Appendix V Letter from the Market Consultant in Relation to Its Hong Kong Hotel Industry Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

5 Days in HK

5 days in HK Contact us | turipo.com | [email protected] 5 days in HK Our Hong Kong trip plan. Full day by day travel plan for our summer vacaon in Hong Kong. It is hard to visualize unless you’ve been there and experienced the energy that envelops the enre country. Every corner of Hong Kong has something to discover, here are the top aracons and things to do in Hong Kong to consider, our China travel guide. Contact us | turipo.com | [email protected] Day 1 - Hong Kong Park & Victoria Peak Contact us | turipo.com | [email protected] Day 1 - Hong Kong Park & Victoria Peak 1. Hong Kong Park 4. Victoria Peak Duration ~ 2 Hours Duration ~ 1 Hour Mid-level, Hong Kong Victoria Peak, The Peak, Hong Kong Rating: 4.5 Start the day off with an invigorang walk through Hong Kong Park, admiring fountains, landscaping, and even an At the summit, incredible visuals await—especially around aviary before heading towards the Peak Tram, which takes sunset. you to the top of the famous Victoria Peak. WIKIPEDIA Victoria Peak is a mountain in the western half of Hong Kong 2. Hong Kong Zoological And Botanical Gardens Island. It is also known as Mount Ausn, and locally as The Duration ~ 1 Hour Peak. With an elevaon of 552 m, it is the highest mountain on Hong Kong island, ranked 31 in terms of elevaon in the Hong Kong Hong Kong Special Administrave Region. The summit is Rating: 2.9 more.. Nearby the peak Tram Hong Kong Zoological and Botanical Gardens, a free aracon, is also not even 5 minutes away from the Peak Tram. -

Ternational Cooperation Forum Hong Kong, 9-10 December 2015

th 5 EASA International Cooperation Forum Hong Kong, 9-10 December 2015 Practical information The Forum will take place at the Auditorium of Hong Kong Civil Aviation Department Headquarters (HKCAD HQ) on 9th December 2015 (09:00 to 18:00) and 10th December 2015 (09:00 to 16:00). Venue address: Auditorium (1st Floor) Civil Aviation Department Headquarters 1 Tung Fai Road, Hong Kong International Airport Lantau, Hong Kong Transportation from Tung Chung MTR Station and nearby hotels to HKCAD HQ: Taxi: Approximately HKD 40.00 / USD 5.00 Bus Route S1: - Bus fare HKD 3.50 - Location of the bus stop is just a few minutes’ walk from either the Tung Chung MTR station (Exit B) or the Regal Airport Hotel or the Hong Kong SkyCity Marriott Hotel. (Note: The Novotel Citygate Hong Kong Hotel is about 5 minutes’ walk from the Tung Chung MTR station.) The Auditorium is located in the public area of HKCAD HQ and no access pass is required. Delegates please proceed to the Registration Desk on the 1st floor, using an escalator located in the middle of the lobby, for the ICF/5 registration on 9th December 2015, before 09:00 a.m. Welcome tea and coffee will be served starting from 08:15 a.m. on the ground floor. Wi-Fi – please choose "CAD-Guest" network, and, once connected, open the browser and accept "Terms and Conditions" (no password required). Afterwards you can access the internet. Smoking is strictly prohibited in all areas in the HKCAD HQ. Delegates who wish to smoke, please approach the CAD staff for assistance. -

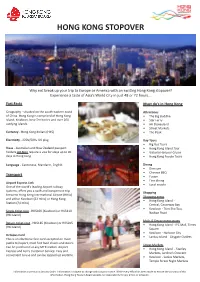

Hong Kong Stopover

HONG KONG STOPOVER Why not break up your trip to Europe or America with an exciting Hong Kong stopover? Experience a taste of Asia’s World City in just 48 or 72 hours... Fast Facts Must do’s in Hong Kong Geography - situated on the south-eastern coast Attractions of China. Hong Kong is comprised of Hong Kong • The Big Buddha Island, Kowloon, New Territories and over 260 • Star Ferry outlying islands. • HK Disneyland • Street Markets Currency - Hong Kong dollars (HK$) • The Peak Electricity - 220V/50Hz UK plug Day Tours • Big Bus Tours Visas - Australian and New Zealand passport • Hong Kong Island Tour holders DO NOT require a visa for stays up to 90 • Victoria Harbour Cruise days in Hong Kong • Hong Kong Foodie Tours Language - Cantonese, Mandarin, English Dining • Dim sum • Chinese BBQ Transport • Fusion • Fine dining Airport Express Link • Local snacks One of the world’s leading Airport railway systems, offers you a swift and inexpensive trip Shopping between Hong Kong International Airport (HKIA) Shopping areas and either Kowloon (22 mins) or Hong Kong • Hong Kong Island - Station (24 mins) Central, Causeway Bay • Kowloon - Tsim Sha Tsui, Single ticket cost - HK$100 (Kowloon) or HK$110 Nathan Road (HK Island) Malls & Department stores Return ticket cost - HK$185 (Kowloon) or HK$205 • Hong Kong Island - IFC Mall, Times (HK Island) Square • Kowloon - Harbour City Octopus Card • Lantau Island - Citygate Outlets This is an electronic fare card accepted on most public transport, most fast food chains and stores. Street Markets Can be purchased at any MTR station, Airport • Hong Kong Island - Stanley Express and Ferry Customer Service. -

Egn201014152134.Ps, Page 29 @ Preflight ( MA-15-6363.Indd )

G.N. 2134 ELECTORAL AFFAIRS COMMISSION (ELECTORAL PROCEDURE) (LEGISLATIVE COUNCIL) REGULATION (Section 28 of the Regulation) LEGISLATIVE COUNCIL BY-ELECTION NOTICE OF DESIGNATION OF POLLING STATIONS AND COUNTING STATIONS Date of By-election: 16 May 2010 Notice is hereby given that the following places are designated to be used as polling stations and counting stations for the Legislative Council By-election to be held on 16 May 2010 for conducting a poll and counting the votes cast in respect of the geographical constituencies named below: Code and Name of Polling Station Geographical Place designated as Polling Station and Counting Station Code Constituency LC1 A0101 Joint Professional Centre Hong Kong Island Unit 1, G/F., The Center, 99 Queen's Road Central, Hong Kong A0102 Hong Kong Park Sports Centre 29 Cotton Tree Drive, Central, Hong Kong A0201 Raimondi College 2 Robinson Road, Mid Levels, Hong Kong A0301 Ying Wa Girls' School 76 Robinson Road, Mid Levels, Hong Kong A0401 St. Joseph's College 7 Kennedy Road, Central, Hong Kong A0402 German Swiss International School 11 Guildford Road, The Peak, Hong Kong A0601 HKYWCA Western District Integrated Social Service Centre Flat A, 1/F, Block 1, Centenary Mansion, 9-15 Victoria Road, Western District, Hong Kong A0701 Smithfield Sports Centre 4/F, Smithfield Municipal Services Building, 12K Smithfield, Kennedy Town, Hong Kong Code and Name of Polling Station Geographical Place designated as Polling Station and Counting Station Code Constituency A0801 Kennedy Town Community Complex (Multi-purpose -

2 March 2016

THE HONGKONG AND SHANGHAI HOTELS, LIMITED 2 March 2016 THE HONGKONG AND SHANGHAI HOTELS, LIMITED CELEBRATES ITS 150th ANNIVERSARY IN 2016 The Hong Kong-based parent company of The Peninsula Hotels, The Peak Tram, Peak Tower and Repulse Bay Complex, celebrates 150 years of tradition well served. HONG KONG 2 March, 2016: The distinguished heritage of The Hongkong and Shanghai Hotels, Limited (HSH) reaches a new milestone today as HSH celebrates its 150th anniversary. Originally incorporated on 2 March 1866 as The Hongkong Hotel Company, Limited, HSH was one of the first companies to be listed on the Hong Kong Stock Exchange and is currently the oldest registered company on the Hong Kong Companies Registry. For a century and a half, the compelling story of HSH has been closely tied to its city of origin, Hong Kong. Whilst evolving to meet the changing times at home and abroad, HSH has never lost respect for its past and its heritage, and it continually strives to emulate the standards of service and style that earned it the accolade of “The Far East’s leading hotel company”. The concept of “Tradition well served” remains fundamental to HSH’s approach. “Tradition is taking account of a wonderful history, but remembering that everybody today looks to the future. It is important not to forget that the future is built on the past, and we have a great legacy,” said The Hon. Sir Michael Kadoorie, Chairman of HSH. “We believe that our rich history gives us a fuller understanding of our shared identity, culture and values, enabling us to manage change responsibly, to safeguard the best of the past and to keep innovating to meet the demands of the next generation.” Today, the HSH legacy encompasses a diverse portfolio of assets worth HK$44.2 billion1 including ten Peninsula Hotels around the world, The Peak Tram, The Peak Tower and The Repulse Bay Complex in Hong Kong. -

Tradition Well Served Well Tradition

TRADITION WELL SERVED TRADITION 2016 1 A LETTER FROM THE CHAIRMAN nniversaries are a time to pause and reflect. As we review The new company, as well as owning hotels in Hong Kong, now our past, it is important to recognise the many milestones had full control over Shanghai’s Astor House and Palace Hotel. that have shaped our company, and to remember the Later additions were The Majestic in Shanghai and the Grand Hotel Aindividuals whose legacies have ensured the beneficial role that we des Wagons-Lits in Peking. have played in Hong Kong’s success story. Plans were soon afoot for a third hotel to be built on the Our history begins in the latter part of the nineteenth century: Kowloon peninsula – at the time a sleepy backwater. Although six years after Kowloon was ceded to Great Britain, and 32 years originally a government project to take advantage of the transport before the New Territories were leased. Sedan chairs and rickshaws links afforded by the railway terminus and the nearby quays of were the transport of the day. Kowloon, it was Taggart’s vision and determination that ensured The 1860s were a period of growing interest in the Far East The Peninsula Hotel, when opened, would become “the finest hotel and, thanks to popular literature at the time, Hong Kong held a east of Suez”. Due to a number of construction challenges, this particular fascination for travellers attracted to the orient. The project was nearly abandoned, but Taggart persisted despite growth of tourism was facilitated by entrepreneurs such as Thomas objections from shareholders who believed any hotel built in Cook who arranged fledging tour services for independent travellers Kowloon would be a “white elephant”. -

Copy of HK Tour Tariff 4

Adult USD86 Tour Ref.: T11-04 Child (3-11 yrs) USD70 360 Lantau Explorer Tour Duration: Approx. 7 hours Daily Morning Departure Hotel pick-up: Approx. 7:50am – 8:25am Lantau Island is one of the best-loved outlying islands in Hong Kong. With the new development of Ngong Ping Cable Car, and the opportunities to see a unique sub-species of the Indo-Pacific Humpback Dolphin, the Island has become a new attraction in Hong Kong. Get close to nature on this tour and explore Tai O, a quaint fishing village where the houses are on stilts, visit the World’s tallest outdoor, seated bronze Buddha statue at the Po Lin Monastery and enjoy a great vegetarian meal there. Cruise Ride on the South China Sea and Dolphin Watching Tour starts with a cruise ride on the South China Sea to see certain outlying islands of Hong Kong and a close-up view on flight departure from Hong Kong International Airport. If you are lucky enough, you can even see the pink dolphins, a unique sub-species of the Indo-Pacific Humpback Dolphin and are known-and loved-for their pink colour. They are also the official mascot of the Hong Kong Special Administrative Region. Tai O Fishing Village Tai O, also known as the “Venice of the East” was once the largest inhabited settlement on Lantau Island. The village’s stilt houses on the waterfront, offer a glimpse into Hong Kong’s past and provide a striking contrast with the modern city. Po Lin Monastery Po Lin Monastery is the most popular Buddhist temple in Hong Kong. -

Information Paper Provided by the Airport Authority Hong Kong

CB(1)730/06-07(04) For information on 22 January 2007 Legislative Council Panel on Economic Services SkyCity Development at the Hong Kong International Airport INTRODUCTION 1. This paper provides an outline of SkyCity development at the Hong Kong International Airport (HKIA), including the new passenger terminal, for the Panel’s information. A presentation will be given at the Panel meeting. REPORT Airport city becoming a global trend 2. The development of ‘airport cities’ and ‘aerotropolis’ (i.e. mega airport city, if reaching certain size) has emerged as a global trend. An airport with its built-in infrastructural connectivity can more readily draw a critical mass. This naturally provides a demand base for commercial development within and beyond the airport boundaries, and thus generates economic spin-off for the interests of the community. 3. Business activities commonly found in airport cities are retail, catering and entertainment facilities at the passenger terminals; logistics and air cargo operations; hotels, offices and convention and exhibition centres; free trade zones and time-sensitive goods processing operations. For places where spines and clusters of airport-linked businesses are set up along the major roads up to 25 kilometres away from the airport, they can be referred to as aerotropolis. Examples of such airport-linked businesses include business parks, industrial estates, wholesale merchandise marts, tourism and entertainment centres and large mixed- use residential developments. The HKIA SkyCity development plan is in line with the airport city concept; Tung Chung and other parts of Lantau seem to have some features of an aerotropolis; and the Pearl River Delta can become a most desirable, greater aerotropolis. -

運 輸 署 TRANSPORT DEPARTMENT SCHEDULE of SERVICE on Tat

運 輸 署 TRANSPORT DEPARTMENT SCHEDULE OF SERVICE On Tat Tour Bus Limited Passenger Service Licence (PSL) Number : 11682A HOTEL SERVICE ROUTE – Hong Kong Skycity Marriott Hotel I. ROUTE ROUTE A Hong Kong Skycity Marriott Hotel – Airport (Circular) via Sky City Road East, Sky City Interchange, Cheong Lin Road, Airport South Interchange, Cheong Lin Road, Cheong Hong Road, Airport Road, Airport South Interchange, Cheong Lin Road, Cheong Tat Road, Airport North Interchange, Sky City Road, Airport Expo Boulevard and Sky City Road East. ROUTE B Hong Kong Skycity Marriott Hotel – Tung Chung Station (Circular) via Sky City Road East, Sky City Interchange, East Coast Road, Scenic Road, Chek Lap Kok South Road, Shun Tung Road, Tat Tung Road, Hing Tung Street general loading/unloading spaces), Tat Tung Road, Shun Tung Road, Chek Lap Kok South Road, Scenic Road, East Coast Road, Sky City Interchange, Sky City Road East and Airport Expo Boulevard. II. STOPPING PLACES ROUTE A 1. Hong Kong Skycity Marriott Hotel 2. Airport Terminal 1 (inner departure kerb outside bus stops) (drop-off only) 3. Coach Station (pick-up only, a valid Travel Industry Vehicle (TIV) Permit is required for access) 4. Hong Kong Skycity Marriott Hotel ROUTE B 1. Hong Kong Skycity Marriott Hotel 2. Tung Chung Station (general loading/unloading spaces at Hing Tung Street) 3. Hong Kong Skycity Marriott Hotel Prior approval has to be obtained from Airport Authority Hong Kong and Hong Kong Skycity Marriott Hotel accordingly III. TIMETABLE ROUTE A Operating hours : 0500 hrs – 0030 hrs of the next day. Frequency : for every 30 minutes ROUTE B Operating hours : 0800 hrs – 2130 hrs. -

The Peninsula

CELEBRATING THE PENINSULA 90 YEARS OF LUXURY HOSPITALITY T H S H, L ANNUAL REPORT 2018 Stock Code: 00045 In this year’s Annual Report we have moved further towards The objective of our approach is to provide a connected view integrated reporting as envisaged by the International of the different aspects of our performance by publishing this Integrated Reporting Council (IIRC – www.theiirc.org). Annual Report and a separate Corporate Responsibility and Sustainability Report to highlight our vision, strategy and our In the IIRC’s words “Integrated Reporting brings together achievements in 2018. Together with our company’s website, material information about an organisation’s strategy, the two reports enable our stakeholders to have a more governance, performance and prospects in a way that reflects informed assessment of our company. the commercial, social and environmental context within which it operates. It provides a clear and concise representation of Our integrated approach encapsulates a number of different how an organisation demonstrates stewardship and how it reference guidelines, including the International Integrated creates and sustains value”. Reporting Framework published by the International Integrated Reporting Council, The Stock Exchange of Hong Kong Limited’s (HKEx) Environmental, Social and Governance Reporting Guide, the Hong Kong Institute of Certifi ed Public Accountants’ (HKICPA) approach on corporate governance disclosure, and the Global Reporting Initiative Sustainability Reporting Guidelines. Our financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting Standards, the requirements of the Hong Kong Companies Ordinance and the applicable disclosure provisions of the Rules Governing the Listing of Securities on HKEx. -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Islands Hong Kong SkyCity Marriott Hotel 11101 North Block 6, Belair Monte 11105 Kowloon City iclub Ma Tau Wai Hotel 11106 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11107 Wan Chai Best Western Hotel Causeway Bay 11108 Kowloon City Metropark Hotel Kowloon 11109 Kwun Tong IW Hotel 11110 Kwai Tsing Dorsett Tsuen Wan Hong Kong 11111 Eastern Ramada Hong Kong Grand View 11112 Kowloon City iclub Ma Tau Wai Hotel 11113 North Block 1, Dawning Views 11114 Islands Block 1, Coastal Skyline 11115 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11116 Central & Western Sing Fai Building 11118 Eastern Hoi Sing Mansion, Taikoo Shing 11120 Eastern Hoi Sing Mansion, Taikoo Shing 11121 Sai Kung Tak On House, Hau Tak Estate 11123 Sham Shui Po 15 Fuk Wing Street 11124 Kowloon City iclub Ma Tau Wai Hotel 11125 Yau Tsim Mong Dorsett Mongkok, Hong Kong 11127 Kwai Tsing Block 1, Regency Park 11128 Central & Western True Light Building 11129 Islands Hong Kong SkyCity Marriott Hotel 11130 Central & Western Yukon Court 11131 Central & Western Bishop Lei International House 11132 Central & Western 40 Conduit Road 11132 Sham Shui Po 15 Fuk Wing Street 11133 Central & Western May Tower I 11134 Kwai Tsing Yat King House, Lai King Estate 11135 Central & Western Yip Cheong Building, -

The Hongkong and Shanghai Hotels Is Celebrating Its 145Th Anniversary in 2011

The Heritage Factor The Hongkong and Shanghai Hotels is celebrating its 145th anniversary in 2011. At the threshold of an era when the world is evolving at a previously unimaginable speed and continuity is challenged by unpredictability, we pause and take time to reflect on our heritage and the attributes which connect us to the past. Above : Sir Elly Kadoorie (middle) and sons. Right : A postcard to a Jewish immigrant in Shanghai in the 1930s (courtesy Peter Nash). 16 T KO HE HONG NG HOTELS, LI TE D AN AI MI 香 港 D SHANGH 公 司 上 海 限 The Heritage Factor 大 酒 店 有 Above : When the Hong Kong Hotel opened in 1868, it was dubbed by the media as “the greatest enterprise of the kind in China and Japan”. Right : The Hong Kong Hotel company debenture in 1909. The Heritage Factor Top : The building that housed the Majestic Hotel Above : The Astor House Hotel today. The building still retains many elements introduced in the in Shanghai was built in 1906. 1920s and continues to provide accommodation for visitors to Shanghai. Above : The Palace Hotel in Shanghai was opened in 1909. The word ‘herit age’ originated from the French language and “The HSH heritage is built on a century-and-a-half of means ‘to inherit’ – to pass on. To us, it is our Company’s tradition, values, experience and passion, as well as the skills legacy. It can be seen, felt and passed from generation to generation of the same owning experienced in every service family and members of staff.” that we provide, through every member of staff and expressed in every product that we deliver.