GAIN Report Global Agriculture Information Network

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Review of Annual Reports 2010 of Euronext Brussels Listed Companies 2 Grant Thornton Corporate Governance Review

Corporate Governance Review Review of Annual Reports 2010 of Euronext Brussels listed companies 2 Grant Thornton Corporate Governance Review Contents Contents 3 Foreword 5 Executive summary 7 PART I - Legally binding provisions 11 1. Corporate Governance Statement 12 2. Remuneration committee 17 3. Remuneration report 19 4. Audit committee – Legal requirements 22 PART II - Results corporate governance code 25 5. Board of directors 26 6. Independence 28 7. Nomination committee 30 8. Audit committee – Code requirements 32 Appendix A - Survey methodology 37 Appendix B - List of companies 39 3 4 Grant Thornton Corporate Governance Review Foreword We are pleased to present the Another key factor in the corporate governance debate is the interest of the European Commission second annual publication in Grant and the impact this will have on corporate governance Thornton’s series of reviews of the legislation. The European Commission released a corporate governance disclosures consultation paper on an EU corporate governance of Belgian companies quoted on framework and is seeking submissions from interested parties. We may, therefore, see a single EU-wide the Euronext stock exchange. The corporate governance framework in the not so distant review examines the extent to which future. companies comply with regulatory Corporate governance is fundamentally about requirements. ensuring that key stakeholders, including the public, can have confidence in how business is conducted and This year’s report arrives at a time of turmoil for results are disclosed by public interest entities such Belgian listed companies. While the Belgian banking as listed companies, financial institutions and public sector was struggling for survival and stock markets sector organisations. -

Global Vs. Local-The Hungarian Retail Wars

Journal of Business and Retail Management Research (JBRMR) October 2015 Global Vs. Local-The Hungarian Retail Wars Charles S. Mayer Reza M. Bakhshandeh Central European University, Budapest, Hungary Key Words MNE’s, SME’s, Hungary, FMCG Retailing, Cooperatives, Rivalry Abstract In this paper we explore the impact of the ivasion of large global retailers into the Hungarian FMCG space. As well as giving the historical evolution of the market, we also show a recipe on how the local SME’s can cope with the foreign competition. “If you can’t beat them, at least emulate them well.” 1. Introduction Our research started with a casual observation. There seemed to be too many FMCG (Fast Moving Consumer Goods) stores in Hungary, compared to the population size, and the purchasing power. What was the reason for this proliferation, and what outcomes could be expected from it? Would the winners necessarily be the MNE’s, and the losers the local SME’S? These were the questions that focused our research for this paper. With the opening of the CEE to the West, large multinational retailers moved quickly into the region. This was particularly true for the extended food retailing sector (FMCG’s). Hungary, being very central, and having had good economic relations with the West in the past, was one of the more attractive markets to enter. We will follow the entry of one such multinational, Delhaize (Match), in detail. At the same time, we will note how two independent local chains, CBA and COOP were able to respond to the threat of the invasion of the multinationals. -

Elia Group Full Year 2020 Results

Elia Group Full Year 2020 Results Wednesday, 3rd March 2021 Transcript produced by Global Lingo London – 020 7870 7100 www.global-lingo.com Elia Group Full Year 2020 Results Wednesday, 3rd March 2021 Elia Group Full Year 2020 Results Marleen Vanhecke: Good morning, ladies and gentlemen. Thank you for participating in our livestreamed event, which is being broadcast from a corona-proof studio in Brussels. It would have been nicer to meet you in person, of course, but the lockdown measures have forced us to present our full year results in another format. The setup is different, but we will keep you just as informed as we normally would. What hasn't changed are today's speakers. Elia Group is represented by Catherine Vandenborre, CFO, and by Chris Peeters, CEO, both in good health, as you can see. Today's programme is as follows. First, we will give you an overview of the headlines from 2020. We will talk with Chris Peeters about the acceleration of the energy transition and how Elia Group is managing it. Catherine Vandenborre will then present the financial results. And finally, we will present our conclusion and an outlook on the years to come. Before we start, I would like to present a disclaimer for today's presentation as mentioned on the title page. You must read the disclaimer before we can continue. I suppose you have all done it by now. Am I right? So let's immediately go to the first question for Chris. Marleen Vanhecke: Chris, looking back at 2020, it's impossible to avoid the corona crisis, of course. -

Romania: Retail Food Sector

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 2/6/2017 GAIN Report Number: RO1703 Romania Post: Bucharest Retail Food Sector Report Categories: Retail Foods Approved By: Russ Nicely Prepared By: Ioana Stoenescu Report Highlights: Over the last three years, Romania has seen strong positive growth, with encouraging developments in the economic and policy areas, becoming one of the most attractive markets in Southeastern Europe. After just a few notable events during 2015, the Romanian retail market experienced remarkable growth in 2016 reaching 2,000 stores operated by international retailers. As modern retail systems grow, exports of U.S. processed and high value foods to Romania will continue to expand. In 2015 U.S. agri- food exports to Romania increased by 45 percent from U.S. $96 million to U.S. $139 million over the last year. Romania's food sector is expected to be among the regional best performers during the next five years, with promising market prospects for U.S. exporters such as tree nuts, distilled spirits and wines. General Information: I. MARKET SUMMARY General Information Romania has been a member of the EU since 2007 and a member of NATO since 2004. Within the 28 EU countries, Romania has the seventh largest population, with 19.5 million inhabitants. Romania is presently a market with outstanding potential, a strategic location, and an increasingly solid business climate. Although there is the need for an exporter to evaluate the market in order to assess the business opportunities, exporting to Romania is steadily becoming less challenging than in previous years in terms of the predictability of the business environment. -

Colruyt Group Increases Stake in Holding That Includes Fashion Retailer ZEB

PRESS RELEASE - Halle (Belgium) – 3 September 2020 (17h45 CET) Colruyt Group increases stake in holding that includes fashion retailer ZEB On 3 September 2020 Colruyt Group increased its stake in Fraluc Group from 68% to over 96%. Fraluc is the holding that includes the fashion retail chains ZEB, PointCarré, The Fashion Store and ZEB For Stars. The management teams of the respective companies remain unchanged. On 21 June 2014 Colruyt Group acquired a 50% stake in the Belgian fashion retailer ZEB through the company Fraluc NV. As part of the agreement, the management agreed to grant put and call options, enabling Colruyt Group to gain control over ZEB via Fraluc NV. In the meantime, ZEB has continued to develop within the Fraluc Group, which also comprises PointCarré, The Fashion Store and ZEB For Stars. At the end of the financial year 2019/20, Colruyt Group held 68% of the Fraluc Group shares. On 3 September 2020, Colruyt Group and Fraluc Group's management entered into an agreement to increase Colruyt Group's stake in Fraluc Group to over 96%. The management remains on board in its current composition. The parties agreed not to disclose any details on the terms of the transaction. The transaction is subject to approval by the Belgian Competition Authority (BCA), which is expected to be obtained in the coming weeks. Following approval by the BCA, the stake held in Fraluc Group will be fully consolidated as a subsidiary of Colruyt Group and no longer be accounted for as a joint venture using the equity method. Contacts For questions on this press release or for further information, please contact us as follows: Journalists: Silja Decock (Press Officer) Tel. -

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

Purpose & Patience

PURPOSE & PATIENCE We aspire to be the preferred partner of entrepreneurs and families who lead growing companies by backing them with patient capital and supportive advice — Q1 2020 Edition — OUR MISSION Our goal at Sofina is to create economic value with a human approach We believe that the entrepreneurial spirit that characterises many family businesses and growth companies is a source of progress. By supporting these entrepreneurs and innovators, we intend to contribute to global growth, development and innovation. We believe entrepreneurs become successful by being competitive in a globalised market Our mission is to provide patient capital, expertise and advice to growing companies led by entrepreneurs and families. We aspire to be their preferred partner, and have a long-term horizon that few other investors can match. Our heritage and culture are what make us unique We put human relationships at the heart of what we do. All our investments are stories of shared values, friendships and ambitious projects with talented entrepreneurs and their management teams. By continuously working in this way, we aspire to become the preferred investment partner of those sharing our beliefs and vision. 2 SOFINA - PURPOSE & PATIENCE OUR MISSION 3 KEY FIGURES Highlights EUR 7.63 BN GLOBAL SHAREHOLDERS’ EQUITY REACH A FAMILY RUN 3 US EUROPE ASIA AND CONTROLLED COMPLEMENTARY Change over the last 20 INVESTMENT COMPANY INVESTMENT years (2) STYLES 8.00 7.00 6.00 5.00 FOUR FOCUS 4.00 SECTORS Long-term minority 3.00 investments 2.00 1.00 43% OF SHAREHOLDERS’ EQUITY (1) Offices in Brussels, 0 Luxembourg and Singapore Consumer and Retail 1999 2019 Sofina Private Funds – Investments in venture and growth capital funds Digital Transformation 31% OF SHAREHOLDERS’ EQUITY (1) Roots going back 26 Sofina Growth – Investments in Education investment fast-growing businesses professionals 120+ YEARS across our 20% OF SHAREHOLDERS’ EQUITY (1) 3 offices Healthcare (1) Considering the portfolio in transparency. -

DEMO Competitive Analysis Retail

COMPETITIVE ANALYSIS – DEMO REPORT LARGE RETAILERS IN ROMANIA AUCHAN CORA CARREFOUR 1.1 Auchan 1. General data Company name: Auchan Romania SA Address (headquarters): Str. Barbu Delavrancea 13, Bucharest Phone: +4021 4080107 Fax: +4021 2232024 Web: www.auchan.ro E-mail: [email protected] Year of establishment: 2005 Ownership: Auchan Group 2. Financial data Year/Category Net turnover Average no of Net profit (mil. EUR) employees (mil. EUR) 2010 355.8 3,184 -4.6 2009 307.6 3,103 -9.7 2008 278.4 3,156 -6.7 A FRD Center Market Entry Services Demo Publication www.market-entry.ro 3. Key persons Name Position Contact details Mr. Patrick Espasa General Director Email: [email protected] Mr. Tiberiu Danetiu Marketing Director Email: [email protected] Ms. Mariana Dragan Communication Manager Email: [email protected] Tel: +4 021 4080294 4. Brief profile Auchan Romania is part of the French Group Auchan. Auchan opened its first hypermarket on the Romanian market in 2006. This store is located in Bucharest (in the Titan area) and has the surface of over 16,000 sqm. The store records a daily traffic of 30,000 – 45,000 persons and registers the biggest sales in the Auchan network in Romania. At present, Auchan has nine hypermarkets in Romania, located in Bucharest (two stores – in the Titan and Militari areas), Pitesti, Targu Mures, Cluj Napoca, Suceava, Timisoara, Constanta and Craiova. The Auchan hypermarket in Cluj Napoca was opened in November 2007, with an investment of 40 million EUR. The store is located in the Iulius Mall, has the surface of some 10,000 sqm and offers over 45,000 products. -

Ets Fr. COLRUYT SA Limited Liability Company Edingensesteenweg 196 – 1500 Halle Company Number: 0400.378.485

PRESS RELEASE - Halle (Belgium), 18/12/2015 - Regulated information – Declaration of transparency Ets Fr. COLRUYT SA Limited Liability Company Edingensesteenweg 196 – 1500 Halle Company number: 0400.378.485 Structure of the shareholdership of the Ets Fr. Colruyt S.A. according to the latest transparency notifications of 17/12/2015 In the framework of the law of 2 May 2007 and the Royal decree of 14 February 2008 (publication of the important participations in the companies listed on the stock exchange) we received an updated notification of the participation of the Colruyt family, Sofina Group and Colruyt Group on 17/12/2015. On 13 July 2015 D.I.M. NV, H.I.M. NV, H.I.M. Drie NV, D.H.A.M. NV and KORYS NV were merged. As a result, all Colruyt shares held by these companies are now owned by KORYS NV and KORYS NV has crossed the 45% threshold . 7.500.000 treasury shares were cancelled on 17/12/2015. Hence, the 'Colruyt treasury shares purchased' rate was updated and the number of treasury shares purchased by Colruyt Group has dropped below the 5% threshold. The new denominator of 149.609.386 shares takes into account the cancellation of 7.500.000 treasury shares and the capital increase reserved for employees, for which 472.883 new shares were issued on 17/12/2015. The company has no knowledge of other agreements between shareholders. The legal thresholds per 5% portion apply.. I. Colruyt family and relatives Number % 1. Stichting Administratiekantoor Cozin 0 0,00 2. Colruyt family 9.127.879 6,10 3. -

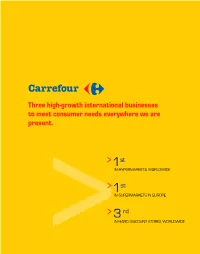

Iacarrefoura2000ieng.Pdf

Three high-growth international businesses to meet consumer needs everywhere we are present. > 1st IN HYPERMARKETS WORLDWIDE > 1st IN SUPERMARKETS IN EUROPE > 3 rd >IN HARD DISCOUNT STORES WORLDWIDE MESSAGEMESSAGE FROM THE CHAIRMAN > At the end of January, the European Commission cleared our mer- ger with Promodès. We decided on the rapid consolidation of all our hyper- markets under the Carrefour trade name, and all our supermarkets under a common trade name in each country. > In 87 hypermarkets and 490 supermarkets in France, and 117 hypermarkets and 109 supermarkets in Spain, Italy, Greece, Turkey, Indonesia, China and Korea, the current teams in Continent, Pryca, Continente, Euromercato, Stoc, Maxor and Supeco stores transform- ed those stores and reopened under the Carrefour or Champion name by the end of the year (January in Italy). > This was a major undertaking since the changes involved more than the name of the store or shelf displays. The changes meant train- ing men and women in new working methods and harmonizing product lines. Inevitably, this effort resulted in some disruption, which explains the year-end drop or slowdown in sales revenue in France and Spain. Sometimes custo- mers could not immediately find products in their usual place, sometimes products were not available in the store for short periods due to system changes. In the first half of 2001, all these stores should steadily return to normal operating conditions. > We plan to continue these changes in other countries. In Belgium, 60 hypermarkets will transfer to the Carrefour trade name by the end of 2001. In France and Spain, we will continue to make progress in pooling logistics, creating synergies over the long term. -

Etn. Fr. COLRUYT NV Publication of a Transparency

PRESS RELEASE – Halle (Belgium), 18/02/2019, 17h45 CET – Regulated information - Transparency notification Etn. Fr. COLRUYT NV Limited liability company Edingensesteenweg 196 – 1500 Halle Enterprise number: 0400.378.485 Publication of a transparency notification (Article 14, first paragraph, of the Law of 2 May 2007 on disclosure of major holdings) Summary of the notification Pursuant to article 14 of the Law of 2 May 2007 on disclosure of major holdings, the Colruyt family and relatives, Colruyt Group and Sofina Group have submitted a notification to the FSMA. This transparency notification dated 15 February 2019 reports the completion of a sale of shares between reference shareholders acting in concert. By virtue of this sale of shares Sofina NV has crossed the threshold of 5% downwards. The shareholders acting in concert Colruyt family and relatives, Colruyt Group and Sofina Group hold a total of 90.955.630 Colruyt shares as per 15 February 2019 and thus jointly represent 63,36% of the total number of shares issued by the company (143.552.090). The company has no knowledge of other agreements between shareholders. The statutory thresholds per bracket of 5% apply. Content of the notification The notification dated 15/02/2019 contains the following information: Reason for the notification: downward crossing of the threshold by persons of the shareholders acting in concert Colruyt family and relatives, Colruyt Group and Sofina Group Notification by: persons acting in concert Person(s) subject to the notification requirement: Stichting Administratiekantoor Cozin, Claude Debussylaan 24, 1085 MD Amsterdam Korys NV, Villalaan 96 – 1500 Halle Korys Business Services I NV, Villalaan 96 – 1500 Halle Korys Business Services II NV, Villalaan 96 – 1500 Halle Korys Business Services III NV, Villalaan 96 – 1500 Halle Korys Investments NV, Villalaan 96 – 1500 Halle Impact Capital NV, Gemeentehuisstraat 6, 3078 Everberg Stiftung Pro Creatura, Oberer Flooz 2579, CH 9620 Lichtensteig Etn. -

85 % Des Entreprises Du Bel20 Vont Verser Des Dividendes

85 % DES ENTREPRISES DU BEL20 VONT VERSER DES DIVIDENDES « LES MARGES SONT LÀ POUR AUGMENTER LES SALAIRES » L’écrasante majorité des entreprises du Bel20 s’apprête à distribuer de juteux dividendes à leurs actionnaires en 2021. Au total, il s’agit d’un montant d’un peu plus de 5 milliards d’euros, selon les chiffres communiqués par les entreprises elles- mêmes. Le service d’étude du PTB a calculé qu’une augmentation salariale de 5 % dans ces entreprises coûterait 1,2 milliard d’euros (voir tableau 1). Soit seulement 25 % des dividendes annoncés. « Cela confirme que dans toute une série de grandes entreprises, il y a de la marge pour augmenter davantage les salaires, constate Raoul Hedebouw, porte-parole du PTB. C’est pourquoi nous exigeons que la loi de 1996 soit modifiée que la norme salariale soit rendue indicative, afin que les travailleurs aient la liberté de négocier de vraies augmentations. » 17 ENTREPRISES DU BEL20 DISTRIBUENT DE GÉNÉREUX DIVIDENDES Selon leurs propres rapports et annonces, la grande majorité des entreprises du Bel20 réalisera des bénéfices et distribuera des dividendes encore cette année. Sur les 19 entreprises qui ont déjà communiqué à ce sujet, 17 annoncent qu’elles verseront des dividendes allant de 34 millions à 1 milliard d’euros. En d’autres mots, au moins 85 % des entreprises du Bel20 verseront des dividendes. Dividende (par Dividende action) proposé (montant total) Nombre d'actions Société du Bel 20 sur base du proposé sur base bénéfice 2020 du bénéfice 2020 AB InBev 0,50 € 1.998.000.000 999.000.000 € Ackermans & van Haaren 2,53 € 33.500.000 84.755.000 € Ageas 2,65 € 198.370.000 525.680.500 € Aperam 1,75 € 83.700.000 146.475.000 € Argen-X 0,00 € 42.760.000 0 € Barco 0,378 € 88.270.000 33.366.060 € Cofinimmo 6,00 € 25.850.000 155.100.000 € Colruyt Group 1,35 € 138.430.000 186.880.500 € Galapagos 0,00 € 64.670.000 0 € GBL 3,03 € 161.360.000 488.920.800 € ING 0,12 € 3.896.730.000 467.607.600 € KBC 0,44 € 416.390.000 183.211.600 € Ontex n.d.