The Bavaria Bank MTN

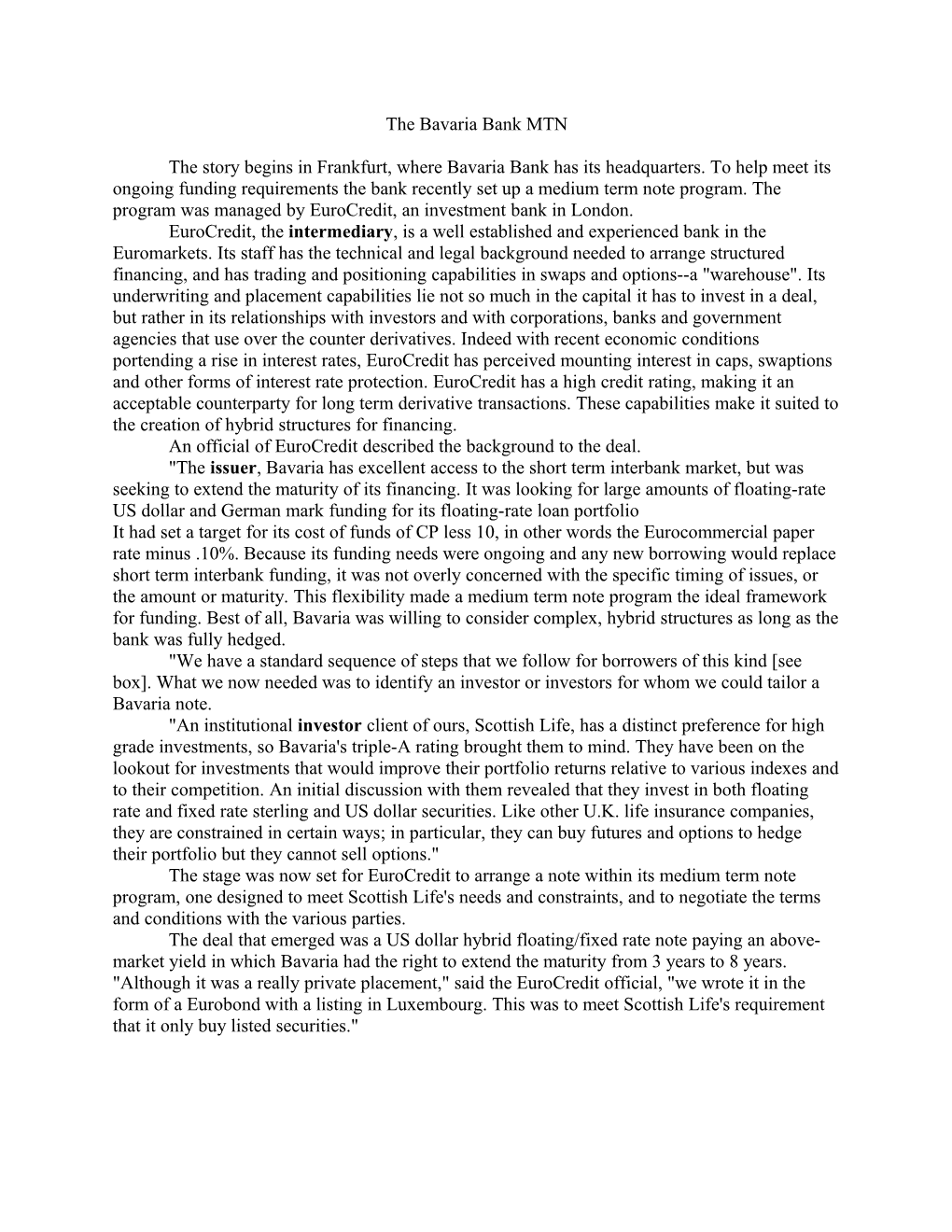

The story begins in Frankfurt, where Bavaria Bank has its headquarters. To help meet its ongoing funding requirements the bank recently set up a medium term note program. The program was managed by EuroCredit, an investment bank in London. EuroCredit, the intermediary, is a well established and experienced bank in the Euromarkets. Its staff has the technical and legal background needed to arrange structured financing, and has trading and positioning capabilities in swaps and options--a "warehouse". Its underwriting and placement capabilities lie not so much in the capital it has to invest in a deal, but rather in its relationships with investors and with corporations, banks and government agencies that use over the counter derivatives. Indeed with recent economic conditions portending a rise in interest rates, EuroCredit has perceived mounting interest in caps, swaptions and other forms of interest rate protection. EuroCredit has a high credit rating, making it an acceptable counterparty for long term derivative transactions. These capabilities make it suited to the creation of hybrid structures for financing. An official of EuroCredit described the background to the deal. "The issuer, Bavaria has excellent access to the short term interbank market, but was seeking to extend the maturity of its financing. It was looking for large amounts of floating-rate US dollar and German mark funding for its floating-rate loan portfolio It had set a target for its cost of funds of CP less 10, in other words the Eurocommercial paper rate minus .10%. Because its funding needs were ongoing and any new borrowing would replace short term interbank funding, it was not overly concerned with the specific timing of issues, or the amount or maturity. This flexibility made a medium term note program the ideal framework for funding. Best of all, Bavaria was willing to consider complex, hybrid structures as long as the bank was fully hedged. "We have a standard sequence of steps that we follow for borrowers of this kind [see box]. What we now needed was to identify an investor or investors for whom we could tailor a Bavaria note. "An institutional investor client of ours, Scottish Life, has a distinct preference for high grade investments, so Bavaria's triple-A rating brought them to mind. They have been on the lookout for investments that would improve their portfolio returns relative to various indexes and to their competition. An initial discussion with them revealed that they invest in both floating rate and fixed rate sterling and US dollar securities. Like other U.K. life insurance companies, they are constrained in certain ways; in particular, they can buy futures and options to hedge their portfolio but they cannot sell options." The stage was now set for EuroCredit to arrange a note within its medium term note program, one designed to meet Scottish Life's needs and constraints, and to negotiate the terms and conditions with the various parties. The deal that emerged was a US dollar hybrid floating/fixed rate note paying an above- market yield in which Bavaria had the right to extend the maturity from 3 years to 8 years. "Although it was a really private placement," said the EuroCredit official, "we wrote it in the form of a Eurobond with a listing in Luxembourg. This was to meet Scottish Life's requirement that it only buy listed securities." The following "term sheet" summarizes the main features of the note.

ISSUER: Bavaria Bank AG AMOUNT: US$ 40 MILLION COUPON: First 3 years: semi-annual LIBOR + 3/8% p.a., paid semi-annually Last 5 years: 8.35% PRICE: 100 MATURITY: February 10, 2000 CALL: Issuer may redeem the notes in full at par on February 10, 1995 FEES: 30 bp ARRANGER: EuroCredit Limited

The crucial elements are the coupon and call clauses. First, to appeal to the investor, the issuer has agreed to pay an above-market rate on both the floating rate note and the fixed rate bond segments of the issue

FRN portion: .75% above normal cost Fixed portion: .50% above normal cost

But by having the right either to extend the issue or terminate it after three years, the issuer has in effect purchased the right to pay a fixed rate of 8.35% on a five-year bond to be issued in three years time. Through its investment bank, the issuer will sell this right for more than it cost him, and so lower his funding cost below normal levels. This is illustrated in the following diagram. Bavaria sells 3 year floating rate note paying LIBOR-_%

For an additional ¾% pa, Bavaria buys right to sell 5 year fixed rate BAVARIA 8.35% note to SL in 3 years SCOTTISH BANK LIFE

For 1% pa, Bavaria sells EuroCredit a swaption (the right to pay fixed 8.35% for 5 years in 3 years)

EuroCredit sells the swaption to a corporate client seeking to hedge its EUROCREDIT funding costs against a rate rise

One could argue that Scottish Life would have been better off selling the swaption directly to EuroCredit or even to EuroCredit's client. This is not realistic: the institutional investor is not permitted to write options directly, although as is typical it is permitted to buy callable bonds and other securities with options embedded. Moreover it may not have a sufficient credit rating to enable it to sell stand-alone long term derivatives at a competitive price.