From FM to DAB+ Final Report of the Digital Migration Working Group Digital Migration – Imprint Page 2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Quickline Senderangebot

Sprachpakete Français CHF 7.90/Mt. Italiano CHF 8.90/Mt. Quickline National Cartoon Network TMC Monte Carlo Boing Geographic Italia TCM Turner Senderangebot Classic Movies Canale 5 Rai 3 Top Calcio 24 Rai 4 HD Premium CHF 19.00/Mt. Iris Rete 4 Italia 1 Video Italia auto motor und sport HD d National Geographic HD d/e CHF 6.90/Mt. English La 7d AXN HD d National Geographic Wild HD d/e d PLANET Boomerang Cartoon Network Animal Planet HD* HD Planet HD d National Turkish CHF 4.90/Mt. Geographic TNT Film Classica HD d Romance TV HD d TNT Serie TM atv Türkiye Show TV Discovery Channel HD d SyFy HD d/e ESPN America HD e TNT Film HD d/e Sprachpakete à la carte Eurosport HD d TNT Serie HD d/e Albanian CHF 19.90/Mt. Brazilian CHF 36.90/Mt. Russian CHF 9.90/Mt. Bosnian CHF 14.90/Mt. FOX HD d/e Travel Channel HD e RTV 21 und TV Globo RTVi Hayat BH Koha Vision International * HD-Version im Verlauf des Jahres 2013 verfügbar Turkish Portuguese CHF 4.90/Mt. Serbian CHF 24.90/Mt. Hayat Folk Pink Plus, Pink Extra Lig TV CHF 28.90/Mt. SIC International Pink Music, pinkids Hayat Plus Grundangebot (unverschlüsselt, ohne Mehrkosten erhältlich) TürkMax CHF 5.90/Mt. (SinemaTurk) Über 130 TV-Sender (davon 21 in HD), über 150 Radiosender Deutsch Das Vierte ORF 1 HD VIVA CH HD Quickline Radio Senderliste SRF 1 Deutsche Welle TV ORF 2 VOX Schweizer Programmsender im Grundangebot SRF 1 HD Deluxe Music TV ORF 2 HD WDR Argovia Classic Rock | Country Radio Switzerland | FM1 St. -

DISCOVER NEW WORLDS with SUNRISE TV TV Channel List for Printing

DISCOVER NEW WORLDS WITH SUNRISE TV TV channel list for printing Need assistance? Hotline Mon.- Fri., 10:00 a.m.–10:00 p.m. Sat. - Sun. 10:00 a.m.–10:00 p.m. 0800 707 707 Hotline from abroad (free with Sunrise Mobile) +41 58 777 01 01 Sunrise Shops Sunrise Shops Sunrise Communications AG Thurgauerstrasse 101B / PO box 8050 Zürich 03 | 2021 Last updated English Welcome to Sunrise TV This overview will help you find your favourite channels quickly and easily. The table of contents on page 4 of this PDF document shows you which pages of the document are relevant to you – depending on which of the Sunrise TV packages (TV start, TV comfort, and TV neo) and which additional premium packages you have subscribed to. You can click in the table of contents to go to the pages with the desired station lists – sorted by station name or alphabetically – or you can print off the pages that are relevant to you. 2 How to print off these instructions Key If you have opened this PDF document with Adobe Acrobat: Comeback TV lets you watch TV shows up to seven days after they were broadcast (30 hours with TV start). ComeBack TV also enables Go to Acrobat Reader’s symbol list and click on the menu you to restart, pause, fast forward, and rewind programmes. commands “File > Print”. If you have opened the PDF document through your HD is short for High Definition and denotes high-resolution TV and Internet browser (Chrome, Firefox, Edge, Safari...): video. Go to the symbol list or to the top of the window (varies by browser) and click on the print icon or the menu commands Get the new Sunrise TV app and have Sunrise TV by your side at all “File > Print” respectively. -

NEUE WELTEN ENTDECKEN MIT SUNRISE TV TV-Senderliste Für Den Ausdruck

NEUE WELTEN ENTDECKEN MIT SUNRISE TV TV-Senderliste für den Ausdruck Sie brauchen Hilfe? Hotline Mo - Fr 08.00 - 22.00 Uhr Sa - So 10.00 - 22.00 Uhr 0800 707 707 Hotline aus dem Ausland (gratis mit Sunrise Mobile) +41 58 777 01 01 Sunrise Shops Sunrise Shops Sunrise Communications AG Thurgauerstrasse 101B / Postfach 8050 Zürich 03|2021 Stand Deutsch Herzlich Willkommen bei Sunrise TV Mit dieser Übersicht finden Sie Ihre Lieblingssender schnell und unkompliziert. Das Inhaltsverzeichnis auf Seite 4 dieses PDF-Dokuments zeigt Ihnen, welche Seiten des Dokuments für Sie relevant sind – je nachdem, welches der Sunrise TV-Pakete TV start, TV comfort und TV neo und welche zusätzlichen Premiumpakete Sie gebucht haben. Sie können im Inhaltsverzeichnis weiter klicken zu den Seiten mit den gewünschten Senderlisten – nach Sender- namen oder alphabetisch geordnet – oder direkt die für Sie relevanten Seiten ausdrucken. 2 Anleitung zum Drucken Legende Falls Sie das vorliegende PDF-Dokument mit Adobe Acrobat Comeback TV steht für die Möglichkeit, TV Sendungen bis 7 Tage Reader geöffnet haben: nach Ihrer Ausstrahlung anschauen zu können (30h bei TV start). Ausserdem können Sie mit Comeback TV die Sendung neu starten, Klicken Sie über die Symbolleiste von Acrobat Reader die anhalten, vor- und zurückspulen. Menübefehle „Datei > Drucken“ an. HD steht für High Definition („hohe Auflösung“) und bezeichnet Falls Sie das PDF-Dokument mit einem Internetbrowser hochauflösendes Fernsehen und Video. (Chrome, Firefox, Edge, Safari…) geöffnet haben: Mit der neuen haben Sie Sunrise TV immer dabei. Klicken Sie in der Symbolleiste oder im oberen Bereich Ihres Sunrise TV App Mit allem, was Sunrise Smart TV so einzigartig macht: Live TV in HD, Browserfensters (je nach Browsertyp) das Druckersymbol oder Comeback TV Agent, Programmtipps, Senderlisten und alle Ihre die Menübefehle „Datei > Drucken“ an. -

Peter H. Seeberger

Peter H. Seeberger Max-Planck Institute for Colloids and Interfaces Freie Universität Berlin Department for Biomolecular Systems Inst. for Chemistry and Biochem. Am Mühlenberg 1 Arnimallee 22 14476 Potsdam 14195 Berlin GERMANY GERMANY Tel: +49-331-567-9300; Fax: +49-331-567-59302 [email protected] Education 1995, May Ph.D. in Biochemistry University of Colorado at Boulder, USA Thesis advisor: Prof. M.H. Caruthers 1989, November B.S. in Chemistry University of Erlangen-Nürnberg, D Experience 2011 - 2012 Managing Director Max-Planck Inst. for Colloids and Interfaces, Potsdam, D 2011 - Honorary Professor of Chemistry Potsdam University, Potsdam, D 2009 - Director, Department for Biomolecular Systems Max-Planck Institute for Colloids and Interfaces, Potsdam, D 2009 - Professor of Chemistry Free University of Berlin, Berlin, D 2003 - 2014 Affiliate Professor The Burnham Institute, La Jolla, USA 2008 Chair, Laboratory for Organic Chemistry Swiss Federal Institute of Technology (ETH) Zurich, CH 2003 - 2009 Professor of Chemistry Swiss Federal Institute of Technology (ETH) Zurich, CH 2002 - 2003 Firmenich Associate Professor of Chemistry Massachusetts Institute of Technology, Cambridge, USA 1998 - 2002 Assistant Professor of Chemistry Massachusetts Institute of Technology, Cambridge, USA 1995 - 1997 Research Fellow Sloan-Kettering Institute for Cancer Research, New York; USA Mentor: Prof. S.J. Danishefsky Awards and Honors 2018 Gusi Peace Prize 2018 Ernst Hellmut Vits-Prize, Univ. Münster 2017 Wissenschaftspreis des Stifterverbandes 2015 Humanity in Science Award 2013 Member, Berlin-Brandenburg Academy of Sciences 2013 C. S. Hamilton Award for Organic Chemistry Univ. of Nebraska 2012 “Honorary Visiting Professor”, Jiangnan University 2012 Whistler Award, Int. Carb. Organization 2011 Hans Herloff Inhoffen-Medal, TU Braunschweig 2010 Tetrahedron Young Investigator Award Bioorg. -

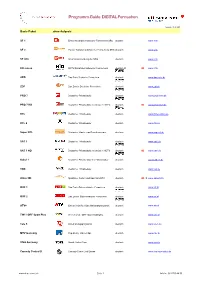

Programm-Guide DIGITAL-Fernsehen

Programm-Guide DIGITAL-Fernsehen Ausgabe Dez. 2007 Basic-Paket ohne Aufpreis SF 1 Erster Kanal des Schweizer Fernsehens SRG deutsch www.sf.tv SF 2 Zweiter Kanal des Schweizer Fernsehens SRG deutsch www.sf.tv SF info Informationssendung der SRG deutsch www.sf.tv HD suisse HDTV-Kanal des Schweizer Fernsehens deutsch./it HD www.sf.tv ARD Das Erste Deutsche Fernsehen deutsch www.daserste.de ZDF Das Zweite Deutsche Fernsehen deutsch www.zdf.de PRO 7 Deutscher Privatsender deutsch www.prosieben.de PRO 7 HD Deutscher Privatsender, teilweise in HDTV deutsch HD www.prosieben.de RTL Deutscher Privatsender deutsch www.rtl-television.de RTL 2 Deutscher Privatsender deutsch www.rtl2.de Super RTL Deutscher Kinder- und Familiensender deutsch www.superrtl.de SAT 1 Deutscher Privatsender deutsch www.sat1.de SAT 1 HD Deutscher Privatsender, teilweise in HDTV deutsch HD www.sat1.de Kabel 1 Deutscher Privatsender mit Filmklassiker deutsch www.kabel1.de VOX Deutscher Privatsender deutsch www.vox.de Anixe HD Spielfilme, Serien und Sport in HDTV deutsch HD ● www.anixehd.tv ORF 1 Das Erste Österreichische Fernsehen deutsch www.orf.at ORF 2 Das Zweite Österreichische Fernsehen deutsch www.orf.at ATV+ Österreichisches Unterhaltungsprogramm deutsch www.atv.at TW1 / ORF Sport Plus Wetterkanal / ORF Sport Highlights deutsch www.tw1.at Tele 5 Unterhaltungsprogramm deutsch www.tele5.de MTV Germany Pop-Musik, Video-Clips deutsch www.mtv.de VIVA Germany Musik, Video-Clips deutsch www.viva.tv Comedy Central D Comedy-Serien und Shows deutsch www.comedycentral.de www.rii-seez-net.ch Seite 1 Infoline 081 755 44 99 Programm-Guide DIGITAL-Fernsehen Ausgabe Dez. -

Solnet Radio Senderliste Nr. Sender-Logo Sender Sprache

August 2020 SolNet Radio Senderliste Nr. Sender-Logo Sender Sprache 1 Radio SRF 1 Deutsch 2 Radio SRF 3 Deutsch 3 Swiss POP Deutsch 4 SRF Musikwelle Deutsch 5 Radio SRF 2 Deutsch 6 Radio 24 Deutsch 7 Energy Zürich Deutsch 8 Radio SRF 4 News Deutsch 9 FM1 Nord Deutsch 10 FM1 Sud Deutsch 11 Radio Central Deutsch 12 Argovia Deutsch 13 Radio Zürisee Deutsch 14 Radio Kanal 8610 Deutsch 15 Pilatus Deutsch 16 Swiss Classic Deutsch 17 Radio Top Deutsch 18 Radio 32 Deutsch 19 Radio 32 Goldies Deutsch 20 Radio Basilisk Deutsch 21 Radio 1 Deutsch 22 SRF Virus Deutsch 23 Radio Sunshine Deutsch 24 Energy Bern Deutsch 25 Energy Basel Deutsch 26 Swiss Jazz Deutsch 1 17. August 2020 BSE Software GmbH, Glutz Blotzheimstrasse 1, CH-4500 Solothurn August 2020 SolNet Radio Senderliste 27 Radio Bern1 Deutsch 28 Radio BeO Deutsch 29 20 Minuten Radio Deutsch 30 Radio Freiburg Deutsch 31 neo1 Deutsch 32 radio rottu oberwallis Deutsch 33 swiss melody Deutsch 34 müsig pur Deutsch 35 Radio X Deutsch 36 Radio Life Channel Deutsch 37 Radio Munot Deutsch 38 Canal 3 Deutsch 39 Radio Grischa Deutsch 40 Radio Top Two Deutsch 41 Radio Inside Deutsch 42 Radio LoRa Deutsch 43 Toxic.fm Deutsch 44 Radio Bern RaBe Deutsch 45 Kanal K Deutsch 46 Kick Ass Radio Deutsch 47 Radio Stadtfilter Deutsch 48 Radio Rasa Deutsch 49 Radio Luna Deutsch 50 Radio Melody Deutsch 51 Radio DASDING Deutsch 52 Klassik Radio Deutsch 53 SWR1 Deutsch 2 17. August 2020 BSE Software GmbH, Glutz Blotzheimstrasse 1, CH-4500 Solothurn August 2020 SolNet Radio Senderliste 54 SWR2 Deutsch 55 SWR3 Deutsch -

Digitalradio: Gesuch Der SRG SSR Idée Suisse Um Die Erteilung Von Zwei Radio-Programmkonzessionen

SRG SSR idée suisse Digitalradio: Gesuch der SRG SSR idée suisse um die Erteilung von zwei Radio-Programmkonzessionen Radio digitale: Requête de SRG SSR idée suisse pour l'octroi de deux concessions de programmes radio 28. Oktober 2006 / 6. Februar 2007 Inhaltsverzeichnis 1 Gesuch 1: Informationskanal SR DRS (Arbeitstitel INKA) 11 Übersicht gemäss Formular BAKOM 2 2ème requête: World Radio Switzerland 21 Vue d'ensemble selon la marche à suivre de l'OFCOM 3 Gemeinsame Angaben 31 Konzession: Änderungsvorschlag 32 Distributionsstrategie 33 Gebührenfinanzierung 1 Gesuch 1: DRS News-Programm auf DAB 11 Übersicht gemäss BAKOM-Schema 1. Zusammenfassung und Übersicht Das DRS News-Programm ist der Informationskanal von Schweizer Radio DRS. Der Kanal orientiert sich an den erfolgreichen Vorbildern von BBC, France info, Info-Radio Berlin- Brandenburgoder Bayern 5. Als Informationssender erfüllt er einen Kernauftrag des Service public, indem er zu Meinungsbildung eines relevanten Publikumssegments (berufstätig, mobil, eher älter, eher gebildet) beiträgt. Als Marktziel sterbt das DRS-News-Programm hohe Reichweiten bei durchschnittlichen Hördauern von 30 bis 60 Minuten an. Grosse Marktanteile mit langen Hördauern sind nicht das Ziel. Aus diesem Grund wird DRS News die marktanteilsorientierten Lokalradio- und Begleitprogramme mit langer Hördauer nicht konkurrenzieren. Verschiebungen von Höreranteilen sind eher für die eigenen Informationssendungen auf DRS1, 2 und 3 zu erwarten, sollen aber durch geschickte Programmabstimmungen in Grenzen gehalten werden. Das News-Programm wird als terrestrisch empfangbares Digitalradioprogramm verbreitet (T-DAB). Der Zeitpunkt des Konzessionsgesuchs ist bewusst mit der öffentlichen Ausschreibung der zweiten T-DAB-Plattform in der deutschsprachigen Schweiz koordiniert. Das Programm erfüllt die Anforderung, das digitale Radioangebot inhaltlich zu bereichern und damit dem Digitalradio in der Schweiz zum gewünschten Auftrieb zu verhelfen. -

Full Programme of the 2012 Conference

PATRONS, SPONSORS & FRIENDS The Geneva Writers’ Conference is wholly non-profi t and is made possible through registration fees and through the generous support of: Patrons Fondation de Groot Hewlett Packard, Genève Webster University, Bellevue Sponsors OffTheShelf English Bookshop Geneva Press Club Friends American International Club, Geneva American International Women’s Club, Geneva American International Women’s Club, Lausanne Bergli Books, Basel BooksBooksBooks, Lausanne 8 TH Hello Switzerland Genève Tourisme International Herald Tribune, Zurich GENEVA International PEN, Centre Suisse Romand International Women’s Writing Guild, New York WRITERS’ Paris Writers News Payot Librairie–Chantepoulet, English Books Radio Frontier CONFERENCE Stauffacher English Bookshop, Bern Swiss News www.LivingInNyon World Radio Switzerland 3–5 GENEVA WRITERS’ CONFERENCE COMMITTEE February Liz Boquet Lang-Hoan Pham 2012 Amanda Callendrier Bob Piller Katie Hayoz Jo Ann Hansen Rasch Karen McDermott Pierre-Yves Tiberghien Sue Niewiarowski Susan Tiberghien Daniela Norris John Zimmer Mary Pecaut For further information, please see the website: www.genevawritersgroup.org Or contact: Susan Tiberghien [email protected] Katie Hayoz [email protected] Karen McDermott [email protected] THE CONFERENCE PROGRAM The 8th Geneva Writers’ Conference welcomes FRIDAY / 3 FEBRUARY writers from around the world to a weekend of work- 17:30 Early Registration shops and panels led by well-known authors, agents, editors and publishers from France, Italy, Switzer- 19:00 Opening Buffet, land, the UK andand thethe USA. Participant Readings The goal is to bring together English-language writ- SATURDAY / 4 FEBRUARY ers for high-level instruction, support and feedback through workshops, discussions, and readings. The 09:00 Registration Conference instructors are experienced in teaching 10:00 Welcome creative writing and committed to sharing their knowl- 10:30 Session I edge, skills, and perspectives on writing as an art 12:30 Lunch and as a profession. -

PRESS RELEASE DAB+ Digital Radio On-Air at Geneva International Motor Show 5-15 March 2015

PRESS RELEASE DAB+ Digital Radio on-air at Geneva International Motor Show 5-15 March 2015 London, 26 February 2015 Digital radio is on-air again at Geneva Motor Show 2015. Once again the automobile industry is at the heart of DAB+ digital radio in Switzerland. This year the automobile industry will be able to tune in to a variety of DAB+ services from the public broadcast SRG-SSR and from the commercial broadcasters. Switzerland presents the perfect use case for digital radio in car with 100% coverage of autobahns (1764km) and a clear plan for coverage of tunnels (which make up a proportion of road in Switzerland). There are 70,000km of roads in Switzerland which have 98% coverage of a digital radio signal. In a press release today from MCDT, the digital radio marketing body for Switzerland, it was reported that "Some 382,000 DAB+ radios were sold in Switzerland last year. As at the end of 2014, there were 1.9 million digital radios in use in Swiss households and vehicles. DAB+ digital radio is set to pass the two-million mark very soon.” Switzerland is committed to digital radio and is one of the countries currently discussing the switch off of FM, following the announcement of the first FM switch off which will take place in Norway in 2017 (or latest 2019). Countries around Europe are now considering the future of radio and ensuring radio is part of today’s digital world. The impact of this on the automotive sector is that all of the major automotive brands now offer digital radio solutions, and many are moving towards digital radio as standard in the mature digital radio markets (UK, Switzerland, Norway). -

Andre LIEBICH 01 2018 Degrees 2013 1974 Dr. H.C. Babes-Bolyai

Andre LIEBICH 01 2018 Degrees 2013 Dr. h.c. Babes-Bolyai University 1974 Ph.D., Political Science, Harvard University 1970 A.M., Regional Studies-USSR, Harvard University 1968 B.A.(Hons) Pol Science & Economics, McGill University Appointments 2013- Honorary Professor of International History and Politics, Graduate Institute 1989-13 Professor of International History and Politics, Graduate Institute of International and Development Studies, Geneva ( - 2008 Graduate Institute of International Studies, HEI) 1982-91 Professor, Political Science, Université du Québec à Montréal (UQAM) 1978-82 Associate Professor, Political Science, UQAM 1974-78 Assistant Professor, Political Science, UQAM 1973-74 Lecturer Political Science, UQAM 1972-73 Junior Associate Member, St. Antony's College, Oxford 1971-72 Teaching Fellow, Government, Harvard Concurrent Appointments 2016-17 Visiting Professor, Global Studies Institute, Université de Genève 2015 aut Visiting Fellow, Institut für Wissenschaft vom Menschen, Vienna 2010 trinity Academic Visitor, Nuffield College, Oxford 2010 hil/trin Senior Research Associate, Modern European History Research Centre, Oxford 2010 hilary Senior Associate Member, St. Antony's College, Oxford 2002-03 Visiting Research Fellow, Institute of Historical Research, London 1997-98 Member, Institute for Advanced Study, Princeton 1996-97 Sessional Lecturer, Faculté des Lettres, Université de Fribourg CH 1990-96 Lecturer, ITC, Program in Strategic & International Studies, Geneva 1990-93 Faculty Lecturer, Colgate University Program in -

Curriculum Vitae

CURRICULUM VITAE PERSONAL INFORMATION Dr. Francesca Falk Date of birth: 17 January 1977 Married, two children (2012/2016) Swiss and Italian dual-citizen [email protected] https://www.hist.unibe.ch/ueber_uns/personen/falk_francesca/index_ger.html ACADEMIC POSITIONS 8/2019 Lectureship (Dozentur) in Migration History, University of Bern, Switzerland 2013–2019 Senior Lecturer in Contemporary History at the bilingual French-German University of Fribourg, Switzerland 2016–17 Advanced Postdoc Mobility Fellowship (with return phase), Swiss National Science Foundation, Switzerland 2012 Lecturer at the ETH Zurich (History of the Modern World), Switzerland 2009–2012 Lecturer at the University of Basel, Switzerland 2009–2012 Swiss National Science Foundation Postdoc Grant in the framework of the ‘Representative Violence’ project, Zurich University of the Arts, Switzerland 2005–2008 PhD National Centre of Competence in Research Eikones (The Power and Meaning of Images), University of Basel, Switzerland EDUCATION 2009 PhD in History, University of Basel, Switzerland, thesis: 5.5; thesis defence: 6 (6 = highest mark) 2005 MA in History and Political Science, Universities of Basel and Zurich, Switzerland; with studies in Basel, Geneva, and Zurich (Switzerland) and Freiburg im Breisgau (Germany), summa cum laude RESEARCH ABROAD AND VISITING ACADEMIC APPOINTMENTS 2016–2017 Visiting scholar at Sapienza University and Istituto Svizzero, Rome, Italy; Centro Studi Movimenti, Parma, Italy; University of Oxford, UK July 2014 Research stays in Rome -

Senderliste Analog

3250 Lyss Telefon 032 387 02 22 Energie Seeland AG Beundengasse 1 Telefax 032 384 26 19 Elektrizität Wasser Kommunikation Postfach 349 MWST.-Nr. 423 372 [email protected] www.esag-lyss.ch Analoge Fernsehsender Taste Sender Info Sprache Kanal Frequenz Bemerkungen Deutsche Schweiz 1 SRF 1 Deutsch C 5 175.25 1 Deutsche Schweiz 2 SRF 2 Deutsch C 6 182.25 2 Deutsche Schweiz Info SRF Info Deutsch S 23 319.25 3 3 Plus 3+ Deutsch C 12 224.25 4 LOLY / Infokanal Deutsch C 10 210.25 5 TeleBärn Deutsch S 29 367.25 6 Tele Bielingue Deutsch S 8 154.25 7 1. Deutsches Fernsehen ARD Deutsch C 7 189.25 8 2. Deutsches Fernsehen ZDF Deutsch C 38 607.25 9 Österreich 1 ORF 1 Deutsch S 5 133.25 10 Österreich 2 ORF 2 Deutsch S 11 231.25 11 Südwest Fernsehen SWR BW Deutsch S 16 266.25 12 Bayerisches Fernsehen BR Deutsch C 8 196.25 13 Sat.1 CH Deutsch S 12 238.25 14 3sat Deutsch S 18 280.25 15 Pro 7 CH Deutsch C 61 791.25 16 RTL CH Deutsch S 13 245.25 17 RTL 2 CH Deutsch S 22 311.25 18 Super RTL CH S RTL Deutsch S 7 147.25 19 Kabel 1 CH Deutsch S 6 140.25 20 VOX CH Deutsch S 25 335.25 21 HSE 24 Deutsch S 27 351.25 22 ARTE Deutsch S 24 327.25 23 KiKa Deutsch S 4 126.25 24 Euronews Deutsch S 19 287.25 25 Schweizer Sportfernsehen SSF Deutsch S 20 294.25 26 Sport1 Deutsch S 15 259.25 27 Eurosport Deutsch S 17 273.25 28 Comedy Central / Nickelodeon CH Deutsch S 21 303.25 29 MTV Deutsch C 11 217.25 30 Französische Schweiz 1 RTS un Französisch C 9 203.25 31 Französische Schweiz 2 RTS deux Französisch C 50 703.25 32 Frankreich 2 (France 2) F 2 Französisch S 9 161.25 33 TV5MONDE EUROPE Französisch S 28 359.25 34 Italienische Schweiz 1 RSI LA 1 Italienisch S 26 343.25 35 Italienische Schweiz 2 RSI LA 2 Italienisch S 10 168.25 36 Rai Uno Italienisch S 14 252.25 37 QuickLine Digital TV/Radio Teleclub Vorgehen bei Bild- oder Tonstörungen Kontrollieren Sie, ob das Empfängeranschlusskabel und der Netzstecker richtig eingesteckt sind.