Valustrat Qatar Real Estate Research Q1 2018-Final

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Name Cuisine Address Timings Phone Number Category

NAME CUISINE ADDRESS TIMINGS PHONE NUMBER CATEGORY AKBAR RESTAURANT (SWISS- 16th Floor, Swiss-Belhotel, JaBr Bin 5 PM to 12 Midnight (Mon, BELHOTEL) INDIAN,MUGHLAI Mohamed Street, Al Salata, Doha Tue, Wed, Thu, Sat, Sun)... 44774248 Medium ANJAPPAR CHETTINAD 11 a.m .till 11:30 p.m.(Mon- RESTAURANT INDIAN Building 16, Barwa Village, Doha Sun) 44872266 Medium Beside Al Mushri Company, Near ANJAPPAR CHETTINAD Jaidah Flyover, Al Khaleej Street, 11:30 a.m .till 11:30 p.m.(Mon- RESTAURANT INDIAN MusheireB, Doha Sun) 44279833 Medium 12 Noon to 11 PM (Mon- Food Court, Villaggio, Al WaaB, Doha & Wed),12 Noon to 11:30 PM 44517867/44529028 ASHA'S INDIAN AL Gharafa (Thu... 44529029 Medium Beside MoBile 1 Center, Old Airport 6 AM to 11:30 PM (Mon, Tue, ASIANA INDIAN Road, Al Hilal, Doha Wed, Thu, Sat, Sun), 12... 44626600 Medium Near Jaidah Flyover, Al Khaleej Street, 7 AM to 3 PM, 6 PM to 11 PM BHARATH VASANTA BHAVAN SOUTH INDIAN/NORTH INDIAN Fereej Bin Mahmoud, Doha (Mon-Sun) 44439955 Budget Opposite Nissan Service Center, Pearl RoundaBout, Al Wakrah Main Street, Al 11:30 AM to 11:30 PM (Mon, BIRYANI HUT INDIAN Wakrah, Doha Tue, Wed, Sat, Sun)... 44641401/33668172 Budget BOLLYWOOED LOUNGE & Mezzanine, Plaza Inn Doha, Al Meena Closed (Mon),12 Noon to 3 RESTAURANT (PLAZA INN) INDIAN Street, Al Souq, Doha PM, 7 PM to 11 PM (Tue-Sun) 44221111/44221116 Medium Ground Floor, Radisson Blu Hotel, BOMBAY BALTI (RADISSON BLU) INDIAN Salwa Road, Al Muntazah, Doha 6 PM to 11 PM (Mon-Sun) 44281555 High-End Opposite The Open Theatre, Katara Closed (Mon, Tue, Wed, Sun), BOMBAY CHAAT INDIAN STREET FOOD Cultural Village, Katara, Doha 4 PM to 11 PM (Thu-Sat) 44080808 Budget Beside Family Food Center, Old Airport BOMBAY CHOWPATTY-I INDIAN STREET FOOD Road, Old Airport Area, Doha 24 Hours (Mon-Sun) 44622100 Budget Near Al Meera, Aasim Bin Omar Street, 5 AM to 12:30 AM (Mon, Tue, BOMBAY CHOWPATTY-II INDIAN STREET FOOD Al Mansoura, Doha Wed, Thu, Sat, Sun), 7.. -

1 Population 2019 السكان

!_ اﻻحصاءات السكانية واﻻجتماعية FIRST SECTION POPULATION AND SOCIAL STATISTICS !+ الســكان CHAPTER I POPULATION السكان POPULATION يعتﺮ حجم السكان وتوزيعاته املختلفة وال يعكسها Population size and its distribution as reflected by age and sex structures and geographical الﺮكيب النوي والعمري والتوزيع الجغراي من أهم البيانات distribution, are essential data for the setting up of اﻻحصائية ال يعتمد علا ي التخطيط للتنمية .socio - economic development plans اﻻقتصادية واﻻجتماعية . يحتوى هذا الفصل عى بيانات تتعلق بحجم وتوزيع السكان This Chapter contains data related to size and distribution of population by age groups, sex as well حسب ا ل ن وع وفئات العمر بكل بلدية وكذلك الكثافة as population density per zone and municipality as السكانية لكل بلدية ومنطقة كما عكسا نتائج التعداد ,given by The Simplified Census of Population Housing & Establishments, April 2015. املبسط للسكان واملساكن واملنشآت، أبريل ٢٠١٥ The source of information presented in this chapter مصدر بيانات هذا الفصل التعداد املبسط للسكان is The Simplified Population, Housing & واملساكن واملنشآت، أبريل ٢٠١٥ مقارنة مع بيانات تعداد Establishments Census, April 2015 in comparison ٢٠١٠ with population census 2010 تقدير عدد السكان حسب النوع في منتصف اﻷعوام ١٩٨٦ - ٢٠١٩ POPULATION ESTIMATES BY GENDER AS OF Mid-Year (1986 - 2019) جدول رقم (٥) (TABLE (5 النوع Gender ذكور إناث المجموع Total Females Males السنوات Years ١٩٨٦* 247,852 121,227 369,079 *1986 ١٩٨٦ 250,328 123,067 373,395 1986 ١٩٨٧ 256,844 127,006 383,850 1987 ١٩٨٨ 263,958 131,251 395,209 1988 ١٩٨٩ 271,685 135,886 407,571 1989 ١٩٩٠ 279,800 -

Sabah Al Ahmad Corridor Project Launched Sabah Al Ahmad Representative of H H the Amir Corridor Is the first of Kuwait, in a Grand Ceremony at the Sheraton Hotel

BUSINESSB | 01 SPORT | 07 Qatar needs to Rins sets get ready for pace on wave of digital second day of disruption Qatar Test Monday 25 February 2019 | 20 Jumada II 1440 www.thepeninsula.qa Volume 23 | Number 7813 | 2 Riyals Sabah Al Ahmad Corridor project launched Sabah Al Ahmad Representative of H H the Amir Corridor is the first of Kuwait, in a grand ceremony at the Sheraton Hotel. Amir and Representative of Kuwait Amir hold talks in Qatar to be called A number of Their Excel- the ‘Corridor’ instead lencies ministers, members of of a road due to its the Kuwaiti delegation, diplo- great importance and matic representatives, senior officials as well as representa- specifications of its tives from the project contractors unique construction. were also present at the The Corridor will be ceremony. The launching of Sabah Al completed in 2021 Ahmad Corridor coincides with and will have a length the celebrations of Kuwait’s of 25km and a total National Day and also meant to works of 37km. recognise Kuwait’s support and strong bonds of solidarity and brotherhood between Qatar and THE PENINSULA Kuwait. DOHA The diplomatic relationship between the two countries is Upon the directives of Amir H H growing stronger under the Sheikh Tamim bin Hamad Al guidance of the countries’ two Thani, the name of the Amir of leaders Amir H H Sheikh Tamim Kuwait, H H Sheikh Sabah Al bin Hamad Al Thani, and H H Ahmad Al Jaber Al Sabah, was Sheikh Sabah Al Ahmad Al Jaber Amir H H Sheikh Tamim bin Hamad Al Thani and H H Sheikh Jassim bin Hamad Al Thani, the Personal Representative of H H the given to a corridor road project Al Sabah. -

CLASSIFIED CONTD. on FOLLOWING PAGES Commission

Gulf Times 1 Thursday, May 4, 2017 CLASSIFIED ADVERTISING SITUATION VACANT A leading Car Rental CCheerfulheerful aandnd EEnthusiasticnthusiastic BBritishritish EEducatedducated DDentistentist AAUTOUTO PPARTSARTS MMANAGERANAGER WANTEDWANTED Sales Engineer Company requires rrequiredequired toto jjoinoin greatgreat teamteam atat BritishBritish WWee aarere ssearchingearching fforor a qqualifiedualified AutomotiveAutomotive SpareSpare PartsParts • 5-7 years’ experience, preferably Graduate Civil / Mechanical or Architect. Light & Heavy vehicle • Should have vast experience in Sales & Marketing of Aluminum Composite Panels or IInternationalnternational DentalDental Centre.Centre. ThoseThose withwith MManager.anager. MMustust hhaveave eexperiencexperience inin thethe locallocal MarketMarket asas wellwell asas related building products such as Insulated Metal Wall panels, Sandwich panels, Drivers Architectural cladding etc. llicenseicense inin QatarQatar ppreferred.referred. SendSend CVCV toto tthehe ccorrespondingorresponding educationeducation inin thethe field.field. PleasePlease sendsend CV’sCV’s toto GULF With valid Qatar driving • Ability to interact and sell to the key influencers: architects, consultants & façade tthehe ffollowingollowing EEmail:mail: [email protected]@gmail.com engineers. TIMES license for transfer [email protected]@gmail.com • Operational experience in dealing with Aluminum Cladding Contractors & consultants. or six months NOC • Results driven personality is a must. Classified -

Experience Record Important Completed Projects

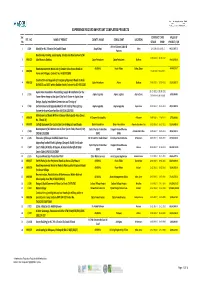

EXPERIENCE RECORD IMPORTANT COMPLETED PROJECTS Ser. CONTRACT DATE VALUE OF REF . NO . NAME OF PROJECT CLIENT'S NAME CONSULTANT LOCATION No STRART FINISH PROJECT / QR Artline & James Cubitt & 1 J/149 Masjid for H.E. Ghanim Bin Saad Al Saad Awqaf Dept. Dafna 12‐10‐2011/31‐10‐2012 68,527,487.70 Partners Road works, Parking, Landscaping, Shades and Development of Al‐ 22‐08‐2010 / 21‐06‐2012 2 MRJ/622 Jabel Area in Dukhan. Qatar Petroleum Qatar Petroleum Dukhan 14,428,932.00 Road Improvement Works out of Greater Doha Access Roads to ASHGHAL Road Affairs Doha, Qatar 48,045,328.17 3 MRJ/082 15‐06‐2010 / 13‐06‐2012 Farms and Villages, Contract No. IA 09/10 C89G Construction and Upgrade of Emergency/Approach Roads to Arab 4 MRJ/619 Qatar Petroleum Atkins Dukhan 27‐06‐2010 / 10‐07‐2012 23,583,833.70 D,FNGLCS and JDGS within Dukhan Fields,Contract No.GC‐09112200 Aspire Zone Foundation Dismantling, Supply & Installation for the 01‐01‐2011 / 30‐06‐2011 5 J / 151 Aspire Logistics Aspire Logistics Aspire Zone 6,550,000.00 Tower Flame Image at the Sport City Torch Tower in Aspire Zone Extension to be issued Design, Supply, Installation.Commission and Testing of 6 J / 155 Enchancement and Upgrade Work for the Field of Play Lighting Aspire Logestics Aspire Logestics Aspire Zone 01‐07‐2011 / 25‐11‐2011 28,832,000.00 System for Aspire Zone Facilities (AF/C/AL 1267/10) Maintenance of Roads Within Al Daayen Municipality Area (Zones 7 MRJ/078 Al Daayen Municipality Al Daayen 19‐08‐2009 / 11‐04‐2011 3,799,000.00 No. -

Access to Quality Education for Displaced Children Stressed

BUSINESS | 23 SPORT | 29 Nebras records Disgraced Smith, huge jump in 2017 Warner out for 12 revenue months Thursday 29 March 2018 | 12 Rajab I 1439 www.thepeninsula.qa Volume 23 | Number 7480 | 2 Riyals Freedom to roam with Bill Protection! Terms & conditions apply Access to quality education for Emir holds talks with Rosneft Chief Executive Officer displaced children stressed THE PENINSULA H H Sheikha Moza Grandi. The discussion touched bint Nasser, while on the ways to ensure education GENEVA: H H Sheikha Moza speaking during for refugees and internally dis- bint Nasser, Chairperson of placed persons, in order to build Qatar Foundation (QF) and a high-level panel a prosperous future for all. Education Above All Foundation discussion at the During the discussion, H H (EAA), has urged the global UN headquarters in Sheikha Moza spoke about the community to facilitate access Geneva, urged the obstacles facing the education of to quality education for refugee and displaced children, displaced children and to global community to which prevents them from con- enforce severe penalties for facilitate access to tributing to the building of their perpetrators of armed conflict. quality education for communities. Her Highness H H Sheikha Moza bint added that education must be Nasser, Advocate for the UN displaced children given priority as it is the tool for Sustainable Development and to enforce the children of the present and Goals, participated yesterday future. A global approach needs severe penalties for Emir H H Sheikh Tamim bin Hamad Al Thani met yesterday at Al Bahr Palace office with Igor Sechin, in a high-level panel discussion to be adapted, in order to remove perpetrators of Chief Executive Officer of Rosneft, and the delegation accompanying him on the occasion of his visit organised by the EAA in coop- institutional barriers which eration with the United Nations armed conflict. -

Valustrat Qatar Real Estate Research Q4 2019

www.valustrat.com Real Estate Market 4th Quarter | 2019 Review VPI ValuStrat Price Index Residential The fourth quarter 2019 ValuStrat Price Index (VPI)-Residential, displayed an overall 5.0% annual and 0.8% quarterly decline in capital values. Villa and freehold apartment prices saw marginal QoQ declines of 0.5% and 1.8% respectively. Amongst freehold apartments, The Pearl witnessed the highest overall decline in values followed by West Bay Lagoon and Lusail. A quarterly capital depreciation of less than 2% was observed in clusters of Ain Khaled, Abu Hamour, West Bay Lagoon, Umm Salal Ali and Al Khor. The remaining clusters experienced no change in capital values. Gross yields for residential units averaged at an overall 5.0% adjusted by 6.1% for apartments and 4.5% for villas. VPI - Qatar Residential Capital Values 13 Villa and 3 Apartment Locations [Base: Q1 2016=100] 120 100.0 100 96.3 94.2 90.9 89.8 87.2 84.9 82.7 81.3 77.7 75.8 75.0 80 73.4 72.8 71.8 71.2 60 40 20 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2016 2017 2018 2019 Source: ValuStrat 1 | Qatar Real Estate Market 4th Quarter 2019 Review Macro-Economic Snapshot • International Monetary Fund (IMF) projected Qatar Population real GDP of Qatar to grow by 2% in 2019 on the back of robust non-hydrocarbon sector growth and oil and gas production recovery 2,773,000 2019-Q4 2,674,000 • The state budget for 2020 was announced 2018 which forecasted a budget surplus of QAR 500 million and expenditure in major projects at 2,641,000 QAR 90 billion, amidst a continued conservative 2017 oil price estimate of $55 a barrel 2,597,000 2016 • Population is estimated at 2.77 million as of Q4 2019. -

Centre-Piece of the Mashaf Township

AL MASHAF DISTRICT 25°10’40.2”N 51°33’57.6”E MASHAFCROSSINGS.COM Mashaf township Centre-piece of the Centre-piece Embrace the new Mashaf lifestyle 001 Mashaf Crossings redefines the way you interact with the township and each other, bringing the best mix of retail, restaurants & entertainment. Where a young professional’s idea of style and sophistication crosses paths with the one’s seeking an uplifting experience. It’s a space where independent businesses nurture your passion, grocers keep you well-fed, and entertainment melts away the stress of daily work. MASHAF CROSSINGS 2 002 The space to grow and thrive. Mashaf Crossings’ newly designed 23,500sqm premier mixed- used community center will feature a modern lounge with extensive indoor-outdoor seating areas; seamlessly blending high caliber retail lifestyle amenities. Embrace the new Mashaf lifestyle 002 Site Plan 23,500 SQ METERS 215 C PARKING SPACES 62 LEASABLE UNITS D 2 FLOORS E A B A Building A C Building C E Building E • 5 Tenant slots • 17 Tenant slots • 4 Tenant slots • Slot sizes >220 sqm • Slot sizes 38 - 220 sqm • Slot sizes 76-160 sqm B Building B D Building D • 29 Tenant slots • 8 Tenant slots • Slot sizes 38 - 220 sqm • Slot sizes 76 - 160 sqm 003 A new way to dine, shop and play MASHAF CROSSINGS 7 8 MASHAF CROSSINGS 003 EXPERIENCE — DINE A CULINARY WALK IN A WORLD OF CUISINES Imagine a rich world of cuisine along the gastronomy corridors of Mashaf Crossings. Explore and discover a modern and constantly evolving selection of Qatar’s most tempting food and beverages establishments. -

Quality of Service Measurements- Mobile Services Network Audit 2012

Quality of Service Measurements- Mobile Services Network Audit 2012 Quality of Service REPORT Mobile Network Audit – Quality of Service – ictQATAR - 2012 The purpose of the study is to evaluate and benchmark Quality Levels offered by Mobile Network Operators, Qtel and Vodafone, in the state of Qatar. The independent study was conducted with an objective End-user perspective by Directique and does not represent any views of ictQATAR. This study is the property of ictQATAR. Any effort to use this Study for any purpose is permitted only upon ictQATAR’s written consent. 2 Mobile Network Audit – Quality of Service – ictQATAR - 2012 TABLE OF CONTENTS 1 READER’S ADVICE ........................................................................................ 4 2 METHODOLOGY ........................................................................................... 5 2.1 TEAM AND EQUIPMENT ........................................................................................ 5 2.2 VOICE SERVICE QUALITY TESTING ...................................................................... 6 2.3 SMS, MMS AND BBM MEASUREMENTS ............................................................ 14 2.4 DATA SERVICE TESTING ................................................................................... 16 2.5 KEY PERFORMANCE INDICATORS ...................................................................... 23 3 INDUSTRY RESULTS AND INTERNATIONAL BENCHMARK ........................... 25 3.1 INTRODUCTION ................................................................................................ -

Qatar Real Estate Market Report

QATAR REAL ESTATE MARKET REPORT CONTENTS IN THIS ISSUE ISSUE 1 - MAY 2018 12 Property Trends TRENDS 16 Long Term Price Trends 1 18 Performance Review 30 The Case for Market Transparency 31 Qatar’s Commission Conundrum CONTRIBUTORS 32 Benefits of Property Management Services 2 33 Is Your Property Always Rent-Ready? CONSUMER 36 Top Searched Areas SEARCHES 38 Top Searched Keywords 3 EXPLAINED 39 User Behaviour 42 What Sets Us Apart WE ARE 44 Our Performance 4 PROPERTYFINDER 45 Awesome Agent Winners CONTRIBUTORS Sam Youssef Jeffrey Asselstine Adrian Camps James Townsend Managing Director, Managing Director, Country Director, Managing Director, Better Homes Qatar NelsonPark Property LCC Colliers Absolute Qatar BACKGROUND Sam established BACKGROUND Jeffrey founded BACKGROUND Adrian has BACKGROUND With a decade Better Homes Qatar in 2009 and NelsonPark Property nine years over 35 years’ experience, with of experience in the real estate has over 15 years of experience ago and has continued to lead 11 years spent in the GCC of market in Qatar and the GCC, in the real estate market. He has as its Managing Director. Armed which the last six years were James has know-how in both been instrumental in leading with a BBA from Wilfrid Laurier Qatar based. Heading the the residential and commercial Better Homes Qatar through University, and as a Chartered Colliers Qatar country team, fields. For seven years, he was remarkable growth and has Financial Analyst (CFA), he has he provides key property running his own agency, prior spearheaded the introduction of spearheaded the development advice to corporations and to launching Absolute Qatar. -

Qatar Industrial Landscape 2.0: Resilient and Stronger Contents

Qatar Industrial Landscape 2.0: Resilient and Stronger Contents Foreword 2 Qatar Industrial Landscape 1.0 3 Blockade: A Blessing in Disguise 7 Outlook: Qatar Industrial Landscape 2.0 12 Qatar 2.0- Resilient and Stronger | 1 Foreword Venkat Krishnaswamy Partner, Head of Advisory at KPMG Qatar The discovery of oil in the 1940’s started Qatar’s“ industrial growth and economic development. At the turn of the 21st century, Qatar witnessed exponential growth and diversification supported by development of industrial and port infrastructure and increased focus on exports. Government’s swift responses to the regional blockade underpinned Qatar’s economic resilience which ensured stability in industrial sector exports, both in the oil and gas and non-oil, non-gas segments. A blessing in disguise, the blockade led to rapid development in Qatar’s agro- and food-based industries driven by initiatives by the government and the private sector. After mitigating the immediate impact of the blockade, the government developed the manufacturing sector strategy, comprising nine strategic enablers which are expected to help Qatar build on its resilience and emerge stronger. The ending of blockade and a multi-sector development pipeline augurs well for Qatar’s industrial sector. ” Qatar 2.0- Resilient and Stronger | 2 Qatar Industrial Landscape 1.0 The discovery of oil in the 1940’s jump started Qatar’s industrial growth and economic development In the early 20th century, Qatar’s economy was heavily reliant on fishing and pearl diving. It transformed significantly with the discovery of oil in 1940. This drove industrial development, with the opening of Mesaieed Industrial City and Mesaieed Port in 1949. -

Pre-Qualification Document

1 Prequalification Gulf Laboratories Co. W.L.L Geotechnical Services, Materials, Petroleum, Environmental and Food Testing Laboratory Gulf Laboratories Co. W.L.L Street No. 13 Gate 112 Salwa Industrial Area, Doha, P.O Box 4024 Phone: +974 44607034 +974 44607036 Fax: +974 44607628 E-mail address: [email protected] Website: www.gulflaboratories.com Prequalification Document Rev 53 17.12.2018 2 Contents Page No. Company Details………………………………………………………………………..……………………………………… 3 Key Personnel………………………………………………………………………………………………..…………………. 4 Equipment and Resources………………………………………….………………………………………………………. 6 Services Offered…………………………………………………………………………………………....…………………. 10 Organizational Structure……………………………………………………………………………..….………………….. 12 Appendices Appendix A - Certificates of Registration, MoE Certificate of Conformity, Municipality License and Qatar Chamber of Commerce and Industry Certificate…… 14 Appendix B - ISO 17025 Accreditation / OHSAS, QMS, EMS Certification………………………………… 31 Appendix C - Resume of Company Experience…………………………………………………………………….. 37 Appendix D - Field and Laboratory Testing ISO 17025 Accredited Test Parameters…………………. 72 Prequalification Document Rev 53 17.12.2018 3 Company Details Name of Company : Gulf Laboratories Co. W.L.L Head Office Address : P.O. Box 4024, Doha, Qatar Commercial Registration No. : 14419 Nature of Business : Ground Investigations and Materials / Environmental Testing Established : Mid-1970’s Owners : Mannai Corporation QPSC, Doha Employees : 400 + Main Office/ Physical Laboratory Location : Street No. 13 Gate 112 Salwa Industrial Area Telephone Nos. : +974 446 07034 / +974 446 07036 Fax No. : +974 446 07628 E-mail Address : [email protected] Geotechnical and Drilling Site Street No. 24, Gate 21, Al Kassarath Street Investigation Department : Salwa Industrial Area Telephone Nos. : +974 446 06585 / +974 445 02371 Fax No. : +974 446 06562 E-mail Address : [email protected] Workshop Location : Street 46, Salwa Industrial Area Chemical, Environmental, Oil Junction of Street No.