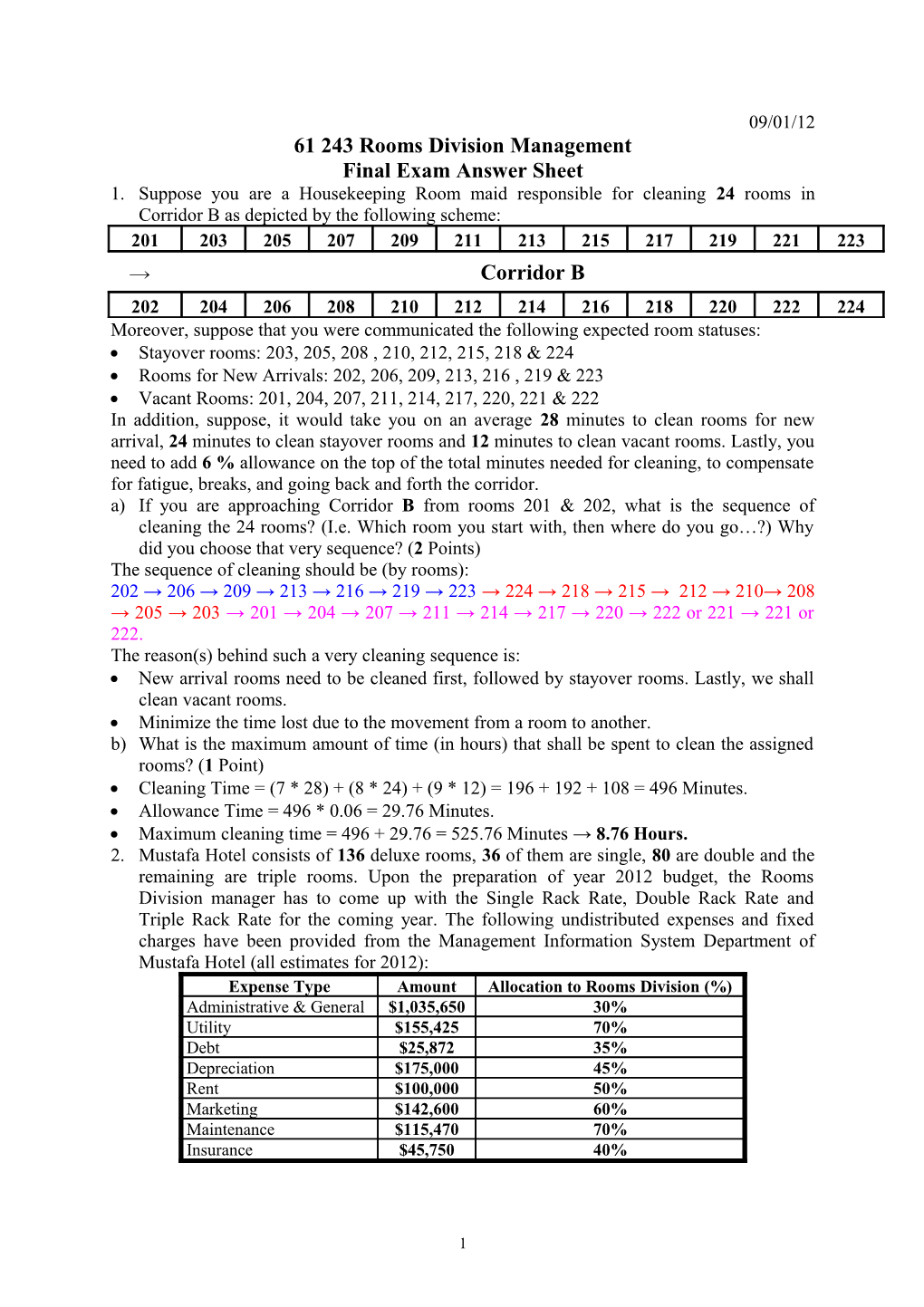

09/01/12 61 243 Rooms Division Management Final Exam Answer Sheet 1. Suppose you are a Housekeeping Room maid responsible for cleaning 24 rooms in Corridor B as depicted by the following scheme: 201 203 205 207 209 211 213 215 217 219 221 223 → Corridor B 202 204 206 208 210 212 214 216 218 220 222 224 Moreover, suppose that you were communicated the following expected room statuses: Stayover rooms: 203, 205, 208 , 210, 212, 215, 218 & 224 Rooms for New Arrivals: 202, 206, 209, 213, 216 , 219 & 223 Vacant Rooms: 201, 204, 207, 211, 214, 217, 220, 221 & 222 In addition, suppose, it would take you on an average 28 minutes to clean rooms for new arrival, 24 minutes to clean stayover rooms and 12 minutes to clean vacant rooms. Lastly, you need to add 6 % allowance on the top of the total minutes needed for cleaning, to compensate for fatigue, breaks, and going back and forth the corridor. a) If you are approaching Corridor B from rooms 201 & 202, what is the sequence of cleaning the 24 rooms? (I.e. Which room you start with, then where do you go…?) Why did you choose that very sequence? (2 Points) The sequence of cleaning should be (by rooms): 202 → 206 → 209 → 213 → 216 → 219 → 223 → 224 → 218 → 215 → 212 → 210→ 208 → 205 → 203 → 201 → 204 → 207 → 211 → 214 → 217 → 220 → 222 or 221 → 221 or 222. The reason(s) behind such a very cleaning sequence is: New arrival rooms need to be cleaned first, followed by stayover rooms. Lastly, we shall clean vacant rooms. Minimize the time lost due to the movement from a room to another. b) What is the maximum amount of time (in hours) that shall be spent to clean the assigned rooms? (1 Point) Cleaning Time = (7 * 28) + (8 * 24) + (9 * 12) = 196 + 192 + 108 = 496 Minutes. Allowance Time = 496 * 0.06 = 29.76 Minutes. Maximum cleaning time = 496 + 29.76 = 525.76 Minutes → 8.76 Hours. 2. Mustafa Hotel consists of 136 deluxe rooms, 36 of them are single, 80 are double and the remaining are triple rooms. Upon the preparation of year 2012 budget, the Rooms Division manager has to come up with the Single Rack Rate, Double Rack Rate and Triple Rack Rate for the coming year. The following undistributed expenses and fixed charges have been provided from the Management Information System Department of Mustafa Hotel (all estimates for 2012): Expense Type Amount Allocation to Rooms Division (%) Administrative & General $1,035,650 30% Utility $155,425 70% Debt $25,872 35% Depreciation $175,000 45% Rent $100,000 50% Marketing $142,600 60% Maintenance $115,470 70% Insurance $45,750 40%

1 Furthermore, assume that: The 2012 forecasted single occupancy: 60 % The 2012 forecasted double occupancy: 90 % The 2012 forecasted triple occupancy: 30 % The estimated single daily Direct Expense per occupied room: $ 65.00. The estimated double daily Direct Expense per occupied room: $ 80.00. The estimated triple daily Direct Expense per occupied room: $ 110.00. Lastly, Mustafa Hotel desires to have a room cost percentage of 70 % on Single Rooms, 55 % on Double Rooms and 35 % on Triple Rooms. Expense Type Amount Allocation to Rooms Division (%) Rooms Division Expense Administrative & General $1,035,650 30% $310,695 Utility $155,425 70% $108,798 Debt $25,872 35% $9,055 Depreciation $175,000 45% $78,750 Rent $100,000 50% $50,000 Marketing $142,600 60% $85,560 Maintenance $115,470 70% $80,829 Insurance $45,750 40% $18,300 Total $741,987 Total number of Single rooms expected to be sold (2012): 36 * 0.60 * 366 = 7,905.60 rooms. Total number of Double rooms expected to be sold (2012): 80 * 0.90 * 366 = 26,352 rooms. Total number of Triple rooms expected to be sold (2012): 20 * 0.30 * 366 = 2,196 rooms. Indirect Expenses per occupied room per day = 741,987 / (7,905.60 + 26,352 + 2,196) = 741,987 / 36,453.60 rooms = $ 20.35. a) What is Mustafa Hotel Single Hurdle Rate? (2 Points) Mustafa Hotel Single Hurdle Rate = 65 + 20.35 = $ 85.35. b) What is Mustafa Hotel Double Hurdle Rate? (2 Points) Mustafa Hotel Double Hurdle Rate = 80 + 20.35 = $ 100.35. c) What is Mustafa Hotel Triple Hurdle Rate? (2 Points) Mustafa Triple Hurdle Rate = 110 + 20.35 = $ 130.35. d) Could you interpret the results found in part a), b) and c)? (1 Point) The results found in parts a), b) and c) refer to the minimum prices with which front office clerks shall sell their rooms. Otherwise, Mustafa Hotel would be selling its rooms at a loss. e) What is Mustafa Hotel Single Rack Rate? (1 Point) Mustafa Hotel Single Rack Rate = 85.35 * (1 / 0.70) = $ 121.93. f) What is Mustafa Hotel Double Rack Rate? (1 Point) Mustafa Hotel Double Rack Rate = 100.35 * (1 / 0.55) = $ 182.45. g) What is Mustafa Hotel Triple Rack Rate? (1 Point) Mustafa Hotel Triple Rack Rate = 130.35 * (1 / 0.35) = $ 372.43. h) Suppose that Mustafa Hotel wants to boost Triple room sales by discounting the Triple Rack Rate by 35 %. Could you help management find the Triple Equivalent Occupancy Rate? (2 Points) Triple Equivalent Occupancy = 0.30 * (372.43 – 110) / ((372.43 * (1 - 0.35) – 110)) = 0.30 * (262.43 / 132.0795) = 0.30 * 1.9869 = 0.5960728 = 59.61 %.

i) Could you interpret the result you found in part h)? (1 Point)

2 A discount on the triple rack rate of 35 % shall lead to an increase of triple occupancy from 30 % to at least 59.61 % so that profitability before and after discounting remains the same. N.B.: All you results for the Second Question shall be rounded to two decimals!

3. Bebbe Resort Hotel has 185 rooms, 15 of them are suites, 20 are triple, 100 are double, and the remaining is single. Management decided to use the Hubbart Formula to estimate 2012 year’s Single, Double, Triple and Suite Rack Rates. Post to a preliminary work, management estimated the Average Room Rate to be $ 300 and the occupancy rate is 67.57 %. Moreover, management estimated the following: Single Occupancy: 55.00 % Double Occupancy: 90.00 % Triple Occupancy: 30.00 % Suite Occupancy: 10.00 % Lastly, management desires to have the following relation between single, double, triple and suite rack rates: Double Rack Rate shall be 1.50 times Single Rack Rate Triple Rack Rate shall be $ 50 more than Double Rack Rate Suite Rack Rate shall be 5 times Triple Rack Rate. a) What is the daily total number of rooms expected to be sold for the upcoming year? (1 Point) Daily Total Number of Rooms expected to be sold = 185 * 67.57 % = 125 rooms. b) What is the daily number of single, double, triple and suite rooms expected to be sold for the upcoming year? (3 Points) Daily Number of Single Rooms expected to be sold = 50 * 55 % = 27.50 Rooms. Daily Number of Double Rooms expected to be sold = 100 * 90 % = 90 Rooms. Daily Number of Triple Rooms expected to be sold = 20 * 30 % = 6 Rooms. Daily Number of Suite Rooms expected to be sold = 15 * 10 % = 1.50 Rooms. c) What is the single rack rate? (2 Points) Let χ denote Single rack rate; (27.50 * χ) + (90 * (1.50 * χ)) + (6 * ((1.50 * χ) + 50) + (1.50 * 5 * ((1.50 * χ) + 50) = 300 * 125 ↔ 182.75 * χ + 300 + 375 = 37,500 ↔ 182.75 * χ + 675 = 37,500 ↔182.75 * χ = 36,825 ↔ χ = $ 201.50. d) What shall be the double, triple and suite rack rates? (1 Point) Double Rack Rate = 201.50 * 1.50 = $ 302.26. Triple Rack Rate = 302.26 + 50 = $ 352.26. Suite Rack Rate = 352.26 * 5 = $ 1,761.29.

4. Amrabat Hotel's historical room nights for the past 12 years are depicted below:

Year Room Nights 2000 7,750 2001 8,060 2002 8,124 2003 8,342 2004 8,225 2005 8,102 2006 8,365 2007 8,500 2008 8,640

3 2009 8,750 2010 9,010 2011 9,300 Forecast Year 2012 room nights using: a) Percentage Growth Method? (1 Point) Total percentage growth in room nights = (9,300 – 7,750) / 7,750 * 100 = 20.00 % Yearly percentage change = 20 % / 12 = 1.67 % 2012 Forecasted room nights = 9,300 * (1 + 1.67 %) ≈ 9,455 room nights. b) Quadruple Moving Average Method? (You shall fill the below table!!) (3 Points) Year Room Nights Quadruple Moving Average AverageAAverage 2000 7,750 ------2001 8,060 ------2002 8,124 ------2003 8,342 8,069.00 2004 8,225 8,187.75 2005 8,102 8,198.25 2006 8,365 8,258.50 2007 8,500 8,298.00 2008 8,640 8,401.75 2009 8,750 8,563.75 2010 9,010 8,725.00 2011 9,300 8,925.00 Total Qaudruple Moving Average percentage growth in room nights = (8,925 – 8,069) / 8,069 * 100 = 10.61 % Period’s percentage change = 10.61 % / (12 – 3) = 1.18 % 2009 - 2010 – 2011 - 2012 Forecasted Triple Moving Average = 8,925 * (1 + 1.18 %) = 9,030.20 room nights 2012 Forecasted room nights = (9,030.201 * 4) – (8,750 + 9,010 + 9,300) ≈ 9,061 room nights. c) Weighted Average Method (Simplest Method)? (1 Point) Year Room Nights Weight Total 2000 7,750 1 7,750 2001 8,060 2 16,120 2002 8,124 3 24,372 2003 8,342 4 33,368 2004 8,225 5 41,125 2005 8,102 6 48,612 2006 8,365 7 58,555 2007 8,500 8 68,000 2008 8,640 9 77,760 2009 8,750 10 87,500 2010 9,010 11 99,110 2011 9,300 12 111,600

4 Total 78 673,872 2012 Forecasted room nights = 673,872 / 78 ≈ 8,639 room nights. d) Suppose, post to running regression analysis, the following regression equation has been found: Demand (in Room Nights) = 113.85 * Year – 219,887.79 Could you forecast 2012 demand using the above regression analysis? (1 Point) 2012 Forecasted room nights = (113.85 * 2012) – 219,887.79 ≈ 9,178 room nights. N.B.: All your answers to parts a), b), c) & d) shall be rounded to the nearest whole number! 5. Braga Club has 258 rooms: 22 are triple, 145 are double and the remaining is single. On the night of January 8th, 12 the night auditor counted 225 rooms occupied, 12 are triple, 132 are double, and the remaining is single. Moreover, the night auditor reported, on the same night, 315 guests registered in the hotel, 234 of them occupy either a double or triple room. Moreover, Braga Club’s night auditor counted 105 rooms occupied by more than 1 guest. In addition, the housekeeping department communicated 6 rooms (3 Single, 2 Double and 1 triple) out of order for the night of January 8th, 12. Lastly, the night auditor reported 5 complimentary rooms and calculated that very night’s room revenue to be $ 85,125. a) What is Braga Club's Occupancy Rate for the night of January 8th, 12? (1 Point) Braga Club’s Occupancy Rate = 225 / (258 – 6) * 100 = 89.29 %. b) What is Braga Club’s Single, Double, and Triple Occupancy rates for the night of January 8th, 12? (3 Points) Braga Club’s Single Occupancy Rate = 81 / (91 – 3) * 100 = 92.05 %. Braga Club’s Double Occupancy Rate = 132 / (145 – 2) * 100 = 92.31 %. Braga Club’s Triple Occupancy Rate = 12 / (22 – 1) * 100 = 57.14 %. c) What is Braga Club’s Multiple Occupancy for the night of January 8th, 12? (1 Point) Braga Club’s Multiple Occupancy = (105 / 225) * 100 = 46.67 %. d) What is Braga Club’s Average Guest per Room Sold? (2 Points) Braga Club’s Average Guest per Room Sold = 315 / (225 – 5) = 1.43 Guest per Room Sold. e) What is Braga Club’s Average Daily Rate? (2 Points) Braga Club’s Average Daily Rate = 85,125 / (225 – 5) = $ 386.93. f) What is Braga Club’s Average Rate per Guest? (2 Points) Braga Club’s Average Rate pr Guest = 85,125 / 315 = $ 270.24 per Guest. N.B.: All your answers to parts a), b), c), d), e) & f) shall be rounded to the nearest cent! 6. Santos Hotel’s Historical Operating Expenses & allocated Fixed Costs to the Rooms Division Department are depicted in the following table: Expense Items 2009 % Rev. 2010 % Rev. 2011 % Rev. Wage / Benefits $725,000 8.68% $745,000 7.93% $785,000 7.93% Laundry / Linen $65,750 0.79% $67,810 0.72% $71,062 0.72% Materials $314,950 3.77% $320,016 3.40% $325,980 3.29% Frills $47,900 0.57% $49,300 0.52% $50,000 0.51% Total Oper. Cost $1,153,600 13.82% $1,182,126 12.58% $1,232,042 12.44% Allcted. Fix. Cost $3,500,000 41.92% $3,825,000 40.69% $3,910,000 39.49% Room Revenue $8,350,000 100% $9,400,000 100% $9,900,000 100.00% Using the Percentage Growth Method: a) Determine the 2012 standards for the operating expense items in the last column. (2 Points)

5 Wage / Benefits: Total percentage growth = (7.93 % – 8.68 %) / 8.68 % * 100 = - 8.64 % Yearly percentage change = - 8.64 % / 3 = - 2.88 % 2012 Wage / Benefits % = 7.93 % * (1 – 2.88 %) ≈ 7.70 %. Laundry / Linen: Total percentage growth = (0.72 % – 0.79 %) / 0.79 % * 100 = - 8.86 % Yearly percentage change = - 8.86 % / 3 = - 2.95 % 2012 Laundry / Linen % = 0.72 % * (1 – 2.95 %) ≈ 0.70 % Materials: Total percentage growth = (3.29 % – 3.77 %) / 3.77 % * 100 = - 12.73 % Yearly percentage change = - 12.73 % / 3 = - 4.24 % 2012 Materials % = 3.29 % * (1 – 4.24 %) ≈ 3.15 % Frills: Total percentage growth = (0.51 % – 0.57 %) / 0.57 % * 100 = - 10.53 % Yearly percentage change = - 10.53 % / 3 = - 3.51 % 2012 Frills % = 0.51 % * (1 – 3.51 %) ≈ 0.49 % b) Estimate the 2012 Room Revenue. (1 Point) Total percentage growth = (9,900,000 – 8,350,000) / 8,350,000 * 100 = 18.56 % Yearly percentage change = 18.56 % / 3 = 6.19 % 2012 Estimated Revenue = 9,900,000 * (1 + 6.19 %) ≈ $ 10,512,575. c) Estimate the 2012 Expense Items and the Total Operating Expenses (1 Point) 2012 Estimated Wage / Benefits = $ 809,637. 2012 Estimated Laundry / Linen = $ 73,455. 2012 Estimated Materials = $ 331,185. 2012 Estimated Frills = $ 51,733. 2012 Estimated Total Operating Expenses = $ 1,266,010. d) Determine the 2012 Allocation % to the Rooms Division Department (1 Point) Total percentage growth = (39.49 % – 41.92 %) / 41.92 % * 100 = - 5.80 % Yearly percentage change = - 5.80 % / 3 = - 1.93 % 2012 Estimated Allocation % to the Rooms Division Dep. = 39.49 % * (1 - 1.93 %) ≈ 38.73 %. N.B.: Only answers to parts a), b), c) & d) without showing how did you reach those very answers will not be graded. Moreover, all your answers to parts a), b), c) & d) shall be rounded to the nearest cent.

6