Australian ESG/SRI

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Monthly NTA and Performance Update

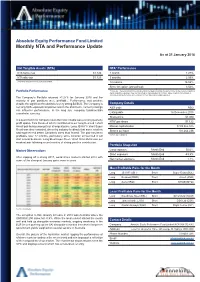

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

June 2019 42

y 4 6 Equit 2019 June High Conviction High Quarterly NewsletterQuarterly No. Selector Fund In this quarterly edition, we review performance and attribution for the quarter. We highlight the importance of innovation and culture within organisations and profile ResMed and Cochlear, two leading healthcare businesses. We visit Fisher & Paykel Healthcare in New Zealand and look at one of the biggest growth industries in the world today, cyber security. Photo. Selector analyst trekking through the Atlas Mountains and local Berber kids. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au P Selector is a boutique fund manager. Our team, combined, have over 150 years of experience in financial markets. We believe in long-term wealth creation and building lasting relationships with our investors. We focus on stock selection, the funds are high conviction, concentrated and index unaware. As a result, the portfolios have low turnover and produce tax effective returns. Selector has a 15-year track record of outperformance and we continue to seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. Selector High Conviction Equity Fund Quarterly Newsletter #64 CONTENTS IN BRIEF – JUNE QUARTER 3 PORTFOLIO OVERVIEW 5 PORTFOLIO CONTRIBUTORS 7 MARKET INSIGHTS AND OBSERVATIONS 13 INNOVATION + CULTURE = SUCCESS 17 RESMED INC. 20 WAKE-UP CALL 31 FISHER & PAYKEL HEALTHCARE – JUNE 2019 42 RISK OUT…UPFRONT 45 COMPANY VISIT DIARY – JUNE 2019 QUARTER 57 2 Selector Funds Management IN BRIEF – JUNE QUARTER Dear Investor, Looking back on 2019, it would be fair to say that few identify the businesses we want to own on a case by case foresaw how the events of the financial year would basis, understand them to the best of our abilities and unfold. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Participant List

PARTICIPANT LIST Please find below a list of current participants in the Quarterly Salary Review. For a complete list by super sector, sector and segment refer to Mercer WIN®. 3M Australia API 7-Eleven Stores API Management A Menarini Australia APL Co. (Aus) - BR A.P.Moller-Maersk AS (AU) Apotex Abbott Australasia APT Management Services (APA Group) AbbVie Aquila Resources Actelion Pharmaceuticals Australia Arrium Mining & Materials Adama Australia Arrow Electronics Australia Adelaide Brighton Asahi Beverages Australia Adelaide Football Club Asaleo Care Australia adidas Australia Ascendas Hospitality Australia Fund Management Adventist Healthcare Aspen Australia AECOM Astrazeneca Afton Chemical Asia Pacific LLC AT & T Global Network Services Australia Aggreko Australia ATCO Australia AIA Australia Atlas Iron Aimia Proprietary Loyalty Australia Ausenco Air New Zealand – Australia AusGroup Akzo Nobel Australia Australia Post Alcatel-Lucent Australia Australian Catholic University Alcon (Novartis) Laboratories Australia Australian Computer Society Alexion Australasia Australian Fashion Labels Allergan Australian Red Cross Blood Service Alphapharm Avaloq Australia Alstom Transport Australia Aveo Group Amadeus IT Pacific Aviall Australia American Express Global Business Travel Australia AVJennings Holdings Amgen Australia Avon Products AMT Group BaptistCare NSW & ACT Amway of Australia Barminco Apex Tool Group BASF Australia © March 2017 Mercer Consulting (Australia) Pty Ltd Quarterly Salary Review 4.1 PARTICIPANT LIST Beam Global Australia -

Seven Group Holdings Limited Annual Report

Seven Group Holdings Limited Annual Report Seven Group Holdings Limited (ABN 46 142 003 469) Annual Report 2010 1 2 Seven Group Holdings Limited From the Executive Chairman 4 Year in Review 6 WesTrac Group 10 Seven Media Group Broadcast Television 16 Magazine Publishing 18 Digital Media 20 Board of Directors 22 Corporate Governance 24 Directors’ Report 31 Auditor’s Independence Declaration 44 Financial Statements 45 Notes to the Financial Statements 49 Directors’ Declaration 104 Independent Auditor’s Report 105 Company Information 107 Investor Information 108 Shareholder Information 109 Corporate Directory 111 TRANSFORMING OUR BUSINESS MIX Seven Group Holdings Limited (ABN 46 142 003 469) Annual Report 2010 3 From the Executive Chairman Welcome to the fiRst I have had a long and proud association ThE past TwElvE with WesTrac and Seven. Both are monthS confirm AnnuAl RepoRt foR leaders in their sectors. Both have what seven GRoup holdinGs. I consider the best management teams in our commitment the country, led by David Leckie at Seven to expanding our this hAs been A and Jim Walker at WesTrac. And, we have siGnificAnt tWelve some of the best people working with us. presencE in media Seven Network Limited took a bold step in Australia. months foR All of four years ago to create Seven Media us, With the cReAtion Group. It is a move that allowed Seven Network Limited to grow and prosper. of a neW compAny, Seven Network Limited evolved into an foRmed thRouGh A scRip investment company with strong media platforms and the financial capacity to foR scRip mergeR of expand into new sectors. -

News Corporation (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 November 15, 2017 DATE OF REPORT (DATE OF EARLIEST EVENT REPORTED) NEWS CORPORATION (EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER) Delaware 001-35769 46-2950970 (STATE OR OTHER JURISDICTION (COMMISSION FILE NO.) (IRS EMPLOYER OF INCORPORATION) IDENTIFICATION NO.) 1211 Avenue of the Americas, New York, New York 10036 (ADDRESS OF PRINCIPAL EXECUTIVE OFFICES, INCLUDING ZIP CODE) (212) 416-3400 (REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2). Emerging growth company ☐ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. -

Abstract a Case Study of Cross-Ownership Waivers

ABSTRACT A CASE STUDY OF CROSS-OWNERSHIP WAIVERS: FRAMING NEWSPAPER COVERAGE OF RUPERT MURDOCH’S REQUESTS TO KEEP THE NEW YORK POST by Rachel L. Seeman Media ownership is an important regulatory issue that is enforced by the Federal Communications Commission. The FCC, Congress, court and public interest groups share varying viewpoints concerning what the ownership limits should be and whether companies should be granted a waiver to be excused from the rules. News Corporation is one media firm that has a history of seeking these waivers, particularly for the New York Post and television stations in same community. This study conducted a qualitative framing analysis of news articles from the New York Times and the Wall Street Journal to determine if the viewpoints expressed by the editorial boards were reflected in reports on News Corp.’s attempt to receive cross-ownership waivers. The analysis uncovered ten frames the newspapers used to assist in reporting the events and found that 80% of these frames did parallel the positions the paper’s editorial boards took concerning ownership waivers. A CASE STUDY OF CROSS-OWNERSHIP WAIVERS: FRAMING NEWSPAPER COVERAGE OF RUPERT MURDOCH’S REQUESTS TO KEEP THE NEW YORK POST A Thesis Submitted to the Faculty of Miami University in partial fulfillment of the requirements for the degree of Master of Arts Department of Communications by Rachel Leianne Seeman Miami University Oxford, OH 2009 Advisor: __________________________________ (Dr. Bruce Drushel) Reader: __________________________________ (Dr. Howard -

Annual Report 2017

17ANNUAL REPORT 2017 p p p p p p 02 04 07 08 32 50 About Us Highlights Chairman’s CEO’s Year Sustainability, Directors’ Introduction In Review Community + + Remuneration People Reports Operating + Financial Review 20 Consolidated Financial Statements 78 Annual General Meeting Group Strategy 22 Executive Team 44 The 54th Annual General Meeting of the Company will be held at 11am on 26 October Group and Divisional Results 24 Directors’ Profiles 48 2017 at the Blackmores Campus, 20 Jubilee Avenue, Warriewood NSW 2102. Financial Review 26 Auditor’s Independence Declaration 72 Cover image: Fiona Yeo, Assistant Marketing Operating Review 28 Independent Auditor’s Report 73 Manger, Export Sales. Fiona is profiled in this Group Risks 30 Directors’ Declaration 77 report on page 42. Additional Information 118 Company Information 119 OUR ANNUAL REPORT 2017 BLACKMORES ANNUAL REPORT 2017 REPORT ANNUAL BLACKMORES OUR OUR #4 STRATEGIC VALUES PURPOSE PRIORITIES Blackmores’ values are at Blackmores improves Blackmores is committed the heart of our business. people’s lives by delivering to superior business These values, known as the world’s best natural performance. Our strategic PIRLS, are both behavioural health solutions. We direction is focused on and aspirational. They achieve this by translating delivering growth and underpin our work practices our unrivalled heritage and continuous improvement to and are supported by legal knowledge into innovative, maintain Blackmores’ leading policies and procedures. quality branded healthcare position in the industry and solutions that work. to achieve ongoing success Passion for Natural Health for our company, our people Integrity and our shareholders. Respect Leadership #1 Consumer Centricity Social Responsibility #2 Asia Growth #3 Product Leadership #4 Operational Effectiveness THE 2017 ANNUAL REPORT OF BLACKMORES LIMITED PROVIDES INFORMATION ON THE ORGANISATION AND COMPANY PERFORMANCE FOR THE YEAR 1 JULY 2016 TO 30 JUNE 2017. -

Is Xero in the BUY Zone?

Monday 15 March 2021 Is Xero in the BUY zone? I don’t think all tech stocks are born equal. What I’m really saying is Apple is very different to Zoom, while Xero is not like Afterpay. They’re lumped in the same tech group and can get sold off when tech loses friends but this sometimes silly sell-off could be creating opportunities. For the last month, tech stocks have been in the twilight zone and Xero has dropped from its highs. Does this mean it’s passed over into the buy zone? Sincerely, Peter Switzer Inside this Issue 02 Is Xero in the buy zone? Is Xero in the buy zone? by Peter Switzer 05 Does environmental, social and corporate governance (ESG) investing stack up? And what’s the best ETF? Does ESG investing stack up? by Paul Rickard 08 5 companies at the forefront of the hydrogen push FMG, HZR, LCK, HXG & PH2 Is Xero in the buy by James Dunn 11 My “HOT” stock: QAN zone? Qantas by Peter Switzer by Maureen Jordan 02 12 Buy, Hold, Sell – What the Brokers Say 12 upgrades, 5 downgrades by Rudi Filapek-Vandyck Important information: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. For this reason, any individual should, before Switzer Super Report is published by Switzer Financial Group Pty Ltd AFSL No. 286 531 acting, consider the appropriateness of the information, having regard to the Level 4, 10 Spring Street, Sydney, NSW, 2000 individual's objectives, financial situation and needs and, if necessary, seek T: 1300 794 893 F: (02) 9222 1456 appropriate professional advice. -

Proposal to Acquire Seven Media Group

West Australian Newspapers Holdings Limited ACN 053 480 845 PROPOSAL TO ACQUIRE SEVEN MEDIA GROUP EXPLANATORY MEMORANDUM INDEPENDENT EXPERT’S REPORT NOTICE OF EXTRAORDINARY GENERAL MEETING Notice is given that an Extraordinary General Meeting of Shareholders will be held at the Hyatt Regency Hotel, 99 Adelaide Terrace, Perth, Western Australia on 11 April 2011, commencing at 10am (Perth time). LEGAL ADVISER FINANCIAL ADVISER Important notices This Explanatory Memorandum is important other information made available by or on Such risks, uncertainties and other important and requires immediate attention. It should behalf of SGH during the due diligence factors include, among other things, the risks be read in its entirety before making a process conducted by WAN in connection in associated with the Proposed Transaction decision on how to vote on the Resolutions. with the Proposed Transaction. There is as set out in Section 6. Shareholders are In particular, it is important that you consider no assurance that this due diligence was cautioned not to place undue reliance on the disadvantages and potential risks conclusive and that all material issues and such forward looking statements. Deviations of the Proposed Transaction set out in risks in relation to the Proposed Transaction as to future results, performance and Section 1.3 and Section 6 and the views and SMG have been identifi ed. To the extent achievement are both normal and expected. of the Independent Expert set out in the that this information is incomplete, incorrect, Any discrepancies between totals and sums Independent Expert’s Report contained inaccurate or misleading, there is a risk of components in tables and fi gures contained in Appendix A. -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher.