Annual Reports [Uk]

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MINUTES MONTANA HOUSE of REPRESENTATIVES 53Rd LEGISLATURE

MINUTES MONTANA HOUSE OF REPRESENTATIVES 53rd LEGISLATURE - REGULAR SESSION COMMITTEE ON BUSINESS & ECONOMIC DEVELOPMENT Call to Order: By CHAIRMAN STEVE BENEDICT, on January 13, 1993, at 9:00 A.M. ROLL CALL Members Present: Rep. Steve Benedict, Chair (R) Rep. Sonny Hanson, Vice Chair (R) Rep. Bob Bachini (D) Rep. Joe Barnett (R) Rep. Ray Brandewie (R) Rep. Vicki Cocchiarella (D) Rep. Fritz Daily (D) Rep. Tim Dowell (D) Rep. Alvin Ellis (R) Rep. Stella Jean Hansen (D) Rep. Jack Herron (R) Rep. Dick Knox (R) Rep. Don Larson (D) Rep. Norm Mills (R) Rep. Bob Pavlovich (D) Rep. Bruce Simon (R) Rep. Carley Tuss (~ Rep. Doug Wagner (R) Members Excused: All Present Members Absent: None Staff Present: Paul Verdon, Legislative Council Claudia Johnson, Committee Secretary Please Note: These are summary minutes. Testimony and discussion are paraphrased and condensed. Committee Business Summary: Hearing: cont. of hearing on HB 29 Executive Action: HB 29 HEARING ON HB 29 Opening Statement by Sponsor: REP. VIVIAN BROOKE, House District 20, continued with HB 29. She distributed 2 exhibits, Terry Karson from MAGDA, and a synopsis of HB 29. EXHIBITS 1 and 2 930113BU.HMl HOUSE BUSINESS & ECONOMIC DEVELOPMENT COMMITTEE January 13, 1993 Page 2 of 5 Proponents' Testimony: Gloria Hermanson said the advocacy feels the overall intent of the bill is appropriate and with the amendments attached they support HB 29. EXHIBIT 12 for amendments. Ms. Hermanson distributed two exhibits, Monte Dolack Graphics from Missoula, and William Frazier, Jr. from Livingston. EXHIBITs 3 and 4 Laura J. Millin, Director Missoula Museum of the Arts, said the fine arts credibility and respectability in the art community is nationwide. -

September 25-29, 2012 Missoula, Montana Recreation and Parks

MONTANA AND IDAHO Recreation and Parks Associations 2012 Conference © MONTE DOLACK “ZOO CITY” September 25-29, 2012 Missoula, Montana AND Hosted by: Outside Montana Recreation & Parks Assn. www.mtrpa.info 406-552-6271 Idaho Recreation & Parks Assn. Active www.irpa-idaho.org Missoula Parks and Recreation Montana Fish, Wildlife & Parks University of Montana Our Montana Inc. Destination Missoula Missoula Children and Nature Program Tracks Professional Development Track MHHS Pool Rules & ADA and VGB: Making Sense of the “Alphabet for Compliance” at Your Pools W 10 - 11:15 a.m. The Power of Partnerships: Milltown State Park/ Blackfoot River Tour W 1:45 - 6 p.m. Implementing Social Media & Technology in Parks and Recreation TH 10 - 11:15 a.m. Partnerships and Creative Funding TH 2:45 - 4 p.m. Mountain Pine Beetle’s Impact on Maintaining Quality Outdoor Recreation Facilities F 8:30 - 9:45 a.m. Park and Trail Design Standards F 10 - 11:15 a.m. Missoula Parks and Recreation Park Tour F 12:45 - 3:30 p.m. Outside & Active… Vision and Relevance Track Missoula Style Saving Money with Green Practices W 1:45 - 6 p.m. Views and Vistas Close To Identifying, Recognizing and Promoting the Benefits of Parks , Trails and Recreation TH 10 - 11:15 a.m. Downtown Missoula Navigating the Politic al Scene: How to W ork with Boards and Elec ted Officials TH 1:15 - 2:30 p.m. How to Plan a “Sunday Streets” Event (Closing Streets to Cars for a Day) TH 2:45 - 4 p.m. Visit Mount Jumbo’s “L” Children and Nature Track trail from the Cherry St. -

Fall 2020 Issue

Fall 2020 October • November • December S MONTANA ARTS COUNCIL Providing information to all Montanans through funding by the National Endowment for the Arts and the State of Montana visual arts native arts native literary arts literary performing arts performing page6 page10 page12 page16 SOUTH NORTH Photo courtesy of Rita Collins Courtesy of Yellowstone Art Museum Tobacco Valley Quilters Yellowstone Art Museum Keep History and Tradition Launches Distance Alive Through Their Craft Learning Opportunity A group of quilters has been making a big impact on a Art News A circuitous art-filled journey, suitcase in hand, has led small town for decades. Their weekly sessions celebrate the Yellowstone Art Museum (YAM) to its well- the heritage of their community, bringing history to life timed destination. while raising funds for an important Eureka institution. Read more, page 20 Read more, page 17 EAST WEST SOUTH NORTH Putting on the Dog book cover art Photo courtesy of Garry Wunderwald Montana Poet Laureate Little Big Man 50 Years Melissa Kwasny Statewide Later Melissa Kwasny speaks to her deep, life-long relationship Director Arthur Penn set out to “De-Hollywoodize with verse and shares her optimism and enthusiasm for the western” in his 1970 Montana-made film, intending to the art of poetry. Her rich experiences bring wisdom to portray the Battle of the Little Bighorn according to her words about poetry’s purpose and meaning as well how the West really was rather than how it was imagined. as her creative process. Read more, page 7 Read more, page 12 First Grants Made from the William B. -

New Mam Annual Report

Artists Exhibited Mark Abrahamson Marcy James Greg Siple Michelle Adam Gesine Janzen David J. Spear Jean Albus G. Peter Jemison Brent Spink Brad Allen Aaron Cordell David Shaner Adrianna Alvarez Johnson Asel Sherimkulova Neal Ambrose-Smith Karlie Kahl Duane Slick Ruth Angel Peter Keefer Tina Slon Justin Anthony Garrett Kelly Edgar Smith Anne Appleby Therese Kenyon Patricia Smart Louis Archambault Steve Krutek Jaune Quick-to- Aden Arnold Dyna Kuehnle See Smith Chris Autio King Kuka Bently Spang Lela Autio Peter Kurinsky Politi Spiridula Rudy Autio Laura Lamiel Mariya Stangl Stephanie Bacon Marion Lavery Ben Steele James Bailey Jacob Lawrence Karl Stein Susan Barnes Henriette Lehtonen Frank Stepek Elizabeth Hughes Bass K Bonnema Leslie Branson Stevenson Joe Batt Aphrodite Litti Susan Stewart Cecilia Benitez Ken Little Bill Stockton Tu Biaxiong Winnie Lloyd Katy Stone Dwight Billedeaux Beth Lo Inez Storer Maxine Blackmer Alyssa Lockwood Alma Suljevic Courtney Blazon Jon Lodge Janet Sullivan Melissa Bob Truman Lowe Jan Swinburne Mary Ann Bonjorni David Lusk Janna Syvanja Jacqueline Brito Nancy MacDonald Marjorie Taylor Kate Brown Maria Machuca Donna Hashitani Shirley Brown Clay Mahn Thomas Marilyn Bruya Cathryn Mallory Wendy Thon John Buck Belkis Ayon Manso Patricia Thornton Calypso Bulbosa Finua Mara Bobby Tilton Don Bunse Jenny Marketou James Todd Freeman Butts Mario Martinez Kaveni Tomuse Lucy Capehart Vivian Maria Mayne Trimpin Margaret Caraway Gordon McConnell Gail Tremblay James Castle Asha McDonald Suzanne Truman Suzana Ceric Jerry McGahan Eva Ursprung Anthony Cesare Bobbie McKibbin Kyle Utter Damian Charette Henry Meloy Andree Van Nuys Russell Chatham Peter Meloy Don Voisine Judy Chicago Terry Melton Celon Volimar Russell Childers Marvin Messing Willem Volkerz Orville Chigbrow Sheila Miles Daniela van Waberer Jason Elliott Clark Leslie Van Laura Cristina Maja Clas Stavern Millar II Valdivieso Andy Cline Wes Mills Peter Voulkos Susan Christie Ryan Mitchell Theodore Waddell Corwin Clairmont Shari Montana Arin Waddell John L. -

A History Montana's Fisheries Division from 1945 to 2000

FGHISTORY1945-2000workcopy1.wpd DRAFT 2/17/01 Note: This document replaces FGhist1943-85workcopy3.wpd and FGhist1986-2000workcopy2.wpd which have been combined into this document and expanded. A HISTORY MONTANA’S FISHERIES DIVISION FROM 1945 TO 2000 “A River is more than an amenity, it is a treasure. It offers a necessity of life that must be rationed among those who have power over it.” – Justice Oliver Wendell Holmes, Jr. “Only an idle little stream, Whose amber waters softly gleam, Where I may wade through woodland shade, And cast a fly, and loaf, and dream. “Only a trout or two, to dart, From foaming pools, and try my art: ‘Tis all I’m wishing -- old fashioned fishing, And just a day in Nature’s heart.” - - - Van Dyke In: Biennial Report of the Montana Fish and Game Commission, 1925-1926. Note: Information that has yet to be included in this history: 1. Additional Fisheries issue papers listed below: Habitat Clark Fork River reclamation, recovery, lawsuit w/ARCO - Glenn Phillips Future Fisheries Improvement Program - Glenn Phillips River Restoration Program - Glenn Phillips Pallid Sturgeon - Bill Gardner Fish Management (Hatcheries): Hatchery renovation and reconstruction - Tim Gallagher & Gary Bertellotti Fish Management: Fisherman Log program - Bob McFarland Angler Surveys - Bob McFarland Bitterroot River efforts - Chris Clancy Canyon Ferry fishery - Ron Spoon Electro fishing development - Dick Vincent Fish population estimates methods development & use - Dick Vincent Madison River - Dick Vincent Whirling disease - Dick Vincent Flathead Lake fishery - Mark Deleray Fort Peck fishery - Bill Wiedenheft Hauser/Holter reservoirs - Steve Leathe Montana Fish Records program - Margie Peterson Mysis shrimp/Kokanee in Flathead Lake - Mark Deleray Paddlefish program - Jim Liebelt (Yellowstone)/ Kent Gilge (Missouri) Pallid sturgeon program - Bill Gardner Scale mounting lab in Bozeman - Wayne Black Fishing regulations historical trend, special regs, etc. -

May 2020 News Releases

University of Montana ScholarWorks at University of Montana University of Montana News Releases, 1928, 1956-present University Relations 5-2020 May 2020 news releases University of Montana--Missoula. Office of University Relations Follow this and additional works at: https://scholarworks.umt.edu/newsreleases Let us know how access to this document benefits ou.y - UM News - University Of Montana A to Z my.umt.edu UM News UM / News / 2020 / May May 2020 News 05/29/2020 - UM Graduate Awarded Fulbright for Iceland Energy Studies - Clint Walker 05/29/2020 - Montana Public Radio Wins Regional Murrow, Associated Press Awards - Josh Burnham 05/28/2020 - Survey: Montana Tourism Anxious as COVID-19 Impacts Continue, Travelers Feel Safer - Jeremy Sage 05/27/2020 - UM to Light Main Hall and M to Honor Area High School Grads - Paula Short 05/27/2020 - Micro-Internships Provide UM Students Big Resume Building Opportunities - Andrea Rhoades 05/26/2020 - UM Wildlife Biology Master’s Student Awarded Fulbright Scholarship - Clint Walker 05/22/2020 - UM Grad and Filmmaker to Travel to Mexico on Fulbright Scholarship - Clint Walker 05/21/2020 - UM Updates Schedule for Fall Semester - Paula Short 05/20/2020 - UM Communication Studies Graduate Awarded Fulbright Scholarship - Clint Walker 05/19/2020 - UM Researchers Study How COVID-19 Affects Missoula Trails, Outdoor Recreation - Elizabeth Metcalf http://news.umt.edu/2020/05/default.php[6/8/2020 1:02:06 PM] - UM News - University Of Montana 05/19/2020 - UM Art Museum Reopens With Popular Monte Dolack Exhibition -

Volume 35 Number 3 November 2010

VOLUME 35 NUMBER 3 NOVEMBER 2010 If you have not already renewed, you are getting this issue of The Pileated Post because a mail delay may have kept some renewals from reaching the Membership Chair in a timely manner. This delay occurred because an address change caused some mail to be diverted through Denver. If there had been no delays, people who did not renew would not be receiving this issue of the Post, as was announced at the October gen- eral meeting. Without renewal, you will not receive the next issue. Please renew, we do not want to lose any members. Big Thank You’s to all of the volun- ies, beverages and pats on the back. This year teers at the FAS OSNA Work Day on Septem- we had some “first timers” and several ber 25. You were perfect! Everything about “everytimers” (never missed a Work Day). Eve- the group effort was perfect: the people, the rybody had a good time and made a difference! weather, the work time, the refreshments, the One very important contribution to FAS, quality of the work, the resulting improve- besides the positive changes at the Natural ments, the safety, the fun and friendship and Area, is the fact that we qualified for considera- especially the place itself – the perfect riparian tion of a $1000 grant from Prudential Global area! Volunteer Day – submitted by Jane Lopp & As- Thirty-three determined volunteers pulled sociates Prudential agency. Jane and Bob Lopp are weeds, cleared trails, shuttled crews, repaired fence, longtime supporters and participants in FAS and mowed, clipped, pulled and sawed their way through a OSNA. -

Spring 2020 Issue

Poetry Out Loud Finals Page 14 Arts in the Age of COVID-19 Pages 6-7 & 17 Spring 2020 n Montana - The Land of Creativity MAC NEWS Crow tell their own story with major Governor appoints two exhibit at Chicago’s Field Museum new members, four By Anna Paige Reprinted with permission from the Billings Gazette, billingsgazette.com, March 15 returnees to MAC As an indigenous female scholar and The Montana Arts curator, Nina Sanders doesn’t lack for stories Council welcomes two to tell. new board members Born and raised on the Crow Indian Res- – Angela Russell of ervation, Sanders is working to decolonize Lodge Grass and Cor- museums and work within such institutions by Skinner of Billings. that have for centuries excluded and misrep- Russell replaces Lynne resented Indigenous voices in exhibits and in Montague, who was history books. appointed in 2015 and served one term, “We can effectively look at cultural insti- and Skinner fills the tutions with historical collections that are the vacated term of Arlene cause of these misinterpretations of our culture Parisot, which ends in and the perpetuation of stereotypes,” said 2023. Corby Skinner Sanders, whose Apsáalooke name, Akbileoosh, “Lynne brought the means Brings the Water. perspectives of an art- Last year, Sanders was invited to curate an ist, an active member exhibition for the Field Museum in Chicago. of the cultural commu- Titled “Apsáalooke Women and Warriors,” it Curator Nina Sanders carries a money tree, a traditional gift to nity, and a profession is the largest exhibition pairing historical and honor someone, in a parade to celebrate the opening of the as an advocate for contemporary items in the Crow tribe’s history Field Museum’s new exhibition “Apsáalooke Women and War- children and juveniles and the first major exhibit curated by a Native riors” in Chicago. -

“I Think the Best Art Feeds the Soul of Civilization. Think About All of the Art, from Day One, That Has Transcended Wars, Famines, the Fall of Empires

“I THINK THE BEST ART FEEDS THE SOUL OF CIVILIZATION. THINK ABOUT ALL OF THE ART, FROM DAY ONE, THAT HAS TRANSCENDED WARS, FAMINES, THE FALL OF EMPIRES. I THINK THAT ARTISTS CAN DIRECTLY AND INDIRECTLY ADDRESS THIS EXISTENTIAL MOMENT.” —RICHARD MISRACH 300 301 Above: Lawrence Gipe, Bisbee, large version, 2012–13, oil on unstretched canvas, 84 by 120 inches; Previous page: Lawrence Gipe, Russian Drone Painting #1 (Mir, Siberia), 2018–19, oil on canvas, 72 by 96 inches Lawrence Gipe, Study for Bisbee, 2012, oil on panel, 14 by 17 inches 302 303 Excerpt from cations, which are critical to earth art’s esthetic im- pact and dissemination. Early land artists without UNDERMINING frequent access to the “timeless” western deserts of- Lucy R. Lippard ten adopted readymade pits (quarries in New Jersey, for instance), where the “timeliness” of nearby sky- Somewhere in an indeterminate time zone between scrapers could be ignored. Smithson, Michelle Stu- the Old and New Wests loom the massive outdoor art, and Charles Simonds, among others, employed sculptures dubbed earthworks in the late 1960s, these geographically ambiguous sites as temporary now more broadly defined as land art. In the U.S., substitutes for the West. Their works are sometimes the best known of these sculptures drawn or cut inspired by the ruins of great monumental civiliza- from the earth itself, or made from its products, tions of the past. Some also visited, and lusted after, are Robert Smithson’s Spiral Jetty, Nancy Holt’s Sun the gigantic western open pit mines (epitomized by Tunnels, the late Walter De Maria’s Lightning Field, the Santa Rita/Chino pit in New Mexico, the Bing- Charles Ross’s Star Axis, James Turrell’s Roden Crater, ham pit in Nevada, and the Berkeley pit in Butte, and Michael Heizer’s Double Negative and City Com- Montana). -

46Th-Annual-Auction-Catalog.Pdf

MISSOULA ART MUSEUM’S SATURDAY FEBRUARY 3 2018 5PM UNIVERSITY CENTER UM 3RD FLOOR AUCTIONEER: Johnna Wells, Benefit Auctions 360, LLC Portland, Oregon PRESENTING SPONSOR A Decade of Support for MAM and the Arts! THANK YOU PRESENTING MEDIA SPONSOR PRINT SPONSOR POWER OF ART AUCTION SPONSORS: Anderson ZurMuehlen Big Sky Commerce Missoulian Missoula Broadcasting Company Noteworthy Paper & Press Rocky Mountain Moving & Storage Slikati Photo + Video University Center and UM Catering Missoula Wine Merchants ACKNOWLEDGEMENTS: Thank you to the many businesses that have donated funds, services, and products to make the auction exhibition, live events, and special programs memorable. We invite you to support the businesses that support MAM. Thank you to all of the auction bidders and attendees for directly supporting MAM’s programs. Thank you to the volunteers who help operate the museum and contribute time, energy, and creativity to help make this important event a success. On behalf of the 46th Benefit Art Auction Committee! We believe art has enormous power—to ignite innovation, engage the next generation, transform perspectives, and inspire a lifetime love of collecting contemporary art. We are honored that artists and art lovers alike have come together to celebrate and support Missoula’s art community and its beloved art museum. COMMITTEE MEMBERS AUCTION JURY Diana Bjorgen Brad Allen Molly Bradford Libby Addington John Calsbeek * Betsy Bach Minette Glaser John Calsbeek * Lynn Metcalf Dustin Hoon Laura Millin * Becca Nasgovitz Becca Nasgovitz Brandon Reintjes * Bethany O’Connell * Lily Scott * *MAM Staff Committee Member Cassie Strauss * THANK YOU to all of the artists for their generous contributions. -

January 2020 News Releases

University of Montana ScholarWorks at University of Montana University of Montana News Releases, 1928, 1956-present University Relations 1-2020 January 2020 news releases University of Montana--Missoula. Office of University Relations Follow this and additional works at: https://scholarworks.umt.edu/newsreleases Let us know how access to this document benefits ou.y Recommended Citation University of Montana--Missoula. Office of University Relations, "January 2020 news releases" (2020). University of Montana News Releases, 1928, 1956-present. 31981. https://scholarworks.umt.edu/newsreleases/31981 This News Article is brought to you for free and open access by the University Relations at ScholarWorks at University of Montana. It has been accepted for inclusion in University of Montana News Releases, 1928, 1956-present by an authorized administrator of ScholarWorks at University of Montana. For more information, please contact [email protected]. - UM News - University Of Montana A to Z my.umt.edu UM News UM / News / 2020 / January January 2020 News 01/31/2020 - UM to Host 103rd Foresters’ Ball - Priya Keller 01/30/2020 - Community Lecture Series at UM to Focus on 19th Amendment - UM Alumni Association 01/29/2020 - Montana Tourism 2019: Nonresident Spending Down, Visitor Numbers Up - Kara Grau 01/28/2020 - UM Team Accepted Into Techstars Accelerator Program - Paul Gladen 01/27/2020 - UM Partners With Montana Colleges For Online Social Work Program - Paige Furniss 01/27/2020 - Astronomy Program at UM Recognized for Great Value - Andrew -

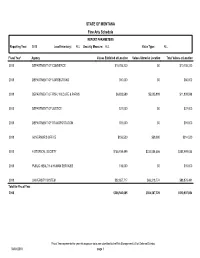

STATE of MONTANA Fine Arts Schedule REPORT PARAMETERS Reporting Year: 2018 Local Inventory: ALL Security Measure: ALL Value Type: ALL

STATE OF MONTANA Fine Arts Schedule REPORT PARAMETERS Reporting Year: 2018 Local Inventory: ALL Security Measure: ALL Value Type: ALL Fiscal Year¹ Agency Values Exhibited at Location Values Stored at Location Total Values at Location 2018 DEPARTMENT OF COMMERCE $10,785,230 $0 $10,785,230 2018 DEPARTMENT OF CORRECTIONS $60,000 $0 $60,000 2018 DEPARTMENT OF FISH, WILDLIFE & PARKS $6,833,699 $5,005,899 $11,839,598 2018 DEPARTMENT OF JUSTICE $27,000 $0 $27,000 2018 DEPARTMENT OF TRANSPORTATION $91,000 $0 $91,000 2018 GOVERNOR'S OFFICE $156,520 $58,000 $214,520 2018 HISTORICAL SOCIETY $155,914,499 $233,084,556 $388,999,055 2018 PUBLIC HEALTH & HUMAN SERVICES $15,000 $0 $15,000 2018 UNIVERSITY SYSTEM $32,657,717 $66,218,774 $98,876,491 Total for Fiscal Year 2018 $206,540,665 $304,367,229 $510,907,894 ¹Fiscal Year represents the year risk exposure data was submitted to the Risk Management & Tort Defense Division. 04/04/2018 page 1 STATE OF MONTANA Fine Arts Schedule REPORT PARAMETERS Reporting Year: 2018 Local Inventory: ALL Security Measure: ALL Value Type: ALL Fiscal Year¹ Reporting Entity Values Exhibited at Location Values Stored at Location Total Values at Location DEPARTMENT OF COMMERCE 2018 DEPARTMENT OF COMMERCE $13,859 $0 $13,859 2018 MONTANA HERITAGE COMMISSION $10,771,371 $0 $10,771,371 TOTAL: $10,785,230 $0 $10,785,230 DEPARTMENT OF CORRECTIONS 2018 DEPARTMENT OF CORRECTIONS, MONTANA WOMEN'S $60,000 $0 $60,000 PRISON TOTAL: $60,000 $0 $60,000 DEPARTMENT OF FISH, WILDLIFE & PARKS 2018 DEPARTMENT OF FISH, WILDLIFE & PARKS $6,833,699 $5,005,899 $11,839,598 TOTAL: $6,833,699 $5,005,899 $11,839,598 DEPARTMENT OF JUSTICE 2018 DEPARTMENT OF JUSTICE $27,000 $0 $27,000 TOTAL: $27,000 $0 $27,000 DEPARTMENT OF TRANSPORTATION 2018 DEPARTMENT OF TRANSPORTATION $91,000 $0 $91,000 TOTAL: $91,000 $0 $91,000 GOVERNOR'S OFFICE 2018 SECRETARY OF STATE $156,520 $58,000 $214,520 TOTAL: $156,520 $58,000 $214,520 ¹Fiscal Year represents the year risk exposure data was submitted to the Risk Management & Tort Defense Division.