An In-Depth Analysis of South Florida's New Condominium

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brochure and to the Documents Required by Section 718.503, Florida Statutes, to Be Furnished by a Developer to a Buyer Or Lessee

OBTAIN THE PROPERTY REPORT REQUIRED BY THE FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE, IF ANY, OF THIS PROPERTY. ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING THE REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. AUBERGE BEACH 1 DEVELOPED BY VISIONARIES page 10 THE AUTHENTIC LUXURY OF AUBERGE page 14 ORIGINAL WORKS OF CONTEMPORARY ART page 22 FEATURES & AMENITIES page 48 FORT LAUDERDALE LIFESTYLE page 62 AUBERGE BEACH 2 SEE LEGAL DISCLAIMERS ON BACK COVER AUBERGE BEACH AUBERGE BEACH 4 5 SEE LEGAL DISCLAIMERS ON BACK COVER INDULGE IN THE ELEGANCE OF BEACHFRONT LIVING AUBERGE BEACH RESIDENCES & SPA FORT LAUDERDALE JOINS AN INTERNATIONAL PORTFOLIO OF AWARD-WINNING PROPERTIES IN NORTH AMERICA Auberge Beach Residences & Spa brings the ultimate personal service ensures that residents’ every need is in luxury living to Fort Lauderdale’s most extraordinary catered to with ease. Unique among even the finest beachfront property. Exquisitely designed residences, a luxury residential properties, Auberge Beach Residences rich array of indoor and outdoor amenities, a tempting & Spa will offer a host of exclusive cultural and culinary selection of restaurants, and a world-class Auberge- experiences that have been thoughtfully crafted to branded dining and spa are perfectly located directly enhance residents’ lifestyle and engage their senses. on 450 linear feet of pristine Atlantic Ocean beachfront. From sunup to sundown and deep into the night, Throughout Auberge Beach Residences & Spa, a curated residents will enjoy living life to its fullest and creating collection of contemporary art creates an atmosphere memories that will last a lifetime. -

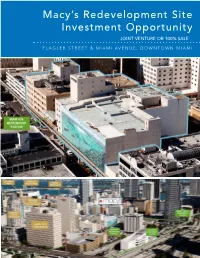

Macy's Redevelopment Site Investment Opportunity

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

Views the Miami Downtown Lifestyle Has Evolved

LOFT LIVINGwww.miamicondoinvestments.com REDESIGNED Feel the Street. At Your Feet. Out your window. At your feet. www.miamicondoinvestments.com ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING THE REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE, IF ANY, OF THIS PROPERTY. See Legal Disclaimers on Back Cover. See Legal Disclaimers on Back Cover. www.miamicondoinvestments.com See Legal Disclaimers on Back Cover. Welcome to the Core of Downtown Life. www.miamicondoinvestments.com See Legal Disclaimers on Back Cover. See Legal Disclaimers on Back Cover. At the center of all life is a place from which all energy flows. In the heart of downtown Miami’s cultural and This is the fusion of commercial district, this is Centro - the new urban address inspired by today’s modern lifestyles. Smart and sleek... Lofty and livable... Inviting and exclusive... work, play, creativity, the Centro experience takes cosmopolitan city dwelling to street level. and accessibility. Step inside. www.miamicondoinvestments.com www.miamicondoinvestments.com See Legal Disclaimers on Back Cover. See Legal Disclaimers on Back Cover. Centro stands as proof that you truly can have it all. Location, style, quality, and value are all hallmarks of life Building Amenities Comfort. in our city center. • Triple-height lobby entrance • 24-Hour reception desk Step outside your door and find yourself in Miami’s • Secured key-fob entry access Convenience. -

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna Businesses searching for space in Miami's urban core have more options than they might think. While vacancy rates are down across the board, significant chunks of space are available in several Class A buildings in downtown and the Brickell Avenue financial district. "There are more alternatives available for those companies that take the time to appropriately investigate the market," said Chris Lovell, a senior managing director with Savills Studley in Miami. Leasing space on an upper floor with a view may be difficult since only six buildings on Brickell have a full floor above the 20th story available for lease. For tenants that can live without the view, there is plenty of open space to choose from. Four downtown Class A buildings have at least 75,000 square feet of contiguous space available, one Class A building on Brickell has a 65,000- square-foot block — "and we don't have tenants of that size standing in line to the claim the space," Lovell said. Savills Studley has found many of the large available blocks are in older downtown buildings. "You're always going to have buildings that are going to have certain pockets available," said Tere Blanca, founder of Miami-based Blanca Commercial Real Estate Inc. She said the market is responding well to the new Miami Central project, which is under construction with 60 percent of its office component pre- leased. The mixed-use development will serve as Brightline's downtown train station and will add 286,000 square feet of office space in two buildings. -

Insight from the Breakers

AUGUST 2018 | SFBWMAG.COM | $7.95 Insight from The Breakers CEO Plan an event On a Celebrity cruise, your team will enjoy premium event experiences, complimentary meeting spaces with state-of-the- that proves business art A/V equipment, world-class accommodations, distinctive restaurants with menus crafted by our Michelin-starred chef, can mix seamlessly and live entertainment throughout the ship. And, with more than with pleasure. 300 destinations on all seven continents, we open up a world of possibilities for your event—literally. Learn about our latest offers contact Joyce Lopez at (754) 317-3505 or [email protected] FOR THE 11TH CONSECUTIVE YEAR 2©2018 AUGUST Celebrity 2018 Cruises. • www.sfbwmag.com Ships' registry: Malta and Ecuador. Let Us Take a Look At Your Employee Benefits Needs! Arthur Novoseletsky Samantha Graveline Laura Sherwin Antonio Tavares Francisco Menendez Brown & Brown Benefit Consultants 1201 W. Cypress Creek Road, #130, Fort Lauderdale, FL 33309 954- 776-2222 1-800 648-9303 www.bbftlaud.com Medical Insurance – Level Funded / Fully Insured / Self-Funded Prescription Drug Dental Insurance Vision Insurance Disability Insurance – Short Term Disability / Long Term Disability Life Insurance Voluntary Programs Assistance with COBRA HR / Benefits Compliance Online Enrollment Technology www.sfbwmag.com • AUGUST 2018 3 WHERE BOUNDARIES ARE BROKEN PROJECT LAW FIRM MIAMI 4 AUGUST 2018 • www.sfbwmag.com WHERE BOUNDARIES ARE BROKEN 2818 Center Port Circle Pompano Beach, FL 33064 • P 954.735.8223 18288 Collins -

Miami Dade College and the Engaging Power of the Arts Eduardo J

© Journal of Higher Education Outreach and Engagement, Volume 17, Number 3, p. 69, (2013) Copyright © 2013 by the University of Georgia. All rights reserved. ISSN 1534-6104 Miami Dade College and the Engaging Power of the Arts Eduardo J. Padrón Abstract In this essay, the president of Miami Dade College describes the anchoring role that the institution plays in the Miami met- ropolitan region, with a particular emphasis on the many arts and cultural contributions. These efforts, combined with the economic and workforce development endeavors, make Miami Dade College a model anchor institution. he Cuban revolution unfolded throughout the 1950s, cul- minating on January 1, 1959, when Fidel Castro’s forces rolled into Havana and took control of the island nation. TIn the 2 years that followed, more than 200,000 Cubans landed in Miami, beginning a dramatic demographic change for South Florida (United States Census Bureau, 2012). In the ensuing years, additional waves of Cuban, Haitian, and other immigrants from Central and South America forever changed the landscape of South Florida. Another event occurred in 1959, in Miami, that would prove essential in providing a pathway to economic and social integra- tion for this enormous influx of new residents. The State of Florida gave formal approval to launch a new junior college in Miami. Classes opened in 1960 with 1,428 students. By 1967, Dade Junior College had become the largest institution of higher education in the state of Florida, enrolling more than 23,000 students. It was also the fastest growing junior college in the nation. It enrolled more freshmen than the University of Florida, Florida State University, and the University of South Florida combined. -

Miami Condos Most at Risk Sea Level Rise

MIAMI CONDOS MIAMI CONDOS MOST AT RISK www.emiami.condos SEA LEVEL RISE RED ZONE 2’ 3’ 4’ Miami Beach Miami Beach Miami Beach Venetian Isle Apartments - Venetian Isle Apartments - Venetian Isle Apartments - Island Terrace Condominium - Island Terrace Condominium - Island Terrace Condominium - Costa Brava Condominium - -Costa Brava Condominium - -Costa Brava Condominium - Alton Park Condo - Alton Park Condo - Alton Park Condo - Mirador 1000 Condo - Mirador 1000 Condo - Mirador 1000 Condo - Floridian Condominiums - Floridian Condominiums - Floridian Condominiums - South Beach Bayside Condominium - South Beach Bayside Condominium - South Beach Bayside Condominium - Portugal Tower Condominium - Portugal Tower Condominium - Portugal Tower Condominium - La Tour Condominium - La Tour Condominium - La Tour Condominium - Sunset Beach Condominiums - Sunset Beach Condominiums - Sunset Beach Condominiums - Tower 41 Condominium - Tower 41 Condominium - Tower 41 Condominium - Eden Roc Miami Beach - Eden Roc Miami Beach - Eden Roc Miami Beach - Mimosa Condominium - Mimosa Condominium - Mimosa Condominium - Carriage Club Condominium - Carriage Club Condominium - Carriage Club Condominium - Marlborough House - Marlborough House - Marlborough House - Grandview - Grandview - Grandview - Monte Carlo Miami Beach - Monte Carlo Miami Beach - Monte Carlo Miami Beach - Sherry Frontenac - Sherry Frontenac - Sherry Frontenac - Carillon - Carillon - Carillon - Ritz Carlton Bal Harbour - Ritz Carlton Bal Harbour - Ritz Carlton Bal Harbour - Harbor House - Harbor House -

Brickell Flatiron Brochure ENGLISH.Pdf

Patricio Javier Orloff, P.A. Cervera Real Estate Miami: 305.726.8155 Buenos Aires: 11.5129.6649 [email protected] www.flatironbrickellmiami.com ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING THE REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. BRICKELL FLATIRON ENVISIONING A LANDMARK Refreshing the Miami Skyline Presenting a new paradigm in luxurious living. Downtown Miami’s hottest neighborhood celebrates a property that represents a true architectural icon. Brickell Flatiron is an urban oasis developed by Ugo Colombo's CMC Group and designed by Luis RevueltaRI Revuelta Architecture International: the tower of soaring glass is defined by its sweeping exposures, which punctuate its romantic renaissance- revival interiors. Artist's Rendering Artist's Rendering BRICKELL FLATIRON BRICKELL FLATIRON BRICKELL A Lively Composition of Commerce and Culture. As Miami’s Financial District, Brickell remains a sophisticated and culturally significant community packed with creative types and tastemakers of every stripe. BRICKELL FLATIRON LOCATION A Walk-around Neighborhood BRICKELL FLATIRON Located in the heart of Downtown Miami, Brickell Flatiron is ideally situated within walking distance of Mary Brickell Village and Brickell City Centre — offering residents unparalleled access to a wide array of fashionable conveniences — with picturesque sidewalk cafés, fine dining, shopping, markets, outdoor and cultural activities along the way. BRICKELL FLATIRON Artist's Rendering BRICKELL FLATIRON A More Playful Line Brickell Flatiron’s innovative architectural design introduces flowing curvilinear forms to accommodate spacious floor plans. -

Locator Keys Identify Sites on This Map, 23 Heading NW from the Confluence of the P Miami River and Biscayne Bay

A NOTE USING THIS GUIDE… Locator keys identify sites on this map, 23 heading NW from the confluence of the P Miami River and Biscayne Bay. Locator keys are in one of the following four 21 categories: HISTORIC SITES: Blue numbers 22 RIVER BRIDGES: Blue letters POINTS OF INTEREST: Green numbers AREA BUSINESSES: Red numbers MIAMI RIVER BRIDGE Bascule (B); Fixed (F) 3 Brickell Bridge (B) . A 19 27 Metro Mover Bridge (F) . B South Miami Avenue (B) . C 2021 O Metrorail (F) . .D S .W . 2nd Avenue (B) . E Interstate I-95 (3F) . F 14 N S .W . First Street (B) . G West Flagler Street (B) . .H 15 N .W . 5th Street (B) . I 24 N .W . 12th Avenue (B) . J 18 19 S .R . 836/Dolphin Expwy . (F) . K 16 14 N .W . 17th Avenue (B) . L M 12 N .W . 22nd Avenue (B) . M 13 N .W . 27th Avenue (B) . N 16 N .W . South River Dr . (B) . O Railroad (B) . P 12 13 L 32 30 POINTS OF INTEREST 4 Beginning of Miami River Greenway . 1 K 10 34 27 James L . Knight Convention Center . 2 J Metro-Mover “Fifth Street” Station .3 26 34 11 Metro-Mover “Riverwalk” Station . 4 MIAMI RIVER BUSINESSES 22 12 Metro-Rail “Brickell” Station . 5 1 5TH STREET MARINA 11 DOWNTOWN DEVELOPMENT AUTHORITY 21 MARITIME AGENCY INC 32 RIVER LANDING Miami-Dade Cultural Center . 6 Marina To grow, strengthen & promote Downtown Miami International Shipping Terminal Retail, Restaurants, Residential 341 NW South River Dr. Miami 33128 (305) 579-6675 3630 NW North River Dr. -

Curriculum Vitae

Curriculum Vitae JEFF CHOOPANI AIA HIGHER EDUCATION Institutional: Florida International Bachelor of Architectural Technology 1988 (Civil Engineering Minor) West Stark Community College Ft Smith, Arkansas Associate in Arts 1979 Certifications: Post-Disaster Safety Assessment Evaluator Training 2009 Members: (AIA) American Institute of Architects (ASTM) American Society for Testing and Materials (BOMA) Building Owners and Managers Association EXPERIENCE QUALIFICATIONS. Knowledgeable and experienced within all aspects of Exterior Wall (Structural and Conventional Panel Systems, Stick Systems, Doors, Windows, Storefronts and Masonry Systems. With over 20 years of experience in providing Exterior Wall Testing Laboratory services inspections. I have 12 years of experience in waterproofing systems (above and below grade); concrete restoration and exterior field applied insulated finishes systems (convention or panel systems). PROFESSIONAL Miami Curtain Wall Consultants, Corp Current Principal, Senior Consultant, Founding Member Client Representative: Produce specifications for the exterior (i.e., Curtain walls, window walls, cladding, masonry, masonry/ stone composite walls) for project construction documents. Provide a full range of Quality Control Procedures on significant buildings. Organized and coordinated the quality control procedures utilized on building systems for manufacturing, delivery, final erection and testing. Witnessed construction of full scale project mock-ups and issued test reports. Provided remedial solutions to problems during testing that where later implemented in buildings already under construction. Reviewed architectural and shop drawings for inadequacies in the areas of water penetration, condensation, vapor penetration, anti-terrorism, and structural performance during design development and construction document phase of projects. Supervised inspections conducted daily in the field and shop. Observed and recorded day to day operations between architects, engineers and contractors. -

Greater Downtown Miami Annual Residential Market Study Update

Greater Downtown Miami Annual Residential Market Study Update Prepared for the Miami Downtown Development Authority (DDA) by Integra Realty Resources (IRR) February 2016 Greater Downtown Miami Annual Residential Market Study Update Prepared for the Miami Downtown Development Authority (DDA) by Integra Realty Resources (IRR) February 2016 For more information, please contact IRR-Miami/Palm Beach The Douglas Centre 2600 Douglas Road, Suite 801 Coral Gables, FL 33134 305-670-0001 [email protected] Contents 2 Key Q1 2016 Conclusions 5 Greater Downtown Miami Market Submarket Map 6 Greater Downtown Miami Condo Pipeline 7 Greater Downtown Miami Market Sizing 8 Greater Downtown Miami Market Condo Delivery and Absorption of Units 10 Current Selling Projects 11 Analysis of Resale 12 Current Resale vs. New Product Pricing $/SF 13 Presale Absorption 14 Currency Exchange and Purchasing Power 16 Submarket Analysis 21 Market Drivers 22 Major Market Comparison 23 Residential Rental Activity 26 Conventional Rental Market Supply 28 Land Prices Trends 30 Occupancy 31 Leverage Analysis 33 Conclusion 34 Condo Development Process Appendix Key Q1 2016 Conclusions Integra Realty Resources – Miami/Palm Beach (IRR-Miami) is pleased to present the following Residential Real Estate Market Study within the Miami Downtown Development Authority’s (Miami DDA) market area, defined as the Greater Downtown Miami market. This report updates IRR-Miami’s findings on the local residential real estate market through January 2016. Findings from this year’s annual study are outlined as follows: • New product preconstruction pricing responded to a slower 2015 selling season. Projects which were 80% or more sold-out by Q1-2015 raised prices on average 5%-15%, and projects which were less than 80% sold out dropped pricing or increased broker incentives, or both, to increase market Millicento share. -

City of Miami Office of Zoning in Compliance with the Miami

CITY OF MIAMI OFFICE OF ZONING IN COMPLIANCE WITH THE MIAMI NEIGHBORHOOD COMPREHENSIVE PLAN AND MIAMI 21, NOTICE OF APPLICATION AND FINAL DECISION FOR WAIVERS IS ISSUED FOR THE FOLLOWING ITEMS: THE FINAL DECISION OF THE ZONING ADMINISTRATOR MAY BE APPEALED TO THE PLANNING, ZONING AND APPEALS BOARD BY ANY AGGRIEVED PARTY, WITHIN FIFTEEN (15) DAYS OF THE DATE OF THE POSTING OF THE DECISION TO THIS WEBSITE BY FILING A WRITTEN APPEAL AND APPROPRIATE FEE WITH THE OFFICE OF HEARING BOARDS, LOCATED AT 444 SW 2ND AVENUE 3rd Floor, MIAMI, FL 33130. TEL. (305) 416-2030 Final Decision Waiver Transect Date of First App. Referral Final Decision Name Address NET Area Use Addt. Referral cannot be issued Status Number Zone Notice Received Date (Issuance) Date prior to: South/West 2013-0084 4215 Braganza 4215 Braganza Demolition 12/4/2013 11/8/2013 11/22/2013 FG 1/4/2014 1/4/2014 Approved with Conditions Coconut Grove NE Coconut single family 2013-0073 2250 Overbrook 2250 Overbrook 11/1/2013 9/11/2013 n/a MDL 12/1/2013 1/14/2014 Approved w/Conditions. Grove residential 2013-0069 Premier 850 S Miami Av Downtown Multifamily 10/8/2013 6/18/2013 10/1/2013 PS 11/8/2013 Approved w/Conditions. 1/17/2014 Presidente Supermarket No. 2014-2001 1/27/2014 1/23/2014 1/23/2014 FG 2/28/2014 In progress 34 North/East 2013-0088 Coconut Grove Duplex 2930 Catalina St Demolition 12/17/2013 11/14/2013 12/10/2013 PS 1/17/2014 1/23/2014 Approved w/Conditions.