GCC Market Entry Project Business Plan Implementation Methodology

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Middle Eastern Luxury Sector Is an Ever-Expanding One. Adam Coulter Looks at the Latest Developments

Source: Selling Travel {Main} Edition: Country: UK Date: Tuesday 1, November 2016 Page: 54,55,56 Area: 1440 sq. cm Circulation: Pub Stmt 14925 Monthly Ad data: page rate £3,750.00, scc rate £19.50 Phone: 020 8649 7233 Keyword: Ras Al Khaimah The Middle Eastern luxury sector is an ever-expanding one. Adam Coulter looks at the latest developments remember quite clearly the feeling "dune bashing," as this crazy activity is known Unprecedented growth I had as the Toyota Landcruiser as in the Middle East, but the descriptions don't The United Arab Emirates, Qatar and I reached the top of the near-vertical do it justice; nor the thrill of hurtling down Oman lie seven to seven-and-a-half-hour sand dune we'd been driving up. a sand dune,your life in the driver's hands. flight time from the UK, and are served My stomach dropped as I looked down this We spent the afternoon in the deserts just by a number of direct daily flights. vast dune and even though I knew I was in safe outside of Dubai, urging Mohamed up ever- The UAE comprises seven emirates - hands, with an experienced driver, I felt terrified. higher dunes and thrilling at the drop once Dubai and Abu Dhabi being the best known, The car paused, Mohamed turned to me and we'd reached the top. It's also good to get out with Ras al Khaimah up-and-coming; said: "Ready?" I gulped and whispered: "Yes." of town for a few days; much as I love Dubai Oman and Qatar are separate states. -

كتاب-الاحصاء-السنوي-الكهرباء-Compressed.Pdf

;jÁÊ“’\;Ï’ÂÄ State Of Kuwait ;ÍÊfiâ ’\;Ô]ë t¸\;g ]i— 2 0 2 0 ;ÎÄÅq i∏\;ÏÕ] ’\Â;Ô]∏\Â;Ô]dÖ‚“ ’\;ÎÑ\Ü ;ÄŬ’\;C;ÏË]dÖ‚“ ’\;ÏÕ] ’\;D 4 4 ” ; W ^ اﻟﻄﺎﻗﺔ اﻟﻜﻬﺮﺑﺎﺋﻴﺔ Electrical Energy Electricity & W ater & Renew able Energy f ;ÍÊfiâ’\;Ô]ët¸\;g]i— Statistical Year Book ;k]ŸÊ÷¬∏\;á—ÖŸÂ;Ô]ët¸\;ÎÑ\Äb;U;ÉË fihÂ;Ä\Å¡b M instry O 2021;U;Ñ\Åêb Statistical Year 2020 ( Electrical Energy ) Edition 44 “A” ;€ËtÖ’\;˛fl∂Ö’\;˛!\;€âd ;ÿ˛Ü]fi˛Ÿ;˛‰ˇÑ˛ÅÕ˛Â;\˛ÑÊ›;ˇÖ˛⁄˛Œ˛’\Â;˛Ô]˲î;ä˛⁄ç’\;◊˛¬˛p;Ͳɒ\;Ê˛·;Dˇ ’˛b;”˛’Ç;ٰ˛!\;ˇœ˛÷˛|;]˛Ÿ;˛ۚ;g]˛â˛¢\Â;˛Ø˛fiâ’\;Ä˛Å˛¡;\Ê˛⁄ˇ÷˛¬iˆ; C;;‡Ê˛⁄ˇ÷˛¬Á;˛‹ÊŒ˛’;k]Á˛˙\;◊ˇë ˛Á;ˇۚ;œ¢]˛d; ;C5D;ÏÁ˙\;U;ä›ÊÁ;ÎÑÊà ;ÓÅ ∏\;Ęe’\;3Ÿ^;Ê⁄â’\;ft]ê;ÎÖït @Åbjó€a@ãibßa@áº˛a@“aÏ„@ÑÓì€a ;jÁÊ“’\;Ï’ÂÄ;3Ÿ^ H.H Sheikh Nawaf Al-Ahmed Al-Jaber Al-Sabah The Amir of the State of Kuwait @Åbjó€a@ãibßa@áº˛a@›»ìfl@ÑÓì€a@Ï8 ;jÁÊ“’\;Ï’ÂÄ;Å‚¡;È’Â H.H Sheikh Mishal Al-Ahmed Al-Jaber Al-Sabah The Crown Prince of the State of Kuwait تقديم تعمل وزارة الكهرباء واملاء جاهدةً على املشاركة يف حتقيق رؤية 2035 التنموية يف جمال توليد الطاقة الكهربائية وحتلية املياه ، ومن اجلهود الواضحة يف هذا اجملال إدخال تكنولوجيا الطاقة البديلة )املتجددة( تدرجيياً للعمل جنباً إىل جنب مع مصادر الطاقة اﻷخرى . إن اهلدف املخطط له من قِبل الوزارة ضمن رؤية 2035 هو الوصول بإنتاج الطاقة الكهربائيةة البديلة إىل ما نسبته 15% من حاجة البﻻد الكلية من الطاقة الكهربائية وحتقيق اﻷمن املائي ، وذلك من خﻻل حتفيز برنامج الشراكة بني القطاعني العام واخلاص يف تنفيذ بعض مشاريع الطاقة الكهربائية وحتلية املياه . -

Urban Megaprojects-Based Approach in Urban Planning: from Isolated Objects to Shaping the City the Case of Dubai

Université de Liège Faculty of Applied Sciences Urban Megaprojects-based Approach in Urban Planning: From Isolated Objects to Shaping the City The Case of Dubai PHD Thesis Dissertation Presented by Oula AOUN Submission Date: March 2016 Thesis Director: Jacques TELLER, Professor, Université de Liège Jury: Mario COOLS, Professor, Université de Liège Bernard DECLEVE, Professor, Université Catholique de Louvain Robert SALIBA, Professor, American University of Beirut Eric VERDEIL, Researcher, Université Paris-Est CNRS Kevin WARD, Professor, University of Manchester ii To Henry iii iv ACKNOWLEDGMENTS My acknowledgments go first to Professor Jacques Teller, for his support and guidance. I was very lucky during these years to have you as a thesis director. Your assistance was very enlightening and is greatly appreciated. Thank you for your daily comments and help, and most of all thank you for your friendship, and your support to my little family. I would like also to thank the members of my thesis committee, Dr Eric Verdeil and Professor Bernard Declève, for guiding me during these last four years. Thank you for taking so much interest in my research work, for your encouragement and valuable comments, and thank you as well for all the travel you undertook for those committee meetings. This research owes a lot to Université de Liège, and the Non-Fria grant that I was very lucky to have. Without this funding, this research work, and my trips to UAE, would not have been possible. My acknowledgments go also to Université de Liège for funding several travels giving me the chance to participate in many international seminars and conferences. -

Kuwaittimes 1-8-2019 Copy.Qxp Layout 1

THULHIJJA 3, 1440 AH SUNDAY, AUGUST 4, 2019 28 Pages Max 47º Min 31º 150 Fils Established 1961 ISSUE NO: 17899 The First Daily in the Arabian Gulf www.kuwaittimes.net Scientific Center expansion to Thousands flee Kashmir Demise of US-Russia nuclear Mbappe magic, Di Maria free kick 4 advance knowledge, science 6 after ‘terror’ warning 24 treaty fuels fears of arms race 28 help PSG claim Champions Trophy Iraq ‘identifies’ remains of 32 Kuwaitis found in mass grave Kuwait cautious, says more tests needed to determine their identity BAGHDAD/KUWAIT: The Iraqi for- Hussein. Iraq will spare no effort for eign ministry declared on Friday “identi- determining the fate of the other missing Kuwait, Iraq sign contract to exploit shared oilfields fying” remains of 32 Kuwaiti prisoners Kuwaitis and “what has been discovered who were found in a mass grave in South recently depicts continuation of the AMMAN: Kuwait and Iraq signed in the Iraq months ago. The ministry efforts that has led to information about Jordanian capital a contract for conducting a spokesperson, Ahmad Al-Sahaf, said in a the remains”, he said. technical study for joint frontier oilfields. Both statement that the “Iraqi technical team But Kuwaiti Assistant Foreign neighboring countries picked British energy tasked with the file of the missing Minister for International Organizations advisory firm ERC Equipoise (ERCE) to deter- Kuwaitis and prisoners was able, in Nasser Al-Hayyen said later on Friday mine the optimal way to invest into and tap cooperation with the Red Cross, to that more examinations are required to their shared oilfields. -

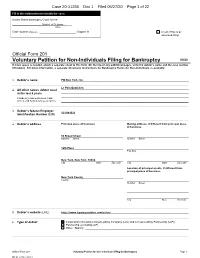

Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If More Space Is Needed, Attach a Separate Sheet to This Form

Case 20-11266 Doc 1 Filed 05/27/20 Page 1 of 22 Fill in this information to identify the case: United States Bankruptcy Court for the: ____________________ District of Delaware (State) Case number (If known): _________________________ Chapter 11 Check if this is an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor’s name and the case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available 1. Debtor’s name PQ New York, Inc. Le Pain Quotidien 2. All other names debtor used in the last 8 years Include any assumed names, trade names, and doing business as names 3. Debtor’s federal Employer 13-3841022 Identification Number (EIN) 4. Debtor’s address Principal place of business Mailing address, if different from principal place of business 50 Broad Street Number Street Number Street 12th Floor P.O. Box New York, New York 10004 City State Zip Code City State Zip Code Location of principal assets, if different from principal place of business New York County County Number Street City State Zip Code 5. Debtor’s website (URL) https://www.lepainquotidien.com/us/en/ 6. Type of debtor Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) Partnership (excluding LLP) Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy Page 1 RLF1 22931188v.9 Debtor PQ New York, Inc. -

Retail Market Snapshot

MENA RETAIL MARKET SNAPSHOT 2013 Accelerating success. RETAIL MARKET SNAPSHOT | 2013 | MENA | INTRODUCTION INTRODUCTION • The MENA region is categorised by two very diversified groups in 482 offices in terms of income and population; 62 countries on o The Arabian Gulf (GCC) countries, enjoy some of the highest per 6 continents capita levels in the world with small population bases, and supported by the registered growth in their oil-based economies. United States: 140 Canada: 42 o Conversely, there are other neighbouring countries in the region, Latin America: 20 some of which have undergone recent regime change, that are Asia Pacific: 195 characterised by a large population base, low GDP per capita and EMEA: 85 significant segments of the population living below the poverty line. • $2.0 billion in revenue • In this report, we take a quick snapshot of the following retail markets; • More than 13,500 employees • 5,100 brokers o Dubai. • $71 billion in transaction volume across more than 78,000 sale and lease transactions o Abu Dhabi. • 1.1 billion square feet under management o Cairo. SERVICES OFFERED BY COLLIERS o Muscat. INTERNATIONAL o Doha. • Retail Development Consultancy. • Retail Zoning & Mix Strategy. o Riyadh. • Tenant Coordination. o Jeddah. • Retail Leasing Services. • These markets have been acknowledged as the most active and • Property Management. promising across the region, in accordance with the existing dynamics pertaining to the Retail Demand Drivers. • Project Management. • Strategic & Business Planning. RETAIL DEMAND DRIVERS • Economic Impact Studies. The profitability of any retail offering is highly dependant on the level • • Market & Competitive Studies. of demand for retail space in the targeted market. -

Dubai Crown Prince Opens Al Ghubaiba Bus Station Vision

Issue No. 149 November 2020 Dubai Crown Prince opens Al Ghubaiba Bus Station Vision The world leader in seamless & sustainable mobility. Mission Develop & manage integrated and sustainable roads & transportation systems at a world-class level, and provide pioneered services to all stakeholders for their happiness, and support Dubai’s vision through shaping the future, developing policies and legislations, adopting technologies, innovations & world-class practices and standards. 2 Revamping Mobility The fast pace of technology and industrial connected, RTA embarked on a master plan for advancements triggered by the 4th Industrial shared and flexible transport. It covered non- Revolution, and the spiral demographic growth conventional mobility means such as shared of key metropolitan cities have brought on bikes, cars, scooters and buses on-demand. new challenges. Governments have to revise Other mobility means loom on the horizon such the basics of urban-planning and plans for as autonomous and individual mobility means. roads and transport infrastructure to cope with RTA currently offers Hala e-hailing service in future trends. partnership with Careem, and bike share (Careem “Smooth mobility and connected communities Bike) service encompassing 780 bikes at 78 have now become core standards of classifying docking stations. It has just started the trial run of future cities. We endeavour to deliver a global e-scooter at five areas, and deployed 13 buses on- model by delivering state of the art advanced demand at five different locations in Dubai. RTA and sustainable infrastructure projects. The is also committed to supporting youth and local smooth mobility and connected communities start-ups and offer them suitable opportunities. -

Fear and Money in Dubai

metropolitan disorders The hectic pace of capitalist development over the past decades has taken tangible form in the transformation of the world’s cities: the epic expansion of coastal China, deindustrialization and suburbanization of the imperial heartlands, massive growth of slums. From Shanghai to São Paolo, Jerusalem to Kinshasa, cityscapes have been destroyed and remade—vertically: the soar- ing towers of finance capital’s dominance—and horizontally: the sprawling shanty-towns that shelter a vast new informal proletariat, and McMansions of a sunbelt middle class. The run-down public housing and infrastuctural projects of state-developmentalism stand as relics from another age. Against this backdrop, the field of urban studies has become one of the most dynamic areas of the social sciences, inspiring innovative contributions from the surrounding disciplines of architecture, anthropology, economics. Yet in comparison to the classic accounts of manufacturing Manchester, Second Empire Paris or Reaganite Los Angeles, much of this work is strikingly depoliticized. Characteristically, city spaces are studied in abstraction from their national contexts. The wielders of economic power and social coercion remain anonymous. The broader political narrative of a city’s metamorphosis goes untold. There are, of course, notable counter-examples. With this issue, NLR begins a series of city case studies, focusing on particular outcomes of capitalist globalization through the lens of urban change. We begin with Mike Davis’s portrait of Dubai—an extreme concentration of petrodollar wealth and Arab- world contradiction. Future issues will carry reports from Brazil, South Africa, India, gang-torn Central America, old and new Europe, Bush-era America and the vertiginous Far East. -

LAPPEENRANNAN-LAHDEN TEKNILLINEN YLIOPISTO LUT School of Engineering Science Industrial Engineering and Management Global Management of Innovation and Technology

LAPPEENRANNAN-LAHDEN TEKNILLINEN YLIOPISTO LUT School of Engineering Science Industrial Engineering and Management Global Management of Innovation and Technology Sofia Savelainen Implementation of SASO certifications and import procedures in mining projects in Saudi Arabia Master’s Thesis 1st Supervisor Associate Professor Lea Hannola 2nd Supervisor Professor Ville Ojanen ABSTRACT Author: Sofia Savelainen Subject: Implementation of SASO certifications and import procedures in mining projects in Saudi Arabia Year: 2020 Place: Espoo, Finland Master’s thesis. Lappeenranta-Lahti University of Technology, School of Engineering Science, Industrial Engineering and Management. 118 pages, 31 figures, 13 tables and 10 appendices. Examiners: Associate Professor Lea Hannola and Professor Ville Ojanen Keywords: SASO, certification, Saudi Arabia, mining project, import challenges The Kingdom of Saudi Arabia has an own import certification system, which includes SASO certificates. SASO certificates are mandatory import certificates for all regulated goods. In 2019, certification application process, document submission and new online platform changed how certifications are managed from importer’s perspective. SASO certificates being the inevitable part of export mining projects, understanding the system and implementing certificates correctly are very vital in terms of project success. This qualitative study studies how SASO certifications are implemented into mining projects in Saudi Arabia, how SASO certifications and import requirements must be considered in mining projects as well as what are the challenges related to SASO certifications and Saudi Arabian import. Selected research methods are literature review and semi-structured interviews. The study reveals that preliminary planning is vital regarding SASO certificates. In Saudi Arabia, there is a possibility to get duty exemption, which is highly recommended to utilize because granted duty exemption removes the need of SASO certificates. -

Leasing Projects Portfolio Leased Projects

Leasing Projects Portfolio Leased Projects # Project Units Developer Location GLA (Sqft) Opening Date 1 Mall of Qatar 450 Urbacon Gen Contracting Doha, Qatar 2,100,000 Open 2 The Onyx 50 Ishraqah for Dev Ltd. Dubai, UAE 120,000 Open 3 Palms Mall 75 Energy City Qatar Doha, Qatar 85,000 Open 4 Ocean Shopping Mall 25 Mustafa Sultan Ent. Qurum, Oman 55,000 Open 5 Muzn Mall 75 Majan Dev Muscat, Oman 140,000 Open 6 Jasmine Complex 50 Taameer Invest. Muscat Oman 55,000 Open 7 Rivette 50 Al Ahly Real Estate Dev Alexandria, Egypt 40,000 Open 8 I Mall 50 Nice home Real estate Sharjah, UAE 65,000 Open 9 Capital Mall 170 Manazel Real Estate Abu Dhabi, UAE 710,000 Open 10 Citylife Al Tallah 67 R Select Holding Ajman, UAE 140,000 Open 11 Citylife Al Khor 40 R Select Holding Ajman, UAE 120,000 Open 12 Juffair Square 38 MARF Inv & Prop Mgmt Manama, Bahrain 95,000 Q1, 2020 Total 1,140 Total 3,725,000 2 Mall of Qatar 3 Projects Currently under Leasing # Project Units Developer Location GLA (Sqft) Opening Date 1 Cityland Mall 350 Cityland RE Dev. Dubai, UAE 1,150,000 Open Akoya Oxygen 2 37 Damac Dubai, UAE 80,200 Q1, 2020 Community Centre 3 Manar Mall 155 HRED RAK, UAE 660,000 Open 4 Hamra Mall 130 HRED RAK, UAE 300,000 Open 5 Omniyat, SZ 21 13 Omniyat Dubai, UAE 55,000 Q2, 2020 6 The Opus 11 Omniyat Dubai , UAE 55,000 Q2, 2020 7 Galleria @ Nation Towers 60 ICT Abu Dhabi, UAE 220,000 Open 8 The Collection @ St. -

IN the UNITED STATES BANKRUPTCY COURT for the DISTRICT of DELAWARE in Re

Case 20-11266 Doc 3 Filed 05/27/20 Page 1 of 15 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE _________________________________________ ) In re: ) Chapter 11 ) PQ New York, Inc., et al.,1 ) Case No. 20-[●] ([●]) ) ) (Joint Administration Requested) Debtors. ) _________________________________________ ) DECLARATION OF STEVEN J. FLEMING IN SUPPORT OF DEBTORS’ CHAPTER 11 PETITIONS AND FIRST DAY MOTIONS Under 28 U.S.C. § 1764, I, Steven J. Fleming, declare as follows under penalty of perjury: 1. I am the proposed Chief Restructuring Officer (“CRO”) of PQ New York, Inc. (“PQ NY”), a Delaware corporation, and its affiliates (collectively the “Debtors”) in the above- captioned chapter 11 cases (the “Chapter 11 Cases”). I am authorized to submit this declaration (the “First Day Declaration”) on behalf of the Debtors. 2. I am a Principal of PricewaterhouseCoopers LLP (“PwC”), an experienced, leading, full-service financial services, consulting, and accounting firm with over seventy-five (75) offices and more than 50,000 employees in the United States. I am the leader of the firm’s U.S. Business Recovery Services Practice, a position that I have held since 2016 after being a senior member in the group for seven years. Prior to these positions, I held a senior position in PwC’s Transaction Services practice in Dubai, UAE, where I was responsible for expanding the firm’s Corporate Finance and Valuation practices across the Middle East and North Africa. I have been 1 The last four digits of PQ New York, Inc.’s federal tax identification number are 1022. The mailing address for the debtors is 50 Broad Street, New York, New York 10004. -

Hotel Intelligence Dubai

Hotels & Hospitality Group | May 2014 Hotel Intelligence Dubai 2 Hotel Intelligence: Dubai Table of Contents Contributors Market Snapshot 3 Sumati Murari Associate Dubai Continuous growth in hotel guest arrivals 4 [email protected] Passenger arrivals continue to rise 6 Dubai’s ambition vision for tourism 2020 6 Market preference for upscale accommodation 7 Rahul Kamalapurkar Analyst Dubai Expanding pipeline due to market recovery 8 [email protected] Hotel performance recovers after economic 11 downturn Hotel performance to remain strong 12 Jessica Jahns Head of Pan-EMEA Research [email protected] Alexander French Pan-EMEA Research Assistant [email protected] JLL’s Hotels & Hospitality Group serves as the hospitality industry’s global leader in real estate services for luxury, upscale, select service and budget hotels; timeshare and fractional ownership properties; convention centres; mixed-use developments and other hospitality properties. The firm’s 300 dedicated hotel and hospitality experts partner with investors and owner/operators around the globe to support and shape investment strategies that deliver maximum value throughout the entire lifecycle of an asset. In the last five years, the team completed more transactions than any other hotels and hospitality real estate advisor in the world totalling nearly USD 36 billion, while also completing approximately 4,000 advisory, valuation and asset management assignments. The group’s hotels and hospitality specialists provide independent and expert advice to clients, backed by industry-leading research. For more news, videos and research from JLL’s Hotels & Hospitality Group, please visit: www.jll.com/hospitality or download the Hotels & Hospi- tality Group’s iPhone app or iPad app from the App Store.