18th European Symposium on Computer Aided Process Engineering – ESCAPE 18 Bertrand Braunschweig and Xavier Joulia (Editors) © 2008 Elsevier B.V./Ltd. All rights reserved.

Addressing Robustness for Crude Oil Scheduling under Uncertainty Jie Li,a I. A. Karimi,a Rajagopalan Srinivasana,b aDepartment of Chemical and Biomolecular Engineering, National University of Singpaore, 4 Engineering Drive 4, Singapore 117576, Singapore bProcess Sciences and Modeling, Institute of Chemical and Engineering Sciences, 1 Pesek Road,Jurong Island, Singapore 627833, Singapore

Abstract Scheduling of crude oil operation is an important section of refinery operations because crude oil costs account for about 80% of a refinery’s turnover. Due to the crude blending, the entire problem is modeled as a nonconvex mixed-integer nonlinear programming (MINLP) problem. However, some common and frequent uncertainties including ship arrival delays, and demand fluctuations are unavoidable in refinery operations. In this paper, we use a penalty function approach to address two important uncertainties in crude oil operations, namely those related to product demands and ship arrivals. We first define schedule robustness, and propose an evaluation procedure and an index for robustness. Then, we develop scenario-based models for addressing demand and ship arrival uncertainties separately. For demand uncertainty, we show that the schedule thus obtained is more robust and more feasible than the “average-demand” schedule over the entire expected range of uncertainty. For ship arrival uncertainty, we propose a heuristic decomposition strategy to obtain a robust schedule. The resulting schedules are superior to the original schedules. Finally, we also solve those two uncertainties simultaneously with heuristic decomposition strategy. The result shows that the resulting schedules also have high robustness than the original schedules.

Keywords: crude oil scheduling, robustness index, uncertainty, scenario-based approach, approximate decomposition strategy, mixed-integer nonlinear programming (MINLP)

1. Introduction Scheduling of crude oil operations is an important and complex routine task in a refinery. It involves crude oil unloading, tank allocation, storage and blending of crudes, and CDU charging. Optimal crude oil scheduling can increase profits by exploiting cheaper but poor quality crudes, minimizing crude changeovers, avoiding ship demurrage, and managing crude inventory optimally. In our previous work (Li et al., 2005 and 2007), we have developed robust algorithms for obtaining optimal schedules for operations without any uncertainty. However, in a practice, uncertainties are unavoidable. Some common and frequent uncertainties in refinery operations include ship arrival delays, demand fluctuations, equipment malfunction, etc. In the face of these uncertainties, an optimal schedule obtained using nominal parameter values may often be suboptimal or even become infeasible. Thus, it is critical to develop algorithms that can consider future uncertainty at the scheduling stage to improve schedule feasibility and robustness. 2 Jie Li et al.

So far, several efforts have been made to address the problem of refinery planning and scheduling under uncertainty. Arief et al. (2004 and 2007a,b) proposed heuristic-based and model-based approaches to reschedule operations of a given schedule to accommodate disruptions. Neiro and Pinto (2005) proposed a production-planning model incorporating product price and demand uncertainties in a refinery. Li et al. (2004, 2005, and 2006) addressed the problem of refinery planning under demand or other economic parameters uncertainties with two-stage stochastic programming approach. Therefore, no work has so far addressed the development of robust schedules for crude oil scheduling in the face of uncertainties. In this paper, we use a penalty function approach to obtain robust schedules for two important uncertainties in crude operations, namely product demands fluctuation and ship arrivals delay.

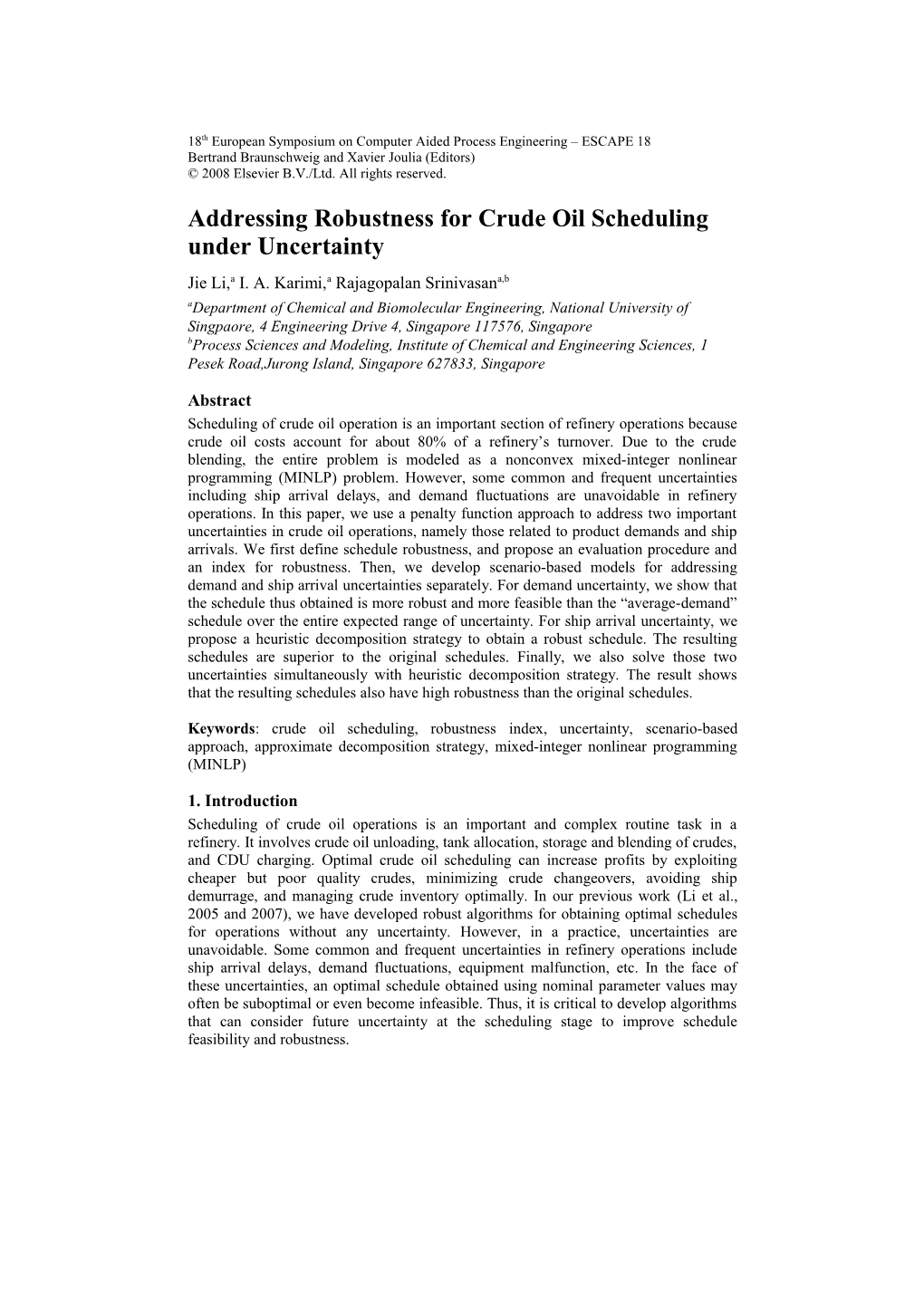

2. Problem statement Figure 1 shows a schematic of crude oil operations in a typical marine-access refinery. It comprises offshore facilities for crude unloading such as a single buoy mooring (SBM) or single point mooring (SPM) station, onshore facilities for crude unloading such as one or more jetties, tank farm consisting of crudes storage and/or charging tanks, and processing units such as crude distillation units (CDUs). The unloading facilities supply crudes to crude storage tanks via pipelines. The pipeline connecting the SBM/SPM station with crude tanks is called the SBM/SPM line, and it normally has a substantial holdup.

Figure 1 Schematic of oil unloading and processing Two types of ships supply crudes to the refinery. Very large crude carriers (VLCCs) or ultra large crude carriers (ULCCs) carry multiple parcels of several crudes and dock at the SBM/SPM station offshore. Small vessels carry single crudes and berth at the jetties. The entire crude oil operation involves unloading and blending crudes from ships into various storage tanks at various times, and charging CDUs from one or more storage tanks at various rates over time. Thus, crude oil operations in a typical refinery involves both scheduling and allocation decisions. The objective of the scheduling problem is to maximize the gross profit, which is the revenue computed in terms of crude margins minus the operating costs such as demurrage, safety stock penalties, etc. The more Addressing Robustness for Crude Oil Scheduling under Uncertainty 3 detailed information can be referred to Reddy et al. (2004a, b) and Li et al. (2005 and 2007).

3. Basic formulation and algorithm We employ the formulation of Li et al. (2005 and 2007) as our basis. In their formulation, three binary decision variables are defined as follows to model parcel to SBM/Jetties connection, SBM/jetties to tank connection and tank to CDU connection.

XP = 1 if parcel p is connected for transfer during period t pt {0 otherwise

XT = 1 if tank i is connected to receive crude during period t it {0 otherwise

Y = 1 if tank i feeds CDU u during period t iut {0 otherwise

The more details about their formulation can be found in their paper. We also use their algorithm to solve this MINLP problem.

4. Robustness definition and evaluation Gan and Wirth (2004) defined schedule robustness as schedule effectiveness, performance predictability and rescheduling stability. To keep effectiveness, we allow CDU shutdown or demand shortfalls to ensure feasibilities. For rescheduling stability, we allow schedule changes (defined later) including parcel-SBM/Jetty connection, SBM/Jetty-Tank connection and Tank-CDU connection changes. To measure effectiveness and rescheduling stability, we impose different penalties and incorporate into the objective function. To measure performance predictability, we propose empirical robustness index (RI) as follows to denote the objective deviation. Now, we propose the following procedure to evaluate the robustness of obtained schedules: (1) Simulate S random disruptions and corresponding probabilities – Ps (2) Obtain optimal schedule for each scenario – Profitopt,s (3) Adjust the obtained schedule to address each scenario and compute Rprofits

Rprofits= Profit s - Penalties s (4) Calculate empirical robustness index for schedules,

S Profitopt, s- Rprofit s RI= 1 - Ps s=1 Profit opt, s

5. Methodology This problem is nonconvex mixed integer nonlinear programming (MINLP) that is difficult to solve even for small practical scenarios under deterministic case. In the following, we first present methods to handle demand and ship arrival uncertainty separately, and then try to combine these two uncertainties. 4 Jie Li et al.

5.1. Demand uncertainty We develop a scenario-based formulation in which we treat all binary decision variables (XPpt, XTit, and Yiut) as here and now, which are independent of scenarios and other continuous decision variables (FPTpit, FTUiut, FCTUiuct, FUut, VCTict, Vit), as wait and see, which are related with scenarios. In other words, we need to add scenario index s only to those continuous decision variables. Then, FPTpit, FTUiut, FCTUiuct, FUut, VCTict, Vit become FPTpits, FTUiuts, FCTUiucts, FUuts, VCTicts, and Vits, respectively. XFpt, XLpt, Xpit, TFp and TLp are related with XPpt and XTit, so they are also independent of scenarios. The objective is to maximize the total profit over all scenarios:

Profit =邋 邋 邋FCTUiucts CP cu - DC v - COC 邋 CO ut - 邋 SC ts i u c t s v u t t s

5.2. Ship arrival uncertainty Similar to demand uncertainty, we also present a scenario-based formulation in which we treat all decision variables as wait and see. It means that XPpt, XTit, Yiut, XFpt, XLpt, Xpit, TFp, TLp, FPTpit, FTUiut, FCTUiuct, FUut, VCTict, Vit become XPpts, XTits, Yiuts, XFpts, XLpts, Xpits, TFps, TLps, FPTpits, FTUiuts, FCTUiucts, FUuts, VCTicts, and Vits. By solving this model, we can obtain optimal schedules for each scenario. Recall that the expected nominal arrival time of each ship has the highest probability among all possible arrival time. The following constraints are used to model schedule changes of other scenarios to the nominal scenario to correlate the nominal scenario with other scenarios.

PPXPpts� XP ptn XP pts (p, t) PT, s≠n (1a)

PPXPpts� XP pts XP ptn (p, t) PT, s≠n (1b)

PPXTits� XT its XT itn s≠n (2a)

PPXTits� XT itn XT its s≠n (2b)

PPYiuts� Y iuts Y iutn (i, u) IU, s≠n (3a)

PPYiuts� Y iutn Y iuts (i, u) IU, s≠n (3b)

Where, index n denotes the nominal scenario. PPXPpts, PPXTits and PPYiuts are 0-1 continuous variables. Crudes are allowed to purchase from spot market if not enough. Here, only one crude can be purchased from spot market. If other classes of crudes are not enough to charge corresponding CDUs, then this crude bought from spot market is allowed to charge those CDUs. To model this, we define IFBCuts as the crude amount needed to purchase from spot market for CDU u during period t under scenario s and add it to the demand constraint of CDU u as follows, FU= FTU + IFBC uts iuts uts (i, u) IU (4) i The objective of this model is to maximize the expected profit and minimize the schedule changes simultaneously as follows, Addressing Robustness for Crude Oil Scheduling under Uncertainty 5

Profit=邋PROPs ( 邋 邋 FCTU iucts CP cu - DC vs - COC 邋 CO uts - SC ts ) s i u c t v u t t

-M邋 邋 PROPs PPXP pts - M 邋 PROP s PPXT its p t s i t s

- M邋 邋 PROPs PPY iuts i u t s

+邋 邋PROPs SCP c IFBC uts- PN邋 PROP s IFBC uts u t su t s

Where, PROPs is the corresponding probability of scenario s. M is a big number. SCPc is the margin of the crude bought from spot market. PN is the penalty for that crude used as other classes of crudes to charge CDU. 5.2.1. Heuristic decomposition strategy The model size increases with the number of scenarios and makes the problem hard to solve. Thus, we develop heuristic decomposition strategy to solve this problem. First, we solve the problem for each scenario except the nominal scenario. Then, we solve the nominal scenario with maximizing the expected profit and minimizing schedule changes simultaneously. We take this obtained schedule as “robust” schedule. 5.3. Combination of demand and ship arrival uncertainty We also employ scenario-based formulation for demand and ship arrival uncertainty simultaneously, in which all decision variables including binary and continuous variables are treated as wait and see. Then, XPpt, XTit, Yiut, XFpt, XLpt, Xpit, TFp, TLp, FPTpit, FTUiut, FCTUiuct, FUut, VCTict, Vit become XPpts, XTits, Yiuts, XFpts, XLpts, Xpits, TFps, TLps, FPTpits, FTUiuts, FCTUiucts, FUuts, VCTicts, and Vits. This formulation is very similar to that for ship arrival uncertainty. The objective is to maximize the expected profit and minimize the schedule changes simultaneously. To solve this model, we also use heuristic decomposition strategy to obtain the “robust” schedule.

6. Examples 6.1. Example 1 In this example, only demand uncertainty is involved. A refinery has one VLCC with four crudes, four storage tanks, and two CDUs with 9-period scheduling horizon. The nominal demands of CDU 1 and CDU 2 are 400 kbbl and 400 kbbl, respectively. These two demands can vary within [250kbbl, 550kbbl] uniformly. Five scenarios involving the four vertexes and the nominal demand are used to obtain the robust schedule. We evaluate the robustness of the obtain schedule and the nominal schedule with the proposed procedure using a uniform grid of 49 points distributed within the range of demand uncertainty. Crudes are allowed to purchase from spot market when infeasibilities happen. RI is 0.956 for nominal schedule, while 0.996 for obtained schedule. It means that the obtained schedule is more robust than the nominal schedule. Moreover, the obtained schedule is feasible over the entire demand uncertainty range, while the nominal schedule is infeasible over some part of the uncertainty range. We also evaluate the robustness of the obtained schedule and the nominal schedule using 625 grid points selected by Monte Carlo sampling with normal distribution [N(400, 30×30)] for two demands. RI for obtained schedule and nominal schedule are 0.998. This is because the selected points are more concentrated around the nominal demand. No infeasibilities occur for nominal schedule. 6 Jie Li et al.

6.2. Example 2 In this example, only VLCC arrival delay is considered. We consider one VLCC with four parcels, six tanks and three CDUs with 15-period scheduling horizon. The nominal arrival time for the VLCC is at period five. The VLCC is assumed to arrive within [0, 9 periods]. To operate CDU continuously, one crude is allowed to purchase from spot market if not enough. We consider five scenarios involving 1, 3, 5, 7, 9 periods with corresponding probability 0.01, 0.12, 0.52, 0.35 and 0.009. RI for the nominal schedule is 0.938, while 0.986 for obtained schedule. Thus, the schedule obtained is more robust than the nominal schedule. 6.3. Example 3 We use Example 2 to address demand of CDU 1 and VLCC arrival uncertainty simultaneously. The VLCC uncertainty is same as Example 2. The demand of CDU 1 is allowed to fluctuate within [300kbbl, 500 kbbl]. The nominal demand of CDU 1 is 400 kbbl. One crude is allowed to purchase from the spot market if not enough. We use twenty-five scenarios with corresponding probabilities to obtain the robust schedule. Fifty random scenarios are produced to evaluate the obtained schedule and nominal schedule. RIs are 0.984 and 0.927 for obtained schedule and nominal schedule respectively. It means our obtained schedule is more robust than the nominal schedule.

7. Conclusions/Remarks/future work In this paper, we defined schedule robustness and proposed a procedure to evaluate schedule robustness. Scenario-based models and heuristic decomposition strategy were proposed for demand and ship arrival uncertainties. The result shows that the resulting schedules were superior to the nominal schedules. In the future, we will refine our methodology for demand and ship arrival uncertainty further, investigate the impact of binary variables as wait and see on schedule robustness, and address more uncertainties.

References A. Adhitya, R. Srinivasan, I. A. Karimi, 2004, A heuristic reactive scheduling strategy for recovering from refinery supply chain disruptions, AIChE Annual Meeting, Austin, TX, Nov 7-12. A. Adhitya, R. Srinivasan, I. A. Karimi, 2007a, A heuristic rescheduling approach for managing abnormal events in refinery supply chains, AIChE Journal, 53, 2, 397-422. A. Adhitya, R. Srinivasan, I. A. Karimi, 2007b, A model-based rescheduling framework for managing abnormal supply chain events, Computers and Chemical Engineering, 31, 496-518. H. S. Gan, A. Wirth, 2004, Generating robust schedules on identical parallel machines: heuristic approaches, ICOTA 6, Ballarat, Austra, Dec 9-11. J. Li, W. K. Li, I. A. Karimi, R. Srinivasan, 2005, Robust and efficient algorithm for optimizing crude oil operations, AIChE Annual Meeting, Cincinnati, OH, Oct 30- Nov 4. J. Li, W. K. Li, I. A. Karimi, R. Srinivasan, 2007, Improving the robustness and efficiency of crude scheduling algorithms, AIChE Journal, 53, 10, 2659-2680. P. C. P. Reddy, I. A. Karimi, R. Srinivasan, 2004a, A new continuous time formulation for scheduling crude oil operations. Chem Eng Sci., 59, 1325–1341. P. C. P. Reddy, I. A. Karimi, R. Srinivasan, 2004b, A novel solution approach for optimizing scheduling crude oil operations. AIChE Journal, 50, 1177-1197. S. Neiro, J. M. Pinto, 2005, Multiperiod optimization for production planning of petroleum refineries, Chemical Engineering Communications, 192, 1, 62-88. W. K. Li, C. W. Hui, P. Li, A. X. Li, 2004, Refinery planning under uncertainty, Ind. Eng. Chem. Res., 43, 6742-6755. W. K. Li, I. A. Karimi, R. Srinivasan, 2005, Planning under correlated and truncated price and demand uncertainties, AIChE Annual Meeting, Cincinnati, OH, Oct 30- Nov 4. Addressing Robustness for Crude Oil Scheduling under Uncertainty 7

W. Li, I.A. Karimi, and R. Srinivasan, 2006, Refinery planning under correlated and truncated price and demand uncertainties, ESCAPE-16 and PSE-9, Garmisch-Partenkirchen, Germany, Jul 9-13.