The UK Pharmaceutical Sector an Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

By in Vivo's Biopharma, Medtech and Diagnostics Teams

invivo.pharmaintelligence.informa.com JANUARY 2018 Invol. 36 ❚ no. 01 Vivopharma intelligence ❚ informa 2018 OUTLOOK By In Vivo’s Biopharma, Medtech and Diagnostics Teams PAGE LEFT BLANK INTENTIONALLY invivo.pharmaintelligence.informa.com STRATEGIC INSIGHTS FOR LIFE SCIENCES DECISION-MAKERS CONTENTS ❚ In Vivo Pharma intelligence | January 2018 BIOPHARMA MEDTECH 2018 DIAGNOSTICS OUTLOOK 12 22 28 Biopharma 2018: Medtech 2018: Diagnostics 2018: Is There Still A Place For Pharma The Place For Innovation Steady Progress And In The New Health Care As Value-based Health Care The Big Get Bigger Economy? Gains Momentum MARK RATNER WILLIAM LOONEY ASHLEY YEO If the beginning of 2017 was marked 2018 will be a time of transition in health 2017 was a watershed year in many by doubts around whether and how care, when biopharma’s counterparts respects, politically, economically the FDA would act with respect to in adjacent industry segments scale up and commercially for many players complex diagnostics, we enter 2018 in a radical redesign of their traditional in the medtech field. Where will the feeling that slow-moving vessel may business models. Biopharma is not opportunities lie in 2018? Will finally be turning. moving as quickly, and it confronts a breakthrough medtech innovation still strategic dilemma on how to address the have a place among providers often prospect of a much more powerful set of riding on fumes when it comes to 36 rivals in the ongoing battle to own the budgets, and is it all as bad as some patient experience in medicine. would make out? Thirty-five Years Covering Health Care: The More Things Change… 30 PETER CHARLISH A Virtuous Cycle: What The The health care industry has come a Immuno-Oncology Revolution long way in the past 35 years, although Means For Other Disease Areas in some areas very little has changed. -

Jefferies 2013 Global Healthcare Conference in London

Jefferies 2013 Global Healthcare Conference in London At the 2012 Jefferies Global Healthcare Conference, there were well over 200 healthcare companies participating with a combined market cap of $1 trillion and close to 1,300 one-on-one/small group meetings over the two-day event. The 2013 conference is set to follow the same footsteps, featuring public and private leading INVITATION global healthcare companies within the areas of pharmaceuticals, biotech, generics, 20-21 NOVEMBER 2013 medtech and healthcare services from the US, Central and Eastern Europe, Latin The Waldorf Hilton America, India, China, Japan, Egypt, Israel and Russia. London, UK Throughout the two-day event, we will feature concurrent tracks of informative presentations as well as 1x1/small group meetings, and thematic panel discussions. This global gathering of institutional investors, private equity investors, VCs and leading executives will address near- and long-term investment opportunities and discuss the mechanisms driving global healthcare. We hope you can join us for what promises to be a unique and comprehensive view of the industry. Registration is now open. Please email your Jefferies representative if you are interested in attending. For general questions, please email [email protected] or contact your Jefferies representative. © 2013 Jefferies LLC. Member SIPC. AGENDA WEDNESDAY, 20 NOVEMBER 2013 Jefferies 2013 Global Healthcare Conference in London ADELPHI 1 ADELPHI 2 ADELPHI 3 EXECUTIVE BOARDROOM 7:30 AM Breakfast & Registration 8:00 AM Clinigen Group Plc Ion Beam Applications Active Biotech AB Syneron Medical Ltd. Specialty Pharma & Healthcare Services Medical Products Biotechnology Medical Technology Paul Thomas; CTO Olivier Legrain, CEO Tomas Leanderson; President and CEO Hugo Goldman, CFO 8:40 AM Valneva Celltrion, Inc. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Biotechnology Worldwide

Biotechnology Worldwide There are several countries that are making special efforts to both develop and capitalise on Biotechnology. Chief amongst them is America, though cutting edge work is also going on in the UK, Ireland, Germany, Korea, Singapore, China and Japan. • America is the world leader in biotechnology, it has 1,379 biotechnology companies and employs 174,000 people. It spends £9 billion on research into biotechnology. • The European market for goods and services dependent on biotechnology is currently estimated at £30 billion and is forecast to exceed £100 billion by the year 2005 • The UK leads Europe in biotechnology and employs 19,000 people • The UK has 300 dedicated biotechnology companies and a further 250-300 involved in broader bioscience related activities • The industrial sectors which stand to benefit from biotechnology are pharmaceutical, agriculture, food and drink, chemicals and environmental technologies • Germany is the second strongest country in Europe, with 332 companies but fewer products in development than the UK. UK The UK biotechnology industry is regarded as second only to the huge effort taking place in the States. UK biotechnology companies generate over a billion pounds in revenue; half of this is pumped back into research and development. The industry has particular strengths, for example: • Britain was a key player in the world wide project of sequencing the 30,000 genes of the human genome. The announcement of the first working draft of the human genome marks a significant step forward in our understanding of the way in which we understand and develop treatments for incurable genetic conditions. -

PULSE: Speaker Biographies March 2019

PULSE: Speaker Biographies March 2019 Supported by @BIA_UK www.bioindustry.org In order of appearance: Dr Barbara Domayne-Hayman Entrepreneur-in-residence, Francis Crick Institute, CBO, Autifony Therapeutics Ltd and formerly Chairman, Puridify Barbara has worked on the commercial side of life sciences for thirty years, first in a large organisation (ICI/Zeneca/AstraZeneca), before transitioning to the entrepreneurial world of biotech. Barbara joined the Francis Crick Institute in January 2018 as Entrepreneur-in- residence. She is also Chief Business officer of Autifony, where she is responsible for strategic partnering, fundraising and commercial aspects of drug development for CNS disorders. In December 2017 Autifony signed a major collaboration with Boehringer Ingelheim. Barbara was also Chair of Puridify, a UCL spin-out with a breakthrough biotherapeutics purification technology, which was acquired by GE in November 2017. She chairs the LifeArc Seed Fund investment committee, and is on the Cambridge Enterprise Seed Fund Investment Committee. Previously, Barbara was CEO of Stabilitech, and she was Commercial Director at Arrow Therapeutics until the company was acquired by AstraZeneca. Barbara was also Senior Business Development Manager at Celltech. Barbara has a BA and D Phil in Chemistry from the University of Oxford, and is a Sloan Fellow from London Business School. Steve Bates, OBE CEO, BioIndustry Association Since his appointment as Chief Executive of the BioIndustry Association in 2012, Steve has led major BIA campaigns for, amongst other things, improved access to finance, the refilling of the Biomedical Catalyst, anti-microbial resistance and the opportunity the sector presents to generalist long term investors. Steve champions the adaptive pathway approach to the licensing of new drugs, the need for Early Access and is particularly proud of the working relationship the BIA has established with the UK’s leading medical research charities. -

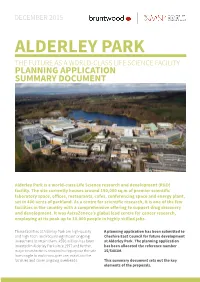

Alderley Park the Future As a World-Class Life Science Facility Planning Application Summary Document

DECEMBER 2015 ALDERLEY PARK THE FUTURE AS A WORLD-CLASS LIFE SCIENCE FACILITY PLANNING APPLICATION SUMMARY DOCUMENT Alderley Park is a world-class Life Science research and development (R&D) facility. The site currently houses around 190,000 sq m of premier scientific laboratory space, offices, restaurants, cafes, conferencing space and energy plant, set in 400 acres of parkland. As a centre for scientific research, it is one of the few facilities in the country with a comprehensive offering to support drug discovery and development. It was AstraZeneca’s global lead centre for cancer research, employing at its peak up to 10,000 people in highly skilled jobs. These facilities at Alderley Park are high-quality A planning application has been submitted to and high-tech, and require significant ongoing Cheshire East Council for future development investment to retain them. £550 million has been at Alderley Park. The planning application invested in Alderley Park since 1997 and further, has been allocated the reference number major investment is required to repurpose the site 15/5401M. from single to multi-occupier use, maintain the facilities and cover ongoing overheads. This summary document sets out the key elements of the proposals. ILLUSTRATIVE MASTERPLAN SIGNIFICANT INVESTMENT PROPOSED OVER THE NEXT 10 YEARS In March 2013, AstraZeneca announced The site was purchased by Bruntwood/MSP, its decision to relocate its R&D facilities to part of Alderley Park Ltd who now wish to Cambridge, leading to uncertainty over the secure the future of the site, retaining talent and future of Alderley Park and its role in the local jobs, by taking forward the Taskforce’s vision. -

A Synopsis of the Joint Environment and Human Health Programme in the UK Michael N Moore*1 and Pamela D Kempton2

Environmental Health BioMed Central Introduction Open Access A synopsis of the Joint Environment and Human Health Programme in the UK Michael N Moore*1 and Pamela D Kempton2 Address: 1Plymouth Marine Laboratory, Prospect Place, the Hoe, Plymouth, PL1 3DH, UK and 2Natural Environment Research Council, Polaris House, North Star Avenue, Swindon, SN2 1EU, UK Email: Michael N Moore* - [email protected]; Pamela D Kempton - [email protected] * Corresponding author from Joint Environment and Human Health Programme: Annual Science Day Conference and Workshop Birmingham, UK. 24-25 February 2009 Published: 21 December 2009 Environmental Health 2009, 8(Suppl 1):S1 doi:10.1186/1476-069X-8-S1-S1 <supplement>Sciences Research <title> Council <p>Proceedings (BBSRC), Engineering of the Joint and Environment Physical Sciences and Human Research Health Council Programme: (EPSRC) Annual and Health Science Protection Day Conference Agency (HPAand Work).</note>shop</p> </sponsor> </title> <note>Proceedings</note> <editor>Michael N Moore <url>http://www.biomedcentral.com/content/pdf/1476-069X-8-s1-info.pdf</url>and Pamela D Kempton</editor> <sponsor> <note>Publication of this supplement </sup wasplement> made possible with support from the Natural Environment Research Council (NERC), Environment Agency (EA), Department of the Environment & Rural Affairs (Defra), Ministry of Defence (MOD), Medical Research Council (MRC), The Wellcome Trust, Economic & Social Research Council (ESRC), Biotechnology and Biological This article is available from: http://www.ehjournal.net/content/8/S1/S1 © 2009 Moore and Kempton; licensee BioMed Central Ltd. This is an open access article distributed under the terms of the Creative Commons Attribution License (http://creativecommons.org/licenses/by/2.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. -

The Impact on Health of Emissions to Air from Municipal Waste Incinerators

The Impact on Health of Emissions to Air from Municipal Waste Incinerators Advice from the Health Protection Agency RCE-13 The Impact on Health of Emissions to Air from Municipal Waste Incinerators Advice from the Health Protection Agency Documents of the Health Protection Agency Radiation, Chemical and Environmental Hazards February 2010 © Health Protection Agency 2010 Contents The Impact on Health of Emissions to Air from Municipal Waste Incinerators Advice from the Health Protection Agency 1 Summary 1 Introduction 3 Particles 4 Carcinogens 8 Dioxins 9 Epidemiological studies: municipal waste incinerators and cancer 11 Conclusions 11 References 12 Glossary 14 The Impact on Health of Emissions to Air from Municipal Waste Incinerators Advice from the Health Protection Agency Prepared by R L Maynard, H Walton, F Pollitt and R Fielder Summary The Health Protection Agency has reviewed research undertaken to examine the suggested links between emissions from municipal waste incinerators and effects on health. While it is not possible to rule out adverse health effects from modern, well regulated municipal waste incinerators with complete certainty, any potential damage to the health of those living close-by is likely to be very small, if detectable. This view is based on detailed assessments of the effects of air pollutants on health and on the fact that modern and well managed municipal waste incinerators make only a very small contribution to local concentrations of air pollutants. The Committee on Carcinogenicity of Chemicals in Food, Consumer Products and the Environment has reviewed recent data and has concluded that there is no need to change its previous advice, namely that any potential risk of cancer due to residency near to municipal waste incinerators is exceedingly low and probably not measurable by the most modern techniques. -

Datasheet Report

Envirocheck ® Report: Datasheet Order Details: Order Number: 211218796_1_1 Customer Reference: 0516105 National Grid Reference: 353910, 383560 Slice: A Site Area (Ha): 2.98 Search Buffer (m): 1000 Site Details: Kawneer UK Ltd, Astmoor Road Astmoor Industrial Estate RUNCORN WA7 1QQ Client Details: Mr J Stapeley ERM Ethos Building Kings Road Swansea Waterfront Swansea SA1 8AS Order Number: 211218796_1_1 Date: 16-Jul-2019 rpr_ec_datasheet v53.0 A Landmark Information Group Service Contents Report Section Page Number Summary - Agency & Hydrological 1 Waste 59 Hazardous Substances 67 Geological 69 Industrial Land Use 73 Sensitive Land Use 94 Data Currency 95 Data Suppliers 101 Useful Contacts 102 Introduction The Environment Act 1995 has made site sensitivity a key issue, as the legislation pays as much attention to the pathways by which contamination could spread, and to the vulnerable targets of contamination, as it does the potential sources of contamination. For this reason, Landmark's Site Sensitivity maps and Datasheet(s) place great emphasis on statutory data provided by the Environment Agency/Natural Resources Wales and the Scottish Environment Protection Agency; it also incorporates data from Natural England (and the Scottish and Welsh equivalents) and Local Authorities; and highlights hydrogeological features required by environmental and geotechnical consultants. It does not include any information concerning past uses of land. The datasheet is produced by querying the Landmark database to a distance defined by the client from a site boundary provided by the client. In this datasheet the National Grid References (NGRs) are rounded to the nearest 10m in accordance with Landmark's agreements with a number of Data Suppliers. -

Register of GDP Sites 2019

Register of GDP Sites 2019 Updated 16 August 2019 There are other sites authorised for wholesale dealing of veterinary medicinal products which do not appear on this register. These sites wholesale deal in both human and veterinary medicinal products and can be found on the MHRA section of GOV.UK: https://www.gov.uk/government/publications/human-and-vetinary-medicines- register-of-licensed-wholesale-distribution-sites-december-2014 Register of Authorised Wholesale Dealer Sites Authorisation Holder: WDA33618 ABBEYVET LLP 310 CHESTER ROAD, HARTFORD, NORTHWICH, CHESHIRE, CW8 2AB SITE ID: S0415 ABBEYVET LLP 310 CHESTER ROAD, HARTFORD, NORTHWICH, CHESHIRE, CW8 2AB SITE ID: S0010 ABBEYVET LLP SHERBURN ENTERPRISE PARK, SHERBURN IN ELMET, LEEDS, WEST YORKSHIRE, LS25 6NB Authorisation Holder: WDA8599 AGRIHEALTH (N.I.) LIMITED 9 SILVERWOOD INDUSTRIAL AREA, SILVERWOOD ROAD, LURGAN, CRAIGAVON, COUNTY ARMAGH, BT66 6LN SITE ID: S0015 AGRIHEALTH (N.I.) LIMITED 9 SILVERWOOD INDUSTRIAL AREA, SILVERWOOD ROAD, LURGAN, CRAIGAVON, COUNTY ARMAGH, BT66 6LN Authorisation Holder: WDA5097 ALBAVET LIMITED BUSINESS INCUBATOR OFFICE 21, MYREGORMIE PLACE, MITCHELSTON INDUSTRIAL ESTATE, KIRKCALDY, FIFE, KY1 3NA SITE ID: S0456 ALBAVET LIMITED BUSINESS INCUBATOR OFFICE 21, MYREGORMIE PLACE, MITCHELSTON INDUSTRIAL ESTATE, KIRKCALDY, FIFE, KY1 3NA SITE ID: S0525 CVS GROUP PLC CVS HOUSE, OWEN ROAD, DISS, NORFOLK, IP22 4ER Authorisation Holder: WDA5030 ALBERT E JAMES & SON LIMITED BARROW MILL BARROW STREET, BARROW GURNEY, BRISTOL, BS48 3RU SITE ID: S0303 ALBERT E JAMES & -

Congressional Record United States Th of America PROCEEDINGS and DEBATES of the 105 CONGRESS, SECOND SESSION

E PL UR UM IB N U U S Congressional Record United States th of America PROCEEDINGS AND DEBATES OF THE 105 CONGRESS, SECOND SESSION Vol. 144 WASHINGTON, WEDNESDAY, SEPTEMBER 23, 1998 No. 128 Senate The Senate met at 9:30 a.m. and was long last, I think we are going to be Lott (for Grassley/Hatch) Amendment No. called to order by the President pro able to complete action on this legisla- 3559, in the nature of a substitute. tempore [Mr. THURMOND]. tion and get it into conference and give Mr. DURBIN addressed the Chair. us a good opportunity then to get this The PRESIDING OFFICER. The Sen- PRAYER work completed by the session’s end. ator from Illinois is recognized. The Chaplain, Dr. Lloyd John It is expected that several amend- Ogilvie, offered the following prayer: ments will be offered and debated this Mr. DURBIN. Mr. President, I thank God our Father, we pause in the morning, with a stacked series of roll- the majority leader for announcing the midst of the changes and challenges of call votes occurring at approximately schedule this morning. Those who have life to receive a fresh experience of 11:45 a.m. It looks like there will be followed the last few days of Senate de- Your goodness. You are consistent; You two votes, probably, in that sequence, bate know we are considering a reform constantly fulfill Your plans and pur- at 11:45. Those votes will hopefully in- of the bankruptcy code. We will be poses; and You are totally reliable. -

Etf-Sparpläne

ETF-SPARPLÄNE ISIN NAME IE00B8KGV557 ISHARES EDGE MSCI EM MIN VOL USD (ACC) IE00B86MWN23 ISHARES EDGE MSCI EUROPE MIN VOLATILITY EUR (ACC) IE00B8FHGS14 ISHARES EDGE MSCI WORLD MIN VOLATILITY USD (ACC) IE00B6SPMN59 ISHARES EDGE S&P 500 MIN VOL USD (ACC) IE00B87G8S03 ISHARES GLOBAL AAA-AA GOV BOND USD (DIST) DE0005933931 ISHARES CORE DAX EUR (ACC) IE0032523478 ISHARES CORP BOND LARGE CAP EUR (DIST) IE00B14X4T88 ISHARES ASIA PACIFIC DIVIDEND USD (DIST) IE00B1W57M07 ISHARES BRIC 50 USD (DIST) DE000A0F5UG3 ISHARES DOW JONES EU SUSTAINABLE EUR (DIST) IE00B6R52143 ISHARES AGRIBUSINESS USD (ACC) IE00B0M62Y33 ISHARES AEX EUR (DIST) DE000A0D8Q23 ISHARES ATX EUR (DIST) IE00B1FZSC47 ISHARES USD TIPS USD (ACC) IE00B14X4S71 ISHARES USD TREASURY BOND 1-3Y USD (DIST) IE00B1FZS798 ISHARES USD TREASURY BOND 7-10Y USD (DIST) IE00B1FZSD53 ISHARES GBP INDEX-LINKED GILTS GBP (DIST) IE00B6QGFW01 ISHARES EMERGING ASIA LOCAL GOV BOND USD (DIST) IE00B5M4WH52 ISHARES JPM EM LOCAL GOV BOND USD (DIST) IE00B3DKXQ41 ISHARES EURO AGGREGATE BOND EUR (DIST) IE00B3F81R35 ISHARES CORE EURO CORP BOND EUR (DIST) IE00B4L60045 ISHARES EURO CORP BOND 1-5Y EUR (DIST) IE00B4L5ZG21 ISHARES EURO CORP BOND EX-FIN EUR (DIST) IE00B4L5ZY03 ISHARES EURO CORP BOND EX-FIN 1-5Y EUR (DIST) IE00B6X2VY59 ISHARES EURO CORP BOND INT. RATE HEDGED (DIST) IE00B14X4Q57 ISHARES EURO GOV BOND 1-3Y EUR (DIST) IE00B4WXJH41 ISHARES EURO GOV BOND 10-15Y EUR (DIST) IE00B1FZS913 ISHARES EURO GOV BOND 15-30Y EUR (DIST) IE00B1FZS681 ISHARES EURO GOV BOND 3-5Y EUR (DIST) IE00B4WXJG34 ISHARES EURO GOV BOND