjusted gross income COLORADO Current taxable income CONNECTICUT Current adjusted gross income DELAWARE Current adjusted gross income FLORIDA no state income tax --- GEORGIA 3/27/20 adjusted gross income HAWAII 3/27/20 adjusted gross income IDAHO 1/1/20 taxable income ILLINOIS Current adjusted gross income INDIANA 1/1/20 adjusted gross income IOWA Current adjusted gross income KANSAS Current adjusted gross income KENTUCKY 12/31/18 adjusted gross income LOUISIANA Current adjusted gross income MAINE 12/31/19 adjusted gross income MARYLAND Current adjusted gross income MASSACHUSETTS 1/1/05 adjusted gross income MICHIGAN Current (a) adjusted gross income MINNESOTA 12/31/18 adjusted gross income MISSISSIPPI --- --- MISSOURI Current adjusted gross income MONTANA Current adjusted gross income NEBRASKA Current adjusted gross income NEVADA no state income tax --- NEW HAMPSHIRE on interest & dividends only --- NEW JERSEY --- --- NEW MEXICO Current adjusted gross income NEW YORK Current adjusted gross income NORTH CAROLINA 5/1/20 adjusted gross income NORTH DAKOTA Current taxable income OHIO 3/27/20 adjusted gross income OKLAHOMA Current adjusted gross income OREGON 12/31/18 taxable income PENNSYLVANIA --- --- RHODE ISLAND Current adjusted gross income SOUTH CAROLINA 12/31/19 taxable income SOUTH DAKOTA no state income tax --- TENNESSEE on interest & dividends only --- TEXAS no state income tax --- UTAH Current adjusted gross income VERMONT 12/31/19 adjusted gross income VIRGINIA 12/31/19 adjusted gross income WASHINGTON no state income tax --- WEST VIRGINIA 12/31/19 adjusted gross income WISCONSIN 12/31/17 adjusted gross income WYOMING no state income tax --- DIST. -

Use IRS Withholding Calculator to Adjust Your Withholding

Sample article for organizations to use to reach customers (320 word count) Customize and post the following article on your websites and/or use in other communication vehicles to inform your readers about how to adjust their withholding. ____________________________________________________________________________ Use IRS Withholding Calculator to Adjust Your Withholding When your federal tax return is completed, you may discover that you’ll either receive a tax refund or owe money. If either of these amounts is substantial, it’s probably time for you to review your withholding election. If you owe a substantial amount of tax, you may need to increase the amount of taxes being withheld from each paycheck you receive. If you are receiving a substantial refund, you may elect to reduce the amount of taxes being withheld from your paychecks. In both cases, the ultimate goal is to get as close to a zero balance at the end of the year as possible. If you find that you owe a significant amount of tax at the end of the year, adjusting your Form W-4 for additional withholding will mean a little less take home pay in each paycheck, but it will eliminate the need to pay taxes at the end of the year. And if you receive a very large refund, a reduction in the amount withheld will mean a little more take home pay in each paycheck to help with day-to-day living expenses. Examples of events that can have a significant impact on your tax liability and require an adjustment to withholding or the number of allowances that you claim on your Form W-4 include: • Change in marital status • Loss of a dependent • Birth or adoption of a child Regardless of your reasons for choosing to review or change your withholdings, IRS provides an excellent interactive online tool to help you make the most informed decision. -

Publication 517, Social Security

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print AH XSL/XML Fileid: … tions/P517/2020/A/XML/Cycle03/source (Init. & Date) _______ Page 1 of 18 11:42 - 2-Mar-2021 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. Publication 517 Cat. No. 15021X Contents Future Developments ............ 1 Department of the Social Security What's New .................. 1 Treasury Internal Reminders ................... 2 Revenue and Other Service Introduction .................. 2 Information for Social Security Coverage .......... 3 Members of the Ministerial Services ............. 4 Exemption From Self-Employment Clergy and (SE) Tax ................. 6 Self-Employment Tax: Figuring Net Religious Earnings ................. 7 Income Tax: Income and Expenses .... 9 Workers Filing Your Return ............. 11 Retirement Savings Arrangements ... 11 For use in preparing Earned Income Credit (EIC) ....... 12 Worksheets ................. 14 2020 Returns How To Get Tax Help ........... 15 Index ..................... 18 Future Developments For the latest information about developments related to Pub. 517, such as legislation enacted after this publication was published, go to IRS.gov/Pub517. What's New Tax relief legislation. Recent legislation pro- vided certain tax-related benefits, including the election to use your 2019 earned income to fig- ure your 2020 earned income credit. See Elec- tion to use prior-year earned income for more information. Credits for self-employed individuals. New refundable credits are available to certain self-employed individuals impacted by the coro- navirus. See the Instructions for Form 7202 for more information. Deferral of self-employment tax payments under the CARES Act. The CARES Act al- lows certain self-employed individuals who were affected by the coronavirus and file Schedule SE (Form 1040), to defer a portion of their 2020 self-employment tax payments until 2021 and 2022. -

Tax Policy State and Local Individual Income Tax

TAX POLICY CENTER BRIEFING BOOK The State of State (and Local) Tax Policy SPECIFIC STATE AND LOCAL TAXES How do state and local individual income taxes work? 1/9 Q. How do state and local individual income taxes work? A. Forty-one states and the District of Columbia levy broad-based taxes on individual income. New Hampshire and Tennessee tax only individual income from dividends and interest. Seven states do not tax individual income of any kind. Local governments in 13 states levy some type of tax on income in addition to the state income tax. State governments collected $344 billion from individual income taxes in 2016, or 27 percent of state own-source general revenue (table 1). “Own-source” revenue excludes intergovernmental transfers. Local governments—mostly concentrated in Maryland, New York, Ohio, and Pennsylvania—collected just $33 billion from individual income taxes, or 3 percent of their own-source general revenue. (Census includes the District of Columbia’s revenue in the local total.) TABLE 1 State and Local Individual Income Tax Revenue 2016 Revenue (billions) Percentage of own-source general revenue State and local $376 16% State $344 27% Local $33 3% Source: Urban-Brookings Tax Policy Center, “State and Local Finance Initiative Data Query System.” Note: Own-source general revenue does not include intergovernmental transfers. Forty-one states and the District of Columbia levy a broad-based individual income tax. New Hampshire taxes only interest and dividends, and Tennessee taxes only bond interest and stock dividends. (Tennessee is phasing its tax out and will completely eliminate it in 2022.) Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming do not have a state individual income tax. -

Anti-Avoidance and Tax Laws: a Case of Fiji

International Journal of Business and Social Research Volume 09, Issue 03, 2019: 01-20 Article Received: 03-07-2019 Accepted: 28-04-2019 Available Online: 22-07-2019 ISSN 2164-2540 (Print), ISSN 2164-2559 (Online) DOI: http://dx.doi.org/10.18533/ijbsr.v9i3.1165 Anti-Avoidance and Tax Laws: A Case of Fiji Shivneil Kumar Raj1, Mohammed Riaz Azam2 ABSTRACT The pervasiveness of tax avoidance is undoubtedly linked to the tax policies of any country. In Fiji, residents for tax purpose have to disclose income from all sources within and outside Fiji whereas non- resident has to disclose income derived from sources in Fiji. Fiji has a comprehensive tax system put in place with tax laws continued to be amended to curb any loopholes in the system so that everyone pays their fair share of tax. Thus, this research paper applied document analysis methodology. The objective of this research was to highlight Fiji’s position on tax avoidance and how has Fiji addressed such issues identified in Base Erosion Profit Shifting (BEPS). Furthermore, the paper has discussed, Fiji’s tax laws relating to anti-avoidance and provide recommendations to further strengthen and protect Fiji’s tax base from being eroded away through various schemes or arrangements that taxpayer’s might indulge into for the purpose of paying less tax or avoiding tax. The findings indicated that Fiji’s position on tax avoidance issues has remained firm, pro-active and have made substantial progress in regulatory framework and in tax compliance culture. Keywords: Tax, Tax Avoidance, Tax Evasion, Anti-Avoidance, BEPS and Fiji Income Tax Act. -

FACT SHEET Creating a Graduated Income

70 East Lake Street, Suite 1700 Chicago, IL • 60601 www.ctbaonline.org FACT SHEET Creating a Graduated Income Tax March 2012 What is a Graduated Income Tax? A flat income tax structure assesses one tax rate for all taxpayers, regardless of income. Unlike a flat tax, a graduated income tax structure assesses greater tax rates on greater levels of income. A graduated rate structure allows an income tax to adjust its burden in accordance with ability to pay. Thus, it helps create a fair tax system, by imposing a greater tax burden on affluent, than on low and middle income families, when tax burden is measured as a percentage of income. Why does Illinois need a Graduated Income Tax Structure? . The answer is simple, the lack of a graduated income tax rate structure makes the state’s tax system unfair and unsustainable, while hurting the Illinois economy. Creating a graduated income tax structure would help remedy both the unfairness and unsustainability of Illinois’ tax structure. Consider fairness first: o Of all the different ways to tax (sales, property, excise, etc.), the income tax is the fairest because it is the only tax which increases or decreases automatically in accordance with ability to pay. If a taxpayer receives a raise, his or her income tax liability will increase. If on the other hand a taxpayer loses his or her job, income tax liability will decrease. The current Illinois tax system is the opposite of fair, because it places the greatest burden on low and middle income families. Indeed Illinois presently has the third highest tax burden for low income families of all 50 states.1 Consequently, as shown in Figure A, the tax burden of the lowest 20percent of income earners is more than double that of the top 1 percent. -

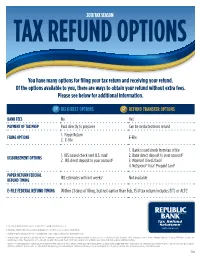

You Have Many Options for Filing Your Tax Return and Receiving Your Refund

2018 TAX SEASON TAX REFUND OPTIONS You have many options for filing your tax return and receiving your refund. Of the options available to you, there are ways to obtain your refund without extra fees. Please see below for additional information. IRS DIRECT OPTIONS REFUND TRANSFER OPTIONS BANK FEES No Yes1 PAYMENT OF TAX PREP Paid directly to preparer Can be deducted from refund 1. Paper Return FILING OPTIONS E-File 2. E-File 1. Bank issued check from tax office 1. IRS issued check sent U.S. mail2 2. Bank direct deposit to your account2 DISBURSEMENT OPTIONS 2. IRS direct deposit to your account2 3. Walmart Direct2Cash3 4. Netspend® Visa® Prepaid Card4 PAPER RETURN FEDERAL IRS estimates within 6 weeks5 Not available REFUND TIMING E-FILE FEDERAL REFUND TIMING Within 21 days of filing, but not earlier than Feb. 15 if tax return includes EITC or ACTC5 1. Consult your tax preparer for the specific amount of this fee and when it will be assessed. 2. It may take additional time for your financial institution to post the refund to your account or for mail delivery. 3. Available at participating Walmart locations for disbursements up to $7,500. An additional one-time $7.00 fee applies. 4. Available at participating tax offices. The Netspend® Visa® Prepaid Card is issued by Republic Bank & Trust Company, member FDIC pursuant to a license from Visa U.S.A. Inc. Netspend®, a TSYS® Company, is a registered agent of Republic Bank & Trust Company. A $5 Monthly Fee will begin upon first load of funds.