Printmgr File

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In the United States District Court for the District Of

Case 1:16-cv-00296-JB-LF Document 132 Filed 12/21/17 Page 1 of 249 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF NEW MEXICO IN RE: SANTA FE NATURAL TOBACCO COMPANY MARKETING & SALES PRACTICES AND PRODUCTS LIABILITY LITIGATION No. MD 16-2695 JB/LF MEMORANDUM OPINION AND ORDER THIS MATTER comes before the Court on: (i) the Defendants’ Request for Judicial Notice in Support of Motion to Dismiss, filed November 18, 2016 (Doc. 71)(“First JN Motion”); (ii) Defendants’ Second Motion for Judicial Notice in Support of the Motion to Dismiss the Consolidated Amended Complaint, filed February 23, 2017 (Doc. 91)(“Second JN Motion”); (iii) Defendants’ Third Motion for Judicial Notice in Support of the Motion to Dismiss the Consolidated Amended Complaint, filed May 30, 2017 (Doc. 109)(“Third JN Motion”); and (iv) the Defendants’ Motion to Dismiss the Consolidated Amended Complaint and Incorporated Memorandum of Law, filed February 23, 2017 (Doc. 90)(“MTD”). The Court held hearings on June 16, 2017 and July 20, 2017. The primary issues are: (i) whether the Court may consider the items presented in the First JN Motion, the Second JN Motion, and the Third JN Motion without converting the MTD into one for summary judgment; (ii) whether the Court may exercise personal jurisdiction over Reynolds American, Inc. for claims that were not brought in a North Carolina forum; (iii) whether the Federal Trade Commission’s Decision and Order, In re Santa Fe Nat. Tobacco Co., No. C-3952 (FTC June 12, 2000), filed November 18, 2016 (Doc. 71)(“Consent Order”), requiring Defendant Santa Fe Natural Tobacco Company, Inc. -

Crime, Law Enforcement, and Punishment

Shirley Papers 48 Research Materials, Crime Series Inventory Box Folder Folder Title Research Materials Crime, Law Enforcement, and Punishment Capital Punishment 152 1 Newspaper clippings, 1951-1988 2 Newspaper clippings, 1891-1938 3 Newspaper clippings, 1990-1993 4 Newspaper clippings, 1994 5 Newspaper clippings, 1995 6 Newspaper clippings, 1996 7 Newspaper clippings, 1997 153 1 Newspaper clippings, 1998 2 Newspaper clippings, 1999 3 Newspaper clippings, 2000 4 Newspaper clippings, 2001-2002 Crime Cases Arizona 154 1 Cochise County 2 Coconino County 3 Gila County 4 Graham County 5-7 Maricopa County 8 Mohave County 9 Navajo County 10 Pima County 11 Pinal County 12 Santa Cruz County 13 Yavapai County 14 Yuma County Arkansas 155 1 Arkansas County 2 Ashley County 3 Baxter County 4 Benton County 5 Boone County 6 Calhoun County 7 Carroll County 8 Clark County 9 Clay County 10 Cleveland County 11 Columbia County 12 Conway County 13 Craighead County 14 Crawford County 15 Crittendon County 16 Cross County 17 Dallas County 18 Faulkner County 19 Franklin County Shirley Papers 49 Research Materials, Crime Series Inventory Box Folder Folder Title 20 Fulton County 21 Garland County 22 Grant County 23 Greene County 24 Hot Springs County 25 Howard County 26 Independence County 27 Izard County 28 Jackson County 29 Jefferson County 30 Johnson County 31 Lafayette County 32 Lincoln County 33 Little River County 34 Logan County 35 Lonoke County 36 Madison County 37 Marion County 156 1 Miller County 2 Mississippi County 3 Monroe County 4 Montgomery County -

Local Business Database Local Business Database: Alphabetical Listing

Local Business Database Local Business Database: Alphabetical Listing Business Name City State Category 111 Chop House Worcester MA Restaurants 122 Diner Holden MA Restaurants 1369 Coffee House Cambridge MA Coffee 180FitGym Springfield MA Sports and Recreation 202 Liquors Holyoke MA Beer, Wine and Spirits 21st Amendment Boston MA Restaurants 25 Central Northampton MA Retail 2nd Street Baking Co Turners Falls MA Food and Beverage 3A Cafe Plymouth MA Restaurants 4 Bros Bistro West Yarmouth MA Restaurants 4 Family Charlemont MA Travel & Transportation 5 and 10 Antique Gallery Deerfield MA Retail 5 Star Supermarket Springfield MA Supermarkets and Groceries 7 B's Bar and Grill Westfield MA Restaurants 7 Nana Japanese Steakhouse Worcester MA Restaurants 76 Discount Liquors Westfield MA Beer, Wine and Spirits 7a Foods West Tisbury MA Restaurants 7B's Bar and Grill Westfield MA Restaurants 7th Wave Restaurant Rockport MA Restaurants 9 Tastes Cambridge MA Restaurants 90 Main Eatery Charlemont MA Restaurants 90 Meat Outlet Springfield MA Food and Beverage 906 Homwin Chinese Restaurant Springfield MA Restaurants 99 Nail Salon Milford MA Beauty and Spa A Child's Garden Northampton MA Retail A Cut Above Florist Chicopee MA Florists A Heart for Art Shelburne Falls MA Retail A J Tomaiolo Italian Restaurant Northborough MA Restaurants A J's Apollos Market Mattapan MA Convenience Stores A New Face Skin Care & Body Work Montague MA Beauty and Spa A Notch Above Northampton MA Services and Supplies A Street Liquors Hull MA Beer, Wine and Spirits A Taste of Vietnam Leominster MA Pizza A Turning Point Turners Falls MA Beauty and Spa A Valley Antiques Northampton MA Retail A. -

TRACEY A. MASH and ANJANETTA LINGARD Plaintiffs V. BROWN

TRACEY A. MASH and ANJANETTA LINGARD Plaintiffs v. BROWN & WILLIAMSON TOBACCO CORPORATION Defendant UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MISSIOURI (ST. LOUIS) Case No. 4:03CV00485TCM September 20, 2004 PURPOSE This backgrounder has been prepared by some the defendant in this case to provide a concise reference document on the case of Tracey A. Mash and Anjanetta Lingard v. Brown & Williamson Corporation, No. 4:03CV00485TCM. It is not a court document. THE PLAINTIFFS: This lawsuit was filed by Tracey A. Mash and Anjanetta Lingard on March 6, 2003 in state court in Missouri. It was later removed to federal court. The plaintiffs are the daughters of Stella Hale who died on Aug. 16, 2001. Plaintiffs allege Ms. Hale died from lung cancer caused by KOOL cigarettes. THE DEFENDANTS: The sole defendant is Brown & Williamson Tobacco Corporation (B&W), formerly headquartered in Louisville, Ky. Its major brands included Pall Mall, KOOL, GPC, Carlton, Lucky Strike and Misty. As of July 31, 2004, Brown & Williamson’s domestic tobacco business merged with R. J. Reynolds Tobacco Company, a New Jersey corporation, to form R. J. Reynolds Tobacco Company, a North Carolina corporation (“RJRT”). RJRT, a wholly-owned subsidiary of Reynolds American, Inc., is headquartered in Winston-Salem, N.C. It is the nation’s second largest manufacturer of cigarettes. Its brands include those of the former B&W as well as Winston, Salem, Camel and Doral. B&W is represented by Andrew R. McGaan of Kirkland & Ellis, LLP, in Chicago; Fred Erny of Dinsmore & Shohl in Cincinnati, Ohio; and Frank Gundlach of Armstrong Teasdale in St. -

Current Status of the Reduced Propensity Ignition Cigarette Program in Hawaii

Hawaii State Fire Council Current Status of the Reduced Propensity Ignition Cigarette Program in Hawaii Submitted to The Twenty-Eighth State Legislature Regular Session June 2015 2014 Reduced Ignition Propensity Cigarette Report to the Hawaii State Legislature Table of Contents Executive Summary .…………………………………………………………………….... 4 Purpose ..………………………………………………………………………....................4 Mission of the State Fire Council………………………………………………………......4 Smoking-Material Fire Facts……………………………………………………….............5 Reduced Ignition Propensity Cigarettes (RIPC) Defined……………………………......6 RIPC Regulatory History…………………………………………………………………….7 RIPC Review for Hawaii…………………………………………………………………….9 RIPC Accomplishments in Hawaii (January 1 to June 30, 2014)……………………..10 RIPC Future Considerations……………………………………………………………....14 Conclusion………………………………………………………………………….............15 Bibliography…………………………………………………………………………………17 Appendices Appendix A: All Cigarette Fires (State of Hawaii) with Property and Contents Loss Related to Cigarettes 2003 to 2013………………………………………………………18 Appendix B: Building Fires Caused by Cigarettes (State of Hawaii) with Property and Contents Loss 2003 to 2013………………………………………………………………19 Appendix C: Cigarette Related Building Fires 2003 to 2013…………………………..20 Appendix D: Injuries/Fatalities Due To Cigarette Fire 2003 to 2013 ………………....21 Appendix E: HRS 132C……………………………………………………………...........22 Appendix F: Estimated RIPC Budget 2014-2016………………………………...........32 Appendix G: List of RIPC Brands Being Sold in Hawaii………………………………..33 2 2014 -

Helsinki in Early Twentieth-Century Literature Urban Experiences in Finnish Prose Fiction 1890–1940

lieven ameel Helsinki in Early Twentieth-Century Literature Urban Experiences in Finnish Prose Fiction 1890–1940 Studia Fennica Litteraria The Finnish Literature Society (SKS) was founded in 1831 and has, from the very beginning, engaged in publishing operations. It nowadays publishes literature in the fields of ethnology and folkloristics, linguistics, literary research and cultural history. The first volume of the Studia Fennica series appeared in 1933. Since 1992, the series has been divided into three thematic subseries: Ethnologica, Folkloristica and Linguistica. Two additional subseries were formed in 2002, Historica and Litteraria. The subseries Anthropologica was formed in 2007. In addition to its publishing activities, the Finnish Literature Society maintains research activities and infrastructures, an archive containing folklore and literary collections, a research library and promotes Finnish literature abroad. Studia fennica editorial board Pasi Ihalainen, Professor, University of Jyväskylä, Finland Timo Kaartinen, Title of Docent, Lecturer, University of Helsinki, Finland Taru Nordlund, Title of Docent, Lecturer, University of Helsinki, Finland Riikka Rossi, Title of Docent, Researcher, University of Helsinki, Finland Katriina Siivonen, Substitute Professor, University of Helsinki, Finland Lotte Tarkka, Professor, University of Helsinki, Finland Tuomas M. S. Lehtonen, Secretary General, Dr. Phil., Finnish Literature Society, Finland Tero Norkola, Publishing Director, Finnish Literature Society Maija Hakala, Secretary of the Board, Finnish Literature Society, Finland Editorial Office SKS P.O. Box 259 FI-00171 Helsinki www.finlit.fi Lieven Ameel Helsinki in Early Twentieth- Century Literature Urban Experiences in Finnish Prose Fiction 1890–1940 Finnish Literature Society · SKS · Helsinki Studia Fennica Litteraria 8 The publication has undergone a peer review. The open access publication of this volume has received part funding via a Jane and Aatos Erkko Foundation grant. -

Appendix 1. Categorization of Cigarette Brands As Either Premium Or Discount

Appendix 1. Categorization of Cigarette Brands as either Premium or Discount Category Name of Cigarette Brand Premium Accord, American Spirit, Barclay, Belair, Benson & Hedges, Camel, Capri, Carlton, Chesterfield, Davidoff, Du Maurier, Dunhill, Dunhill International, Eve, Kent, Kool, L&M, Lark, Lucky Strike, Marlboro, Max, Merit, Mild Seven, More, Nat Sherman, Newport, Now, Parliament, Players, Quest, Rothman’s, Salem, Sampoerna, Saratoga, Tareyton, True, Vantage, Virginia Slims, Winston, Raleigh, Business Club Full Flavor, Ronhill, Dreams Discount 24/7, 305, 1839, A1, Ace, Allstar, Allway Save, Alpine, American, American Diamond, American Hero, American Liberty, Arrow, Austin, Axis, Baileys, Bargain Buy, Baron, Basic, Beacon, Berkeley, Best Value, Black Hawk, Bonus Value, Boston, Bracar, Brand X, Brave, Brentwood, Bridgeport, Bronco, Bronson, Bucks, Buffalo, BV, Calon, Cambridge, Campton, Cannon, Cardinal, Carnival, Cavalier, Champion, Charter, Checkers, Cherokee, Cheyenne, Cimarron, Circle Z, Class A, Classic, Cobra, Complete, Corona, Courier, CT, Decade, Desert Gold, Desert Sun, Discount, Doral, Double Diamond, DTC, Durant, Eagle, Echo, Edgefield, Epic, Esquire, Euro, Exact, Exeter, First Choice, First Class, Focus, Fortuna, Galaxy Pro, Gauloises, Generals, Generic/Private Label, Geronimo, Gold Coast, Gold Crest, Golden Bay, Golden, Golden Beach, Golden Palace, GP, GPC, Grand, Grand Prix, G Smoke, GT Ones, Hava Club, HB, Heron, Highway, Hi-Val, Jacks, Jade, Kentucky Best, King Mountain, Kingsley, Kingston, Kingsport, Knife, Knights, -

A Rhetorical Analysis of Selected Sermons by Sam Jones During His Emergence As a National Figure, 1872-1885

Louisiana State University LSU Digital Commons LSU Historical Dissertations and Theses Graduate School 1980 A Rhetorical Analysis of Selected Sermons by Sam Jones During His Emergence as a National Figure, 1872-1885. Herman Daniel Champion Jr Louisiana State University and Agricultural & Mechanical College Follow this and additional works at: https://digitalcommons.lsu.edu/gradschool_disstheses Recommended Citation Champion, Herman Daniel Jr, "A Rhetorical Analysis of Selected Sermons by Sam Jones During His Emergence as a National Figure, 1872-1885." (1980). LSU Historical Dissertations and Theses. 3553. https://digitalcommons.lsu.edu/gradschool_disstheses/3553 This Dissertation is brought to you for free and open access by the Graduate School at LSU Digital Commons. It has been accepted for inclusion in LSU Historical Dissertations and Theses by an authorized administrator of LSU Digital Commons. For more information, please contact [email protected]. INFORMATION TO USERS This was produced from a copy of a document sent to us for microfilming. While the most advanced technological means to photograph and reproduce this document have been used, the quality is heavily dependent upon the quality of the material submitted. The following explanation of techniques is provided to help you understand markings or notations which may appear on this reproduction. 1. The sign or “target” for pages apparently lacking from the document photographed is “Missing Page(s)”. If it was possible to obtain the missing page(s) or section, they are spliced into the film along with adjacent pages. This may have necessitated cutting through an image and duplicating adjacent pages to assure you of complete continuity. 2. -

Negativliste. Tobaksselskaber. Oktober 2016

Negativliste. Tobaksselskaber. Oktober 2016 Læsevejledning: Indrykket til venstre med fed tekst fremgår koncernen. Nedenunder, med almindelig tekst, fremgår de underliggende selskaber, som der ikke må investeres i. Alimentation Couche Tard Inc Alimentation Couche-Tard Inc Couche-Tard Inc Alliance One International Inc Alliance One International Inc Altria Group Inc Altria Client Services Inc Altria Consumer Engagement Services Inc Altria Corporate Services Inc Altria Corporate Services International Inc Altria Enterprises II LLC Altria Enterprises LLC Altria Finance Cayman Islands Ltd Altria Finance Europe AG Altria Group Distribution Co Altria Group Inc Altria Import Export Services LLC Altria Insurance Ireland Ltd Altria International Sales Inc Altria Reinsurance Ireland Ltd Altria Sales & Distribution Inc Altria Ventures Inc Altria Ventures International Holdings BV Batavia Trading Corp CA Tabacalera Nacional Fabrica de Cigarrillos El Progreso SA Industria de Tabaco Leon Jimenes SA Industrias Del Tabaco Alimentos Y Bebidas SA International Smokeless Tobacco Co Inc National Smokeless Tobacco Co Ltd Philip Morris AB Philip Morris Albania Sh pk Philip Morris ApS Philip Morris Asia Ltd Philip Morris Baltic UAB Philip Morris Belgium BVBA Philip Morris Belgium Holdings BVBA Philip Morris Belgrade doo Philip Morris BH doo Philip Morris Brasil SA Philip Morris Bulgaria EEOD Philip Morris Capital Corp Philip Morris Capital Corp /Rye Brook Philip Morris Chile Comercializadora Ltda Philip Morris China Holdings SARL Philip Morris China Management -

Studies in African Linguistics Volume 44, Number 2, 2015 Mauro Tosco

Studies in African Linguistics Volume 44, Number 2, 2015 FROM ELMOLO TO GURA PAU: A REMEMBERED CUSHITIC LANGUAGE OF LAKE TURKANA AND ITS POSSIBLE REVITALIZATION Mauro Tosco University of Turin This article discusses the “extinct” Elmolo language of the Lake Turkana area in Kenya. A surprisingly large amount of the vocabulary of this Cushitic language (whose community shifted to Nilotic Samburu in the 20th century), far from being lost and forgotten, is still known and is, to a certain extent, still used. The Cushitic material contains both specialized vocabulary (for the most part related to fishing) and miscellaneous and general words, mostly basic lexicon. It is this part of the lexicon that is the basis of recent revitalization efforts currently undertaken by the community in response to the changing political situation in the area. The article describes the Cushitic material still found among the Elmolo and discusses the current revitalization efforts (in which the author has, albeit marginally, taken part), pinpointing its difficulties and uncertain results. The article is followed by a glossary listing all the Cushitic words still in use or remembered by at least a part of the community.1 Keywords: Elmolo, Cushitic, language revitalization, language classification 1. The Elmolo people today The Elmolo are a small fishing community living near Lake Turkana, in northeast Kenya. Long considered “the smallest tribe of Kenya” and on the verge of extinction, the Elmolo have actually been increasing in number in recent years; while less than 100 people were counted by Spencer (1973), and Heine (1980) gave their number as approximately 200, they are today approximately 700 (Otiero 2008: 5 gives their number as 613 following a headcount he personally conducted). -

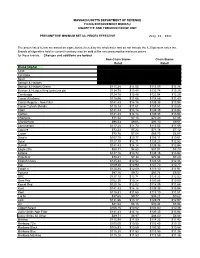

Cigarette Minimum Retail Price List

MASSACHUSETTS DEPARTMENT OF REVENUE FILING ENFORCEMENT BUREAU CIGARETTE AND TOBACCO EXCISE UNIT PRESUMPTIVE MINIMUM RETAIL PRICES EFFECTIVE July 26, 2021 The prices listed below are based on cigarettes delivered by the wholesaler and do not include the 6.25 percent sales tax. Brands of cigarettes held in current inventory may be sold at the new presumptive minimum prices for those brands. Changes and additions are bolded. Non-Chain Stores Chain Stores Retail Retail Brand (Alpha) Carton Pack Carton Pack 1839 $86.64 $8.66 $85.38 $8.54 1st Class $71.49 $7.15 $70.44 $7.04 Basic $122.21 $12.22 $120.41 $12.04 Benson & Hedges $136.55 $13.66 $134.54 $13.45 Benson & Hedges Green $115.28 $11.53 $113.59 $11.36 Benson & Hedges King (princess pk) $134.75 $13.48 $132.78 $13.28 Cambridge $124.78 $12.48 $122.94 $12.29 Camel All others $116.56 $11.66 $114.85 $11.49 Camel Regular - Non Filter $141.43 $14.14 $139.35 $13.94 Camel Turkish Blends $110.14 $11.01 $108.51 $10.85 Capri $141.43 $14.14 $139.35 $13.94 Carlton $141.43 $14.14 $139.35 $13.94 Checkers $71.54 $7.15 $70.49 $7.05 Chesterfield $96.53 $9.65 $95.10 $9.51 Commander $117.28 $11.73 $115.55 $11.56 Couture $72.23 $7.22 $71.16 $7.12 Crown $70.76 $7.08 $69.73 $6.97 Dave's $107.70 $10.77 $106.11 $10.61 Doral $127.10 $12.71 $125.23 $12.52 Dunhill $141.43 $14.14 $139.35 $13.94 Eagle 20's $88.31 $8.83 $87.01 $8.70 Eclipse $137.16 $13.72 $135.15 $13.52 Edgefield $73.41 $7.34 $72.34 $7.23 English Ovals $125.44 $12.54 $123.59 $12.36 Eve $109.30 $10.93 $107.70 $10.77 Export A $120.88 $12.09 $119.10 $11.91 -

ISAAC KOOL (COOL Or COLE)

r-E" cA* csii a.k^ i^a t 3^ ISAAC KOOL (COOL or COLE) CATHARINE SERVEN, MARRIED OCT. 15, 1764, AT (then Tappan^ Rockland pan of orange) Co.^ N . Y. THEIR DESCENDANTS COMPLETE TO MAY I, 1876. ALSO THEIR AMERICAN ANCESTORS FROM THE SETTLEMENT OK NEW YORK CITY. COMPILED FOR THE FAMILY REV. DAVID COLE, D.D., (Pastor the of Reformed Church of Yonkers, N. Y. ,) ONE OF THEIR GREAT-GRANDCHILDREN. -*• f NEW YORK: L JOHN F. TROW & SON, PRINTERS. 1876. *^^^(^^(C^%^^^ X^^t^/^^^n^^ >^ c?c^^^^ ISAAC KOOL (COOL or COLE) AND CATHARINE SERVEN, MARRIED OCT. 15, 1764, AT Tappan^ Rockland (then part of orange) Co., N'. 1. THEIR DESCENDANTS COMPLETE TO MAY I, 1876. ALSO THEIR AMERICAN ANCESTORS FKOM THE SETTLEMENT OK NEW YORK CITY. COMPILED FOR THE FAMILY BY REV. DAVID COLE, D.D., (Pastor of the Reformed Church of Yonkers, N. }'.J ONE OF THEIK GKEAT-GRANDCHILDREN. NEW YORK: JOHN F. TROW & SON, PRINTERS. 1876. Entered, according to Act of Congress, in the year 1S76, By Rev. DAVID COLE, In ;he Office of the Librarian of Congress at Washington. ^i/(: ; 1^ GENERAL INDEX OF CONTENTS. Introductory Statement to the Family. Remarks on Holland Names. York City) from Chronicles of Holland from 1579 to 1621 ; of New Amsterdam (now New 1609 to 1674; and of the Reformed (Dutch) Church in America from 1619 to 1700. Isaac Cole and Catharine Serven. PART I. —Their American Ancestors from the settlement of New Amsterdam, compris- ing one Holland-born and three American-born generations. This part also contains a beginning of the genealogy of the Holland Meyer family in America (continued in Part III).