Gasification for Bio-Sng Production Adjacent to an Existing Forest Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hallandsjunior År Namn Förening Kommun 1979 Månadens Junior

Hallandsjunior År Namn Förening Kommun 1979 Månadens Junior 1980 Månadens Junior 1981 Månadens Junior 1982 Månadens Junior 1983 Jörgen Persson Halmstads BTK Halmstad 1983 Torbjörn Eliasson Varbergs Handikappidrottsförening Varberg 1983 Anita Karlsson Ätrans Sportskytteklubb Falkenberg 1983 Viktoria Bengtsson SK Laxen Halmstad 1984 Lars Lagerborg Varbergs AIK Varberg 1984 Per Andersson IF Tre Hjärtan Halmstad 1984 Peter Hedman Åsa IF Kungsbacka 1985 Mats Ahlgren Halmstad Fäktsällskap Halmstad 1985 Stefan Johansson Gång Krogsered 1985 Anna Simes Hylte OK Hyltebruk 1985 Anette Möller Varbergs SIM Varberg 1986 Maria Salsgård Söndrums Tennisklubb Halmstad 1986 Magnus Eriksson Skrea IF Falkenberg 1986 Leif Pettersson Falkenbergs Roddklubb Falkenberg 1986 Lars Lagerborg Varbergs AIK Varberg 1987 Åsa Svensson Halmstad Bordtennisklubb Halmstad 1987 Henrik Dagård IFK Halmstad Halmstad 1987 Peter Olsson Halmstads Golfklubb Halmstad 1987 Olle Karlsson Falkenbergs Golfklubb Falkenberg 1987 Peter Hansson Varbergs Badmintonklubb Varberg 1988 Jeanette Ryrman BMX Kungs Kungsbacka 1988 Yvonne Svensson BK Hallandia Halmstad 1988 Annika Morin SK Laxen Hyltebruk 1988 Tomas Kjellqvist Varbergs Handikappidrottsförening Varberg 1989 Linda Fredriksson IFK Halmstad Halmstad 1989 Niklas Gudmundsson Halmstad Bollklubb Halmstad 1989 Mikael Kjellström Hylte Volley Hyltebruk 1989 Anders Lehrman Halmstad Skyttegille Halmstad 1990 Fredrik Andersson Laholms Golfklubb Laholm 1990 Fredrik Andersson CK Wano Varberg 1990 Mats Andersson BK Falkarna Falkenberg 1990 Peter Nilsson -

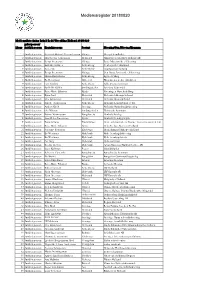

Medlemsregister 20180820

Medlemsregister 20180820 Medlemsförteckning Lokalt Ledd Utveckling Halland 20180820 privatperson/ Löpnr juridisk person Kontaktperson: Postort Förening/Org./Företag/Kommun 1 Juridisk person Berit och Roland Alexandersson Slöinge Alex på Sandbolet 2 Juridisk person Magdalena Johansson Halmstad Almi Företagspartner Halland AB 3 Juridisk person Bengt Svensson Slöinge Berte Museum ideell förening 4 Juridisk person Anki Enevoldsen Falkenberg Centerpartiet i Halland 5 Juridisk person Kajsa Vik Falkenberg Coompanion Halland 6 Juridisk person Bengt Svensson Slöinge Den Goda Jorden ideell förening 7 Juridisk person Martin Haraldsson Falkenberg Egareds Skog 8 Juridisk person Bo Bengtsson Älvsered Ekomuseum nedre Ätradalen 9 Juridisk person Lars Fröding Falkenberg Falkenbergs kommun 10 Juridisk person Kjell-Åke Källén Simlångsdalen Fylleåns Vattenråd 11 Juridisk person Rose-Marie Eriksson Fjärås Föreningen Hunehals Borg 12 Juridisk person Björn Lind Halmstad Hallands bildningsförbund 13 Juridisk person Olle Kristenson Halmstad Hallands Idrottsförbund 14 Juridisk person Elisabet Johansson Falkenberg Hallands Länsförbund av 4H 15 Juridisk person Anders Kinch Steninge Hallands Naturskyddsförening 16 Juridisk person Ola Nilsson Simlångsdalen Halmstads kommun 17 Juridisk person Bonny Wernersson Kungsbacka Hanhals Byalag 18 Juridisk person Ann-Helen Davidsson Fjärås Hanhals Hembygdsgille 19 Juridisk person Tommy Lang Träslövsläge Havs- och Kustfiskets Producentorganisation Ek. För. 20 Juridisk person Rose-Marie Eriksson Fjärås Hela Sverige Ska Leva Halland -

Integrerad Psykiatri Med Resursgruppsarbete Vård

Kännedomsutbildning Integrerad psykiatri med resursgruppsarbete Vård- och stödsamordning i Halland Varför Kännedomsutbildning? • 3 tillfällen, december 2015, Januari 2016, April 2016 • En av de största satsningarna inom psykiatrin i Halland • Viktigt med bred förankring för implementering Vilka är vi idag? • Christel Lood Taktisk grupp psykiatri • Marica Nilsson Granlund Utvecklingsledare • Mikael Nilsson avdelningschef • Maria Nordin utbildningssamordnare • Monica Granskär utbildare Kännedomsutbildning, för vem? • Ni som inte själva går utbildningen men som är Indirekt berörda. Tex: • politiker, chefer, handläggare • psykiatri och socialtjänst • Brukare, patienter, närstående, anhöriga • Närsjukvård, habilitering, försäkringskassa , arbetsförmedling, • Har vi glömt någon? Återkoppla och föreslå! Vi hoppas att ni idag får kännedom och reflektioner om: • Vad Hallands psykiatri och socialtjänst planerar att införa för gemensamt arbetssätt och varför • vad Integrerad psykiatri och resursgruppsarbete är • Integrerad psykiatri i Halland, för vem? • Vad personal i psykiatri och socialtjänst kommer att utbildas i (innehållet i utbildningen) • Vad det kan innebära att vara en del i en resursgrupp (som Brukare /patient, vård och stödsamordnare eller som annan deltagare) Forts: Vi hoppas att ni idag får kännedom och reflektioner om • Vad innebär integrerad psykiatri för den enskilde Individen? • Vad är skillnaden mellan Integrerad psykiatri och nuläget? • Om man inte har psykosrelaterad diagnos eller tillhör ett psykosteam, vilka möjligheter finns -

Hallands Geografi Och Resbehov

0(25) Hallands geografi och resbehov ETT UNDERLAG TILL REGIONALT TRAFIKFÖRSÖRJNINGSPROGRAM 2019 1(25) Inledning Denna rapport utgör ett av underlagen till det regionala trafikförsörjningsprogrammet. Syftet med rapporten är att ge en bild av Hallands förutsättningar och strukturer samt vilka resbehov som de ger upphov till. Genom att kartlägga såväl nuläget som historiska data och prognoser framåt i tiden så är ambitionen att läsaren ska få en ökad förståelse för dagens Halland och få del av underlag för att reflektera över framtidens Halland. De olika kapitlen behandlar i tur och ordning befolknings- och ortsstruktur, befolkningsutveckling, näringslivsstruktur, arbetspendling, gymnasie- och studiependling samt en avslutande analys. Ett särskilt fokus har legat på att fördjupa kunskapen om pendlingsströmmarna i länet, som i hög grad pekar ut kollektivtrafikens geografiska dimensioner och omfattning. Det faktiska resandet utifrån dagens turutbud beskrivs i rapporten: Resandet i kollektivtrafiken i Halland. 2(25) Befolknings- och ortsstruktur I det avlånga Halland bor de allra flesta nära kusten. Väster om E6 bor hela 60 procent av befolkningen på en yta som motsvarar 15 procent av länet. I någon av de sex kommunhuvudorterna bor varannan hallänning och än fler då orternas omland räknas in. De halländska orternas placering och storlek vittnar om små och stora målpunkter för arbete, service och nöjen. 3(25) Längs kusten i Halland finns fyra större orter från norr till söder: Kungsbacka, Varberg, Falkenberg och Halmstad. Halmstad är Hallands klart största tätort med knappt 70 000 invånare. På listan över de tio största tätorterna i länet återfinns samtliga kommunhuvudorter och totalt fyra orter i Kungsbacka kommun. Antal invånare i de tio största tätorterna i Halland (2017) Halmstad 68 085 Varberg 34 774 Kungsbacka1 25 167 Falkenberg 24 480 Onsala 12 363 Särö/Kullavik2 10 490 Laholm 6 696 Åsa 6 300 Oskarström 4 270 Hyltebruk 4 224 1 Den del av Göteborgs tätort som ligger inom Kungsbacka kommun. -

Bekräfta Din Vinst Senast Måndag Den 16 Nov 2015 Bekräfta Din Eller Barnets Plats Genom Att Skicka E-Post Till [email protected] Senast Den 16 Nov 2015

Bekräfta din vinst senast måndag den 16 nov 2015 Bekräfta din eller barnets plats genom att skicka e-post till [email protected] senast den 16 nov 2015. Därefter återkommer vi med vilka tider som gäller för upptäcktsfärden och ”Peterturen”. Vuxna: skriv ”Petertur” i ämnesraden och ange ditt namn och ort. Vill du ta med en vän? Ange då även vännens namn. Barn: skriv ”Upptäcktsfärd” i ämnesraden och ange barnets namn och ort. Vill barnet ta med sig en vän? Ange då även vännens namn. Givetvis är föräldrarna också välkomna på upptäcktsfärden i Trollskogen. Vinnare barn ”räkna Mattis Bertilsson, Gullbrandstorp Carina Bruzell, Halmstad Lisa Wilhelmsson, Halmstad djuren” Maya Reuter, Våxtorp Carina Holmberg, Mellbystrand Lisbeth Johansson, Ljungby Vinst: följ med Skillatrollet på Milla Sevandersson, Laholm Carina Wistrand, Halmstad Lorik, Halmstad upptäcktsfärd i Trollskogen och Mio Sevandersson, Laholm Catharina Adlerhill, Halmstad Lotta Paulsson, Harplinge ta med en vän. Moa Svensson, Holm Christin Karlsson, Halmstad Maarit Steen, Helsingborg Tid och plats: Laholms Stadspark, Molly Bårdén, Gullbrandstorp Curt-Ove Johansson, Ljungby Magnus Leander, Laholm 21 maj 2016 Naiomi Andersson, Falkenberg Dan Isaksson, Knäred Maj-Lis Persson, Halmstad Natalie Sjöstrand, Falkenberg Daniel Larsson, Markaryd Malin Pettersson, Falkenberg Agnes Mezei, Halmstad Noah Persson, Mellbystrand Ebba Sundin, Halmstad Margareta Söderberg, Åled Alba Jiménez Jönsson, Laholm Nova Byhmer, Halmstad Eija Moskuvaara, Halmstad Margareta Öström, Hyltebruk Albin Persson, -

Järnvägen Halmstad - Nässjö

Järnvägen Halmstad - Nässjö - en resurs för befolkning och näringsliv LTH Ingenjörshögskolan vid Campus Helsingborg Institutionen för Teknik och samhälle Examensarbete: David Nygren © Copyright David Nygren LTH Ingenjörshögskolan vid Campus Helsingborg Lunds Universitet Box 882 251 08 Helsingborg LTH School of Engineering Lund University Box 882 SE-251 08 Helsingborg Sweden Tryckt i Sverige Media-Tryck Biblioteksdirektionen Lunds Universitet Lund 2006 Sammanfattning Syftet med denna studie är att visa vilka möjligheter som de för närvarande lågtrafikerade järnvägarna i västra Småland kan erbjuda befolkningen och näringslivet. Bakgrunden är att trafiken på dessa banor lider av lönsamhetsproblem p.g.a. dålig infrastrukturstandard samt för långa restider och för låg turtäthet. Järnvägen mellan Halmstad och Nässjö färdigställdes 1882, och bibanan till Jönköping blev klar 1892. Ytterligare bibanor byggdes till huvudlinjen, som bidrog till en industriell utveckling i området. Efter 1950 började det ökade personbilsägandet och lastbilstrafiken orsaka minskat resande med tåg. Detta orsakade bannedläggningar av de trafiksvaga bibanorna och rationaliseringar längs huvudstråket. Efter en rad transportpolitiska beslut lättades SJ:s monopol och andra aktörer fick lov att bedriva järnvägstrafik. Därför inleddes ett samarbete mellan de olika länstrafikbolagen för att möjliggöra gemensam trafikering med tåg över länsgränserna. Redan 2006 började åter nedläggningsdiskussioner då Banverket ansåg att de pengar som regeringen anslagit inte räcker till underhåll av dessa järnvägar. Det är därför extra intressant att utföra denna studie, då banornas framtid faktiskt är satt på spel! En nulägesbeskrivning visar en stor variation av befolkningsmängder vars förändringar oftast är stabila eller negativa förutom för residensstäderna där den ökar. Oftast är det större inpendling än utpendling i orterna samt att en hög förvärvsgrad observeras, vilket innebär att arbetsmarknaden är god. -

Bekräfta Din Vinst Senast Måndag Den 14 November 2016

Bekräfta din vinst senast måndag den 14 november 2016 Bekräfta din eller barnets plats genom att skicka e-post till [email protected] senast måndag den 14 november 2016. Därefter återkommer vi med vilka tider som gäller för upptäcktsfärden och ”Peterturen”. Observera att till Peterturen är det först till kvarn som gäller (484 personer svarade rätt men det finns max 300 platser). Däremot får alla barn som hjälpte Skillatrollet att hitta djuren följa med på Skillas upptäcktsfärd den 20 maj. Vuxna: skriv ”Petertur” i ämnesraden och ange ditt namn och ort. Vill du ta med en vän? Ange då även vännens namn. Barn: skriv ”Upptäcktsfärd” i ämnesraden och ange barnets namn och ort. Vill barnet ta med sig en vän? Ange då även vännens namn. Givetvis är föräldrar också välkomna på upptäcktsfärden i Trollskogen. Bo Sjöholm, Hylte Gunnel Svensson, Halmstad Kerstin Zelander Nilsson, Knäred Monica Nylander, Genevad Agnes Klevedalen, Halmstad Vinnare vuxna ”Gissa Bo Vångerdal, Halmstad Gunvor Persson, Simlångsdalen Kicki Davidsson, Falkenberg Monika Arvidsson, Laholm Agnes Lönnergård, Oskarström träden” Bodil Göransson, Laholm Göran Forsberg, Kvibille Kim Ceder, Halmstad Monika Lindell, Halmstad Alba Jönsson, Laholm Vinst: följ med på Petertur i Bodil Nilsson, Skummeslöv Göran Hillar, Ullared Kirsi Kuitunen Johansson, Hyltebruk Mzriz T. Revelj, Båstad Albert Lindau, Partille-Göteborg Stadsparken - Mästerverket Boris Carlsson, Halmstad Gösta König, Halmstad Kjell Boström, Svenljunga Märit Jacobsson, Falkenberg Albin Nilsson, Mellbystrand i Laholm och ta med en vän. Britt- Marie Petersson, Båstad Hanna Andersson, Halmstad Kjell Enberg, Knäred Nellie Gudmundsson, Halmstad Alexandra Date, Halmstad Britt Nilsson, Laholm Hans Bagge, Falkenberg Kjell Jönsson, Laholm Nils Anders Nilsson, Gullbrandstorp Alicia Ilin Persson, Lindome Tid och plats: 20 maj 2017, Britta Larsson, Karlstorp 562 Harriet Bengtsson, Slöinge Kjell Pihl, Halmstad Nisse Bengtsson, Halmstad Alicia Karlsson, Skedala Laholms Stadspark. -

A Transnational Project and Its Results

A transnational Project and its Results The European Agricultural Fund 1 EUROPEAN UNION for Rural Development: European Social Fund Europe investing in rural areas Introduction and description Background - Political and social context In 2015 more than a million migrants and refugees from Syria, Afghanistan, Iraq and other countries crossed into Europe. This caused a crisis, as countries struggled to cope with the influx, and created a division within the EU over how best to deal with integration. While Europe’s leaders were debating, arguing and looking for solutions, without being able to find a common understanding, the situation drove volunteers all over Europe into action. Volunteers and LEADER-areas from rural Europe came together in the European Rural Parliament in Austria, November 2015, and stated: “The arrival of desperate people from areas of conflict and disaster, seeking refuge and new lives in Europe, is provoking thought and action within our networks. While urging governments and other agencies to work urgently to solve the underlying causes of the crisis, we call for a warm-hearted response, based on solidarity between people. We believe, that for many rural areas, and particularly those with declining population, this offers an opportunity to integrate refugees and other newcomers. The process of integration must include the necessary job creation, investment in housing, services and infrastructure. Successful integration efforts should be celebrated.” Through the international LEADER-Network, similar project-ideas between partners from Austria, Finland, Germany and Sweden could be brought together. Sweden had established a partnership with the regional project Integration Halland who brought in expertise- knowledge on the topic of integrating refugees to the labour market. -

Stor Karta Över Hylte Kommun – Se Mitten!

VISIT HYLTE Mat | Natur | Kultur 2021 NJUT AV LIVET HOS OSS I HYLTE! ENJOY LIFE WITH US IN HYLTE! GENIESSEN SIE DAS LEBEN BEI UNS IN HYLTE! STOR KARTA ÖVER HYLTE KOMMUN – SE MITTEN! 1 HYLTEBYGDEN ÄR ETT RIKTIGT NATURPARADIS FÖR ALLA – ÅRET OM! ”Det var en gång en plats längs Nissan med storskogen alldeles nära, som visade sig vara den perfekta platsen. Redan på stenåldern tog sig människor hit vandrande längs Nissans virvlande vatten. Här fann de storskogen och de goda jaktmarkerna. Här fanns friska vattendrag och skydd för väder och vind” Sjörikt, pittoreskt och kulinariskt Välkommen till en härlig vistelse i vår idylliska och sjörika bygd. Här har du alltid nära till fina fiskevatten, utmärkta kanotupplevelser, lugna sjöbad, inspirerande cykelturer och vackra vandringsleder. Eller varför inte göra en resa bakåt i tiden genom att besöka våra intressanta museer, pittoreska kulturminnen och välbevarade hembygdsgårdar? Känner du förresten till att ”svamparnas Linné” Elias Fries, föddes i Femsjö? Eller att stamföräldrarna till världens största dokumenterade släkt bodde och verkade här? Passa på och besök det spännande Friesmuseet i Femsjö och vandra i Långarydssläktens fotspår. På vintern kan vi erbjuda utförsbackar med liftar, bandy- bana samt en konstsnöanläggning med längdskidspår och skidlekplats för barnen. Hos oss hittar du också småskalig shopping, konst och hantverk, kulinariska upplevelser och trivsamma boende. Man mår bra här hos oss Tempot i Hyltebygden är lite lugnare, så här är det lätt att trivas och må bra. Vi tror att ett aktivt och socialt liv nära service och natur skapar välmående. Landskapet präglas av skog och sjöar, samt av mindre byar och samhällen. -

Hallandsjunior År Namn Förening Kommun 1979 Månadens Junior

Hallandsjunior År Namn Förening Kommun 1979 Månadens Junior 1980 Månadens Junior 1981 Månadens Junior 1982 Månadens Junior 1983 Jörgen Persson Halmstads BTK Halmstad 1983 Torbjörn Eliasson Varbergs Handikappidrottsförening Varberg 1983 Anita Karlsson Ätrans Sportskytteklubb Falkenberg 1983 Viktoria Bengtsson SK Laxen Halmstad 1984 Lars Lagerborg Varbergs AIK Varberg 1984 Per Andersson IF Tre Hjärtan Halmstad 1984 Peter Hedman Åsa IF Kungsbacka 1985 Mats Ahlgren Halmstad Fäktsällskap Halmstad 1985 Stefan Johansson Gång Krogsered 1985 Anna Simes Hylte OK Hyltebruk 1985 Anette Möller Varbergs SIM Varberg 1986 Maria Salsgård Söndrums Tennisklubb Halmstad 1986 Magnus Eriksson Skrea IF Falkenberg 1986 Leif Pettersson Falkenbergs Roddklubb Falkenberg 1986 Lars Lagerborg Varbergs AIK Varberg 1987 Åsa Svensson Halmstad Bordtennisklubb Halmstad 1987 Henrik Dagård IFK Halmstad Halmstad 1987 Peter Olsson Halmstads Golfklubb Halmstad 1987 Olle Karlsson Falkenbergs Golfklubb Falkenberg 1987 Peter Hansson Varbergs Badmintonklubb Varberg 1988 Jeanette Ryrman BMX Kungs Kungsbacka 1988 Yvonne Svensson BK Hallandia Halmstad 1988 Annika Morin SK Laxen Hyltebruk 1988 Tomas Kjellqvist Varbergs Handikappidrottsförening Varberg 1989 Linda Fredriksson IFK Halmstad Halmstad 1989 Niklas Gudmundsson Halmstad Bollklubb Halmstad 1989 Mikael Kjellström Hylte Volley Hyltebruk 1989 Anders Lehrman Halmstad Skyttegille Halmstad 1990 Fredrik Andersson Laholms Golfklubb Laholm 1990 Fredrik Andersson CK Wano Varberg 1990 Mats Andersson BK Falkarna Falkenberg 1990 Peter Nilsson -

Kollektivtrafikplan 2019 Med Utblick 2020-2021 Antagen I Hallandstrafikens Styrelse 2018-09-14

HALLANDSTRAFIKEN AB Kollektivtrafikplan 2019 med utblick 2020-2021 Antagen i Hallandstrafikens styrelse 2018-09-14 Innehållsförteckning 1. Sammanfattning ........................................................................................................... 3 2. Inledning ....................................................................................................................... 4 Hur fungerar kollektivtrafiken i Halland ....................................................................... 4 Vad är Kollektivtrafikplan ............................................................................................. 4 3. Mål för kollektivtrafiken i Halland ................................................................................ 5 Övergripande mål ......................................................................................................... 5 Hallandstrafikens mål ................................................................................................... 6 4. Utveckling under 2017 .................................................................................................. 9 Marknadsandel ........................................................................................................... 10 Resande ...................................................................................................................... 11 Nöjdhet ....................................................................................................................... 17 Miljö ........................................................................................................................... -

2021-01-08 Ta Med Detta Brev Till Vårdcentralen När Du Ska Vaccinera

Ta med detta brev till vårdcentralen när du ska vaccinera dig 1 (2) 2021-01-08 Nu erbjuds du som har hemtjänst, och du som bor tillsammans med någon som har hemtjänst, vaccination mot covid-19 Vaccinationen mot covid-19 har startat. Vaccinationen är ett skydd mot svår sjukdom och du tillhör den grupp som prioriteras först för vaccinering. Vaccinationen mot covid-19 är ett erbjudande, var och en avgör själv om man vill vaccinera sig eller inte. För att kunna få vaccination mot covid-19 ska du boka en tid och fylla i en hälsodeklaration. Detta gör du på 1177.se/Halland. Det går bra att boka vaccinationstid för två personer samtidigt. Bokningen är enkel och kräver ingen inloggning. Vaccinationen omfattar två doser som ges med tre veckors mellanrum. Du bokar två tider direkt, både för dos 1 och dos 2, med tre veckors mellanrum, på samma vårdcentral. Om tiderna är slut gå in igen om någon dag, det läggs kontinuerligt ut tider i takt med att vi får tillgång till vaccin. Om du behöver hjälp med att boka tid, så kan du be någon i din närhet att hjälpa dig, till exempel hemtjänstpersonal eller en närstående. Har du inga möjligheter att boka via 1177.se/Halland kan du ringa till någon av de vårdcentraler som vaccinerar mot covid-19. Nedan finns en lista på de vårdcentraler som vaccinerar. Detta innebär att du kan behöva gå till en vårdcentral som du inte är listad på. Kungsbacka Vårdcentralen Kungsbacka, Sjukstugegatan 18, 0300-565240 Capio Husläkarna Kungsbacka, Nygatan 10 D, 0300-566766 Varberg Neptunuskliniken, Sjöallén 12, 0340-16016 Falkenberg Vårdcentralen Falkenberg, Urmakaregatan 2, ingång D, 0346-56210 Capio Familjeläkarna Falkenberg, Nygatan 64, 0346-715050 Vårdcentralen Ullared, Falkenbergsv.