Option Repricing, Management Turnover, and Restatement

Woody M. Liao Professor, A. Gary Anderson Graduate School of Management University of California, Riverside, USA

Hsiu-Ying Lee Associate Professor, Department of Accounting Tunghai University, Taiwan

Yi-Mien Lin* Professor, Department of Accounting National Chung Hsing University, Taiwan [email protected]

Chao-Kai Hsu Ernst & Young, Taiwan

September 10, 2010

JEL: M12, M52, M40

* Corresponding author Option Repricing, Management Turnover, and Restatement

Abstract

This study examines the association between financial restatements and executive option repricings and tests whether stock option repricings reduce management turnover in restating firms. We find a positive association between financial restatement and management turnover exists as well as financial restating firms are likely to implement option repricings when management equity compensation is large and the sensitivity of option value is high. However, we cannot find evidence that executive option repricings reduce management turnover in financial restating firms. Our analysis shows that, although financial restating firms may implement option repricing to restore the option incentive effect, valuable managers often leave their jobs because of the poor future prospects in the restating firms. Our results, therefore, suggest that the repricing of executive stock option is not an effective management retention strategy in financial restating firms.

Keywords: Management turnover, Executive Stock option, Option repricing, Financial restatement

2 1. Introduction

Financial restatement is a serious economic event. It signals that previously reported accounting information is not fairly presented in accordance with generally accepted accounting principles (GAAP). Prior research documents that financial restatements are often followed by negative market reactions and significant share price decreases (Kinney and McDaniel, 1989; DeFond and Jiambalvo, 1991; Dechow, Sloan and

Sweeney, 1996; Palmrose et al., 2004; GAO, 2003 and 2007). In addition to negative market reactions to restatements, a recent study by Desai, Hogan and Wilkins (2006) finds that 60 percent of restating firms experience at least one top manager turnover within 24 months of the restatement compared to that of 35 percent of matched non-restating firms.

Therefore, generally speaking, financial restating firms are likely to be punished by the market with share price declines and possibly management turnover.

Despite the possibility that managers may leave their jobs because of financial restatement events, companies sometimes implement option repricing strategy to restore the option incentive effect and retain valuable managers (Callaghan et al., 2004; Desai et al., 2006). But, option repricing is a controversial practice. Opponents of repricing argue that option repricing is to reward managers for poor stock performance. It weakens the link between management pay and performance (Gilson and Vetsuypens,

1993; Chance, Kumar and Todd, 2000; Brenner, Sundaram and Yermack, 2000;

Callaghan, Saly and Subramaniam, 2004). On the other hand, defenders of repricing argue that option repricing can help restore the incentive effect and realign the interests between management and shareholders (Hall, 1998; Murphy, 1999; Leonhardt, 2000).

In addition to the conflicting arguments among scholars, empirical evidence of the effectiveness of option repricing has also been mixed. Some find evidence that the adopters of option repricing have reduced management turnover (Kole, 1997; Core and

3 Guay, 2001; Ittner et al., 2003; Carter and Lynch, 2004). Others find evidence that option repricing firms have high management turnover (Daily, Certo and Dalton, 2002;

Chidambaran and Prabhala, 2003). As a result, it is difficult to conclude whether option repricing is an effective management retention strategy. But, generally speaking, it may be very difficult for a restating firm to retain valuable managers without option repricing to restore the option incentive effect. This is particularly true if the restating firm operates in a tight managerial labor market.

Thus, our motivation in this study is to examine the effects of financial restatement and option repricing on management turnover. Specifically, we first examine the relation between financial restatement and management turnover and then test whether option repricing affects management turnover in restating firms. Since not all restating firms implement option repricing, specific management compensation characteristics such as the size of executive equity compensation and the sensitivity of option value

(see Cheng and Warfield, 2005) may explain why or why not restatement leads to option repricing in restating firms. Therefore, we also examine whether the level of executive equity compensation and the sensitivity of option value play important roles in determining managerial adoption of option repricing in restating firms. The results of our study contribute to the literature by adding our knowledge about whether option repricing is an effective management retention strategy in restating firms.

The remainder of the paper is organized as follows. Section 2 presents review of relevant literature and development of hypothesis. Section 3 describes research design and empirical models. Section 4 reports research findings. Section 5 provides summary and concluding remarks.

4 2. Literature Review and Hypothesis

2.1 Financial restatement and management turnover

Financial restatement signals investors that non-GAAP accounting information has been issued by the firm. Prior studies document common characteristics of restating firms and provide strong evidence of negative market reactions to restatements. For example, Kinney and McDaniel (1989), DeFond and Jiambalvo (1991), and Sennetti and Turner (1999) find that financial restating firms have the following common characterizes: young, small size, low profitability, low growth, high leverage, no independent audit committee, high frequency of qualified opinion, and more diffuse ownership. Palmrose et al. (2004) also find that earning forecasts by the restating firms are often required a downward revision because of their abnormal stock returns and poor quality of financial statements. Another study by Palmrose and Schols (2004) find a significant relation between litigation again management and negative market reactions to financial restatements. Furthermore, a study of earnings manipulation by

Dechow et al. (1996) documents significant negative market reactions to a subset of

SEC enforcement actions. On the other hand, Beneish (1999) suggests that, using non-

GAAP accounting reports, managers protect self-interests and thus their stock trading behavior may signal a possible earnings management. Therefore, substantial evidence in the literature suggests negative market reactions to financial restatements that result from frauds or aggressive accounting practices.

Although the relation between negative market reactions and financial restatements has been substantially documented in prior research, evidence of financial restatements leading to management turnover has been mixed. Earlier studies find no evidence of significant relationship between management turnover and restatements (Agrawal et al.,

5 1999 and Beneish, 1999). Agrawal et al. (1999) conclude that it may be very costly sometimes for a firm to design an effective internal control system and to replace top managers. In another study, Beneish (1999) find that the SEC and the financial market tend to not seriously punish management for overestimation of earnings. But, due to the recent trend of attention in corporate governance and concern of regulators, more current studies document a significant association between financial restatements and management turnover. For example, the result of Carter and Lynch (2004) study suggests that market return is negatively related to management turnover rate. This implies that a low stock return resulting from restatements is likely followed by a high management turnover. Desai et al. (2006) also find that the market seriously punishes management for financial restatements. They find that 60% of the restating firms experience management turnover and the displaced manager’s subsequent new job is inferior to the prior position. Therefore, unlike earlier studies, more recent research supports that financial restatements are likely to lead to negative market reactions, decreases in the stock prices, and possibly management turnover. Accordingly, we develop the following hypothesis to test the association between management turnover and financial restatements:

H1: Management turnover is positively associated with financial restatement.

2.2 Compensation characteristics and option repricing after restatement

In the modern highly competitive business environment, equity-based compensation plans offer managers incentives to maintain competitive and continuous business success. Smith and Stulz (1985) assert that stock options may be used to alleviate the effects of managerial risk aversion and align the interests between managers and shareholders.1 Also, Morck, Shleifer and Vishny (1988), and McConnell

1 Also, Core, Guay and Larcker (2003) indicate that the main component in management compensation

6 and Servaes (1990) point out that executive equity ownership is an important mechanism to align the interests between management and shareholders. Since the early

1990s, investors and corporate policymakers have increasingly looked to equity-based compensation (such as restricted stocks and stock options) to strengthen the link between management pay and performance. As a result, stock option grants have become a popular and important component of executive compensation package in the past 15 years. But, the incentive effect of executive stock options may decrease or disappear when a restating firm experiences a significant fall in the share price. To restore the incentive effect of stock options, the firm may reset a lower exercise price for the options (also known as option repricings).2

Morgan and Poulsen (2001) find evidence that stock option plans increase the

value of firm. Other research also supports the strategy of using stock options to align

the interests between managers and shareholders and to retain valuable managers in the

firm. For example, Kole (1997) and Core and Guay (2001) find that, when managerial

experience and knowledge are expensive, stock option grants can be used to retain

managers in the firm. Ittner, Lambert and Larcker (2003) also find that equity

compensations in stocks and stock options represent about 80% of total management

compensation and new economy firms use them to retain valuable managers.

But, stock option plans may have some implementation issues. First, because of

information asymmetry, managers can sell their equity holdings to avoid the future loss

before releasing poor performance information. Bartov and Mohanram (2004) find

strong evidence that management uses private information to time option exercises and

plans is stock options. Morgan and Poulsen (2001) find that the market reacts positively to compensation plans linked to performance and shareholders are in favor of adopting stock options to reduce agency cost for firms with serious agency problem. 2 Prior studies did not clearly distinguish between option reissuing and option repricing. In the past, researchers used option resetting to cover both option reissuing and option repricing (Brenner, Sundaram and Yermack, 2000; Chance, Kumar and Todd, 2000). But, more recent studies clearly distinguish between option repricing (Carter and Lynch, 2001, 2003, 2004) and option reissuing (Coles, Hertzel and Kalpathy, 2006). Our study focuses on option repricing.

7 increase the value of their options. Therefore, although stock option plans can help align the interests between management and shareholders, managers often gain from timing option grants and exercises. Second, the incentive value of tock options may decrease or disappear when the share price declines. An out-of-money (underwater) stock option has no market value on the expiration date and becomes no value for managers. In this case, the promise of the option compensation becomes valueless and valuable managers may seek for better opportunities and leave the firm (Leonhardt,

2000).

In order to maintain the incentive value of stock option, the option issuing firm may reset the exercise price of the stock option (Hall, 1998; Murphy, 1999). However, repricing stock option is a controversial practice. Brenner et al. (2000) and Chance et al. (2000) find that option repricings accompany firms with poor performance.

Callaghan et al. (2004) further find evidence that management often announces good news after and bad news before option repricing to achieve the purpose of lowering new exercise price and enhance the value of options. Coles et al. (2006) also find that discretionary accruals are abnormally low until option repricing. Hence, opponents of repricing argue that option repricing rewards managers for poor performance and is not consistent with the interest of shareholders (Moore, 1999; Reingold, 1999). However, supporters of repricing justify that option repricing can realign the interests between managers and shareholders and retain valuable managers (Hall, 1998; Murphy, 1999;

Carter and Lynch, 2001). In another study, Carter and Lynch (2004) find evidence that option repricing reduces management turnover. But, Daily et al. (2002) and

Chidambaran and Prabhala (2003) report evidence that repricing firms have higher management turnover.

Therefore, while recent research provides evidence that restatements are likely to

8 lead to negative market reactions and share price decreases, option repricing after

restatement is only found in some but not all restating firms. A possibility regarding

why some restating firms do not implement option repricing after restatement is that

the cost of repricing may exceed the benefit. This is so because option repricing often

comes with high costs of implementation, reputation, and possible unsuccessful

retention of valuable managers. Furthermore, shareholder groups generally expressed

major concern about the high repricing costs and often opposed the practice directly.

Cheng and Warfield (2005) indicate that option repricing may restore the incentive

effect, but it also incurs costs such as reputation loss arising from frequent repricings.

But, even if repricing does produce a positive effect on management incentives going

forward, there is still the question of whether this incentive is worth the cost of paying

poor stock performance resulting from restatements. Carter and Lynch (2003) also

agree that firms with high cost of repricing are not likely to reset their stock options

because they do not create cost-effective incentives.

It is interesting to note that the relation between management compensation plans and management incentives has received a great deal of research interests in recent years. For example, Cheng and Warfield (2005) examine the link between management equity incentives and earnings management. The degree of management equity incentives is measured by the ratio of management equity compensation to the market value of outstanding shares. It is a proxy for the degree of management self-interest incentives in equity compensation. As expected, Cheng and Warfield (2005) find that equity incentives motivate managers to engage in earnings management. Burns and

Kedia (2006) on the other hand investigate the effect of stock options on management adoption of aggressive accounting practices. They find that option incentives affect the likelihood of managerial engaging in unusual accounting practices that result in

9 financial restatements. They measure option incentives in terms of the sensitivity of option value due to the stock price changes. In other words, management option incentives induce managerial desire to adopt unusual accounting practices that result in financial restatements. Collectively, this line of research suggests that equity compensation characteristics play important roles in managerial engagement of earnings management and stock option strategies to protect managers’ self-interests. Accordingly, we follow this line of research and expect that large equity and high option incentives induce management adoption of option repricing to protect self-interests in financial restating firms. Therefore, we hypothesize that

H2: Large equity compensation and high option value incentives induce management adoption of option repricing to protect self-interests in financial restating firms.

2.3 Effect of option repricing on management turnover in restating firms

Stock option repricing is a controversial practice. Opponents of repricing argue that

option repricing rewards managers for poor performance and is not consistent with the

interest of shareholders (Moore, 1999; Reingold, 1999). However, supporters justify

that option repricing can realign the interests between managers and shareholders and

retain valuable managers (Hall, 1998; Murphy, 1999; Carter and Lynch, 2001). Not

surprisingly, empirical evidence of the incentive and retention effect of option

repricing has also been mixed. For example, Carter and Lynch (2004) and Ittner et al.

(2003) find evidence that option repricing is likely to reduce management turnover.

But, Daily et al. (2002) and Chidambaran and Prabhala (2003) find that repricing firms

have higher management turnover. Given that option repricing is a controversial

practice and the empirical evidence of its effectiveness is mixed, we develop no formal

hypothesis to test our research question on how option repricing affects management

10 turnover in restating firms. However, we develop a regression model in the next

section to shed additional light on the effect of option repricing on management

turnover in financial restating firms.

3. Research Design

3.1 Empirical model

We develop three empirical models to test each of our three research questions

(two with a formal hypothesis and one without a formal hypothesis as explained above).

For each of the regression analysis, we employ the White Test to make sure no heterogeneity problem in our data. Also, because we use the panel data in this study, both of the random and the fixed effects are analyzed in our regression Models 1 and 3, but not in our logistic Model 2. For easy reference, the definition and proxy for each variable are listed in Table 1.

Model 1: Effect of financial restatement on management turnover

TURNOVi,t a0 a1RSTi,t a2 RETURNi,t a3EQUITYi,t a4SENSITi,t a HITECH a GROW a TA a ROE a NPM 5 i,t 6 i,t 7 i,t 8 i,t 9 i,t (1)

YEAR i,t where TURNOV: management turnover during the year of restatement, RST: 1 if restatement, and 0 otherwise, RETURN: stock return, EQUITY: equity compensation incentives, SENSIT: sensitivity of stock option value, HITECH: a dummy variable for high-tech firm, GROW: growth potential of the firm, TA: firm size, ROE: return on equity, NPM: profit margin.

Model 2: Effect of compensation characteristics on option repricing

11 REPRICEi,t b0 b1RSTi,t b2TURNOVi,2average b3RSTi,t *TURNOVi,2average b RETURN b RST * RETURN b SENSIT b EQUITY 4 i,t 5 i,t i,t 6 i,t 7 i,t (2)

b8HITECHi,t b9GROWi,t b10TAi,t b11ROEi,t b12 NPM i,t i,t

where TURNOVi,2average is the average of management turnover rates in year t-1 and year t-2. This specific variable is used in Model 2 to capture the effect of past management turnover on current option repricing strategy. We expect that a restating firm is more likely to adopt option repricing to reduce a continuous management turnover in the current year. Other variables are defined as those in Model 1.

Model 3: Effect of option repricing on management turnover in restating firms

TURNOVi,t b0 b1RSTi,t b2 REPRICEi,t b3RSTi,t * REPRICEi,t

b4 RETURNi,t b5 RSTi,t * RETURNi,t b6SENSITi,t b7 EQUITYi,t (3) b8HITECHi,t b9GROWi,t b10TAi,t b11ROEi,t b12 NPM i,t

YEAR i,t

where TURNOV is management turnover for the year with financial restatement and option repricing. All other variables in Model 3 are defined the same as before.

------Insert Table 1 ------

3.2 Data

In this study, we examine the effect of financial restatement and stock option repricing on management turnover during 1997–2004. Since FASB announced new requirements for accounting stock option repricing in 1998, we exclude the year of 1998 in our analysis. Accordingly, we first search the Lexis/Nexis database to identify firms

12 that have adopted stock option repricing from 1997-2004.3 Our sample firms with financial restatement are obtained from the Financial Statement Restatement Database issued by the United States Government Accounting Office (GAO, 2003 and 2007). All financial statement data and top-five managers’ data are obtained from Compustat and

ExecuComp, respectively. Our sample selection criteria include: publicly traded firms with executive stock options, availability of financial data, availability of management turnover data, non-finance or non-insurance firms with the SIC code starting from 60 to

67. The result of the sample selection process is summarized in Table 2. The final available sample of firm-year with stock options is 2911 which includes 106 financial restatements and 42 option repricings.

------Insert Table 2 ------

Table 3 reports the statistic distribution of our sample data. Panel A shows the sample number of option repricings and restatements. Panel B exhibits the industry distribution of all sample firms. As shown in Panel A, the total number of direct option repricings is 42 and the year of 2001 has the largest number of repricings (11). With respect to the distribution of restatements, the latter years have more restatements than the earlier years. This is expected because the SEC has expanded regulations in the recent years and the Sarbanes-Oxley Act of 2002 has more detailed requirements for financial statement disclosures. Moreover, the year of 2003 has the largest number of financial restatements (28). As reported in Panel B of Table 3, the high-tech industry with the SIC code of 35, 36, 38 and 73 has more restating and repricing firms than other industries.

3 We use survey language: option! w/1 reprice! and filing-date=1999 to search for firms adopting direct option repricing in the sample period.

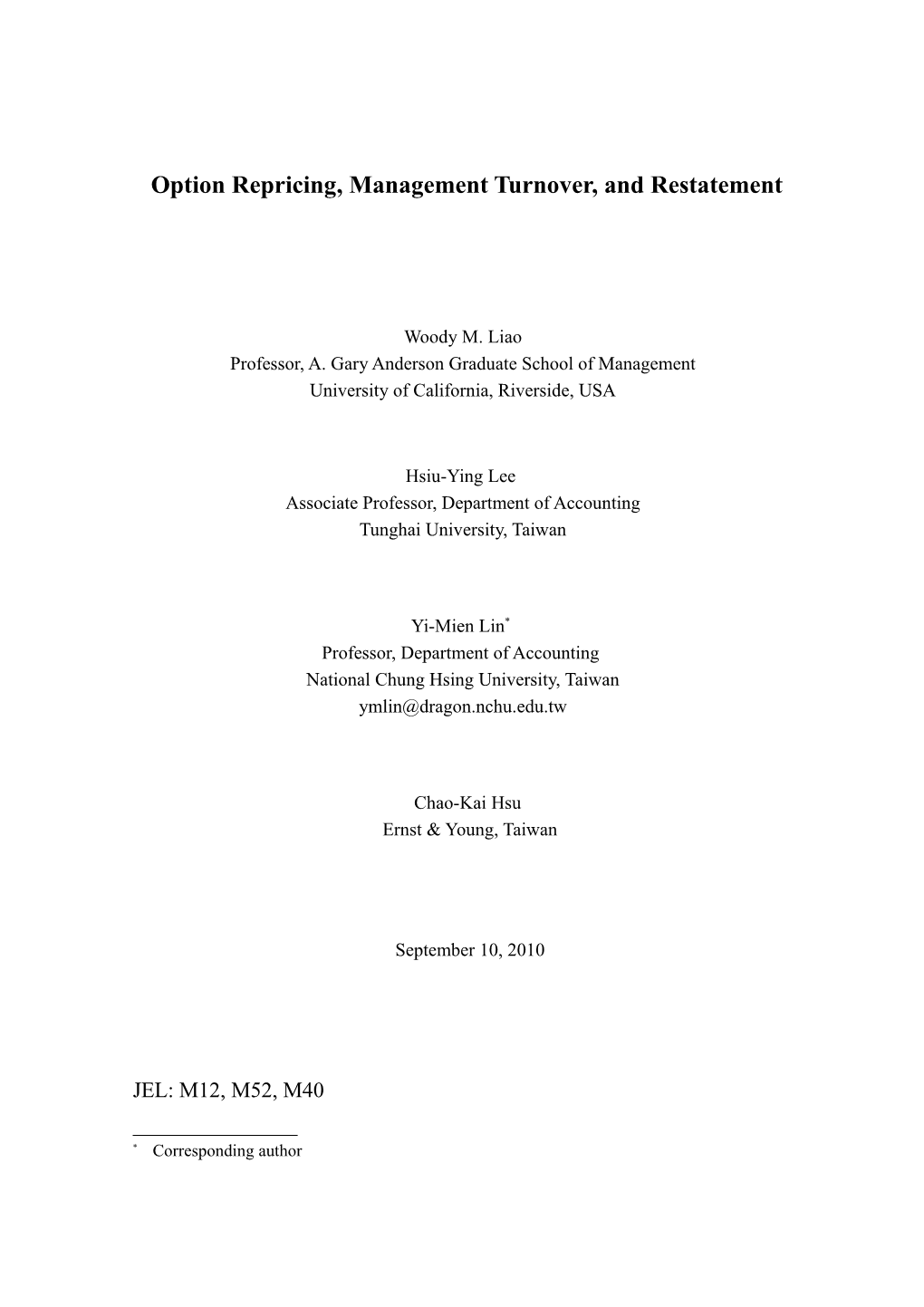

13 Figure 1 displays the volatility of the stock returns within 20 days around the announcement of restatement, where day 0 is the announcement date of restatement.

The results reported in Figure 1 appear to be consistent with Palmrose et al. (2004) finding that stock returns are negative around the announcement date of restatement.

This suggests that the immediate market reaction to restatement is negative. In addition, we report the reasons of restatements in Table 4. It shows that revenue recognition and expense or cost classifications are the main reasons for financial restatements in our sample period.

------Insert Table 3 ------Insert Figure 1 ------Insert Table 4 ------

3.3 Variables

Dependent variables

Model 1 tests the effect of financial restatement on management turnover. We obtain the dependent variable (TURNOV) data from the ExecuComp database.4 This dependent variable measures the percentage change in management turnover. It is measured by the change in management turnover rate from year t-1 to year t. That is the previous period’s management turnover rate minus the current period’s management turnover rate. Model 2 tests the association between option repricing and financial restatement. We obtain the dependent variable (REPRICE) from the Lexis/Nexis database. REPRICE is a dummy variable that is equal to 1 if the restating firm reprices

4 TURNOV variable is a dependent variable measured by the management turnover rate in the year of restatement in Model 1 and Model 3. But, it is an independent variable in Model 2 with a different definition and measure (i.e., the average of management turnover rates in year t-1 and year t-2).

14 executive stock options and 0 otherwise. Model 3 analyzes whether option repricing affects management turnover in the restating firms. We use the same dependent variable

(TURNOV) as defined in Model 1.

Explanatory variables

Financial restatement (RST) is a dummy variable. It is equal to 1 if restatement is announced, and 0 otherwise. We obtain the RST data from the Financial Restatement database issued by GAO in 2003 and 2007. We expect that RST is positively related to management turnover and option repricing.

The size of executive equity compensation incentive (EQUITY) is computed by total management equity compensations divided by the market value of common shares outstanding at the end of the year. We expect that equity compensation incentive is positively related to option repricing and negatively related to management turnover.

The sensitivity of stock option value (SENSIT) is computed by the value of stock options multiplied by 0.01, in which the value of stock options is obtained from the

Black-Scholes value provided by ExecuComp. We expect that the sensitivity of the option value is positively related to option repricing and negatively related to management turnover.

Control variables

The stock return (RETURN) will move downward when the firm announces restatement. A low stock return is likely to lead to management turnover and option repricing. Therefore, we control the effect of RETURN in the regression analysis of option repricing and management turnover. Also, we use book-to-market ratio to measure the growth potential of a firm (GROW) and control its effect on option repricing and management turnover. Managers may be more willing to stay in a firm

15 with high growth and these firms may also offer higher incentive for retaining valuable managers. Therefore, we expect that growth potential is positively related to repricing of stock option and negatively related to management turnover. Because the repricers often have negative performance, we control the effect of return on equity (ROE) and margin profit (NPM) on management turnover and option repricing. ROE is income before income tax divided by total equity. NPM is income before extraordinary items divided by sales, then multiplied by 100.

Furthermore, high-tech firms are usually operating in a tighter labor market, so they are more likely to adopt option repricing to retain talented managers. We refer to the definition of high-tech firms used in Carter and Lynch (2004), and control the effect of HITECH on option repricing and management turnover. Finally, we control for the effect of the firm size by using TA as a proxy for the size. TA is measured by taking log of total assets at the end of each period.

4. Empirical Results

4.1 Preliminary analysis

Table 5 presents descriptive statistics and univariate test results of the mean

(median) difference for each variable between those restating firms with and without repricing. In all cases, the results of the mean (median) test are generally consistent as expected. For example, those with repricing have a higher management turnover than those without repricing. This suggests that repricing did not reduce average management turnover (p = 0.0634), but the result of the median test is not significant

(p= 0.284). Also, those without repricing have a higher mean of stock return (p =

0.0189) and profit margin (p = 0.002) than those with repricing. It implies that repricing is more likely adopted by firms with poor performance. Similarly, both the mean of

16 equity incentive and the mean of option sensitivity for those with repricing are higher than those without pricing. This indicates that repricing is more likely associated with high equity compensation and option sensitivity, but the result of the median test is not significant.

For the dummy variable (HITECH), the mean and the median for sample firms with repricing are higher than those without repricing (p = 0.096 and p = 0.013, respectively). This result indicates that option repricings are widely adopted in the high- tech industry. Interestingly, we also find that those with repricing have a lower growth potential which is consistent with the general expectation that repricing is more likely to be adopted by firms with poor performance. As expected, those without repricing have a larger mean of total assets (TA) than those with repricing (p = 0.0764). This suggests that option repricers are small in size. Finally, the mean and median of profit margin

(NPM) for those without repricing are higher than those with repricing (p = 0.0501 and p = 0.063, respectively). This implies that option repricers are less profitable firms.

------Insert Table 5 ------Insert Table 6 ------

4.2 Correlation coefficients

Table 6 reports Pearson correlation coefficients of our model variables.

Management turnover is positively correlated with financial restatement (0.0407, p =

0.016). This suggests that management turnover is related to financial restatement. But, management turnover is not significantly correlated with option repricing (0.0262, p =

0.1207). This suggests that option repricing may not reduce management turnover. On the other hand, option repricing is positively correlated with equity

17 compensation (0.0337, p = 0.0463), but insignificantly correlated with the sensitivity of option value (0.0179, p = 0.2905). This suggests that equity compensation has a significant effect on option repricing, but the sensitivity of option value has only a moderate effect on option repricing. As expected, high tech is positively correlated with management turnover (0.063, p = 0.002) and option repricing (0.039, p = 0.0193). This result is consistent with prior research finding that high tech firms operate in competitive labor markets and often implement option repricing to retain managers in their firms.

4.3 Regression analysis

4.3.1 Association between financial restatement and management turnover

In our OLS regression analysis of Model 1 to test the relation between financial restatement and management turnover, we adopt the White Test to make sure that there is no heterogeneity problem in our data. Also, given that most of the VIF value of our variables is approximately 1.23 and far less than 10, we conclude that our regression model does not appear to have the collinearity problems.5 Furthermore, because we use the panel data in this study, we decided to analyze both the random effect and the fixed effect in the regression analysis and to control the effect of using data from different years to avoid the time-series effect. From the Hausman test, we find 2 = 31.4 meeting the significance level of 10%. Although our result supports the fixed effect model better than the random effect model (p = 0.0003), both models have high goodness of fit and meet the significance level of 10%.

Results of the regression analysis for Model 1 are presented in Table 7. We find a positive association between restatement and management turnover in both the fixed 5 The VIF value of each variable is not listed in Table 7 because each VIF meets the critical value for no collinearity problem.

18 effect and the random effect models. As expected, this result is consistent with the prior research finding that management is responsible for financial restatement resulting from non-GAAP financial reports (Desai, et al., 2006). As a result of financial restatement, managers are likely to leave their jobs because of poor future prospects in the firm or are forced to leave because of the punishment pressure from the market. Furthermore, our results show high management turnover in high-tech, low profitability, or low growth firms. Overall, our results support H1.

------Insert Table 7 ------

4.3.2 Effect of compensation characteristics on option repricing

As discussed earlier, management compensation characteristics (equity compensation and option value incentives) are likely to motivate managers to engage in strategies such as aggressive accounting and option repricing to protect their self- interests. Therefore, the purpose of Model 2 is to test the effect of the size of equity compensation (EQUITY) and the sensitivity of option value (SENTIV) on option repricing. Table 8 reports the results of the regression analysis of Model 2. As expected, option repricing is positively related to the size of equity compensation (p = 0.012) and the sensitivity of option value (p = 0.033). This result suggests that executive equity compensation and option value incentives are important determinants of option repricing. Moreover, the results of the regression analysis also show that low firm growth, high-tech, and low stock return are significantly associated with option repricing. Therefore, our results support H2.

------Insert Table 8 ------

19 4.3.3 Effect of option repricing on management turnover in restating firms

Executive option repricing is a controversial practice in the investment community.

Not surprisingly, prior empirical evidence of its incentive effects has also been mixed in the literature. As explained in the research design section, we do not formulate a formal hypothesis to test the retention effect of option repricing on management turnover.

However, we develop Model 3 to explore whether option repricing reduces management turnover in restating firms. Table 9 reports the results of the regression analysis of

Model 3. As shown in the regression analysis, management turnover is not significantly related to option repricing in both the random effect model (p = 0.309) and the fixed effect model (p = 0.286). This result suggests that option repricing is not effective in retaining managers in restating firms.

However, all of the other explanatory and control variables except profit margin

(NPM) are significantly related to management turnover. For example, management turnover is related to restatement. This implies that, because of financial restatement, managers are forced to leave or willing to leave for better job opportunities in the labor market. Furthermore, high-tech, low profitability, and low firm growth are associated with higher management turnover. This result also implies that more management turnover because of poor future prospects in the firm or better job opportunities in the labor market. Finally, equity compensation incentives and sensitivity of option values are positively related to management turnover. This result implies that more management turnover is associated with significant decreases in equity compensation and option value incentives because of the restatement problem and poor performance in the firm. Overall, our results support the argument that option repricing is not effective in retaining valuable managers in restating firms.

20 ------Insert Table 9 ------

5. Summary and Conclusion

A financial restatement signals that previously reported accounting information is not fairly presented in accordance with generally accepted accounting principles.

Thus, financial restatement is likely to lead to negative market reactions and a drop in the market value of the firm. As a result, the incentive value of executive stock options declines and managers may leave for other job opportunities. To restore the incentive value of stock option, the option issuing firm may reprice the stock option and realign the interests between valuable managers and shareholders. However, option repricing is a controversial practice and empirical evidence of its incentive and retention effects so far has been mixed.

In this study, we are motivated to investigate the effects of financial restatement and option repricing on management turnover. We first examine the relation between financial restatement and management turnover and then test whether option repricing affects management turnover in restating firms. We find that financial restatement is positively related to management turnover. This finding suggests that managers are responsible for faulty financial statements and are forced to leave or managers are willing to leave for other job opportunities because of the poor future prospects in the restating firm.

We also investigate whether management uses option repricing to restore the incentive value of stock options or to protect their self-interests from stock rice changes due to financial restatement. We find a positive relation between option repricing and management equity and option value incentives. This result suggests that large equity

21 compensation and high option value incentives motivate managers to implement option repricing in financial restating firms.

However, our analysis shows that option repricing did not reduce management turnover in financial restating firms. This result further suggests that, even though financial restating firms implement option repricing to realign the interests between valuable managers and shareholders, managers often leave the firm for other job opportunities in the labor market. Therefore, our results support the argument that option repricing is not effective in the retention of valuable managers in restating firms.

This finding suggests that, although executive option repricing is a managerial retention strategy, it produces less successful results in financial restating firms.

22 Reference

Agrawal, A., J. Jaffe, and J. Karpoff. 1999. Management Turnover and Governance Changes Following the Revelation of Fraud. Journal of Law and Economics 42 (April): 309-342. Baker, T., C. Denton, and R. Austin. 2003. Stock Option Compensation and Earnings Management Incentives. Journal of Accounting, Auditing and Finance 18(4): 557- 582. Bartov, E. and P. Mohanram. 2004. Private Information, Earnings Manipulations, and Executive Stock-Option Exercises. The Accounting Review 79(4): 889-920. Beneish, M. D. 1999. Incentives and Penalties Related to Earnings Overstatements that Violate GAAP. The Accounting Review 74(4): 425-457. Bebchuk, L. A. and J. M. Fried, 2004. Pay without Performance: The Unfilled Promise of Executive Compensation. Cambridge, MA: Harvard University Press. Brenner, M., R. Sundaram, and D. Yermack. 2000. Altering the Terms of Executive Stock Options. Journal of Financial Economics 57(1): 103-128. Burns, N. and S. Kedia. 2006. The Impact of Performance-Based Compensation on Misreporting. Journal of Financial Economics 79(1): 35-67. Callaghan, S. R., P. J. Saly, and C. Subramaniam. 2004. The Timing of Option Repricing. Journal of Finance 59(4): 1651-1676. Carter, M. E. and L. J. Lynch. 2001. An Examination of Executive Stock Option Repricing. Journal of Financial Economics 61(2): 207-225. Carter, M. E. and L. J. Lynch. 2003. The Consequences of the FASB's 1998 Proposal on Accounting for Stock Option Repricing. Journal of Accounting and Economics 35(1): 51-72. Carter, M. E. and L. J. Lynch, 2004. The Effect of Stock Option Repricing on Employee Turnover. Journal of Accounting and Economics 37(1): 91-112. Chance, D., R. Kumar, and R. Todd. 2000. The Repricing of Executive Stock Options. Journal of Financial Economics 57(1): 129-154. Cheng, Q. and T. Warfield, 2003. Stock-Based Compensation, Earnings Management to Meet Analysts' Forecasts, and the Informativeness of Earnings. SSRN Working Paper. Cheng, Q. and T. D. Warfield. 2005. Equity Incentives and Earnings Management. The Accounting Review 80(2): 441-476.

23 Chidambaran, N. K. and N. R. Prabhala. 2003. Executive Stock Option Repricing, Internal Governance Mechanisms, and Management Turnover. Journal of Financial Economics 69(1): 153-189. Coles, J. L., M. Hertzel, and S. Kalpathy. 2006. Earnings Management Around Employee Stock Option Reissues. Journal of Accounting and Economics 41(1/2): 173-200. Core, J., W. Guay. 2001. Stock Option Plans for Nonexecutive Employees. Journal of Financial Economics 61(2): 253-287. Core, J., W. Guay, and D. Larcker. 2003. Executive Equity Compensation and Incentives: A Survey. Economics Policy Review 9(1): 24-27. Daily, C., S. Certo, and D. Dalton. 2002. Executive Stock Option Repricing, Retention and Performance Reconsidered. California Management Review 44(4): 8-23. Dechow, P. M., R. G. Sloan, and A. P. Sweeney. 1996. Causes and Consequences of Earnings Manipulation: An Analysis of Firms Subject to Enforcement Actions by the SEC. Contemporary Accounting Research 13(1): 1-36. DeFond, M. L. and J. Jiambalvo. 1991. Incidence and Circumstances of Accounting Errors. The Accounting Review 66(3): 643-655. Denis, D. J., D. K. Denis, and A. Sarin. 1997. Ownership Structure and Top Executive Turnover. Journal of Financial Economics 45(2): 193-222. Desai, H., C. E. Hogan, and M. S. Wilkins. 2006. The Reputational Penalty for Aggressive Accounting, Earnings Restatements and Management Turnover. The Accounting Review 81(1): 83-112. Gilson, S., M. Vetsuypens. 1993. CEOs Compensation in Financially Distressed Firms: An Empirical Analysis. Journal of Finance 48(2): 425-458. Hall, B. 1998. The Pay to Performance Incentive of Executive Stock Options. Working Paper No.6674, NBER. Ittner, C. D., R. A. Lambert, and D. F. Larcker. 2003. The Structure and Performance Consequences of Equity Grants to Employees of New Economy Firms. Journal of Accounting and Economics 34(1-3): 89-127. Jensen, M. C. and W. H. Meckling. 1976. Theory of the Firm, Managerial Behavior, Agency Costs, and Ownership Structure. Journal of Financial Economics 3 (4): 305-360. Kinney, J. W. and L. S. McDaniel. 1989. Characteristics of Firms Correcting Previously Reported Quarterly Earnings. Journal of Accounting and Economics 11(1): 71-93.

24 Kole, S. 1997. The Complexity of Compensation Contracts. Journal of Financial Economics 43 (1): 79-104. Lazar, G. 2001. Keep Your Key People. Electronic Business: May 2001, p. 86-94. Leonhardt, D. 2000. Technology Share Downturn Diminishing Stock Options. The New York Times. April 19, 2000, p. C1. McConnell, J. and H. Servaes. 1990. Additional Evidence on Equity Ownership and Corporate Value. Journal of Financial Economics 27, 593–612. Moore, B. 1999. Investor Advocates Press Companies to Curb Stock-Option Repricings. Wall Street Journal: March 10, p. C2. Morck, R., A. Shleifer, and R. W. Vishny. 1988. Management Ownership and Market Valuation: An Empirical Analysis. Journal of Financial Economics 20 (1-2): 293- 315. Morgan, A. G. and A. B. Poulsen. 2001. Linking Pay to Performance-Compensation Proposals in the S&P 500. Journal of Financial Economics 62(3): 489-523. Murphy, K. 1999. Executive Compensation. In Handbook of Labor Economics, edited by O. Ashenfelter, and D. Card, 2485-2563. Amsterdam, The Netherlands: Elsevier. Palmrose, Z. V., V. J. Richardson, and S. Scholz. 2004. Determinants of Market Reactions to Restatement Announcements. Journal of Accounting and Economics 37(1): 59-89. Palmrose, Z. V., S. Scholz, and J. M. Wahlen. 2004. The Circumstances and Legal Consequences of Non-GAPP Reporting: Evidence from Restatements. Contemporary Accounting Research 21(1): 139-190. Reingold, J. 1999. Anatomy of a Unusual Stock-Option Windfall. The Wall Street Journal: June 2, P. B1. Sennetti, J.T. and J. L. Turner. 1999. Post-audit Restatement Risk and Brand-name Audits. Working Paper, Nova Southeastern University. Smith, C. and R. Stulz. 1985. The Determinants of Firms' Hedging Polices. Journal of Financial and Quantitative Analysis 20(4): 391-405. Yermack, D. 1997. Good Timing: CEOs Stock Option Awards and Company News Announcements. Journal of Finance 52(2): 476-449.

25 Table 1 Summary of Abbreviation, Definition, and Proxy of Variables

Abbreviation Definition Proxy Sources

RST Restatement We set to 1 if the firm Financial has restatement, Statement Restatement otherwise 0. Database, GAO REPRIC Repricing of stock We set to 1 if the firm Lexis/Nexis options has repricing of stock options, otherwise 0. TURNOV Management The % change in the ExecuComp turnover top-five executives turnover EQUITY Executive equity Total management ExecuComp compensation equity compensation / market value of common stocks at the ending of the year SENSIT Sensitivity of the The % change in the ExecuComp / stock option value stock option value LexisNexis when there is a change of 1% in the stock return. GROW Firm growth market value of equity Compustat at year-end / book value of equity at year-end HITECH High-tech firm 1 for high-tech firm, 0 Compustat for non-high-tech firm. TA Firm size Log (Total assets at the Compustat ending of the year) ROE Return on equity Income before tax / Compustat total shareholders equity NPM Margin profit (income before Compustat extraordinary items /net sales)*100 RETURN Stock return Stock return at the end Compustat of the year

26 Table 2 Sample Selection Process for Firms with Stock Options In Compustat, the $c cs active module (firm-year)* 129413 Lack of management turnover in ExecuComp (113725) Unusable data (e.g., management compensation is negative) (976) Finance and Insurance firms (the first number of the SIC code is 6) (1535) Financial data unavailable (10266) Available samples (firm - year) 2911 * Various choices of sample firms are available in Compustat, for example, S&P 500, S&P 1000,…etc. Because the number of option repricing firms is small, we use the $c cs active module that includes most firms with stock options. All companies in the database are actively traded in the US. This excludes Canadian companies not traded on U.S. exchanges, but includes ADRs.

Table 3 Year Distribution and Industry Distribution of Samples

27 Panel A: Year Distribution Year Repricing firm Restatement firm Year Repricing firm Restatement firm 1997 3 2 2001 7 18 1998 - - 2002 10 21 1999 3 6 2003 4 28 2000 11 9 2004 4 22 Total 42 106

Panel B:Industry distribution SIC code Kind Number SIC code Kind Number of firms of firms 1 Agriculture Production-Crops 3 41 Transit and Passenger Trans 4 7 Agricultural Services 1 42 Motor Freight Trans,Warehous 32 10 Metal Mining 37 44 Water Transportation 8 13 Oil and Gas Extraction 99 45 Transportation by Air 29 14 Mining, Quarry Nonmetal Minerals 14 47 Transportation Services 12 15 Bldg Construction, General Construction 13 48 Communications 23 Builders 16 Heavy Construction other than Building 21 49 Electric, Gas and Sanitary Services 52 Construction Contractor 20 Food and Kindred Products 79 50 Durable Goods-Wholesale 91 21 Tobacco Products 2 51 Nondurable Goods-Wholesal 17 22 Textile Mill Products 36 52 Bldg Matl, Hardwr, Garden-Retl 12 23 Apparel and Other Finished Products 52 53 General Merchandise Stores 23 24 Lumber and Wood Products, Excluding 29 54 Food Stores 8

28 Furniture 25 Furniture and Fixtures 39 55 Auto Dealers, Gas Stations 11 26 Paper and Allied Products 55 56 Apparel and Accessory Stores 101 27 Printing, Publishing and Allied 78 57 Home Furniture, Furnishings and Equipment 23 Stores 28 Chemicals and Allied Products 302 58 Eating and Drinking Places 94 29 Petroleum Refining and Related Industries 19 59 Miscellaneous Retail 51 30 Rubber and Miscellaneous Plastics Products 35 72 Personal Services 22 31 Leather and Leather Products 41 73 Business ServiceS 358 32 Flat Glass 31 75 Auto Repair, Services, Parking 5 33 Primary Metal Industries 111 78 Motion Pictures 14 34 Fabricated Metal Products, except Machinery 91 79 Amusement and Recreation Services 5 and Transport Equip. 35 Industrial and Commercial Machinery and 284 80 Health Services 61 Computer Equipment 36 Electronic and Other Electrical Components, 511 82 Educational Services 53 except Computer Equip. 37 Transportation Equipment 103 87 Engr, Acc, Resh, Mgmt, Rel Services 38 Meas Instr, Photo Gds, Watches 366 99 Nonclassifiable Establishmnt 39 Misc Manufacturng Industries 63

29 Table 4 Reasons for Restatement

The reasons of restatement observations

Acquisition or Merger 4 Cost or expense 27 IPR&D (in-process research& 3 development) Reclassification 5 Restructuring, assets, or inventory 5 Revenue recognition 42 Securities related 2 Unspecified 1 Other 3 Multiple reasons (include at least above 14 two reasons) Total sample 106

0.02 0.015 0.01 0.005 0 Sstock - 7 4 1 8 5 2 1 4 7 0 3 6 9 return -0.005 -1 -1 -1 - - - 1 1 1 1 -0.01 -0.015 -0.02 -0.025 Date

Figure 1 Volatility of stock return around restatement

30 Table 5 Descriptive Statistics variable firms without repricing (N= 2869) firms with repricing (N=42) Difference Difference Mean test Median test mean median Std. Dev. mean median Std. Dev. in Mean in Median (p-value) (p-value) TRUNOV 0.1190 0.1250 0.1359 0.1513 0.1545 0.1538 -0.0323 -0.0295 0.0634 0.2840 RETURN 25.3809 13.1770 78.0536 0.1546 -14.9245 85.3569 25.2263 28.1015 0.0188 0.0020 EQUITY 6.4550 3.7676 15.2814 11.3704 5.1342 16.0036 -4.9154 -1.3666 0.0192 0.1200 SENSIT 5.6411 2.4928 10.9289 11.3430 3.9782 27.1016 -5.7018 -1.4854 0.0006 0.7750 HITECH 0.4851 0 0.4999 0.6667 1 0.4771 -0.1816 -1.0000 0.0096 0.0190 GROW 3.3816 2.2990 5.563 2.2740 1.4325 3.3282 1.1075 0.8665 0.099 0.0130 TA 5.9233 6.0479 0.7271 5.7613 5.9440 0.9190 0.1620 0.1039 0.0764 0.2150 ROE 1.2054 10.183 55.415 -2.1175 3.3740 84.0129 3.3229 6.8090 0.3507 0.0300 NPM -1.676 4.5270 44.505 -13.0791 1.7225 56.176 11.4031 2.8045 0.0501 0.0630

1. Variable definitions: TURNOV: management turnover at year end; RST: dummy variable for restatement, we set to 1 if restatement, otherwise 0; RETURN: stock return; EQUITY: equity compensation incentive; SENSIT: sensitivity of stock option values; HITECH: dummy variable for high-tech firm, we set to 1 if high-tech firm, otherwise 0; GROW: firm growth; TA: log of total assets at the end of the year; ROE: return on equity; NPM: profit margin. 2. The significant level is 10%.

31 Table 6 Pearson correlation analysis

Variable TRUNOV REPRIC RST RETURN EQUITY SENSIT HITECH GROW TA ROE NPM

TRUNOV 1 REPRIC 0.0262 1 (0.1207) RST 0.0407 0.0284 (0.016) (0.0934) RETURN -0.0528 -0.061 -0.0499 1 (0.0018) (0.0003) (0.0031) EQUITY 0.0537 0.0337 0.0168 0.0484 1 (0.0015) (0.0463) (0.3193) (0.0042) SENSIT 0.0656 0.0179 0.0265 0.0011 0.5304 1 (0.0001) (0.2905) (0.1172) (0.947) (0) HITECH 0.0633 0.0395 0.0181 -0.0424 0.1846 0.2489 1 (0.0002) (0.0193) (0.2848) (0.0122) (0) (0) GROW -0.0624 -0.0574 -0.0482 0.4216 0.2808 0.345 0.201 1 (0.0002) (0.0007) (0.0044) (0) (0) (0) (0) TA -0.0051 -0.0173 0.0127 -0.0074 -0.3804 0.1426 -0.1825 -0.0447 (0.7613) (0.3075) (0.4531) (0.6604) (0) (0) (0) (0.0081) ROE -0.1325 -0.0481 -0.0692 0.1849 0.0075 0.0704 -0.1411 0.4626 0.0949 1 (0) (0.0044) (0) (0) (0.6582) (0) (0) (0) (0) NPM -0.1339 -0.0455 -0.0779 0.1574 -0.0548 0.1343 -0.002 0.4355 0.0267 0.8022 1 (0) (0.0071) (0) (0) (0.0012) (0) (0.9062) (0) (0.1139) (0)

1. variable definitions: TURNOV: management turnover at year end; RST: dummy variable for restatement, we set to 1 if restatement, otherwise 0; RETURN: stock return; EQUITY: equity compensation incentive; SENSIT: sensitivity of stock options values; HITECH: dummy variable for high-tech firm, we set to 1 if high-tech industry, otherwise 0; GROW: firm growth; TA: log of total assets at the end of the year; ROE: return of equity; NPM: profit margin. 2. P value is in ( ).

32 Table 7 Effect of Restatement on Management Turnover

TURNOVi,t a0 a1RSTi,t a2 RETURNi,t a3EQUITYi,t a4SENSITi,t

a5HITECHi,t a6GROWi,t a7TAi,t a8ROEi,t a9 NPM i,t

YEAR i,t

RANDOM EFFECT FIXED EFFECT Variables z value P value t value P value coefficient coefficient RST 0.0298 2.120 0.017 0.0317 2.250 0.013 RETURN 0.0000 0.860 0.196 0.0000 1.320 0.094 SENSIT 0.0003 1.630 0.052 0.0003 1.570 0.058 EQUITY 0.0001 0.760 0.223 0.0001 0.580 0.282 HITECH 0.0200 3.790 0.000 0.0203 3.840 0.000 GROW -0.0021 -3.890 0.000 -0.0022 -4.140 0.000 TA -0.0062 -1.600 0.055 -0.0058 -1.500 0.067 ROE -0.0001 -2.230 0.013 -0.0001 -2.340 0.010 NPM -0.0001 -0.730 0.234 -0.0001 -0.970 0.167 CONSTANT 0.1564 6.550 0.000 0.1543 0.460 0.000 includ YEAR included ed Sample size =2911 Sample size = 2911 Wald 2 (12) value = 67.2 F(12,2886) = 7.99 P value = 0.000 P value = 0.000 R2 = 0.0241 R2 = 0.0242 Variable definitions: TURNOV: management turnover at year end; RST: dummy variable for restatement, we set to 1 if restatement, otherwise 0; RETURN: stock return; EQUITY: equity compensation incentive; SENSIT: sensitivity of stock option values; HITECH: dummy variable for high-tech industry, we set to 1 if high-tech industry, otherwise 0; GROW: firm growth; TA: log value of total assets at the year ending; ROE: return on equity; NPM: profit margin.

33 Table 8 Effects of Management Equity Incentives on Option Repricing

REPRICEi,t b0 b1RSTi,t b2TURNOVi,2average b3RSTi,t *TURNOVi,2average b RETURN b RST * RETURN b SENSIT b EQUITY 4 i,t 5 i,t i,t 6 i,t 7 i,t

b8HITECHi,t b9GROWi,t b10TAi,t b11ROEi,t b12 NPM i,t i,t

variable z value P value coefficient RST 3.5003 1.300 0.096 TURNOV -0.5000 -0.420 0.338 RST* TURNOV -0.0019 -0.910 0.181 RETURN -0.9937 -1.840 0.033 RST*RETURN -0.9884 -0.740 0.229 SENSIT 1.0153 2.270 0.012 EQUITY 1.0118 1.840 0.033 HITECH 2.1358 2.040 0.021 GROW -0.9719 -1.450 0.074 TA -0.8419 -0.790 0.216 ROE -1.0049 -1.680 0.047 NPM -0.9978 -1.020 0.306 Sample size = 2911 LR 2 value = 25.76 P value = 0.012 R2 = 0.0636

Variable definition: TURNOV2average: management turnovers at t-1 and t-2; RST: dummy variable for restatement, we set to 1 if restatement, otherwise 0; RETURN: stock return; RST* TURNOV2average: interaction of restatement and turnover; RST*RETURN: interaction of restatement and stock return; EQUITY: equity compensation incentive; SENSIT: sensitivity of stock options values; HITECH: dummy variable for high-tech firm, we set to 1 if high-tech industry, otherwise 0; GROW: firm growth; TA: log value of total assets at year ending; ROE: return of equity; NPM: profit margin.

34 Table 9 Effect of Option Repricing on Management Turnover

TURNOVi,t b0 b1RSTi,t b2 REPRICEi,t b3RSTi,t * REPRICEi,t

b4 RETURNi,t b5 RSTi,t * RETURNi,t b6SENSITi,t b7 EQUITYi,t

b8HITECHi,t b9GROWi,t b10TAi,t b11ROEi,t b12 NPM i,t

YEAR i,t

RANDOM EFFECT FIXED EFFECT Variables z value P value t value P value coefficient coefficient RST 0.0250 1.720 0.043 0.0270 1.850 0.032 REPRICE 0.0118 0.500 0.309 0.0133 0.570 0.286 RST*REPRICE 0.0382 0.460 0.324 0.0225 0.270 0.394 RETURN -0.0003 -4.600 0.000 -0.0004 -4.840 0.000 RST*RETURN 0.0000 0.060 0.478 0.0000 0.130 0.450 SENSIT 0.0003 1.430 0.077 0.0003 1.300 0.096 EQUITY 0.0003 1.480 0.070 0.0003 1.490 0.069 HITECH 0.0177 3.350 0.001 0.0178 3.380 0.001 GROW -0.0013 -2.350 0.010 -0.0013 -2.480 0.007 TA -0.0069 -1.800 0.036 -0.0066 -1.730 0.042 ROE -0.0009 -1.750 0.040 -0.0001 -1.810 0.035 NPM -0.0000 -0.020 0.493 -0.0000 -0.240 0.405

CONSTANT 0.1621 6.820 0.000 0.1608 6.770 0.000 includ include YEAR ed d Sample size =2904 Sample size = 2904 Wald 2 (12) value = 88.37 F(12,2886) = 7.88 P value = 0.00 P value = 0.000 R2 = 0.032 R2 = 0.032 Variable definitions: REPRICE: 1 if repricing of stock options, otherwise 0; TURNOV: management turnover at year end; RST: dummy variable for restatement, we set to 1 if restatement, otherwise 0; RETURN: stock return; EQUITY: equity compensation incentive; SENSIT: sensitivity of stock option values; HITECH: dummy variable for high-tech firm, we set to 1 if high-tech firm, otherwise 0; GROW: firm growth; TA: log value of total assets at the year ending; ROE: return of equity; NPM: profit margin.

35