Berkeley Group Holdings Plc (BKG:LN)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Documento Che Attesta La Proprietà Di Una Quota Del Cap- Itale Sociale È Il Titolo Azionario E Garantisce Una Serie Di Diritti Al Titolare

Università degli Studi di Padova Facoltà di Scienze Statistiche Corso di Laurea Specialistica in Scienze Statistiche, Economiche, Finanziarie e Aziendali Tesi di Laurea : PORTFOLIO MANAGEMENT : PERFORMANCE MEASUREMENT AND FEATURE-BASED CLUSTRERING IN ASSET ALLOCATION Laureando: Nono Simplice Aimé Relatore: Prof. Caporin Massimiliano Anno accademico 2009-2010 1 A Luise Geouego e a tutta la mia famiglia. 2 Abstract This thesis analyses the possible effects of feature-based clustering (using information extracted from asset time series) in asset allocation. In particu- lar, at first, it considers the creation of asset clusters using a matrix of input data which contains some performance measure. Some of these are choosen between the classical measures, while others between the most sofisticated ones. Secondly, it statistically compares the asset allocation results obtained from data-driven groups (obtained by clustering) and a-priori classifications based on assets industrial sector. It also controls how these results can change over time. Sommario Questa tesi si propone di esaminare l’eventuale effetto di una classificazione dei titoli nei portafogli basata su informazioni contenute nelle loro serie storiche In particolare, si tratta di produrre inizialmente una suddivisione dei titoli in gruppi attraverso una cluster analysis, avendo come matrice di input alcune misure di performance selezionate fra quelle classiche e quelle più sofisticate e in un secondo momento, di confrontare i risultati con quelli ottenuti operando una diversificazione dei titoli in macrosettori industriali; infine di analizzare come i risultati ottenuti variano nel tempo. Indice 1 Asset Allocation 7 1.1 Introduzione . 7 1.2 Introduzione alle azioni . 8 1.3 Criterio Rischio-Rendimento . -

Taylor Woodrow Plc Report and Accounts 2006 Our Aim Is to Be the Homebuilder of Choice

Taylor Woodrow plc Report and Accounts 2006 Our aim is to be the homebuilder of choice. Our primary business is the development of sustainable communities of high-quality homes in selected markets in the UK, North America, Spain and Gibraltar. We seek to add shareholder value through the achievement of profitable growth and effective capital management. Contents 01 Group Financial Highlights 54 Consolidated Cash Flow 02 Chairman’s Statement Statement 05 Chief Executive’s Review 55 Notes to the Consolidated 28 Board of Directors Financial Statements 30 Report of the Directors 79 Independent Auditors’ Report 33 Corporate Governance Statement 80 Accounting Policies 37 Directors’ Remuneration Report 81 Company Balance Sheet 46 Directors’ Responsibilities 82 Notes to the Company Financial Statement Statements 47 Independent Auditors’ Report 87 Particulars of Principal Subsidiary 48 Accounting Policies Undertakings 51 Consolidated Income Statement 88 Five Year Review 52 Consolidated Statement of 90 Shareholder Facilities Recognised Income and Expense 92 Principal Taylor Woodrow Offices 53 Consolidated Balance Sheet Group Financial Highlights • Group revenues £3.68bn (2005: £3.56bn) • Housing profit from operations* £469m (2005: £456m) • Profit before tax £406m (2005: £411m) • Basic earnings per share 50.5 pence (2005: 50.6 pence) • Full year dividend 14.75 pence (2005: 13.4 pence) • Net gearing 18.6 per cent (2005: 23.7 per cent) • Equity shareholders’ funds per share 364.7 pence (2005: 338.4 pence) Profit before tax £m 2006 405.6 2005 411.0 2004 403.9 Full year dividend pence (Represents interim dividends declared and paid and final dividend for the year as declared by the Board) 2006 14.75 2005 13.4 2004 11.1 Equity shareholders’ funds per share pence 2006 364.7 2005 338.4 2004 303.8 * Profit from operations is before joint ventures’ interest and tax (see Note 3, page 56). -

Disclaimer Strictly Not to Be Forwarded to Any

DISCLAIMER STRICTLY NOT TO BE FORWARDED TO ANY OTHER PERSONS IMPORTANT: You must read the following disclaimer before reading, accessing or making any other use of the attached document relating to SEGRO plc (the “Company”) dated 10 March 2017. In accessing the attached document, you agree to be bound by the following terms and conditions, including any modifications to them from time to time, each time you receive any information from us as a result of such access. You acknowledge that this electronic transmission and the delivery of the attached document is confidential and intended for you only and you agree you will not forward, reproduce, copy, download or publish this electronic transmission or the attached document (electronically or otherwise) to any other person. The attached document has been prepared solely in connection with the proposed rights issue and offering of nil paid rights, fully paid rights and new ordinary shares (the “Securities”) of the Company (the “Transaction”). The Prospectus has been published in connection with the admission of the Securities to the Official List of the UK Financial Conduct Authority (the ‘‘Financial Conduct Authority’’) and to trading on the London Stock Exchange plc’s main market for listed securities (together, ‘‘Admission’’). The Prospectus has been approved by the Financial Conduct Authority as a prospectus prepared in accordance with the Prospectus Rules made under section 73A of the Financial Services and Markets Act 2000, as amended. NOTHING IN THIS ELECTRONIC TRANSMISSION AND THE ATTACHED DOCUMENT CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. -

The Taylor Wimpey Difference

Annual Report and Accounts 2019 Difference The Taylor Wimpey Taylor Wimpey plc Annual Report and Accounts 2019 www.taylorwimpey.co.uk Taylor Wimpey plc is a customer-focused residential developer building and delivering homes and communities across the UK and in Spain. Our Company purpose is to deliver new homes within thriving communities, in a safe and environmentally responsible manner, with customers at the heart of our decision making and consideration of the potential impact on wider stakeholders. Contents Strategic report Financial statements Connect with us 1 The Taylor Wimpey difference 140 Independent auditor’s report There are several ways you can get in 12 Investment case 148 Consolidated income statement touch with us or follow our news. 14 Chair’s statement 149 Consolidated statement of www.taylorwimpey.co.uk/corporate 17 Group Management Team Q&A comprehensive income 18 UK market review 150 Consolidated balance sheet www.twitter.com/taylorwimpeyplc 22 Chief Executive’s letter 151 Consolidated statement of changes in equity 24 Our strategy and www.linkedin.com/company/taylor-wimpey key performance indicators 152 Consolidated cash flow statement 30 Our business model 153 Notes to the consolidated financial statements 32 Making a difference for our stakeholders Navigating this report 183 Company balance sheet 44 Non-financial information statement The icons below help to signpost where you 184 Company statement of changes 45 Our approach to identifying and can find more information. in equity managing risk 185 Notes to the -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Post-Modern Portfolio Theory Supports Diversification in an Investment Portfolio to Measure Investment's Performance

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Rasiah, Devinaga Article Post-modern portfolio theory supports diversification in an investment portfolio to measure investment's performance Journal of Finance and Investment Analysis Provided in Cooperation with: Scienpress Ltd, London Suggested Citation: Rasiah, Devinaga (2012) : Post-modern portfolio theory supports diversification in an investment portfolio to measure investment's performance, Journal of Finance and Investment Analysis, ISSN 2241-0996, International Scientific Press, Vol. 1, Iss. 1, pp. 69-91 This Version is available at: http://hdl.handle.net/10419/58003 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend -

307439 Ferdig Master Thesis

Master's Thesis Using Derivatives And Structured Products To Enhance Investment Performance In A Low-Yielding Environment - COPENHAGEN BUSINESS SCHOOL - MSc Finance And Investments Maria Gjelsvik Berg P˚al-AndreasIversen Supervisor: Søren Plesner Date Of Submission: 28.04.2017 Characters (Ink. Space): 189.349 Pages: 114 ABSTRACT This paper provides an investigation of retail investors' possibility to enhance their investment performance in a low-yielding environment by using derivatives. The current low-yielding financial market makes safe investments in traditional vehicles, such as money market funds and safe bonds, close to zero- or even negative-yielding. Some retail investors are therefore in need of alternative investment vehicles that can enhance their performance. By conducting Monte Carlo simulations and difference in mean testing, we test for enhancement in performance for investors using option strategies, relative to investors investing in the S&P 500 index. This paper contributes to previous papers by emphasizing the downside risk and asymmetry in return distributions to a larger extent. We find several option strategies to outperform the benchmark, implying that performance enhancement is achievable by trading derivatives. The result is however strongly dependent on the investors' ability to choose the right option strategy, both in terms of correctly anticipated market movements and the net premium received or paid to enter the strategy. 1 Contents Chapter 1 - Introduction4 Problem Statement................................6 Methodology...................................7 Limitations....................................7 Literature Review.................................8 Structure..................................... 12 Chapter 2 - Theory 14 Low-Yielding Environment............................ 14 How Are People Affected By A Low-Yield Environment?........ 16 Low-Yield Environment's Impact On The Stock Market........ -

Securitization & Hedge Funds

SECURITIZATION & HEDGE FUNDS: COLLATERALIZED FUND OBLIGATIONS SECURITIZATION & HEDGE FUNDS: CREATING A MORE EFFICIENT MARKET BY CLARK CHENG, CFA Intangis Funds AUGUST 6, 2002 INTANGIS PAGE 1 SECURITIZATION & HEDGE FUNDS: COLLATERALIZED FUND OBLIGATIONS TABLE OF CONTENTS INTRODUCTION........................................................................................................................................ 3 PROBLEM.................................................................................................................................................... 4 SOLUTION................................................................................................................................................... 5 SECURITIZATION..................................................................................................................................... 5 CASH-FLOW TRANSACTIONS............................................................................................................... 6 MARKET VALUE TRANSACTIONS.......................................................................................................8 ARBITRAGE................................................................................................................................................ 8 FINANCIAL ENGINEERING.................................................................................................................... 8 TRANSPARENCY...................................................................................................................................... -

Risk and Return Comparison of MBS, REIT and Non-REIT Etfs

International Journal of Business, Humanities and Technology Vol. 7, No. 3, September 2017 Risk and Return Comparison of MBS, REIT and Non-REIT Etfs Hamid Falatoon Ph.D Faculty at School of Business University of Redlands Redlands, CA 92373, USA Mohammad R. Safarzadeh Economics California State PolytechnicUniversity Pomona, CA, USA Abstract MBS has become an investment instrument ofchoice for retiring individuals and the ones who have preference for a secure stream of returns while taking lower risk relative to other vehicles of investment. As well, MBS has lately become a recommended investment strategy by financial advisers and investment bankers for safeguarding the retirement accounts of retirees from wild market fluctuations. The objective of this paper is to compare the risk and return of MBS with REIT and Non-REIT invetment opportunities. The paper uses finance ratios such as Sharpe, Sortino, and Traynor ratios as well as market risk and value at risk (VaR) analysis to compare and contrast the relative risk and return of a number equities in MBS, REIT and Non-REIT. The study extends the analysis to pre-recession of 2007-2009 to analyze the effect of the great recession on the relative risk and return of three diffrerent mediums of investment. Keywords: Risk and Return, MBS, REIT, Sharpe, Sortino, Treynor, VaR, CAPM I. Introduction Mortgage-backed securities (MBS) are debt obligations that represent claims to the cash flows from a pool of commercial and residential mortgage loans. The mortgage loans, purchased from banks, mortgage companies, and other originators are securitized by a governmental, quasi-governmental, or private entity. -

Building Excellence

Barratt Developments PLC Building excellence Annual Report and Accounts 2017 Annual Report and Accounts 2017 Inside this report 1 45 113 175 Strategic Report Governance Financial Statements Other Information 1 Key highlights 46 The Board 114 Independent Auditor’s Report 175 KPI definitions and why we measure 2 A snapshot of our business 48 Corporate governance report 119 Consolidated Income Statement 176 Glossary 4 Our performance and financial highlights 60 Nomination Committee report 119 Statement of Comprehensive Income 177 Other Information 6 How we create and preserve value 65 Audit Committee report 120 Statement of Changes in 8 Chairman’s statement 74 Safety, Health and Environment Shareholders’ Equity – Group 10 Key aspects of our market Committee report 121 Statement of Changes in 76 Remuneration report Shareholders’ Equity – Company 12 Chief Executive’s statement Notice regarding limitations on Directors’ liability under 106 Other statutory disclosures 122 Balance Sheets English law 17 Our Strategic priorities Under the Companies Act 2006, a safe harbour limits the 112 Statement of Directors’ 123 Cash Flow Statements liability of Directors in respect of statements in, and omissions from, the Strategic Report contained on pages 1 to 44 and the Our principles Responsibilities 124 Notes to the Financial Statements Directors’ Report contained on pages 45 to 112. Under English Law the Directors would be liable to the Company (but not to 34 Keeping people safe any third party) if the Strategic Report and/or the Directors’ Report contains errors as a result of recklessness or knowing 35 Being a trusted partner misstatement or dishonest concealment of a material fact, 36 Building strong but would not otherwise be liable. -

Organisations/Groups on the Consultation Database Planning

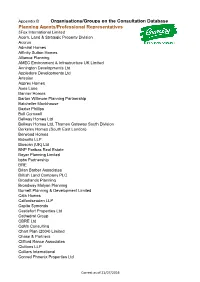

Appendix B Organisations/Groups on the Consultation Database Planning Agents/Professional Representatives 3Fox International Limited Acorn, Land & Strategic Property Division Acorus Admiral Homes Affinity Sutton Homes Alliance Planning AMEC Environment & Infrastructure UK Limited Annington Developments Ltd Appledore Developments Ltd Artesian Asprey Homes Axes Lane Banner Homes Barton Willmore Planning Partnership Batcheller Monkhouse Baxter Phillips Bell Cornwell Bellway Homes Ltd Bellway Homes Ltd, Thames Gateway South Division Berkeley Homes (South East London) Berwood Homes Bidwells LLP Bioscan (UK) Ltd BNP Paribas Real Estate Boyer Planning Limited bptw Partnership BRE Brian Barber Associates British Land Company PLC Broadlands Planning Broadway Malyan Planning Burnett Planning & Development Limited Cala Homes Calfordseaden LLP Capita Symonds Castlefort Properties Ltd Cathedral Group CBRE Ltd CgMs Consulting Chart Plan (2004) Limited Chase & Partners Clifford Rance Associates Cluttons LLP Colliers International Conrad Phoenix Properties Ltd Correct as of 21/07/2016 Conrad Ritblat Erdman Co-Operative Group Ltd., Countryside Strategic Projects plc Cranbrook Home Extensions Crest Nicholson Eastern Crest Strategic Projectsl Ltd Croudace D & M Planning Daniel Watney LLP Deloitte Real Estate DHA Planning Direct Build Services Limited DLA Town Planning Ltd dp9 DPDS Consulting Group Drivers Jonas Deloitte Dron & Wright DTZ Edwards Covell Architecture & Planning Fairclough Homes Fairview Estates (Housing) Ltd Firstplan FirstPlus Planning Limited -

Driving Sustainability in New Homes: a Resource for Local Authorities VERSION 1.1: July 2018

Driving sustainability in new homes: a resource for local authorities VERSION 1.1: July 2018 (Version 1.0 originally published March 2018) An output from the UKGBC Cities Programme, sponsored by: 1 Acknowledgements This resource is the output of a UKGBC project in association with The intention is that key stakeholders feel ‘co-ownership’ of this Core Cities UK. It has been produced through a combination of resource, and we are grateful to the organisations below for their workshops, meetings, written consultation and individual feedback. endorsement. We invite others to do likewise. A large number of organisations have taken time to feed into the For any queries in relation to this resource, contact process. A full list can be found on the following slide. However, John Alker, Director of Policy & Places, UKGBC: we are particularly grateful for the extensive time provided by [email protected] Charlene Clear, BRE and Duncan Price, BuroHappold. 2 Acknowledgements The following organisations provided input and/or review during the original process. This acknowledgement does not imply endorsement. Barratt Developments GLA Newcastle City Council Berkeley Group Greater Manchester Combined Authority PassivHaus Trust Bioregional Hoare Lea PRP BRE HTA Rockwool BuroHappold Hurstwyn Associates Saint Gobain Cambridge City Council Igloo Regeneration St Albans & District Council Clarion Housing Group JLL Sustainable Homes Climate KIC Lendlease UK100 Core Cities UK Levitt Bernstein Useful Projects Currie Brown Linkcity WSP Eastleigh Borough Council