Corporate Taxation System in Japan

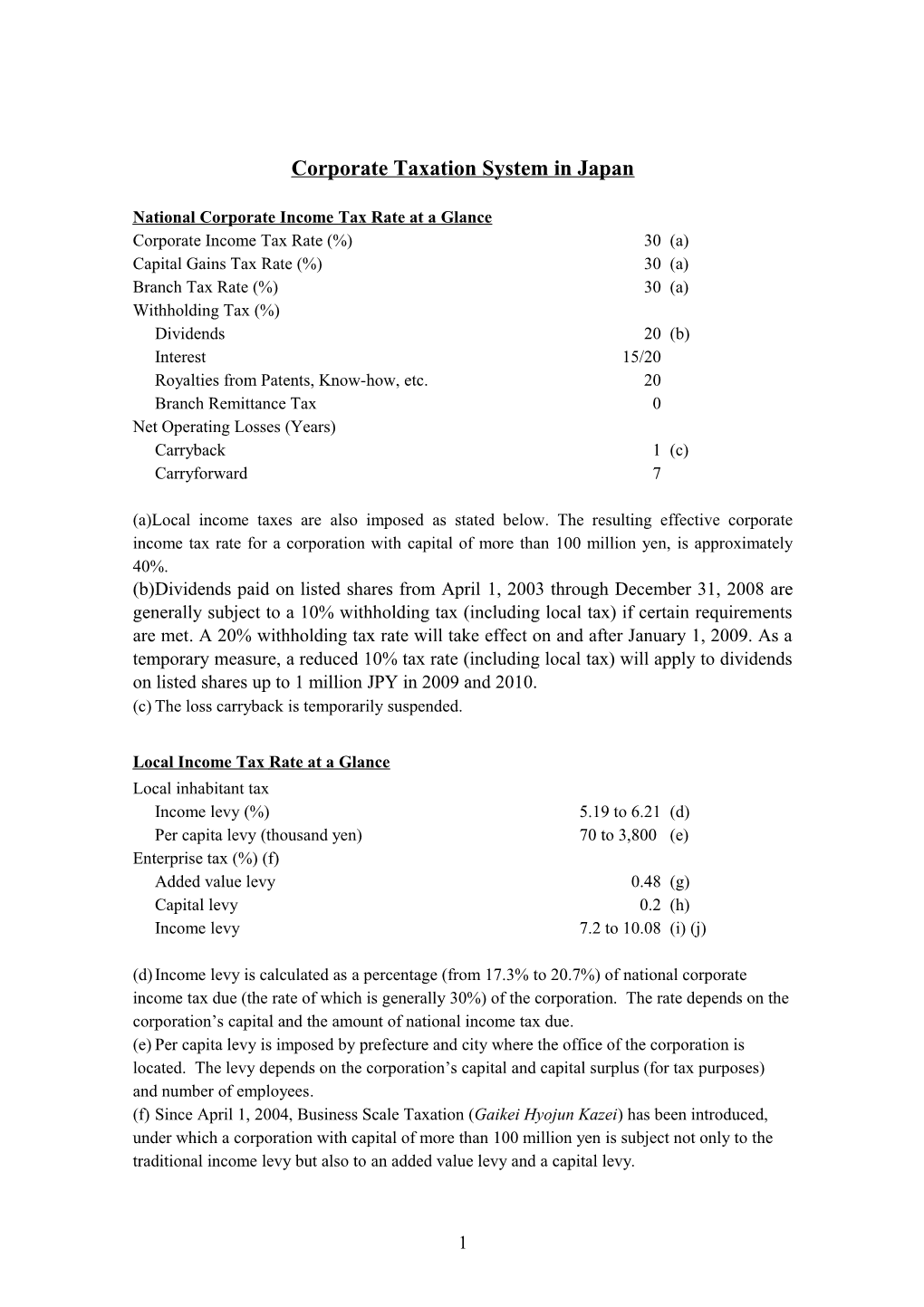

National Corporate Income Tax R ate at a G lance Corporate Income Tax Rate (%) 30 (a) Capital Gains Tax Rate (%) 30 (a) Branch Tax Rate (%) 30 (a) Withholding Tax (%) Dividends 20 (b) Interest 15/20 Royalties from Patents, Know-how, etc. 20 Branch Remittance Tax 0 Net Operating Losses (Years) Carryback 1 (c) Carryforward 7

(a)Local income taxes are also imposed as stated below. The resulting effective corporate income tax rate for a corporation with capital of more than 100 million yen, is approximately 40%. (b)Dividends paid on listed shares from April 1, 2003 through December 31, 2008 are generally subject to a 10% withholding tax (including local tax) if certain requirements are met. A 20% withholding tax rate will take effect on and after January 1, 2009. As a temporary measure, a reduced 10% tax rate (including local tax) will apply to dividends on listed shares up to 1 million JPY in 2009 and 2010. (c) The loss carryback is temporarily suspended.

Local Income Tax Rate at a Glance Local inhabitant tax Income levy (%) 5.19 to 6.21 (d) Per capita levy (thousand yen) 70 to 3,800 (e) Enterprise tax (%) (f) Added value levy 0.48 (g) Capital levy 0.2 (h) Income levy 7.2 to 10.08 (i) (j)

(d) Income levy is calculated as a percentage (from 17.3% to 20.7%) of national corporate income tax due (the rate of which is generally 30%) of the corporation. The rate depends on the corporation’s capital and the amount of national income tax due. (e) Per capita levy is imposed by prefecture and city where the office of the corporation is located. The levy depends on the corporation’s capital and capital surplus (for tax purposes) and number of employees. (f) Since April 1, 2004, Business Scale Taxation (Gaikei Hyojun Kazei) has been introduced, under which a corporation with capital of more than 100 million yen is subject not only to the traditional income levy but also to an added value levy and a capital levy.

1 (g) The tax base for the added value levy is salaries (remunerations), net interest payable, net rental fees payable and profit or loss of the taxable year. Some prefectures apply different rate up to 0.504%. (h) The tax basis for the capital levy is the total amount of capital and capital surplus (for tax purposes) of the corporation. Some prefectures apply different rate up to 0.21%. (i) Under Business Scale Taxation, the rate of income levy is 7.2% (up to 7.56% for some prefectures). Corporations exempt from Business Scale Taxation are taxed at 9.6% (up to 10.08% for some prefectures). (j)The current Enterprise tax rules will be amended and a new “Special local corporate tax”, which is a national tax, will be applied to financial years starting on or after October 1, 2008.

The rate of Enterprise Tax of Income Levy for a corporation which is subject to Business Scale Taxation will change from 7.2% to 2.9% and that for a corporation exempt from Business Scale Taxation will change from 9.6% to 5.3%.

Corporations subject to Business Scale Taxation will be subject to the “Special local corporate tax” at a tax rate of 148% on the Enterprise Tax of Income Levy. Corporations exempt from Business Scale Taxation will be subject to the “Special local corporate tax” at a tax rate of 81% on the Enterprise Tax of Income Levy. The government would redistribute these tax revenues back to the prefectures as a “Special local corporate transfer tax”. The introduction of these new taxes will not lead to an increase in the total tax burden of corporate taxpayers.

Outline of Japanese Corporate Tax S ystem Taxable Income Japanese domestic companies are subject to tax on their worldwide income, but nonresident companies pay taxes only on Japanese-source income.

Capital Gain Capital gains are not taxed separately. Such gains are treated as ordinary income to which normal tax rates apply. Transferor corporations in qualified reorganizations may defer the recognition of capital gains and losses arising in such transactions. Mergers, corporate spinoffs and contributions in kind are considered qualified reorganizations if they satisfy certain conditions.

Bonuses, Entertainment Expenses and Donations Bonuses to directors are considered a distribution of income and are generally not deductible by the corporation. The deductibility of entertainment expenses incurred by a corporation is restricted according to the size (capitalization) of the corporation. Deductions of donations, except for those to national or local governments or similar organizations, are limited.

Transfer Pricing Rules The transfer-pricing law stipulates that pricing between internationally affiliated entities

2 should be determined at arm’s length. Entities are considered to be internationally affiliated entities if there is a direct or indirect relationship by having either 50% or more ownership or substantial control.

Tax Haven Rules If a Japanese domestic company owns 5% or more of the issued shares of a tax-haven subsidiary of which more than 50% is owned directly or indirectly by Japanese domestic companies and Japanese resident individuals, the undistributed income of the subsidiary must be included in the Japanese parent company’s taxable income in proportion to the equity held. A foreign subsidiary is considered a tax-haven subsidiary if its head office is located in a country that does not impose income tax or if the company is subject to tax at an effective rate of 25% or less. If certain conditions are met, active business exemption can apply.

Thin Capitalization Thin-capitalization rules limit the deduction for interest expense for companies with foreign related-party debt if the debt-to-equity ratio exceeds 3:1.

Foreign Tax Credit A Japanese company may be entitled to claim a foreign tax credit against both Japanese national corporate tax and local inhabitant tax.

R&D Tax Credit A corporation may claim a credit of 8% to 10% of total research and development expenses or 20% of the national corporate tax due, whichever is smaller. If the 8% to 10% creditable expenses exceed the 20% tax due, the excess amount can be carryforward to the following year. In addition to the current R&D tax credits, a new R&D tax credit is available with respect to R&D expenses for financial years starting in the period from April 1, 2008 to March 31, 2010, if certain conditions are met. The upper limit for the new R&D tax credit is 10% of the corporate income tax due of the financial year.

The Consolidated Tax Return System (CTRS) CTRS applies to a domestic parent corporation and its 100% domestic subsidiaries. A consolidated group must elect the application of the CTRS, subject to the approval of the National Tax Agency (NTA). If a consolidated group wants to terminate its CTRS election, it must obtain the approval of the NTA.

Taxable Year The tax year for a corporation is its fiscal year. A corporation must file a tax return within two months of the end of its fiscal year, paying the tax at that time. In general, one month extension is allowed by filing an application.

3 Other Significant Tax Consumption Tax Consumption tax is imposed on most of the domestic Japanese transactions (including transfers of goods or services) and at importation of goods. In general, financial transactions, capital transactions and certain specific transactions are tax exempt. The tax rate is 5%. A corporation is generally allowed to credit consumption tax paid against its consumption tax liability. . Fixed Assets Tax Lands, buildings and depreciable fixed assets are subject to fixed assets tax imposed by municipal tax authorities. The tax base is fair market value of the assets and the general tax rate is 1.4%. For lands and buildings, the fair market value is determined by the municipal tax authorities, which are revaluated once in every three years. For depreciable fixed assets, generally, the tax is imposed based on a report filed by the taxpayer, which includes information on the acquisition cost and depreciation of the assets.

Treaty Withholding Tax Rates at a Glance For treaty countries, the rates reflect the lower of the treaty rate and the rate under domestic tax laws on outbound payments.

Dividends Interest Royalties % % % Australia (a) 15 10 10 Austria 10/20 10 10 Bangladesh 10/15 10 10 Belgium 10/15 10 10 Brazil 12.5 12.5 12.5/15/20 Bulgaria 10/15 10 10 Canada 5/10/15 10 10 China 10 10 10 Czechoslovakia 10/15 10 0/10 Denmark 10/15 10 10 Egypt 15 15/20 15 Finland 10/15 10 10 France 0/5/10 10 10 Germany 10/15 10 10 Hungary 10 10 0/10 India 15 10 20 Indonesia 10/15 10 10 Ireland 10/15 10 10 Israel 5/15 10 10 Italy 10/15 10 10 Korea 5/15 10 10

4 Luxembourg 5/15 10 10 Malaysia 5/15 10 10 Mexico 0/5/15 10/15 10 Netherlands 5/15 10 10 New Zealand 15 15/20 20 Norway 5/15 10 10 Pakistan (b) 15/20 0/15/20 0 Philippines (c) 10/20 10/15 15/20 Poland 10 10 0/10 Romania 10 10 10/15 Singapore 5/15 10 10 South Africa 5/15 10 10 Spain 10/15 10 10 Sri Lanka 20 15/20 0/10 Sweden 0/5/15 10 10 Switzerland 10/15 10 10 Thailand 15/20 10/20 15 Turkey 10/15 10/15 10 USSR 15 10 0/10 United Kingdom 0/5/10 10 0 United States 0/5/10 10 0 Vietnam 10 10 10 Zambia 0 10 10 Nontreaty countries 20 15/20 20

(a) Although Japan and Australia have singed a new tax treaty, it has not yet come into effect as of March, 2008. If the tax treaty comes into effect in 2008, the following withholding tax rates will be applied from January 1, 2009.

Dividends 0/5/10/15 Interest 10 Royalties 5

(b) Although Japan and Pakistan have signed a new tax treaty, it has not yet come into effect as of March, 2008. If the tax treaty comes into effect in 2008, the following withholding tax rates will be applied from January 1, 2009.

Dividends 5/7.5/10 Interest 10 Royalties 10

(c) Although Japan and the Philippines have signed a new tax treaty, it has not yet come into effect as of March, 2008. If the tax treaty comes into effect in 2008, the following withholding tax rates will be applied from January 1, 2009.

Dividends 10/15

5 Interest 10 Royalties 10

6