Swiss Watch Meltdown.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report / 2016 > 163 > Financial Statements

SWATCH GROUP / ANNUAL REPORT / 2016 > 163 > FINANCIAL STATEMENTS NICO (9) FINANCIAL STATEMENTS 2016 CONSOLIDATED FINANCIAL STATEMENTS FINANCIAL STATEMENTS OF THE SWATCH GROUP LTD > 164 SWATCH GROUP / ANNUAL REPORT / 2016 > FINANCIAL STATEMENTS > TABLE OF CONTENTS Consolidated financial statements 164–215 Financial review 165 Consolidated income statement 171 Consolidated balance sheet 172 Consolidated statement of cash flows 174 Consolidated statement of changes in equity 175 Notes to the consolidated financial statements 176–211 1. General information 176 2. Summary of significant accounting policies 176 3. Financial risk management 183 4. Segment information 184 5. Revenues and expenses 187 6. Income taxes 188 7. Earnings per share 190 8. Dividends paid and proposed 190 9. Cash and cash equivalents 191 10. Marketable securities and derivative financial instruments 191 11. Trade receivables 192 12. Other current assets 192 13. Inventories 193 14. Prepayments and accrued income 193 15. Property, plant and equipment 194 16. Intangible assets 195 17. Investments in associates and joint ventures 196 18. Business combinations 196 19. Other non-current assets 198 20. Financial debts and derivative financial instruments 199 21. Other liabilities 199 22. Accrued expenses 200 23. Provisions 200 24. Retirement benefit obligations 201 25. Commitments and contingencies 202 26. Share capital and reserves 203 27. Acquired goodwill 204 28. Details to the consolidated statement of cash flows 205 29. Employee stock option plan 205 30. Related party transactions -

The Impact of the Quartz Crisis in Switzerland Tate Twinam Department of Economics College of William

Trade Shocks and Growth: The Impact of the Quartz Crisis in Switzerland Tate Twinam Department of Economics College of William & Mary Abstract. Agglomeration economies and clustering effects are a key driver of urban growth. They can also be a source of vulnerability when cities and regions specialize in export- intensive industries. Foreign competition and technological change can threaten the survival of exporters, and shocks to these industries can have long-run effects on the communities which rely on them. In this paper, I study the impact of a rapid and large-scale trade shock: The quartz crisis, which devastated the globally dominant Swiss watch industry in the 1970s. I document the geographic agglomeration pattern of the industry and the impact of the crisis on exports, employment, and wages. Using a differences-in-differences strategy, I show that this trade shock led to a large and rapid loss of population in affected areas, and a long-run change in growth patterns. I explore the mechanisms behind this population change, including the role of manufacturing employment and immigration. I discuss the implications of these results for theories of urban growth, and contrast them with recent work on the China shock in Europe and the United States. 1. Introduction Agglomeration economies are widely recognized as a key driver of urban and regional growth. They can also be a source of resilience. Path dependence in the location of eco- nomic activity has allowed many regions to survive and grow despite the irrelevance of their initial natural advantages or immense physical devastation stemming from wars or natural disasters. -

Swiss Watch Industry Study 2020 | an Accelerated Transformation

The Deloitte Swiss Watch Industry Study 2020 | An accelerated transformation About the study This report is the seventh edition of the Deloitte study on the Swiss watch industry. It is based on an online survey and interviews conducted between mid-August and mid-September 2020 with 55 senior executives in the watch industry. The study is also based on an online survey of 5,800 consumers in China, France, Germany, Hong Kong, Italy, Japan, Singapore, Switzerland, the United Arab Emirates, the United Kingdom and the United States. The year 2020 marks 175 years of Deloitte making an impact that matters. Today Deloitte is a thriving global organisation, which has grown to more than 300,000 people proudly carrying forth a legacy of connection and collaboration. We’re not trusted because we’ve existed for 175 years. We’ve existed for 175 years because we’re trustworthy. That’s our legacy. That’s our future. 02 The Deloitte Swiss Watch Industry Study 2020 | An accelerated transformation Contents .+ BUi p^TY^Wc -1 2. Industry overview 05 2.1 COVID-19: Unexpected and unprecedented 05 2.2 Quartz watches: Continuing drop in exports and sales 07 2.3 China: Key for recovery and growth 09 3. Looking ahead 11 3.1 Beyond the pandemic 11 3.2 The Far East and high-end are vital for growth 12 1+ ;XQ\\U^WUc bU]QY^ .0 1+. =hdUb^Q\ bYc[c7 Gb_dUcdc Q^T `_\YdYSc .0 1+/ J]QbdgQdSXUc7 u^Tecdbi ]YccUT dXU R_Qd .1 5. Business strategies 18 2+. <YWYdQ\YcY^W V_b Q mS_^ce]Ub pbcdm g_b\T .5 5.2 The pre-owned market heats up 23 5.3 Sustainability: The future is green 25 6. -

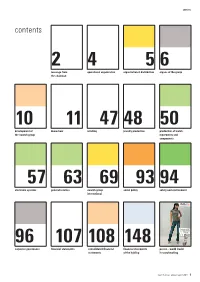

Contents Contents 2 4 5 6 Message from Operational Organization Organization & Distribution Organs of the Group the Chairman

contents contents 2 4 5 6 message from operational organization organization & distribution organs of the group the chairman 10 11 47 48 50 development of know-how retailing jewelry production production of watch, the swatch group movements and components 57 63 69 93 94 electronic systems general services swatch group social policy safety and environment international 96 107 108 148 corporate governance financial statements consolidated financial financial statements poster – world leader statements of the holding in watchmaking swatch group annual report 2004 1 message from the chairman message from the chairman Ladies and Gentlemen, Shareholders, Another year has come to an end. 2004 was in fact a very good year for the Swatch Group despite some major obstacles, the first of which was – and I’m sorry to have to mention it yet again – the problem of the Swiss franc, which con- tinues to rise at a staggering rate compared with all other currencies except the euro and the pound sterling. This is causing serious problems for all of Switzer- land apart from some sections of the financial community. Some of the air of stagnation and resignation, which we see in many of our political leaders, is beginning to spread right across the country. The collapse of Swissair-Swiss then Swiss-Lufthansa is one upsetting and depressing example of this. In fact, I am outraged that in Switzerland, the land of some great business founders of the past, we are no longer able to find enough entrepreneurs capable of preserving and developing the heritage that has been handed down to us, and of which we are the guardians. -

Risks and Opportunities for the Swiss Watch Industry

Copie Juré Copie Conseiller Copie Infothèque Risks and opportunities for the Swiss watch industry Travail de Bachelor réalisé en vue de l’obtention du Bachelor HES par : Alexander Kenel Conseiller au travail de Bachelor : Cyril Pasche Genève, 17.08.2018 Haute École de Gestion de Genève (HEG-GE) Filière économie d’entreprise Déclaration Ce travail de Bachelor est réalisé dans le cadre de l’examen final de la Haute école de gestion de Genève, en vue de l’obtention du titre de Bachelor of Science en économie d’entreprise < … >. L’étudiant a envoyé ce document par email à l'adresse d'analyse remise par son conseiller au travail de Bachelor pour analyse par le logiciel de détection de plagiat URKUND. http://www.urkund.com/fr/student/392-urkund-faq L’étudiant accepte, le cas échéant, la clause de confidentialité. L'utilisation des conclusions et recommandations formulées dans le travail de Bachelor, sans préjuger de leur valeur, n'engage ni la responsabilité de l'auteur, ni celle du conseiller au travail de Bachelor, du juré et de la HEG. « J’atteste avoir réalisé seul< e > le présent travail, sans avoir utilisé des sources autres que celles citées dans la bibliographie. » Fait à Genève, le 13.08.2018 Alexander Kenel Risks and opportunities for the Swiss watch industry KENEL, Alexander 1 Summary In the first part of my bachelor thesis I am presenting the watch industry in Switzerland. My goal is to impart the most essential information to convey a good overview about this highly interesting domain. I am explaining the current state of the sector, but also important historical events like the quartz crisis from the 1970ies. -

Key Figures 2018

PRESS RELEASE Biel/Bienne, 31 January 2019 SWATCH GROUP: KEY FIGURES 2018 • Group net sales increased by 6.1% to CHF 8 475 million at current exchange rates (+5.7% at constant rates). • Operating result increased by 15.2% to CHF 1 154 million. Operating margin increased from 12.5% in the previous year to 13.6%. • Net income increased by 14.8% to CHF 867 million, with a net margin of 10.2% (previous year: 9.5%). • Dividend proposal: increase of 6.7% to CHF 8.00 per bearer share and CHF 1.60 per registered share. • Business slowed in the last three months of the year under review. The month of December in particular was slow, due in part to the very high comparison basis. • Production companies in the Habillage sector (cases, dials, watch hands, etc.) worked at or even above capacity limits, which led to significant delivery delays, mainly for products for Omega and Longines. • Record number of 212 new patent applications in 2018. • Creation of over 1 700 new jobs, mainly in Switzerland. • January 2019 started with solid growth, even in comparison with the very strong January in the previous year. The Swatch Group expects a positive trend in 2019, both in demand and in elimination of capacity bottlenecks. 1 Press release 31 January 2019 Group Key Figures (CHF million) 2018 20171) Change in % at constant currency Total rates effect Net sales 8 475 7 989 + 5.7% + 0.4% + 6.1% Operating result 1 154 1 002 + 15.2% – in % of net sales 13.6% 12.5% Net income 867 755 + 14.8% – in % of net sales 10.2% 9.5% Equity 11 274 11 289 – 0.1% – as a % of balance sheet total 82.5% 83.8% Average return on equity (ROE) 7.7% 6.8% Unaudited figures 1) As of 2018, sales-related transaction costs such as credit card fees are recognized as Other operating expenses. -

Swatch Group Annual Report 2013

SWATCH GROUP ANNUAL REPORT 2013 SWATCH GROUP | ANNUAL REPORT 2013 1 Contents Message from the Chair 2 Operational Organization 4 Organization and Distribution in the World 5 Organs of Swatch Group 6 Board of Directors 6 Executive Group Management Board 8 Extended Group Management Board 9 Development of Swatch Group 10 Big Brands 11 Watches and Jewelry 12–76 Retailing and Presence 77–82 Production 83 Electronic Systems 93 Corporate, Belenos 99 Swatch Group in the World 107 Governance 133 Environmental Policy 134 Social Policy 136 Corporate Governance 138 Financial Statements 2013 151 Consolidated Financial Statements 152 Financial Statements of the Holding 206 Swatch Group’s Annual Report is published in French, German and English. The text on pages 1 to 137 is originally published in French and the text on pages 138 to 216 in German. These original versions are binding. © The Swatch Group Ltd, 2014 2 SWATCH GROUP | ANNUAL REPORT 2013 | MESSAGE FROM THE CHAIR Message from the Chair Dear Madam, Dear Sir, automation, robotics and design. The Swatch SISTEM51 that we Dear Fellow Shareholders, launched in Switzerland in December 2013 is an emblematic example of this philosophy. Swatch Group is the name of the multi-faceted company that we all jointly own. The fact that it was Swatch that gave its name to This change did not only make it possible to create an incredible our company is no coincidence. Thirty-one years ago, the launch number of jobs, thus consolidating the position as a hub of of Swatch saved the Swiss watchmaking industry. On the occa- Swiss industry; it did not only save professions – which today sion of its 30th birthday, which we celebrated with a number of are undoubtedly different but are nonetheless secured; it did events in 2013, Swatch finally reached adulthood. -

The Comeback of the Swiss Watch Industry on the World Market: a Business History of the Swatch Group (1983-2010)

Munich Personal RePEc Archive The comeback of the Swiss watch industry on the world market: a business history of the Swatch Group (1983-2010) Donzé, Pierre-Yves Osaka University, Graduate School of Economics April 2011 Online at https://mpra.ub.uni-muenchen.de/30736/ MPRA Paper No. 30736, posted 06 May 2011 02:26 UTC Discussion Papers In Economics And Business The Comeback of the Swiss Watch Industry on the World Market: A Business History of the Swatch Group (1983-2010) Pierre-Yves DONZÉ Discussion Paper 11-14 Graduate School of Economics and Osaka School of International Public Policy (OSIPP) Osaka University, Toyonaka, Osaka 560-0043, JAPAN The Comeback of the Swiss Watch Industry on the World Market: A Business History of the Swatch Group (1983-2010) Pierre-Yves DONZÉ Discussion Paper 11-14 April 2011 Graduate School of Economics and Osaka School of International Public Policy (OSIPP) Osaka University, Toyonaka, Osaka 560-0043, JAPAN The Comeback of the Swiss Watch Industry on the World Market: A Business History of the Swatch Group (1983-2010)* † Pierre-Yves DONZÉ Abstract The objective of this paper is to contribute to a better understanding of the comeback of the Swiss watch industry on the world market since the end of the 1980s. It focuses on the Swatch Group (SG), currently the world’s biggest watch company. In 1983, the merger of the largest watch group (SSIH) and of the trust controlling the production of parts and movements of watches (ASUAG) into SG was the main measure taken to overcome the Japanese competition. Managed since 1986 by Nicolas G. -

Swatch Group Annual Report 2014

SWATCH GROUP ANNUAL REPORT 2014 SWATCH GROUP 1 ANNUAL REPORT 2014 CONTENTS Message from the Chair 2 Operational Organization 4 Organization and Distribution in the World 5 Organs of Swatch Group 6 Board of Directors 6 Executive Group Management Board 8 Extended Group Management Board 9 Development of Swatch Group 10 Art & Philanthropy 11 Big Brands 15 Watches and Jewelry 16–80 Retailing and Presence 81–86 Production 87 Electronic Systems 97 Corporate, Belenos 103 Swatch Group in the World 111 Governance 137 Environmental Policy 138 Social Policy 140 Corporate Governance 142 Financial Statements 2014 155 Consolidated Financial Statements 156 Financial Statements of the Holding 206 Compensation Report 2014 219 Swatch Group’s Annual Report and Compensation Report are published in French, German and English. Pages 1 to 141 are originally published in French and pages 142 to 218, as well as the Compensation Report, in German. These original versions are binding. © The Swatch Group Ltd, 2015 2 SWATCH GROUP MESSAGE ANNUAL REPORT FROM 2014 THE CHAIR MESSAGE FROM THE CHAIR Dear Madam, Dear Sir, materials; we examine, we explore, we review… and, of course, Dear Fellow Shareholders, we also invent. In 2014, we registered a new patent on average every two days. “Construction site”… a term often used to identify an area where Speaking of the latest skills, we have also always invested in there are still problems to solve. I would like to use it in the way training. Swatch Group employees have bright prospects here: Swatch Group sees it: building, creating something new, devel we train several hundred apprentices and then offer them stable oping, improving, taking the bull by the horns. -

Annual Report / 2017 1 Contents

ANNUAL 2017 REPORT THE EARTH, THE SUN, A YEAR The Earth needs about 365.25 days to complete its gravity-assisted elliptical orbit of the sun. Of course, we generally round this number down and take care of that extra quarter day every four years. Typically, a day consists of 24 hours but we often record its two 12-hour halves. The 8760 hours in Swatch Group’s 2017 were significant. This is their story. SWATCH GROUP / ANNUAL REPORT / 2017 1 CONTENTS MESSAGE FROM THE CHAIR 2 OPERATIONAL ORGANIZATION 4 ORGANIZATION AND DISTRIBUTION IN THE WORLD 5 ORGANS OF SWATCH GROUP 6 BOARD OF DIRECTORS 6 EXECUTIVE GROUP MANAGEMENT BOARD 8 EXTENDED GROUP MANAGEMENT BOARD 9 DEVELOPMENT OF SWATCH GROUP 10 ART & PHILANTHROPY 11 BIG BRANDS 19 WATCHES AND JEWELRY 20 – 84 RETAILING AND PRESENCE 85 – 90 PRODUCTION 91 ELECTRONIC SYSTEMS 101 CORPORATE, BELENOS 107 SWATCH GROUP IN THE WORLD 115 GOVERNANCE 141 ENVIRONMENTAL POLICY 142 SOCIAL POLICY 149 CORPORATE GOVERNANCE 152 FINANCIAL STATEMENTS 2017 165 CONSOLIDATED FINANCIAL STATEMENTS 166 FINANCIAL STATEMENTS OF THE SWATCH GROUP LTD 216 COMPENSATION REPORT 2017 231 PLEIADES Swatch Group’s Annual Report and The Pleiades are an open star cluster in the Compensation Report are published in constellation Taurus. They are part of the French, German and English. Milky Way and can be seen from Earth with Pages 1 to 151 are originally published in the naked eye. Its name connects it not only French and pages 152 to 230, as well as the to the nymphs in Greek mythology, but also Compensation Report, in German. -

Annual Report 2020 24 25

ANNUAL REPORT 2020 24 25 GOVERNANCE CORPORATE RESPONSIBILITY SOCIAL POLICY CORPORATE GOVERNANCE Nathan Wyburn (United Kingdom) THANK YOU Pictures of National Health Service (NHS) workers collected on social media and put together to create an image of a nurse wearing a protective mask, with the words “thank you”. To show respect to the true NHS heroes. SWATCH GROUP / ANNUAL REPORT / 2020 ART IN LOCKDOWN SWATCH GROUP / ANNUAL REPORT / 2020 GOVERNANCE 26 27 www.swatchgroup.com Legal & Functional Requirements Training Standards CORPORATE RESPONSIBILITY Product improvement Materials Homologation Laboratories OUR APPROACH TO SUSTAINABILITY GOVERNANCE compliance with regulatory requirements by all Group companies. Our high standards of quality, safety and sustainability are also CORPORATE RESPONSIBILITY This includes regular courses and training for our employees. Our required of our partners and suppliers. This includes, in particular, The Executive Group Management Board is responsible for en- Group companies are currently subject to various directives and responsible sourcing, i.e. full compliance with our Code of Conduct, Taking responsibility for the protection of life, quality of life, safe- suring compliance with our high standards in the area of sustain- technical specifications, e.g., substances that we exclude from our the principles of our business practices and zero-tolerance policy ty and health, and the protection of our environment are funda- ability. It anchors our ESG principles in our corporate strategy watch components and packaging materials, marketing and label- to human rights violations. As a company with a special responsi- mental concerns of Swatch Group. We endeavor to do the best we and defines concrete targets and measures to achieve them. -

2015 Annual Report Complete En.Pdf

SWATCH GROUP EP. 08 16 7430 ANNUAL REPORT 2015 X CH 7 965 A (ANNUAL REPORT [CH]) 1 MESSAGE FROM THE CHAIR OPERATIONAL ORGANIZATION A ORGANIZATION AND DISTRIBUTION IN THE WORLD 1 ORGANS OF SWATCH GROUP BOARD OF DIRECTORS EXECUTIVE GROUP MANAGEMENT BOARD EXTENDED GROUP MANAGEMENT BOARD DEVELOPMENT OF SWATCH GROUP ART & PHILANTHROPY BIG BRANDS WATCHES AND JEWELRY RETAILING AND PRESENCE PRODUCTION ELECTRONIC SYSTEMS CORPORATE, BELENOS SWATCH GROUP IN THE WORLD GOVERNANCE ENVIRONMENTAL POLICY SOCIAL POLICY CORPORATE GOVERNANCE FINANCIAL STATEMENTS 2015 CONSOLIDATED FINANCIAL STATEMENTS FINANCIAL STATEMENTS OF THE HOLDING COMPENSATION REPORT 2015 Biel/Bienne 10 March 2016 N. Hayek SWATCH GROUP / ANNUAL REPORT / 2015 SWATCH GROUP / ANNUAL REPORT / 2015 ( 1 ) [ CONTENTS ] CONTENTS Message from the Chair 2 Operational Organization 4 Organization and Distribution in the World 5 Organs of Swatch Group 6 Board of Directors 6 Executive Group Management Board 8 Extended Group Management Board 9 Development of Swatch Group 10 Art & Philanthropy 11 Big Brands 17 Watches and Jewelry 18 – 82 Retailing and Presence 83 – 88 Production 89 Electronic Systems 99 Corporate, Belenos 105 Swatch Group in the World 113 Governance 139 Environmental Policy 140 Social Policy 144 Corporate Governance 146 Financial Statements 2015 159 Consolidated Financial Statements 160 Financial Statements of the Holding 210 Compensation Report 2015 223 Swatch Group’s Annual Report and Compensation Report are published in French, German and English. Pages 1 to 145 are originally published in French and pages 146 to 222, as well as the Compensation Report, in German. These original versions are binding. © The Swatch Group Ltd, 2016 ( 2 ) SWATCH GROUP / ANNUAL REPORT / 2015 [ MESSAGE FROM THE CHAIR ] MESSAGE FROM THE CHAIR Dear Madam, Dear Sir, is still the thinnest in the world.