Chapter 30: Mergers and Acquisitions Answers to suggested problems

30.4 a. False. Although the reasoning seems correct, the Stillman-Eckbo data do not support the monopoly power theory. b. True. When managers act in their own interest, acquisitions are an important control device for shareholders. It appears that some acquisitions and takeovers are the consequence of underlying conflicts between managers and shareholders. c. False. Even if markets are efficient, the presence of synergy will make the value of the combined firm different from the sum of the values of the separate firms. Incremental cash flows provide the positive NPV of the transaction. d. False. In an efficient market, traders will value takeovers based on “Fundamental factors” regardless of the time horizon. Recall that the evidence as a whole suggests efficiency in the markets. Mergers should be no different. e. False. The tax effect of an acquisition depends on whether the merger is taxable or non-taxable. In a taxable merger, there are two opposing factors to consider, the capital gains effect and the write-up effect. The net effect is the sum of these two effects. f. True. Because of the coinsurance effect, wealth might be transferred from the stockholders to the bondholders. Acquisition analysis usually disregards this effect and considers only the total value.

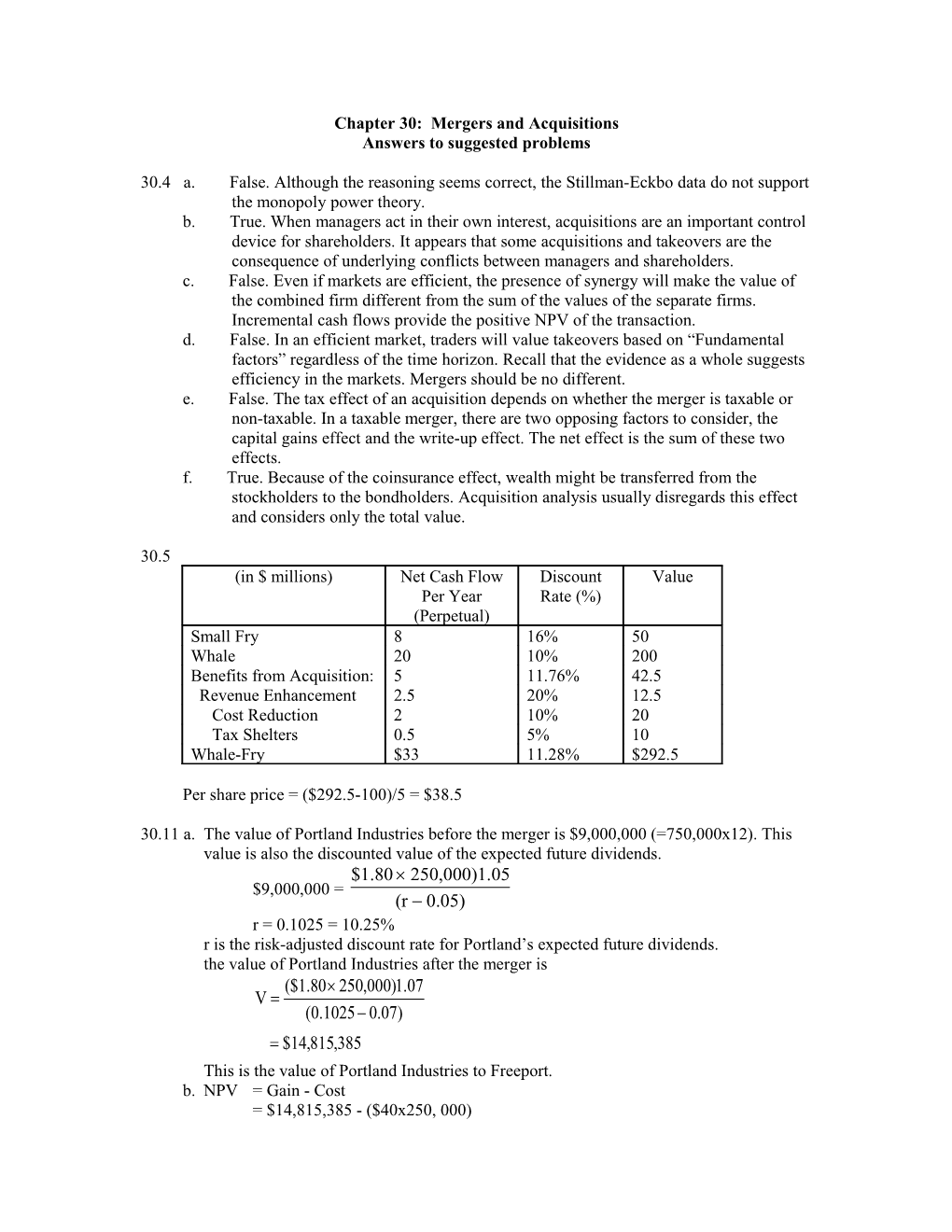

30.5 (in $ millions) Net Cash Flow Discount Value Per Year Rate (%) (Perpetual) Small Fry 8 16% 50 Whale 20 10% 200 Benefits from Acquisition: 5 11.76% 42.5 Revenue Enhancement 2.5 20% 12.5 Cost Reduction 2 10% 20 Tax Shelters 0.5 5% 10 Whale-Fry $33 11.28% $292.5

Per share price = ($292.5-100)/5 = $38.5

30.11 a. The value of Portland Industries before the merger is $9,000,000 (=750,000x12). This value is also the discounted value of the expected future dividends. $1.80 250,000)1.05 $9,000,000 = (r 0.05) r = 0.1025 = 10.25% r is the risk-adjusted discount rate for Portland’s expected future dividends. the value of Portland Industries after the merger is ($1.80 250,000)1.07 V (0.1025 0.07) $14,815,385 This is the value of Portland Industries to Freeport. b. NPV = Gain - Cost = $14,815,385 - ($40x250, 000) = $4,815,385 c. If Freeport offers stock, the value of Portland Industries to Freeport is the same, but the cost differs. Cost = (Fraction of combined firm owned by Portland’s stockholders) x(Value of the combined firm) Value of the combined firm = (Value of Freeport before merger) + (Value of Portland to Freeport) = $15x1,000,000 + $14,815,385 = $29,815,385 600,000 Fraction of ownership 0.375 1,000,000 600,000 Cost = 0.375x$29,815,385 = $11,180,769 NPV= $14,815,385 - $11,180,769 =$3,634,616 d. The acquisition should be attempted with a cash offer since it provides a higher NPV. e. The value of Portland Industries after the merger is ($1.80 250,000)1.06 V $11,223,529 (0.1025 0.06) This is the value of Portland Industries to Freeport. NPV = Gain-Cost =$11,223,529 - ($40x250,000) =$1,223,529

If Freeport offers stock, the value of Portland Industries to Freeport is the same, but the cost differs. Cost = (Fraction of combined firm owned by Portland’s stockholders) x(Value of the combined firm) Value of the combined firm = (Value of Freeport before merger) + (Value of Portland to Freeport) = $15x1,000,000 + $11,223,529 = $26,223,529 600,000 Fraction of ownership 0.375 1,000,000 600,000 Cost = 0.375 * $26,223,529=$9,833,823 NPV = $11,223,529 - $9,833,823=$1,389,706 The acquisition should be attempted with a stock offer since it provides a higher NPV.

30.14 The commonly used defensive tactics by target-firm managers include: i. corporate charter amendments like super-majority amendment or staggering the election of board members. ii. repurchase standstill agreements. iii. exclusionary self-tenders. iv. going private and leveraged buyouts. v. other devices like golden parachutes, scorched earth strategy, poison pill, ..., etc.