Accounting and Office Management for Law Firms

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Medical Office Management Aas.Mdom 2013 – 2014

MEDICAL OFFICE MANAGEMENT AAS.MDOM 2013 – 2014 Associate of Applied Science TEXAS SOUTHMOST COLLEGE Health Care, Career and Technical Education Division A degree in Medical Office Management will prepare the student to handle the functions of receptionist/appointment scheduler, billing specialist, business office coordinator, reimbursement specialist, and/or medical coder. It will also prepare them for positions such as a Medical Office Manager, Billing Supervisor, Office Coordinator, Reception Manager, Hospital Billing Specialist or Medical Records Manager. FIRST YEAR – FALL SEMESTER CREDIT HOURS BCIS 1305 Business Computer Applications…………………………………………………………………………………………………………………… 3 HITT 1305 Medical Terminology I…………………………………………………………………………………………………………………………………. 3 POFM 1317 Medical Administrative Support…………………………………………………………………………………………………………………. 3 MDCA 1309 Anatomy and Physiology for Medical Assistants………………………………………………………………………………………….. 3 SPCH 1315 Public Speaking……………………………………………………………………………………………………………………………………………. 3 SPCH 1318 OR Interpersonal Communication FIRST YEAR – SPRING SEMESTER HRPO 1311 Human Relations………………………………………………………………………………………………………………………………………… 3 POFI 2301 Word Processing……………………………………………………………………………………………………………………………..………….. 3 MDCA 1343 Medical Insurance……………………………………………………………………………………………………………………………………….. 3 POFM 1300 Basic Medical Coding..…………………………………………………………………………………………………………………………………. 3 POFI 1349 Spreadsheets……………………………………………………………………………………………………………………………………………….. 3 HRPO 2301 Human Resources Management…………………………………………………………………………………………………………………. -

Chapter1: Basic Concepts and Trends in Office Management

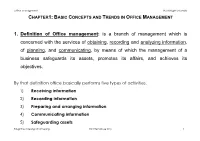

Office Management Build Bright University CHAPTER1: BASIC CONCEPTS AND TRENDS IN OFFICE MANAGEMENT 1. Definition of Office management: is a branch of management which is concerned with the services of obtaining, recording and analyzing information, of planning, and communicating, by means of which the management of a business safeguards its assets, promotes its affairs, and achieves its objectives. By that definition office basically performs five types of activities, 1) Receiving information 2) Recording information 3) Preparing and arranging information 4) Communicating information 5) Safeguarding assets Taught by Soeung Channeang for internal use only 1 Office Management Build Bright University 2. New Trends of Office Management Traditional: Office management functions were limited to basic clerical services and to office personnel Now office management has changed significantly due to corporate downsizing, the economy, and technology. (Please identify the functions of traditional and modern office personnel?) Organizational Traditional Nontraditional charts reflect Supervisory the change Top Management Management from hierarchical (traditional) to Middle Management Middle Management horizontal (nontraditional) management. Supervisory Top Management Management Management from Management from Bottom Up Top Down Taught by Soeung Channeang for internal use only 2 Office Management Build Bright University 3. Administrative Office Management Function The main responsibility is to manage the organizational information by enabling them to enhance their productivity. In the future, this function and services will become even more systems oriented and will use even greater amounts of technology. Objectives of AOM 1. Maximize individual and unit productivity 2. To provide effective management of the organization’s information. 3. To maintain reasonable quantity and quality standards. -

Office Management and Technology College of Rural Alaska 4

Office Management and Technology College of Rural Alaska 4. Complete one of the following concentrations: Business Technologies Division Bookkeeping Bristol Bay Campus (907) 842-5109 a. Complete 20 credits from the following: Chukchi Campus (907) 442-3400 ABUS 101—Principles of Financial Accounting I...........................3 Interior-Aleutians Campus (907) 474-5439 or ABUS 201—Principles of Financial Accounting II................3 Kuskokwim Campus (907) 543-4500 ABUS 141—Payroll Accounting......................................................3 Northwest Campus (907) 443-2201 ABUS 175—Customer Service ........................................................3 Tanana Valley Campus (907) 455-2800 ABUS 220—Microcomputer Accounting: QuickBooks (3) or ABUS/CIOS 221—Microcomputer Accounting (3)...............3 Certificate; A.A.S. Degree CIOS 135—Microcomputer Spreadsheets.......................................3 Minimum Requirements for Certificate: 30 credits; CIOS 164—Alphabetic Filing..........................................................1 for Degree: 61 credits CIOS 165—Office Procedures.........................................................3 CIOS 240—Microcomputer Databases ...........................................3 The program in office management and technology offers career CIOS 276—Independent Project (1-3) education courses in eight concentration areas leading to a certificate, or CIOS 282—Cooperative Work Experience (3)..................1-3 an associate of applied science degree or a departmental certificate Advisor-approved -

Procurement Manager

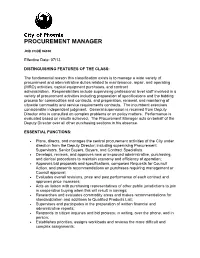

PROCUREMENT MANAGER JOB CODE 04350 Effective Date: 07/13 DISTINGUISHING FEATURES OF THE CLASS: The fundamental reason this classification exists is to manage a wide variety of procurement and administrative duties related to maintenance, repair, and operating (MRO) activities, capital equipment purchases, and contract administration. Responsibilities include supervising professional level staff involved in a variety of procurement activities including preparation of specifications and the bidding process for commodities and contracts, and preparation, renewal, and monitoring of citywide commodity and service requirements contracts. The incumbent exercises considerable independent judgment. General supervision is received from Deputy Director who is consulted on complex problems or on policy matters. Performance is evaluated based on results achieved. The Procurement Manager acts on behalf of the Deputy Director over all other purchasing sections in his absence. ESSENTIAL FUNCTIONS: Plans, directs, and manages the central procurement activities of the City under direction from the Deputy Director; including supervising Procurement Supervisors, Senior Buyers, Buyers, and Contract Specialists. Develops, reviews, and approves new or improved administrative, purchasing, and clerical procedures to maintain economy and efficiency of operation; Approves bid proposals and specifications, composes Requests for Council Action, and presents recommendations on purchases requiring management or Council approval; Evaluates overall revisions, price -

Job Description – Office Assistant/Receptionist

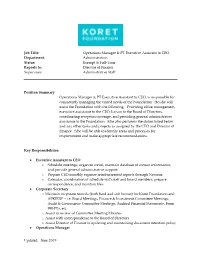

Job Title: Operations Manager & PT Executive Assistant to CEO Department: Administration Status: Exempt & Full-Time Reports to: Director of Finance Supervises: Administrative Staff Position Summary Operations Manager & PT Executive Assistant to CEO, is responsible for consistently managing the varied needs of the Foundation. He/she will assist the Foundation with the following: Providing office management, executive assistance to the CEO, liaison to the Board of Directors, coordinating reception coverage, and providing general administrative assistance to the Foundation. S/he also performs the duties listed below and any other tasks and projects as assigned by the CEO and Director of Finance. S/he will be able to identify areas and processes for improvement and make appropriate recommendations. Key Responsibilities: • Executive Assistant to CEO o Schedule meetings, organize travel, maintain database of contact information, and provide general administrative support. o Prepare CEO monthly expense reimbursement reports through Nexonia o Calendar, coordination of schedule with staff and board members, prepare correspondence, and maintain files • Corporate Secretary o Maintain corporate records (both hard and soft format) for Koret Foundation and AFKIEDF – i.e. Board Meetings, Finance & Investment Committee Meetings, Audit & Governance Committee Meetings, Audited Financial Statements, Form 990-PFs, etc. o Assist in review of Committee Meeting Minutes o Assist with correspondence to the Board of Directors o Assist Director of Finance in updating and maintaining document retention policy • Operations Manager Updated: June 2019 o Manage the administrative staff to meet the needs of the Foundation staff and coordinate office needs – i.e. quarterly board meetings, organization of office supplies, snacks, lunches for staff, etc. -

Administrative Office Management Course Syllabus ‐ ‐ ‐ ‐

AOM 239 OL – Administrative Office Management Course Syllabus ‐ ‐ ‐ ‐ Course Information Course Description: This course is designed to study the basic principles of office management including the areas of recruiting and orienting the office staff, supervising and promoting office personnel, problem solving and communication processes to include coverage of telephone techniques, ergonomics and office productivity. In addition to classroom activities, this course includes 14 hours of assisting in an office setting. Learning Outcomes: Upon successful completion of the course, the student will be able to: • Discuss the role of management in the workplace. • Discuss the levels and functions of management. • Identify and describe challenges that affect administrative managers. • Discuss the major areas of management: human resources, leadership and communications, administrative services, and workplace systems and technology. • Discuss emerging elements impacting administrative management practices. • Define a computer system and discuss the use of networks within the system. • Apply good techniques in the selection and orientation of an office staff. • Discuss the major causes of office personnel problems that affect the well‐being of workers and how these may be handled. • Discuss and demonstrate good supervision skills, as well as good motivation techniques. • Apply good work ethics and business etiquette. • Use problem‐solving skills to handle problems in the office. • Determine and understand group dynamics, the effects of teamwork, and conflict issues. Prerequisites: READ 0810 Course Topics: Management in the workplace; challenges that affect managers; workplace technology; staff orientation; motivation techniques; etiquette; problem‐solving techniques; teamwork; conflict resolution; group dynamics. • Students are expected to read and study text, as assigned before each class. -

Post-Implementation Success Factors for Enterprise Resource Planning (Erp) Student Administration Systems in Higher Education In

University of Central Florida STARS Electronic Theses and Dissertations, 2004-2019 2009 Post-implementation Success Factors For Enterprise Resource Planning (erp) Student Administration Systems In Higher Education In Linda Sullivan University of Central Florida Part of the Educational Leadership Commons Find similar works at: https://stars.library.ucf.edu/etd University of Central Florida Libraries http://library.ucf.edu This Doctoral Dissertation (Open Access) is brought to you for free and open access by STARS. It has been accepted for inclusion in Electronic Theses and Dissertations, 2004-2019 by an authorized administrator of STARS. For more information, please contact [email protected]. STARS Citation Sullivan, Linda, "Post-implementation Success Factors For Enterprise Resource Planning (erp) Student Administration Systems In Higher Education In" (2009). Electronic Theses and Dissertations, 2004-2019. 3884. https://stars.library.ucf.edu/etd/3884 POST-IMPLEMENTATION SUCCESS FACTORS FOR ENTERPRISE RESOURCE PLANNING (ERP) STUDENT ADMINISTRATION SYSTEMS IN HIGHER EDUCATION INSTITUTIONS by LINDA S. SULLIVAN B.P.A. Embry-Riddle Aeronautical University, 1986 M.B.A. Embry-Riddle Aeronautical University, 1988 A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Education in the Department of Educational Research, Technology, and Leadership in the College of Education at the University of Central Florida Orlando, Florida Summer Term 2009 Major Professor: William C. Bozeman © 2009 Linda S. Sullivan ii ABSTRACT This research study investigated the post-implementation experiences of 6 higher education institutions following the initial implementation of a Student Administration ERP system and explored how these institutions used the post-implementation phase to maximize the benefits from the ERP system. -

Office Manager Location: Yangon (Myanmar) Information Pack

OFFICE MANAGER LOCATION: YANGON (MYANMAR) INFORMATION PACK Position Number: 4559 Classification: Austrade Overseas Performance Level 2 Salary: Range from US$11,220 to $13,200 p.a.(gross) Term: Ongoing Engagement Group: Asian Markets Division: International Operations Reports to: Senior Trade Commissioner, Yangon Location: Yangon, Myanmar Security Clearance: Entry Level ABOUT AUSTRADE The Australian Trade and Investment Commission (Austrade) contributes to Australia’s economic prosperity by helping Australian businesses, education institutions, tourism operators, governments and citizens as they: develop international markets and promote international education; win productive foreign direct investment; strengthen Australia’s tourism industry; and seek consular and passport services. To read more about Austrade, please click here and for more on the Executive Group please click here. THE ROLE This position, located at the Austrade office, Australian Embassy in Yangon, provides accounting and administrative support to the Senior Trade Commissioner and the Austrade team in Yangon. In this role, you will: Provide administrative assistance to the Senior Trade Commissioner including: Plan, organise and coordinate daily diary including travel arrangements, meetings and other events as directed by the Senior Trade Commissioner. Handle and maintain highly confidential and sensitive information in a professional manner. Provide assistance to the Senior Trade Commissioner on monthly payments and management of the budget. Perform administrative tasks assigned by the Senior Trade Commissioner. Prepare regular management reports. Page | 1 Provide administrative support to Austrade team in Yangon including: Assist in answering the general enquiries phone line for the Yangon office and receive visitors. Prepare and maintain procurement records and payments for the office. Liaise with Department of Foreign Affairs & Trade (DFAT) accounts team for any tax refunds or shared service payments. -

Total Quality Management in Government| Can TQM Work in a Small VA Facility?

University of Montana ScholarWorks at University of Montana Graduate Student Theses, Dissertations, & Professional Papers Graduate School 1991 Total quality management in government| Can TQM work in a small VA facility? Lee FitzGerald Logan The University of Montana Follow this and additional works at: https://scholarworks.umt.edu/etd Let us know how access to this document benefits ou.y Recommended Citation Logan, Lee FitzGerald, "Total quality management in government| Can TQM work in a small VA facility?" (1991). Graduate Student Theses, Dissertations, & Professional Papers. 3924. https://scholarworks.umt.edu/etd/3924 This Thesis is brought to you for free and open access by the Graduate School at ScholarWorks at University of Montana. It has been accepted for inclusion in Graduate Student Theses, Dissertations, & Professional Papers by an authorized administrator of ScholarWorks at University of Montana. For more information, please contact [email protected]. Maureen and Mike MANSFIELD LIBRARY Copying allowed as provided under provisions of the Fair Use Section of the U.S. COPYRIGHT LAW, 1976. Any copying for commercial purposes or financM gain may be undertaken only with the author's written consent. MontanaUniversity of TOTAL QUALITY MANAGEMENT IN GOVERNMENT: Can TQM Work in a Small VA Facility? By Lee FitzGerald Logan B. A., University of Arizona, 1972 Presented in partial fulfillment of the requirements for the degree of Master's of Public Administration University of Montana 1991 Approved by UMI Number: EP34430 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. -

Audit of the Unfpa Country Office in Somalia Phase I – Operations Management Activities

United Nations Population Fund Delivering a world where every pregnancy is wanted, every childbirth is safe and every young person’s potential is fulfilled. OFFICE OF AUDIT AND INVESTIGATION SERVICES AUDIT OF THE UNFPA COUNTRY OFFICE IN SOMALIA PHASE I – OPERATIONS MANAGEMENT ACTIVITIES FINAL REPORT No IA/2017-01 09 February 2017 AUDIT OF THE UNFPA COUNTRY OFFICE IN SOMALIA – PHASE I – OPERATIONS MANAGEMENT ACTIVITIES TABLE OF CONTENTS EXECUTIVE SUMMARY........................................................................................................................1 I. OBJECTIVES, SCOPE AND METHODOLOGY.................................................................................4 II. BACKGROUND..........................................................................................................................5 III. DETAILED FINDINGS .................................................................................................................6 C. – OPERATIONS MANAGEMENT............................................................................................................................. 6 C.1 – HUMAN RESOURCES......................................................................................................................................................6 C.2 – PROCUREMENT ..............................................................................................................................................................6 Enhance the effectiveness of local procurement of goods and services through redesign -

The Use of Technology-Enabled Human Capital Management Tools in the Practices Of

1 The Use of Technology-Enabled Human Capital Management Tools in the Practices of Hiring, Developing, Managing, and Retaining Talent: Experiences of Top Management of Large Multinational Corporations in Hong Kong A thesis presented by Yat Ngok Rocky Tung to The School of Education In partial fulfilment of the requirements for the degree of Doctor of Education in the field of Organizational Leadership College of Professional Studies Northeastern University Boston, Massachusetts April 2020 2 Abstract Effective and efficient human capital management has been a key attribute contributing to the success of companies. Given the significant technological improvements, company executives have been presented with more, and arguably better, options for enhancing their human capital management efficiency. For employers in Hong Kong, lingering tight labor market conditions as well as rising Chinese demand for Hong Kong’s talent have led to fiercer competition for employees. The primary purpose of this study was to explore the adoption experience of human resources (HR) technology in multibillion-dollar multinational companies (MNCs) with significant operations in Hong Kong. Using the diffusion of innovations theory, this case study answered the following central research question: How do top managers of large multinational corporations in Hong Kong use emerging human resource technologies to hire, manage, develop, and retain employees? This study found that constant and effective communications with both internal and external stakeholders, the presence of a technology-welcoming environment, and the ability to consolidate data inputs from different sources and systems are key elements of the successful incorporation of technologies in companies. Implications for practice and areas for future research are discussed. -

GAO-21-40, Federal Buying Power: OMB Can Further Advance

United States Government Accountability Office Report to Congressional Requesters November 2020 FEDERAL BUYING POWER OMB Can Further Advance Category Management Initiative by Focusing on Requirements, Data, and Training GAO-21-40 November 2020 FEDERAL BUYING POWER OMB Can Further Advance Category Management Initiative by Focusing on Requirements, Data, and Highlights of GAO-21-40, a report to Training congressional requesters Why GAO Did This Study What GAO Found In fiscal year 2019, federal agencies Category management is a government-wide initiative led by the Office of obligated over $350 billion to meet Management and Budget (OMB) that saves the federal government billions of requirements for common products dollars each year by improving how agencies buy common products and and services, such as medical supplies services. Defining requirements is a key first step agencies should take to and computers. Since 2016, OMB has understand what products and services they need before deciding how to buy led efforts to improve how agencies them. However, OMB has primarily focused on the contracting aspects of the buy these products and services initiative, for example, in its guidance and implementation metrics. Leading through the category management practitioners of category management told GAO that agencies could save billions initiative, which directs agencies of additional dollars if OMB focused more on how agencies define requirements, across the government to buy more which is consistent with GAO’s previous findings (see figure). like a single enterprise. OMB has reported the federal government has Office of Management and Budget’s (OMB) Category Management Guidance and Metrics saved $27.3 billion in 3 years through category management.