CBL Annual Report 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Economic Review 2015 Government of Liberia

GOVERNMENT OF LIBERIA ANNUAL ECONOMIC REVIEW 2015 MINISTRY OF FINANCE & DEVELOPMENT PLANNING APRIL 2016 ANNUAL ECONOMIC REVIEW | 2015 FOREWORD Together as a nation, and with the help of our macroeconomic management and our firm development partners, we have charted a adherence to convergence criteria. path through the major hurdles of the last We also remain optimistic for 2016, two years, and toward our goal of building a anticipating a revival of major growth sectors, stable and sustainably developed economy, by 2030. In 2014, we united to fight the namely: agriculture, which we project to deadly Ebola Virus Disease (EVD) epidemic, register a 1.4 percent real growth rate, which struck our society and caused a nearly against an estimated 1.0 percent contraction 5 percent setback in our projected 2014 GDP in 2015; mining, which signals some growth. In 2015, we saw the falling global improvement, while remaining below 1 prices of rubber and iron ore – our major percent; and manufacturing, which promises export commodities – slow the domestic a 5.2 percentage-point jump to 11.3 percent, mining and agriculture activities and from an estimated 6.1 percent in 2015. downgrade our real GDP growth projection Moreover, we expect improvement in the from 0.9 percent to 0.3 percent. services sector, especially in the hospitality and tourism sub-sectors, in view of the Yet, in the face of all these challenges, we eradication of EVD. maintained a single-digit inflation rate – closing 2015 at 8.0 percent – through In this fourth edition of its Annual Economic stronger collaboration with the Central Bank Review, or AER 15, the Ministry of Finance & of Liberia (CBL), our commitment to strong Development Planning (MFDP) highlights developments in the real, fiscal, monetary, and external sectors; and elaborates on the J MINISTRY OF FINANCE & DEVELOPMENT PLANNING i 2015 | ANNUAL ECONOMIC REVIEW Government’s efforts to address current Finally, the MFDP expresses its unchanging challenges, while advancing its development gratitude to President Johnson Sirleaf and Her agenda. -

Covert Capital the Kabila Family’S Secret Investment Bank

Covert Capital The Kabila Family’s Secret Investment Bank May 2019 Cover photo: The Sentry. The Sentry • TheSentry.org Covert Capital: The Kabila Family’s Secret Investment Bank May 2019 Executive Summary It would have been hard to understand the significance of Kwanza Capital just by looking at the company’s headquarters in a commercial garage in Kinshasa’s business district. No sign marked its presence. There was nothing to indicate the company was shuffling over one hundred million dollars through accounts held at a bank linked to the family of Joseph Kabila, who served as president of the Democratic Republic of Congo (Congo) from 2001 to January 2019. Nor would onlookers have had reason to suspect that the company was controlled by members of Congo’s former first family and its close allies. Individuals with knowledge of the company’s activities told The Sentry it maintained a low profile by design and the individuals behind Kwanza Capital apparently sought to minimize their public association with the company. Kwanza Capital, which is now reportedly under liquidation, gained only fleeting public notice as it made unusual maneuvers in the country’s banking sector, but its story is more expansive than the public record would suggest. An investigation by The Sentry into Kwanza Capital’s activities provides a new glimpse into how members of Kabila’s family and inner circle have done business. The Sentry examined the firm’s operations, finances, apparent beneficiaries, business partners, and relationships with government agencies and officials. In addition to maintaining extensive links to a bank run by members of Kabila’s family, Kwanza Capital participated in multiple acquisition attempts in the Congolese banking sector. -

Annex a Italian “White List” Countries and Lists of Supranational Entities and Central Banks (Identified by Acupay System LLC As of July 1, 2014)

Important Notice The Depository Trust Company B #: 1361-14 Date: July 17, 2014 To: All Participants Category: Dividends From: International Services Attention: Operations, Reorg & Dividend Managers, Partners & Cashiers Tax Relief – Country: Italy Intesa Sanpaolo S.p.A. CUSIP: 46115HAP2 Subject: Record Date: 12/28/2014 Payable Date: 01/12/2015 EDS Cut-Off: 01/09/2015 8:00 P.M Participants can use DTC’s Elective Dividend System (EDS) function over the Participant Terminal System (PTS) or Tax Relief option on the Participant Browser System (PBS) web site to certify all or a portion of their position entitled to the applicable withholding tax rate. Participants are urged to consult the PTS or PBS function TAXI or TaxInfo respectively before certifying their elections over PTS or PBS. Important: Prior to certifying tax withholding elections, participants are urged to read, understand and comply with the information in the Legal Conditions category found on TAXI or TaxInfo in PTS or PBS respectively. ***Please read this Important Notice fully to ensure that the self-certification document is sent to the agent by the indicated deadline*** Questions regarding this Important Notice may be directed to Acupay 212-422-1222. Important Legal Information: The Depository Trust Company (“DTC”) does not represent or warrant the accuracy, adequacy, timeliness, completeness or fitness for any particular purpose of the information contained in this communication, which is based in part on information obtained from third parties and not independently verified by DTC and which is provided as is. The information contained in this communication is not intended to be a substitute for obtaining tax advice from an appropriate professional advisor. -

Labor Migration and Rural Agriculture Among The

LABOR MIGRATION AND RURAL AGRICULTURE AMONG THE GBANNAH MANO OF LIBERIA by JAMES COLEMAN RIDDELL A THESIS Presented to the Department of Anthropology and the Graduate School of the University of Oregon in partial fulfillment of the requirements for the degree of Doctor of Philosophy June 1970 APPROVED: f V FOREWORD To the anthropologist who is preparing to do research among the Mano of Liberia the descriptions by Harley of the blood-filled Poro ceremonies and the early maps that indicate territory inhabited by cannibals are enough to engender some second thoughts. There is, however, no relationship whatsoever between the reputation the Mano have in the literature and the way they treat visiting anthropologists. Not only did Paramount Chief Dahn and Clan Chief Blah understand the nature of anthropology, but they so enthusiastically supported the research that the towns vied with each other to be included in the sample. This study owes so much to the help given by several residents of Gbannah. My field assistant, Tom B. Sonkarley, approached the research with such vigor that he made it a pleasure to walk five or ten miles in the tropical heat to complete an interview or to witness a ceremony. Also, Tom and I were advised and helped continuously by S. Yini, N. Biin and N. Kokwei, three elders who personally checked any data they thought had been erroniously reported, and alerted us to all pending activities. The citizens of the town of Gipo, who were our hosts for four teen months, deserve a special note of appreciation. Their patience in the face of the constant jntm•ruptions causecl IJy my int<-,rvjewin1r, was truly remarkable. -

Absa Bank 22

Uganda Bankers’ Association Annual Report 2020 Promoting Partnerships Transforming Banking Uganda Bankers’ Association Annual Report 3 Content About Uganda 6 Bankers' Association UBA Structure and 9 Governance UBA Member 10 Bank CEOs 15 UBA Executive Committee 2020 16 UBA Secretariat Management Team UBA Committee 17 Representatives 2020 Content Message from the 20 UBA Chairman Message from the 40 Executive Director UBA Activities 42 2020 CSR & UBA Member 62 Bank Activities Financial Statements for the Year Ended 31 70 December 2020 5 About Uganda Bankers' Association Commercial 25 banks Development 02 Banks Tier 2 & 3 Financial 09 Institutions ganda Bankers’ Association (UBA) is a membership based organization for financial institutions licensed and supervised by Bank of Uganda. Established in 1981, UBA is currently made up of 25 commercial banks, 2 development Banks (Uganda Development Bank and East African Development Bank) and 9 Tier 2 & Tier 3 Financial Institutions (FINCA, Pride Microfinance Limited, Post Bank, Top Finance , Yako Microfinance, UGAFODE, UEFC, Brac Uganda Bank and Mercantile Credit Bank). 6 • Promote and represent the interests of the The UBA’s member banks, • Develop and maintain a code of ethics and best banking practices among its mandate membership. • Encourage & undertake high quality policy is to; development initiatives and research on the banking sector, including trends, key issues & drivers impacting on or influencing the industry and national development processes therein through partnerships in banking & finance, in collaboration with other agencies (local, regional, international including academia) and research networks to generate new and original policy insights. • Develop and deliver advocacy strategies to influence relevant stakeholders and achieve policy changes at industry and national level. -

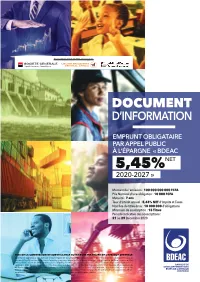

Document Dinformation BDEAC OK OK

Consortium Chef de File, Arrangeurs DOCUMENT D’INFORMATION EMPRUNT OBLIGATAIRE PAR APPEL PUBLIC À L’ÉPARGNE « BDEAC 5,45%NET 2020-2027 » Montant de l’émission : 100 000 000 000 FCFA Prix Nominal d’une obligation : 10 000 FCFA Maturité : 7 ans Taux d’intérêt annuel : 5,45% NET d’Impôts et Taxes Nombre de titres émis : 10 000 000 d’obligations Minimum de souscription : 15 Titres Période indicative des souscriptions : 21 au 29 Décembre 2020 VISA DE LA COMMISSION DE SURVEILLANCE DU MARCHÉ FINANCIER DE L’AFRIQUE CENTRALE La présente opération a été visée par la Commission de Surveillance du Marché Financier de l’Afrique Centrale (COSUMAF) sous le numéro APE---/20 conformément aux dispositions régissant l’appel public à l’épargne sur le Marché Financier Régional, notamment les articles 90 et suivants de l’Acte Uniforme sur le Droit des Sociétés Commerciales et du GIE, 12, alinéa (iv) du Règlement n°06/03 du 12 novembre 2003 portant Organisation, Fonctionnement et Surveillance du Marché Financier de l’Afrique Centrale, 25 et suivants du Règlement Général de la COSUMAF, 1 alinéa (1) de l’Instruction n°2006-01 du 3 mars 2006 relative au document d’information exigé dans le cadre d’un appel public à l’épargne. Le visa de la Commission ne porte pas sur l’opportunité de l’opération envisagée, mais atteste simplement que la COSUMAF a vérifié la pertinence et la cohérence de l’information publiée. I. Sommaire I. SOMMAIRE 02 II. CONDITIONS DE DIFFUSION DU PRESENT DOCUMENT D’INFORMATION 03 III. SIGLES ET ABREVIATIONS 05 IV. -

World Bank Document

RESTRICTED FILE COPY Report No. AF-10a Public Disclosure Authorized This report was prepared for use within the Bank and its affiliated organizations. They do not accept responsibility for its accuracy or completeness. The report may not be published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized THE ECONOMY OF LIBERIA Public Disclosure Authorized September 4, 1963 Public Disclosure Authorized Department of Operations Africa CONTENTS Psage Basic Data Map Summary and Conclusions I. THE BACKGROUND.......................................... 1 The Country and People.................................. 1 The Government........................................ 2 The Political Situation................................. 2 II. THE STRUCTURE OF THE ECONOMY............................ 3 The National Income..................................... 3 The Basis of the Economy................................ 4 The Financial Structure................................. 4 Public Finance........................................ Foreign Trade........................................... 6 III. MAIN ECONOTIC SECTORS................................... 7 Agriculture............................................. 7 Forestry................................................ 9 Fisheries............................................... 10 Kining.................................................. 10 Iron Ore.............................................. 10 Diamonds............................................. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite -

Liberia: Background and U.S

Liberia: Background and U.S. Relations February 14, 2020 Congressional Research Service https://crsreports.congress.gov R46226 SUMMARY R46226 Liberia: Background and U.S. Relations February 14, 2020 Introduction. Congress has shown enduring interest in Liberia, a small coastal West African country of about 4.8 million people. The United States played a key role in the Tomas F. Husted country’s founding, and bilateral ties generally have remained close despite significant Analyst in African Affairs strains during Liberia’s two civil wars (1989-1997 and 1999-2003). Congress has appropriated considerable foreign assistance for Liberia, and has held hearings on the country’s postwar trajectory and development. In recent years, congressional interest partly has centered on the immigration status of over 80,000 Liberian nationals resident in the United States. Liberia participates in the House Democracy Partnership, a U.S. House of Representatives legislative- strengthening initiative that revolves around peer-to-peer engagement. Background. Liberia’s conflicts caused hundreds of thousands of deaths, spurred massive displacement, and devastated the country’s economy and infrastructure, aggravating existing development challenges. Postwar foreign assistance supported a recovery characterized by high economic growth and modest improvements across various sectors. An Ebola outbreak from 2014-2016 cut short this progress; nearly 5,000 Liberians died from the virus, which overwhelmed the health system and spurred an economic recession. The outbreak also exposed enduring governance challenges, including weak state institutions, poor service delivery, official corruption, and public distrust of government. Politics. Optimism surrounding the 2018 inauguration of President George Weah—which marked Liberia’s first electoral transfer of power since 1944—arguably has waned as his administration has become embroiled in a series of corruption scandals and the country has encountered new economic headwinds. -

Licensed Commercial Banks As at July 01, 2020

LICENSED COMMERCIAL BANKS AS AT JULY 01, 2020 S/N NAME ADDRESS OF PHONE FAX SWIFT CODE E-MAIL AND WEBSITE HEADQUARTERS 1. ABC Capital Bank Plot 4 Pilkington Road, +256-414-345- +256-414-258- ABCFUGKA [email protected] Uganda Limited Colline House – Kampala 200 310 P.O. BOX 21091 Kampala [email protected] +256-200-516- 600 https://www.abccapitalbank.co.ug/ 2. Absa Bank Uganda Plot 16 Kampala Road, +256-312-218- +256-312-218- BARCUGKX [email protected] Limited P.O. Box 2971, Kampala, 348 393 Uganda +256-312-218- https://www.absa.co.ug/ 300/317 +256-417-122- 408 3. Afriland First Bank - - - - https://www.afrilandfirstgroup.com/ Uganda Limited 4. Bank of Africa Plot 45, Jinja Road. +256-414-302- +256-414-230- AFRIUGKA [email protected] Uganda Limited P.O. Box 2750, Kampala. 001 902 [email protected] +256-414-302- 111 https://boauganda.com/ 5. Bank of Baroda 18, Kampala Road, +256-414-233- +256-414-230- BARBUGKA Uganda Limited Kampala, Uganda. 680 781 [email protected] P.O. Box 7197, Kampala +256-414-345- https://www.bankofbaroda.ug/ 196 6. Bank of India Picfare House, Plot +256 200 422 +256 414 341 BKIDUGKA Uganda Limited No.37,(Next to NWSC 223 880 [email protected] Head Offices) Jinja Road, Kampala + 256 200 422 https://www.boiuganda.co.ug P.O. Box 7332, Kampala, 224 Uganda + 256 313 400 S/N NAME ADDRESS OF PHONE FAX SWIFT CODE E-MAIL AND WEBSITE HEADQUARTERS 437 7. Cairo International Greenland Towers, Plot +256 (0) 414 +256 (0) 414 CAIEUGKA Bank Limited 30 Kampala Road, 230 132/6/7 230 130 [email protected] Kampala P.O.Box 7052 Kampala, +256 (0) 417 Uganda 230 105 https://www.cib.co.ug/ +256 (0) 414 230 141 8. -

Looking Forward : U.S.- Africa Relations

LOOKING FORWARD: U.S.-AFRICA RELATIONS HEARING BEFORE THE SUBCOMMITTEE ON AFRICA, GLOBAL HEALTH, GLOBAL HUMAN RIGHTS, AND INTERNATIONAL ORGANIZATIONS OF THE COMMITTEE ON FOREIGN AFFAIRS HOUSE OF REPRESENTATIVES ONE HUNDRED SIXTEENTH CONGRESS FIRST SESSION TUESDAY, MARCH 26, 2019 Serial No. 116–19 Printed for the use of the Committee on Foreign Affairs ( Available: http://www.foreignaffairs.house.gov/, http://docs.house.gov, or http://http://www.govinfo.gov U.S. GOVERNMENT PUBLISHING OFFICE 35–615PDF WASHINGTON : 2019 COMMITTEE ON FOREIGN AFFAIRS ELIOT L. ENGEL, New York, Chairman BRAD SHERMAN, California MICHAEL T. MCCAUL, Texas, Ranking GREGORY W. MEEKS, New York Member ALBIO SIRES, New Jersey CHRISTOPHER H. SMITH, New Jersey GERALD E. CONNOLLY, Virginia STEVE CHABOT, Ohio THEODORE E. DEUTCH, Florida JOE WILSON, South Carolina KAREN BASS, California SCOTT PERRY, Pennsylvania WILLIAM KEATING, Massachusetts TED S. YOHO, Florida DAVID CICILLINE, Rhode Island ADAM KINZINGER, Illinois AMI BERA, California LEE ZELDIN, New York JOAQUIN CASTRO, Texas JIM SENSENBRENNER, Wisconsin DINA TITUS, Nevada ANN WAGNER, Missouri ADRIANO ESPAILLAT, New York BRIAN MAST, Florida TED LIEU, California FRANCIS ROONEY, Florida SUSAN WILD, Pennsylvania BRIAN FITZPATRICK, Pennsylvania DEAN PHILLIPS, Minnesota JOHN CURTIS, Utah ILHAN OMAR, Minnesota KEN BUCK, Colorado COLIN ALLRED, Texas RON WRIGHT, Texas ANDY LEVIN, Michigan GUY RESCHENTHALER, Pennsylvania ABIGAIL SPANBERGER, Virginia TIM BURCHETT, Tennessee CHRISSY HOULAHAN, Pennsylvania GREG PENCE, Indiana TOM -

Cbl Strategic Objectives

CENTRAL BANK OF LIBERIA STRATEGIC PLAN • 2017-2019 THIS PAGE IS BLANK ON PURPOSE CONTENTS CONTENTS ....................................................................................................................................................... i FOREWORD ................................................................................................................................................... iii ACKNOWLEDGEMENTS ........................................................................................................................... v ABBREVIATIONS ......................................................................................................................................... vi EXECUTIVE SUMMARY........................................................................................................................... viii SECTION 1: INTRODUCTION .................................................................................................................. 1 SECTION 2: OVERVIEW OF THE CBL ................................................................................................ 16 SECTION 3: CBL SITUATIONAL ANALYSIS...................................................................................... 26 SECTION 4: CBL STRATEGIC OBJECTIVES ...................................................................................... 38 SECTION 5: IMPLEMENTATION OUTLINE ..................................................................................... 46 SECTION 6: PERFORMANCE MANAGEMENT, MONITORING & EVALUATION