Appendices Appe

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Differences in Energy and Nutritional Content of Menu Items Served By

RESEARCH ARTICLE Differences in energy and nutritional content of menu items served by popular UK chain restaurants with versus without voluntary menu labelling: A cross-sectional study ☯ ☯ Dolly R. Z. TheisID *, Jean AdamsID Centre for Diet and Activity Research, MRC Epidemiology Unit, University of Cambridge, Cambridge, United a1111111111 Kingdom a1111111111 ☯ These authors contributed equally to this work. a1111111111 * [email protected] a1111111111 a1111111111 Abstract Background OPEN ACCESS Poor diet is a leading driver of obesity and morbidity. One possible contributor is increased Citation: Theis DRZ, Adams J (2019) Differences consumption of foods from out of home establishments, which tend to be high in energy den- in energy and nutritional content of menu items sity and portion size. A number of out of home establishments voluntarily provide consumers served by popular UK chain restaurants with with nutritional information through menu labelling. The aim of this study was to determine versus without voluntary menu labelling: A cross- whether there are differences in the energy and nutritional content of menu items served by sectional study. PLoS ONE 14(10): e0222773. https://doi.org/10.1371/journal.pone.0222773 popular UK restaurants with versus without voluntary menu labelling. Editor: Zhifeng Gao, University of Florida, UNITED STATES Methods and findings Received: February 8, 2019 We identified the 100 most popular UK restaurant chains by sales and searched their web- sites for energy and nutritional information on items served in March-April 2018. We estab- Accepted: September 6, 2019 lished whether or not restaurants provided voluntary menu labelling by telephoning head Published: October 16, 2019 offices, visiting outlets and sourcing up-to-date copies of menus. -

12 Point Arial

Nicola Hesketh Project and Information Coordinator Our Ref: FOI3743/NH/02 Please ask for: Nicola Hesketh Direct dial: 01827 709 587 E-mail: [email protected] [name redacted] 9th February 2016 Dear [name redacted] Freedom of Information – Request for Information With regards to your recent enquiry for information held by the Authority under the provisions of the Freedom of Information Act. Please find the information you requested below with reference in the box to your original enquiry for clarity where multiple answers are required. Details of Your Request We would like an extract from the Public Register of Food Businesses in the local authority's region with the following information on all food businesses: 1. Business Name 2. Business Address Line 1 3. Business Address Line 2 4. Business Address Line 3 5. Business Address City 6. Business Address Post code 7. Business Email address 8. Business Telephone number 9. Type of food business / usage The response to your request as follows: Please see attached PDF IMPORTANT NOTICE ABOUT USE OF INFORMATION PROVIDED UNDER THE FREEDOM OF INFORMATION ACT (FoIA) Most of the information that we provide in response to Freedom of Information Act 2000 requests will be subject to copyright protection. In most cases the copyright will be owned by Tamworth Borough Council. The copyright in other information may be owned by another person or organisation, as indicated on the information itself. You are free to use any information supplied for your own non-commercial research or private study purposes. The information may also be used for any other purpose allowed by a limitation or exception in copyright law, such as news reporting. -

Appendix D C10097

Trowbridge Retailer Requirements (March 2007) Store Type Location Required Size (sq.ft) Convenience Goods Comparison Goods Service Other Prime Pitch / High Street In Town Shopping Centre Good Secondary Frontage Neighbourhood Parades / Estates Prominent Busy Main Road Retail Park Leisure Park / Business Greenfield Site Brownfield Site Edge of Town / Out Requirement (min) Requirement (max) Ask (café/bar) x x x x x 2500 5000 Bakers Oven (bakers) x x x x x 1200 2500 Barnados (charity) x x x x x x x 400 3000 Bathstore.Com (bathrooms) x x x x 2500 5000 Billabong (clothing) x x 3000 5000 Body Shop (cosmetics) x x x 1000 Bon Marche (clothing) x not provided 2500 3500 Bookends (books) x x x 750 1500 Debenhams (department store) x x x x 12000 20000 Edinburgh Woollen Mill (knitwear) x x x 1750 2250 Emporio (furniture) x x x x x 7000 10000 Ex Stores (sports and leisurewear) x x x x x 2500 5000 Farmfoods (food) x xxxxxx xxx5000 8000 Fopp Records (cds/dvds) x x 2000 10000 KFC (restaurant/take-away) x not provided 2000 3000 Matalan (clothing) x x x 20000 35000 Nationwide Autocentres (vehicle sales) x x 4000 10000 Pizza Hut (restaurant/take-away) x x x x x 3189 3500 Pizza Express (bar/restaurant) x x x x x 2500 5000 Poundland (variety/discount) x x x x 2500 10000 Robert Dyas (ironmongers/hardware) x x x x 2500 3000 Saks (hair) x x 1000 Savers (health and beauty) x x x 2000 2500 T-Mobile (mobile phones) x x x 800 1200 TJ Hughes (discount department store) x x 25000 40000 TK Maxx (variety / discount) x x x x x x x x 15000 40000 Vintage Inns (public houses) -

Annual Report and Accounts

2 0 1 4 Annual Report and Accounts www.mbplc.com Mitchells & Butlers plc Annual Report and Accounts 2014 Mitchells & Butlers plc is Our strategy to achieve this a member of the FTSE 250 vision has five key elements: and runs some of the UK’s •• Focus•the•business•on•the•most• best-loved restaurant and pub attractive•market•spaces•within• brands including All Bar One, eating•and•drinking•out Harvester, Toby Carvery, •• Develop•superior•brand• Browns, Vintage Inns and propositions•with•high•levels•• Sizzling Pubs. Our vision is to of•consumer•relevance run businesses that guests love •• Recruit,•retain•and•develop• to eat and drink in, and as a engaged•people•who•deliver• result grow shareholder value. excellent•service•for•our•guests •• Generate•high•returns•on• investment•through•scale• advantage •• Maintain•a•sound•financial•base Strategic report 2–33 Contents Strategic report 2 2014 Highlights 3 Chairman’s statement 4 Mitchells & Butlers at a glance Chief Executive’s statement Page 6 Governance Governance 35 Chairman’s introduction to Governance 36 Board of Directors 34–66 38 Directors’ report 6 Chief Executive’s statement 42 Directors’ responsibilities statement 8 Our market 43 Corporate governance statement 10 Our business model 48 Audit Committee report 12 Our strategy 50 Report on Directors’ remuneration 14 Our strategy in action 18 Risks and uncertainties 22 Key performance indicators Financial statements 24 Business review 68 Independent auditor’s report to the 26 Corporate social responsibility members of Mitchells & Butlers -

Schedule of Multilpe National Retailers

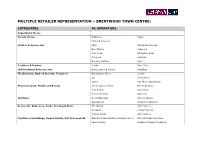

MULTIPLE RETAILER REPRESENTATION – BRENTWOOD TOWN CENTRE: CATEGORIES A1 OPERATORS Department Stores Variety Stores Wilkinson Argos Marks & Spencer Fashion & Accessories M&Co Clares Accessories Bon Marche Peacocks New Look CC Ladies Wear Monsoon Fat Face Dorothy Perkins Next Footwear & Repairs Clarks Shoe Zone Childrenswear & Accessories Early Learning Centre BabyGap TV, Electrical, Radio & Records, Telephone Blockbuster Video 3 Store O2 Phones 4 U Game Car Phone Warehouse Pharmaceutical; Health and Beauty The Fragrance Shop The Body Shop Toni & Guy Superdrug Boots Chemists Uppercut Opticians Boots Opticians Vision Express Specsavers Dolland & Aitchison Books, Art, Stationery, Cards, Printing & Photo The Works Card Factory WHSmith Kodak Express Clinton Cards Waterstones Furniture, Furnishings, Carpet Outlets, DIY & Household Granite Transformations Interior Decor Clive Christian Furniture Laura Ashley Steamer Trading Cookshop Dreams Furniture Ponden Home Interiors Unmistakeably Mark Wilson Sports, Camping & Outdoor Millets Sports Direct Fenton Sports Travel Agencies First Choice Thompson Thomas Cook Charity Shops St Francis Hospice Cancer Research UK Oxfam British Heart foundation Miscellaneous Cooperative Funeral Directors Cartridge World Julian Graves Health foods Holland & Barrett Halfords Metro Foodstores, Off-Licences & CNT Subway Nisa Metro Bakers Oven Somerfield Thorntons Iceland Sainsburys Greggs The Baker Bagelbyte Humbug Confectionary A2 OPERATORS A3 OPERATORS Swinton Insurance Office Ladbrokes Prezzo Nando’s HSBC Bank Britannia Building Society McDonald’s Cafe Rouge Santander Coral Betting Office Zizzi BB’s Coffee & Muffins Natwest Halifax Starbucks Caffe Nero Lloyds TSB Barclays Pizza Express Slug & Lettuce The Money Shop Bairstow Eves KFC Nationwide Saffron Building Society A4 OPERATORS A5 OPERATORS O’Neills Public House Domino’s Pizza . -

Restaurants, Takeaways and Food Delivery Apps

Restaurants, takeaways and food delivery apps YouGov analysis of British dining habits Contents Introduction 03 Britain’s favourite restaurants (by region) 04 Customer rankings: advocacy, value 06 for money and most improved Profile of takeaway and restaurant 10 regulars The rise of delivery apps 14 Conclusion 16 The tools behind the research 18 +44 (0) 20 7012 6000 ◼ yougov.co.uk ◼ [email protected] 2 Introduction The dining sector is big business in Britain. Nine per cent of the nation eat at a restaurant and order a takeaway at least weekly, with around a quarter of Brits doing both at least once a month. Only 2% of the nation say they never order a takeaway or dine out. Takeaway trends How often do you buy food from a takeaway food outlet, and not eat in the outlet itself? For example, you consume the food at home or elsewhere Takeaway Weekly or Monthly or several Frequency more often times per month Less often Never Weekly or more often 9% 6% 4% 1% Monthly or several times per month 6% 24% 12% 4% Eat out Eat Less often 3% 8% 14% 4% Never 0% 1% 1% 2% (Don’t know = 2%) This paper explores British dining habits: which brands are impressing frequent diners, who’s using food delivery apps, and which restaurants are perceived as offering good quality fare and value for money. +44 (0) 20 7012 6000 ◼ yougov.co.uk ◼ [email protected] 3 02 I Britain’s favourite restaurants (by region) +44 (0) 20 7012 6000 ◼ yougov.co.uk ◼ [email protected] 4 02 I Britain’s favourite restaurants (by region) This map of Britain is based on Ratings data and shows which brands are significantly more popular in certain regions. -

Follow Us! Opening Hours Contact Snow+Rock &Runnersneed What's New at Bluewater There's a World to Explore

*Terms and conditions available at bluewater.co.uk at available conditions and *Terms bluewaterthoughts.com Thomas Cook | TSB | TUI | TSB | Cook Thomas | Santander | Spencer & Marks card * Barclays | Halifax | John Lewis | Kanoo | | Kanoo | Lewis John | Halifax | Barclays and you could win a £500 gift gift £500 a win could you and your experience at Bluewater Bluewater at experience your following stores: following Tell us what you think about about think you what us Tell Bureau de Change can be found at the the at found be can Change de Bureau HOLIDAY SPENDING MONEY? SPENDING HOLIDAY more! 101 signings and and signings offers, book book offers, out on events, events, on out dinotropolis.co.uk us. Don’t miss miss Don’t us. BOOK NOW at at NOW BOOK like like have to to have love us you you us To have a t-rexcellent birthday. t-rexcellent a have themed party rooms you’ll you’ll rooms party themed parties too! With three three With too! parties school groups and birthday birthday and groups school Dinotropolis is roarsome for for roarsome is Dinotropolis this weekend this O’Neill to refuel! to at more and essentials your all Get winter? this slopes the Hitting time to visit the Fossil Cafe Cafe Fossil the visit to time sleeping dinosaurs! Then it’s it’s Then dinosaurs! sleeping be careful not to wake the the wake to not careful be collection has a sexy vibe that’s more tart and sweet! and tart more that’s vibe sexy a has collection and beat the laser beams.. -

Retail Study Update 2009 and Appendices (PDF 5Mb)

Basingstoke & Deane Borough Council Retail Study Update APPENDICES January 2009 Prepared by: Strategic Perspecti>es LLP 24 Bruton Place London W1J 6NE Tel: 020 7529 1500 Fax: 020 7491 9654 January 2009 Basingstoke and Deane Borough Council Retail Study Update ____________________________________________________________________________________ APPENDICES 1. BASINGSTOKE TOWN CENTRE: CATCHMENT AREA 2. HOUSEHOLD TELEPHONE INTERVIEW SURVEY – QUESTIONNAIRE & RESULTS 3. CONVENIENCE GOODS SHOPPING – MARKET SHARE PATTERNS FOR MAIN FOOD & TOP-UP SHOPPING 4. COMPARISON GOODS SHOPPING – MARKET SHARE PATTERNS 5. BASINGSTOKE TOWN CENTRE: EXPERIAN GOAD ‘CENTRE REPORT’ 6. BASINGSTOKE TOWN CENTRE: FOCUS RETAILER REQUIREMENTS REPORT 7. BASINGSTOKE TOWN CENTRE: PEDESTRIAN FLOWCOUNT SURVEY 8. STRATEGIC PERSPECTI>ES LLP – BASINGSTOKE TOWN CENTRE AUDIT 9. BASINGSTOKE TOWN CENTRE – USE CLASSES & VACANT UNITS 10. DISTRICT & LOCAL CENTRES AUDIT 11. CONVENIENCE & COMPARISON GOODS FLOORSPACE & ‘BENCHMARK’ TURNOVER ESTIMATES 12. RETAIL CAPACITY ASSESSMENT – EXPLANATORY NOTE 13. COMPARISON GOODS RETAIL CAPACITY ASSESSMENT 14. CONVENIENCE GOODS RETAIL CAPACITY ASSESSMENT 15. RETAIL CAPACITY ASSESSMENT – POPULATION ‘SENSITIVITY’ ANALYSIS 16. MAJOR DEVELOPMENT AREA – RETAIL CAPACITY ASSESSMENT APPENDIX 1: BASINGSTOKE TOWN CENTRE CATCHMENT AREA - Plan 1: Catchment and Borough Area SLOUGH M25 HAYES M25 A346 A4074 WINDSOR A4 M4 READING FELTHAM EGHAM ASHFORD A339 A33 BRACKNELL MARLBOROUGH WOKINGHAM ASCOT HUNGERFORD A33 WEST MOLESEY NEWBURY VIRGINIA WATER THATCHAM A322 CHERTSEY -

Fast Food Industry Report June 2018

Fast Food Industry Report June 2018 Fast Food Report Mexico 2018Washington, D.C. Mexico City Monterrey Fast Food Industry Industry Overview • The industry is made up by all the fast food participants in Mexico, including restaurant chains, franchises, food retail chains, convenience stores and street vendors • The approximate industry value in 2017 was MX$203 billion, while outlets numbers increased to more than 262 thousand • The fast food industry in Mexico is expected to have a value of MXN$234 billion in 2022, with a compound annual growth of 3% • Fomento Económico Mexicano led sales in 2017, posting a value share of 8% Industry Sales Industry Outlets MXN Billion Units $221.4 283,585 $209.7 $215.6 $203.3 276,208 $188.3 $179.4 269,091 262,246 252,236 242,747 2015 2016 2017 2018 2019 2020 2015 2016 2017 2018 2019 2020 Historical Forecast Industry Trends: • Fast food restaurants are offering more value packs for breakfast, lunch and dinner, thus increasing options for consumers who eat at home, in order to compete against small local restaurants and convenience stores • The increasing preference among consumers for healthy food has benefited several brands that offer salads and other healthy options, changing the industry perception • The actual growth of the fast food industry in Mexico is driven by the great performance of the convenience stores • Convenience store OXXO remains as the leading company, it expects to continue growing over the short term as its sales increase remarkably. It reached over 16,000 stores in 2017, eight -

Butt Foods Vegan Snapshot UPDATED 11 05 18

SNAPSHOT OF THE GROWING VEGAN SCENE IN THE UK The rise of veganism in the UK and what it may mean for foodservice opportunities From being seen as niche and ‘quirky’ even just ten years ago, veganism is now more popular than ever across the UK. Driven primarily by younger people responding to growing fears over personal health, animal welfare and climate change – and fuelled by campaigns such as the annual Veganuary – the growing interest and participation in veganism looks set to continue. As ever, for foodservice operators, the vegan movement represents both a challenge and an opportunity. Either way, it can’t be ignored. Veganism is Most trend forecasters and market analysts agree that the era of mainstream becoming more veganism has arrived. Growing out of its perceived eccentric origins, and latterly its mainstream and trendy, ‘metropolitan hipster' cache, the increasingly wide interest in the vegan way less niche. of eating is fuelled by a variety of powerful – and highly topical – consumer motives and supported by a burgeoning industry of crowd-funded new business start-ups, cookbooks, Youtube channels, social media and events. But to properly understand the growth it’s important to recognise that it’s largely a ground-up movement, driven mainly by under-35s, and their motivations suggest that this is sustainable growth. "1 of "15 What’s a vegan? Like vegetarians, vegans have cut all meat and fish from their diet, but they go a step further and also exclude any products of animal origin, such as milk, cheese, eggs and honey. More than 860,000 of all vegetarians and vegans also avoid all non- dietary animal products such as leather and wool.! ! The vegan ‘halo effect’ Demand is being It’s interesting to note that, beyond the core of declared vegans, there seems to be a driven not only by growing ‘halo’ of consumers who are not actually vegans themselves, but exhibit declared vegans, but by non-vegans vegan buying behaviour from time to time. -

Weekly Briefing Report Week Ending 26 July 2020

Weekly Briefing Report Week ending 26 July 2020 Published 27 July 2020 Introduction I have been publishing The Quarterly Briefing Report since 2009. Over four months ago, I started producing The Weekly Briefing Report to provide a more immediate view. I would value your feedback on topics you would particularly like me to add to my coverage - my email address is [email protected] and my phone number is 07785 242809. My insight What happens to the foodservice sector when the coronavirus packs its bags and leaves town, as one day it will? The answer to this question depends on many things but they will all be influenced in one way or another by the length of time between now and the end of the virus. I have been investigating these issues in conjunction with the IGD over the last few months (and some results have been published in our joint report “Eating Out vs Dining In”). But there are many specifics that remain to be investigated and answered. It seems to me that up to now, for the foodservice sector at any rate and I would guess most other sectors of the economy, there have been four ways that the coronavirus has impacted on the industry and the people and companies within it. First, the virus has exposed faults (and positives) that underline foodservice. Second, it has led to a process of degrading (businesses have been downsized, valued employees have been made redundant and much more). Third, there has been an acceleration of past trends (reduction in overcapacity, and the rebalancing of relationships between tenants and landlords spring to mind). -

A Historical Look at the Shops – Past and Present in the Colchester Town Centre Area

A HISTORICAL LOOK AT THE SHOPS – PAST AND PRESENT IN THE COLCHESTER TOWN CENTRE AREA 1 INTRODUCTION Having written about walking around our town and others over Christmas and the month of January, looking at churches in Essex, Suffolk and Norfolk, the weekend of 1st and 2nd February 2014, saw me writing and photographing the main shops in our town of Colchester and trying to find out the National History of the businesses. So here is my story again …… 99p STORE (84-86 Culver Street East) 99p Stores Ltd. is a family run business founded in January 2001 by entrepreneur Nadir Lalani, who opened the first store in the chain in Holloway, London, with a further three stores opening later that year. In 2002, Lalani decided to expand the business throughout the UK and has rapidly developed 99p Stores, operating a total of 129 stores as of March 2010 and serving around 1.5 million customers each week, undercutting their main rival Poundland by a penny. As of mid-2009 the company offered more than 3,500 different product lines throughout its stores. Most of their stores are based in the south of the UK, although there are stores as far north as Liverpool and Hartlepool. The chain saw accelerated store expansion upon the collapse of Woolworths Group, where they took the opportunity to acquire 15 of these former stores, increasing their estate to 79 at that time. Landlords are now regarding 99p Stores as an anchor tenant due to the significant number of customers one of their stores can bring to a location.