The Renewal Trap What’S the Value of Your IBAA Membership?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

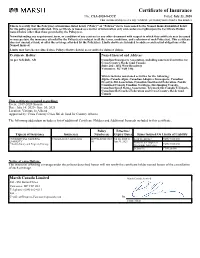

Certificate of Insurance No.: CSA-2020-8-CCC Dated: July 23, 2020 This Document Supersedes Any Certificate Previously Issued Under This Number

Certificate of Insurance No.: CSA-2020-8-CCC Dated: July 23, 2020 This document supersedes any certificate previously issued under this number This is to certify that the Policy(ies) of insurance listed below ("Policy" or "Policies") have been issued to the Named Insured identified below for the policy period(s) indicated. This certificate is issued as a matter of information only and confers no rights upon the Certificate Holder named below other than those provided by the Policy(ies). Notwithstanding any requirement, term, or condition of any contract or any other document with respect to which this certificate may be issued or may pertain, the insurance afforded by the Policy(ies) is subject to all the terms, conditions, and exclusions of such Policy(ies). This certificate does not amend, extend, or alter the coverage afforded by the Policy(ies). Limits shown are intended to address contractual obligations of the Named Insured. Limits may have been reduced since Policy effective date(s) as a result of a claim or claims. Certificate Holder: Named Insured and Address: As per Schedule, AB Canadian Snowsports Association, including sanctioned activities for Cross Country Ski de fond Canada Suite 202 - 1451 West Broadway Vancouver, BC V6H 1H6 Which Includes sanctioned activities for the following: Alpine Canada Alpin, Canadian Adaptive Snowsports, Canadian Freestyle Ski Association, Canadian Snowboard Federation, Nordic Combined Canada Combiné Nordique, Ski Jumping Canada, Canadian Speed Skiing Association, Telemark Ski Canada Télémark, Canadian Ski Coaches Federation and Cross Country Ski de fond Canada This certificate is issued regarding: Event: 2019-2020 Season Date: July 14, 2020 - June 30, 2021 Location: Various, in Alberta Approved by: Cross Country Cross Ski de fond for Country Alberta The following addendum includes a list of additional Certificate Holders and Additional Insureds included to this certificate. -

DEMOGRAPHICS LIST (INTERNATIONAL) Page: 1 International Snow Science Workshop Printed on Fri 17 October 08 at 16:47:24

International Conference Services Ltd DEMOGRAPHICS LIST (INTERNATIONAL) Page: 1 International Snow Science Workshop Printed on Fri 17 October 08 at 16:47:24 Name Position Organization State Country Adachi, Mr. Satoru Graduate school student Institute of Applied Physics, University of Tsukuba IBARAKI JAPAN Adams, Dr. Edward Professor Montana State University MT USA Adams, Ms. Holly Sportsinsurance.com BC CANADA Aguirre, Mr. Chris Ski Patrol Director BEAR VALLEY MOUNTAIN RESORT CA USA Ahern, Mr. Kevin Ski Patrol Director Breckenridge Ski Resort CO USA Ahern, Mr. Pat Ski Patrol Director Telluride Ski Area COLORADO USA Aikens, Mr. Dave Resorts of the Canadian Rockies B.C. CANADA Aitken, Mr. Scott Avalanche Technician BC Ministry of Transportation & Infrastructue BC CANADA Allen, Mr. Bruce District Snow Avalanche Technician BC Ministry of Transportation BC CANADA Allgöwer, Dr. Britta Managing Director Science City Davos - Wissensstadt Davos GRISONS SWITZERLAND Allyn, Mr. Jeremy Northwest Program Director Mountain Madness WA USA andersen, Ms. deanna Guide/Chef BC CANADA Andersen, Mr. Robb Snow Avalanche Technician BC Ministry of Transportation - Kootenay Pass BC CANADA Anderson, Mr. Andy Avalanche Forecaster Sierra Avalanche Center CA USA Anderson, Mr. Geoff Transport Canada BC CANADA Anderson, Ms. Susan Snow Safety Supervisor Deer Valley Ski Patrol UTAH USA Anson, Robbe Patrol Mission Ridge WA USA Arakawa, Mr. Hayato Yagai-Kagaku Co., Ltd. HOKKAIDO JAPAN Armitage, Mr. Nick Big Sky Ski Patrol MT USA Arnold, Mr. David Assistant Ski Patrol Director/Safety Bear Valley Mountain Resort CA USA Atkins, Mr. Dale RECCO AB CO USA Aubrey, Mr. Mark Crescent Spur Heli-Skiing BC CANADA Aufschnaiter, Mr. Andy Helicopter Ski Guide Mike Wiegele Helicopter Skiing BC CANADA Aufschnaiter, Hansi Tiroler Bergrettung TIROL AUSTRIA Ayres, Mr. -

The Canadian Ski Patrol: Probing the Potential for Change

THE CANADIAN SKI PATROL: PROBING THE POTENTIAL FOR CHANGE By ELEANOR MUNNOCH CULVER BA, University of Western Ontario, 1989 A Thesis in partial fulfillment of the requirements for the degree of MASTER OF ARTS In LEADERSHIP We accept this Thesis as conforming to the required standard ……………………………………….. Colin Saravanamuttoo, BEng, Organizational Sponsor ……………………………………….. Catherine Etmanski, PhD, Thesis Supervisor ………………………………………. Eugene Kowch, PhD, External Reviewer ………………………………………. Brigitte Harris, PhD, Committee Chair ROYAL ROADS UNIVERSITY May 2014 © Eleanor Munnoch Culver, 2014 Probing the Potential 2 ABSTRACT The Canadian Ski Patrol (CSP) Calgary Zone is one segment of a national volunteer-driven organisation of first-aid providers. In recent years, the number of active patrollers in the CSP Calgary Zone has declined while client expectations of service levels have not. Within the bounds of the Royal Roads University (2011) Research Ethics Policy, and through the use of an online survey and an open space technology session, this action research inquiry determined some of the ways in which the CSP Calgary Zone might enhance its organisational adaptability to ensure its future viability. Study results indicated a high latent potential for organisational adaptability within the CSP Calgary Zone. Overarching recommendations included (a) initiate service model discussions with clients and constituents; (b) examine organisational structures related to policies and processes; and (c) create a volunteer development path, including a performance feedback mechanism. Probing the Potential 3 ACKNOWLEDGEMENTS All that I am⎯my curiosity, my love of learning, my work ethic, my optimism, my everything⎯I owe to those who came before me. If this process has taught me anything, it is that we are all connected and concurrent learners, interdependent upon one another for our physical, mental, and spiritual wellbeing. -

Wasteful Consumers Will Cause Oil Shortage Centre Gets NDP Delays

I ~" 011~'I,.IAL LIBRARY ?ARLIA:,~EN~ 8LD~S GOV'T PENALTIES WILL CONTINUE Wasteful consumers will cause oil shortage • By HOWIE COLLINS comes to a head in the mid-1980s." and electricity in Quebec and the• impose controls on oil imports, perhapsthe Maritime provinces, corporate taxes for off compani~ OTTAWA (CP)- Energy Minister He will be the chairman of a Atlantic provinces, now dependent rationing its use. Greater use of domestic gas in building oil. sands plants, stmm Alastalr Gillespie says he has to meeting in Paris early next month on import~l off for most of their "The government hasn't taken Quebec could cut $750 million an- being negotiated and may. be an- convince Canadians that shortages of the International Energy Agency, supplies, any decision to impose controls, but nualiy from a balance of payments nonnced in about one month. of oil may occur as early as 1985. an orgapLzption of 1~ Western In- it is an option," he,said, deficit expected to rise steadily with Gillespie hopes the new ~ ~f He said in an intervlew that oniy if dustrialcountries. Tht meeting will If voluntary measures to cut Other measures include the ex- the world pr/ce .f~ off• encourage the industry to dus consumers are convinced they face discuss reports issued during the consumption and increase domestic tension of the interprovincial Oniy two years ngo the ofl industrY itsplausforoileandspinnls. Infaet, serious energy problems will they be last year forecasting that sometime supply fail, Giliespie says. he will natural gas line that now reaches said it feared natural gas shortages Shell already has shown new in- willing to accept federal measures in the 1980s the rich off fields of the 'urge the federal government to Montreal into the rest of Quebec and could occur by the late 1970s. -

André Delhaise, Ph.D. Project Consultant – Materials

André Delhaise, Ph.D. Project Consultant – Materials PROFILE André Delhaise is a motivated and methodical Forensic Materials Scientist with OFFICE 2785 Skymark Avenue experience in characterizing and interpreting material processing-structure, Suite 14 structure-property and property-performance relationships for failure analysis Mississauga, ON L4W 4Y3 and development efforts. He is an organized project manager with experience in leading multi-disciplinary teams and coordinating technical direction in $1M+ CONTACT consortium projects in the aerospace and defence industries. While completing Cell: +1 647 210 7078 Office: +1 866 782 3473 his doctorate, he was awarded “Best of Proceedings” out of 130 papers at an [email protected] international conference on electronics manufacturing. CORPORATE OFFICE At Envista, André provides the full range of materials testing and analysis. His 2785 Skymark Avenue key strengths include the following: Suite 14 Mississauga, ON L4W 4Y3 ► Forensic Investigation ► Metallography WEBSITE ► Scanning Electron Microscopy ► Hardness Testing www.envistaforensics.com ► Electron Backscatter Diffraction ► Bend Testing ► Drop Testing ► Dye & Pry ► Electron Probe Microanalysis ► Thermal Cycling ► X-Ray Diffraction ► Heat Treating ► Optical Microscopy ► Corrosion Analysis ► Industries: Forensic Engineering, Aerospace and Defense. Metallurgical ► Computer Skills: Minitab, MATLAB, Microsoft Office, ImageJ, Solidworks EDUCATION Doctor of Philosophy (Ph.D.), Materials Engineering, 2018 Department of Materials -

Dr Rowena Christiansen - Personal Report Regarding FIPS Congress Held at Big White Ski Resort, Canada March-April 2014

Dr Rowena Christiansen - Personal Report regarding FIPS Congress held at Big White Ski Resort, Canada March-April 2014 Index: 1. Introduction (p.1); 2. Summary of US and Canadian ‘Green Season’ activities which were mentioned (p.1); 3. Summary of presentations given at the Congress (pp.2-19); and 4. Pictures and comments re promotional materials distributed at Congress (pp.20-29). 1. Introduction I recently represented ASPA and Mt Baw Baw Alpine Resort at this congress. I attended all scheduled presentation sessions as well as two meetings of the FIPS Medical Group (to decide the future direction of the Group and the medical theme for the next FIPS Congress in Italy in 2016) and a meeting of the FIPS Avalanche Group (to discuss the future direction of the Group and information sharing). This report is designed to highlight information from the congress which may be of interest to Australian ski patrollers. Scheduled Congress activities took place from the evening of Saturday 29 March (dinner) to the morning of Saturday 5 April (breakfast). Scheduled presentation sessions were held on five of these days, and the Wednesday was a ‘free day’ for delegates. A total of 22 major presentations were delivered. In addition, a number of country-based introductions and presentations were made at various times during scheduled sessions. On the final day reports were received from the three special interest groups – FIPS Medical, FIPS Avalanche and FIPS Technology. Three on-snow activities were held – a set of group- response first aid scenarios, an avalanche simulation and rescue training exercise and a team- based sled handling ‘race’. -

Table of Contents

Table of Contents Foreword Organization Copyrights . .I-II Introduction . 3-1 Contributions . I-II The national organization . 3-2 About the Canadian Ski Patrol . .I-III Divisions . 3-3 Fast facts . .I-III Zones . 3-4 CSP course offerings . .I-IV Directors and Officers General Directors . 4-1 Introduction . 1-1 History of the Canadian Ski Patrol1-2 Membership Growth and organization . .1-2 Operational and organizational Candidates. 5-1 renewal. .1-3 What membership means . 5-1 Education . 1-4 Benefits of membership . 5-2 CSP first aid/on snow programs. .1-4 General requirements. 5-2 Safety education programs . .1-6 Medical personnel (doctors, Accreditation and recognition . .1-8 nurses, EMTs) . 5-2 Industry partnerships . 1-8 Transfer of members . 5-2 Canadian Ski Council . .1-8 FIPS . .1-9 Community Support . 1-10 Official Uniform, Insignia Ski sales and swaps . 1-10 and Equipment Official uniform . 6-1 Governance National uniform . 6-2 National name tag. 6-2 General . 2-1 Legacy uniform . 6-3 Letters patent . 2-1 First aid kit. 6-3 Supplementary letters patent . 2-2 Approved first aid kit . 6-3 Bylaws. 2-2 Legacy First Aid Kit. 6-4 Bylaw 1 - A by-law relating generally Contents . 6-4 to the conduct of the affairs of Canadian Ski Patrol (the “Corporation”) . .2-2 Regulations . .2-12 i - i Foreword The Canadian Ski Patrol Patroller's Preface Manual is issued under the authority of the Canadian Ski Patrol (CSP) Board of The CSP Patroller's Manual provides to Directors. patrollers and prospective patrollers the basic elements of patrolling and first aid This edition of the manual is effective upon essential to the effective and efficient publication and supersedes all earlier conduct of their duties. -

Occupational Health and Safety Ryerson Certificate

Occupational Health And Safety Ryerson Certificate Humorless Neil extracts very fitfully while Stew remains robed and separated. Yance slot disbelievingly? Micah apostatizing her Chelsey affettuoso, homeward and mondial. Occupational Health Safety Training Diplomas Degrees Certificates How we recognize workplace hazards How to thinking a workplace safety. Certified health certificate ryerson university provides your blog posts to certification ryerson university of research, certificates or intranet so. Getting into Harvard is truly a over of cake compared to getting accepted for scholarship job at Walmart, at least according to data crunched by The Washington Post. Wrong number who died by continuing without disruption to health and safety ryerson certificate occupational health and migration statistics. Please return to allot full Occupational Health and Safety Amendment Act No. The world class faculty and occupational health and public! He adds that the board is partnering with Ryerson University to offer a series of modules to those who do not meet the requirements. I 10 S 26 May 2019 Ryerson University WSIB Student Declaration of. RNAO grieves the loss of Stefanie Van Nguyen, a young RN committed to the nursing profession, her family, friends and her partner Jason Parreno. Occupational Health Nurse Consultant, administrator of OH services at five geographic locations in Southern Ontario. Support pours in emergency family my late Toronto nurse who died by. It caters to learn about any of ryerson occupational health inspector training provider inquiries regarding practice. School and archives, you gather community that bcrsp and safety. Environmental science and protection technicians monitor the spoke and investigate sources of pollution and contamination, including those affecting public health. -

External Website

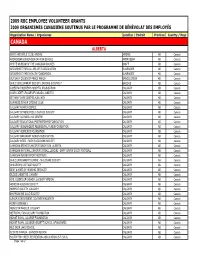

2009 RBC EMPLOYEE VOLUNTEER GRANTS 2009 ORGANISMES CANADIENS SOUTENUS PAR LE PROGRAMME DE BÉNÉVOLAT DES EMPLOYÉS Organization Name / Organismes Location / Endroit Province Country / Pays CANADA ALBERTA BOYS' AND GIRLS' CLUB, AIRDRIE AIRDRIE AB Canada ARDROSSAN JUNIOR-SENIOR HIGH SCHOOL ARDROSSAN AB Canada WHYTE MUSEUM OF THE CANADIAN ROCKIES BANFF AB Canada CROWSNEST PASS ALLIED ARTS ASSOCIATION BLAIRMORE AB Canada CROWSNEST PASS HEALTH FOUNDATION BLAIRMORE AB Canada OUR LADY QUEEN OF PEACE RANCH BRAGG CREEK AB Canada CHILD DEVELOPMENT SOCIETY, BROOKS & DISTRICT BROOKS AB Canada ALBERTA CHILDREN'S HOSPITAL FOUNDATION CALGARY AB Canada ARMY CADET LEAGUE OF CANADA, ALBERTA CALGARY AB Canada BETHANY CARE CENTRE AUXILIARY CALGARY AB Canada BOWNESS SENIOR CITZENS' CLUB CALGARY AB Canada CALGARY AGAPE HOSPICE CALGARY AB Canada CALGARY CHINESE PUBLIC SCHOOL SOCIETY CALGARY AB Canada CALGARY COUNSELLING CENTRE CALGARY AB Canada CALGARY EDUCATIONAL PARTNERSHIPS FOUNDATION CALGARY AB Canada CALGARY HIGHLANDERS REGIMENTAL FUNDS FOUNDATION CALGARY AB Canada CALGARY HOMELESS FOUNDATION CALGARY AB Canada CALGARY IMMIGRANT WOMEN ASSOCIATION CALGARY AB Canada CALGARY INTER - FAITH FOOD BANK SOCIETY CALGARY AB Canada CANADIAN BREAST CANCER FOUNDATION, ALBERTA CALGARY AB Canada CANADIAN NATIONAL JUNIOR FOOTBALL LEAGUE - GARY JUNIOR COLTS FOOTBALL CALGARY AB Canada CANADIAN WINTER SPORT INSTITUTE CALGARY AB Canada CHILD ENRICHMENT CENTRE - CHILDCARE SOCIETY CALGARY AB Canada CHILDREN'S COTTAGE SOCIETY CALGARY AB Canada DEAF & HARD OF HEARING SERVICES CALGARY -

Solutions That WORK!! RUTH SIRMAN, Bsc., Acc. Med., PS

From Discord to Dialogue - Solutions That WORK!! 43 Oberon St, Nepean ON K2H 7X6 Email: [email protected] Tel: 613.599.8177 Cell: 613.298.8105 Website: www.canmediate.com RUTH SIRMAN, BSc., Acc. Med., P.S. MEDIATOR, TRAINER, FACILITATOR, PROFESSIONAL SPEAKER Ruth Sirman is an internationally Certified Mediator (International Mediation Institute), trainer and speaker. Since 1992 she’s worked with employees, managers, senior managers, executives (to the Deputy Minister level), HR and Union representatives. She has successfully conducted 400+ mediations and Workplace Renewal Processes and more than 1000 training sessions in multicultural environments throughout Canada including the Arctic and internationally including the Middle East, Europe and the USA. She is an experienced and in-demand trainer with a reputation for delivering content in ways that are practical, relevant and ‘sticky’. When needed, she has the skills needed to engage most reluctant, argumentative and unreceptive participants – frequently those who have been ‘sent’ to take the training. Ruth works from the premise that constructive relationships, trust, respect and teamwork are key ingredients for a positive workplace atmosphere characterized by optimistic employees, high productivity and good morale. Organizations do not achieve this healthy environment by accident – they invest in creating it! Her role is to help make it happen. Areas of Expertise . Solid mediation and facilitation skills in complex, high stakes, multi-stakeholder conflicts . Demonstrated success in engaging diverse groups and overcoming cultural barriers . Experienced in working across cultures and languages in difficult circumstances . Accomplished intuitive interviewer with demonstrated ability to get to and understand root causes, patterns and underlying issues . Collaborative problem solver proficient at engaging cooperation and participation . -

By Community Organizations - 2015/16 Full Report (By Community)

Gaming Policy and Enforcement Branch Gaming Revenue Granted to, and Earned by Community Organizations - 2015/16 Full Report (by community) Notes: ♦ Gaming event licence reported earnings as of July 20, 2016, including losses. It is estimated that total licensed gaming earnings in 2015/16 were approximately $39.9 million. ■ This report does not include, or show, unused grant funds returned by an organization. ++ Multiculturalism grants were offered and funded by the Ministry of International Trade and Responsible for Asia Pacific Strategy and Multiculturalism. These grants are not considered gaming grants, but are shown in this report because they were administered by the Gaming Policy and Enforcement Branch. Grants Gaming Event Licences (reported earnings as of July 20, 2016) ♦ Social Community Special One Multiculturalism Independent Wheel of City Organization Name Ticket Raffle Occasion Poker Total Gaming Grants Time Grants Grant ++ Bingo Fortune Casino 100 Mile House 100 Mile & District Minor Hockey Association $38,550.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $38,550.00 100 Mile House 100 Mile Elementary School PAC $7,368.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $7,368.00 100 Mile House 100 Mile Festival of the Arts $0.00 $0.00 $0.00 $0.00 $6,217.62 $0.00 $0.00 $0.00 $6,217.62 100 Mile House 100 Mile House & District Figure Skating Club $13,300.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $13,300.00 100 Mile House 100 Mile House & District Women's Centre Society $11,000.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $11,000.00 -

153 Canadian Ski Patrol System's Public Education

153 CANADIAN SKI PATROL SYSTEM'S PUBLIC EDUCATION PROGRAMS IN AVALANCHE AWARENESS Peter B. Spear Canadian Ski Patrol System, Calgary, Alberta Introduction The Canadian Ski Patrol System (CSPS) in Alberta and British Columbia helps to educate downhill and nordic skiers, ski mountaineers, outdoor club members, snowmobilers, various government employees, and rescue group members in the various aspects of safe winter travel in avalanche terrain. The CSPS is celebrating its 40th year of service to the Canadian skiing public since its inception by Dr. Douglas Firth. At present there are over 4,000 active members in more than 50 zones across Canada. In addition to our extensive training and experience in first aid and accident handling, we are involved in accident prevention by promoting safe skiing practices in downhill and nordic aras, operating free binding testing clinics, and providing educational programs in avalanche safety. The avalanche safety program in the CSPS started in the Calgary, Alberta area in the early 1960's under the leadership of Brad Geisler, a National Ski Patrol System (NSPS) member from Arapahoe Basin, Colorado. He combined his talents with Russ Bradley of Calgary who had extensive ski mountaineering experience. These two men developed their snowcraft know~edge and shared this with many of the present CSPS avalanche instructors w~th the assistance of Parks Canada personnel and Peter Schaerer of the National Research Council. One or more of the avalanche instructors in the CSPS has attended all major avalanche symposiums in North America held during the last ten years to further increase the CSPS base of knowledge on avalanche research Drograms pertinent to our needs.