Issues Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pocketbook for You, in Any Print Style: Including Updated and Filtered Data, However You Want It

Hello Since 1994, Media UK - www.mediauk.com - has contained a full media directory. We now contain media news from over 50 sources, RAJAR and playlist information, the industry's widest selection of radio jobs, and much more - and it's all free. From our directory, we're proud to be able to produce a new edition of the Radio Pocket Book. We've based this on the Radio Authority version that was available when we launched 17 years ago. We hope you find it useful. Enjoy this return of an old favourite: and set mediauk.com on your browser favourites list. James Cridland Managing Director Media UK First published in Great Britain in September 2011 Copyright © 1994-2011 Not At All Bad Ltd. All Rights Reserved. mediauk.com/terms This edition produced October 18, 2011 Set in Book Antiqua Printed on dead trees Published by Not At All Bad Ltd (t/a Media UK) Registered in England, No 6312072 Registered Office (not for correspondence): 96a Curtain Road, London EC2A 3AA 020 7100 1811 [email protected] @mediauk www.mediauk.com Foreword In 1975, when I was 13, I wrote to the IBA to ask for a copy of their latest publication grandly titled Transmitting stations: a Pocket Guide. The year before I had listened with excitement to the launch of our local commercial station, Liverpool's Radio City, and wanted to find out what other stations I might be able to pick up. In those days the Guide covered TV as well as radio, which could only manage to fill two pages – but then there were only 19 “ILR” stations. -

Hallett Arendt Rajar Topline Results - Wave 3 2019/Last Published Data

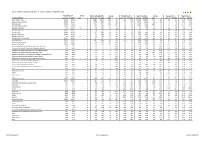

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2019/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W3 2019 000's % Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 Bauer Radio - Total 55032 55032 0 0% 18083 18371 288 2% 33% 33% 156216 158995 2779 2% 8.6 8.7 15.3% 15.9% Absolute Radio Network 55032 55032 0 0% 4743 4921 178 4% 9% 9% 35474 35522 48 0% 7.5 7.2 3.5% 3.6% Absolute Radio 55032 55032 0 0% 2151 2447 296 14% 4% 4% 16402 17626 1224 7% 7.6 7.2 1.6% 1.8% Absolute Radio (London) 12260 12260 0 0% 729 821 92 13% 6% 7% 4279 4370 91 2% 5.9 5.3 2.1% 2.2% Absolute Radio 60s n/p 55032 n/a n/a n/p 125 n/a n/a n/p *% n/p 298 n/a n/a n/p 2.4 n/p *% Absolute Radio 70s 55032 55032 0 0% 206 208 2 1% *% *% 699 712 13 2% 3.4 3.4 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1779 1824 45 3% 3% 3% 9294 9435 141 2% 5.2 5.2 0.9% 1.0% Absolute Radio 90s 55032 55032 0 0% 907 856 -51 -6% 2% 2% 4008 3661 -347 -9% 4.4 4.3 0.4% 0.4% Absolute Radio 00s n/p 55032 n/a n/a n/p 209 n/a n/a n/p *% n/p 540 n/a n/a n/p 2.6 n/p 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 741 721 -20 -3% 1% 1% 3438 3703 265 8% 4.6 5.1 0.3% 0.4% Hits Radio Brand 55032 55032 0 0% 6491 6684 193 3% 12% 12% 53184 54489 1305 2% 8.2 8.2 5.2% 5.5% Greatest Hits Network 55032 55032 0 0% 1103 1209 106 10% 2% 2% 8070 8435 365 5% 7.3 7.0 0.8% 0.8% Greatest Hits Radio 55032 55032 0 0% 715 818 103 14% 1% 1% 5281 5870 589 11% 7.4 7.2 0.5% -

Great Yarmouth & Lowestoft

Analogue Commercial Radio Licence: Format Change Request Form Date of request: 25 April 2017 Station Name: The Beach Licensed area and licence Great Yarmouth and Lowestoft number: AL100585BA/2 Licensee: Celador Radio Broadcasting Ltd Contact name: Paul Smith Details of requested change(s) to Format Character of Service Existing Character of Service: Complete this section if you are requesting a change to this part of your Format Proposed new Character of Service: Programme sharing and/or Current arrangements: co-location arrangements The Beach will share all programming with Complete this section if North Norfolk Radio and Radio Norwich. They you are requesting a will locate at the Radio Norwich premises in change to this part of your Norwich NR7 0EE where all weekday peak Format hours 0600-1900 and weekend peak hours 0800-1200 will be made. Proposed new arrangements: The Beach may share all programming with Radio Norwich, North Norfolk Radio, Town 102, or Dream 100, with the service originating from Radio Norwich. Locally-made hours and/or Current obligations: local news bulletins Locally made hours: Complete this section if At least 10 hours a day during daytime you are requesting a weekdays (must include Breakfast). change to this part of your At least 4 hours daytime Saturdays and Format Sundays. Local news bulletins: Hourly at peaktime weekdays and weekends. Outside peak, UK-wide, national and international news should feature. Proposed new obligations: Locally made hours: At least 7 hours a day during daytime weekdays (must include Breakfast). At least 4 hours daytime Saturdays and Sundays. Local news bulletins: At least hourly during weekday daytime and at peaktime weekends. -

Bauer Media Group Phase 1 Decision

Completed acquisitions by Bauer Media Group of certain businesses of Celador Entertainment Limited, Lincs FM Group Limited and Wireless Group Limited, as well as the entire business of UKRD Group Limited Decision on relevant merger situation and substantial lessening of competition ME/6809/19; ME/6810/19; ME/6811/19; and ME/6812/19 The CMA’s decision on reference under section 22(1) of the Enterprise Act 2002 given on 24 July 2019. Full text of the decision published on 30 August 2019. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties or third parties for reasons of commercial confidentiality. SUMMARY 1. Between 31 January 2019 and 31 March 2019 Heinrich Bauer Verlag KG (trading as Bauer Media Group (Bauer)), through subsidiaries, bought: (a) From Celador Entertainment Limited (Celador), 16 local radio stations and associated local FM radio licences (the Celador Acquisition); (b) From Lincs FM Group Limited (Lincs), nine local radio stations and associated local FM radio licences, a [] interest in an additional local radio station and associated licences, and interests in the Lincolnshire [] and Suffolk [] digital multiplexes (the Lincs Acquisition); (c) From The Wireless Group Limited (Wireless), 12 local radio stations and associated local FM radio licences, as well as digital multiplexes in Stoke, Swansea and Bradford (the Wireless Acquisition); and (d) The entire issued share capital of UKRD Group Limited (UKRD) and all of UKRD’s assets, namely ten local radio stations and the associated local 1 FM radio licences, interests in local multiplexes, and UKRD’s 50% interest in First Radio Sales (FRS) (the UKRD Acquisition). -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 15Th September 2019

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 15th September 2019 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 55,032,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48537 88 18.0 20.4 989221 100.0 All BBC Radio Q 33451 61 8.9 14.6 488274 49.4 All BBC Radio 15-44 Q 12966 51 4.6 8.9 115944 33.9 All BBC Radio 45+ Q 20485 69 12.5 18.2 372330 57.5 All BBC Network Radio1 Q 30828 56 7.7 13.8 425563 43.0 BBC Local Radio Q 7430 14 1.1 8.4 62711 6.3 All Commercial Radio Q 35930 65 8.6 13.2 475371 48.1 All Commercial Radio 15-44 Q 17884 71 8.5 12.0 214585 62.7 All Commercial Radio 45+ Q 18046 61 8.8 14.5 260786 40.3 All National Commercial1 Q 22361 41 3.8 9.5 211324 21.4 All Local Commercial (National TSA) Q 25988 47 4.8 10.2 264047 26.7 Other Radio Q 4035 7 0.5 6.3 25577 2.6 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 24th October 2019 information for the purposes of the Criminal Justice Act 1993. -

Codes Used in D&M

CODES USED IN D&M - MCPS A DISTRIBUTIONS D&M Code D&M Name Category Further details Source Type Code Source Type Name Z98 UK/Ireland Commercial International 2 20 South African (SAMRO) General & Broadcasting (TV only) International 3 Overseas 21 Australian (APRA) General & Broadcasting International 3 Overseas 36 USA (BMI) General & Broadcasting International 3 Overseas 38 USA (SESAC) Broadcasting International 3 Overseas 39 USA (ASCAP) General & Broadcasting International 3 Overseas 47 Japanese (JASRAC) General & Broadcasting International 3 Overseas 48 Israeli (ACUM) General & Broadcasting International 3 Overseas 048M Norway (NCB) International 3 Overseas 049M Algeria (ONDA) International 3 Overseas 58 Bulgarian (MUSICAUTOR) General & Broadcasting International 3 Overseas 62 Russian (RAO) General & Broadcasting International 3 Overseas 74 Austrian (AKM) General & Broadcasting International 3 Overseas 75 Belgian (SABAM) General & Broadcasting International 3 Overseas 79 Hungarian (ARTISJUS) General & Broadcasting International 3 Overseas 80 Danish (KODA) General & Broadcasting International 3 Overseas 81 Netherlands (BUMA) General & Broadcasting International 3 Overseas 83 Finnish (TEOSTO) General & Broadcasting International 3 Overseas 84 French (SACEM) General & Broadcasting International 3 Overseas 85 German (GEMA) General & Broadcasting International 3 Overseas 86 Hong Kong (CASH) General & Broadcasting International 3 Overseas 87 Italian (SIAE) General & Broadcasting International 3 Overseas 88 Mexican (SACM) General & Broadcasting -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 25Th June 2017

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 25th June 2017 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 54,466,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 49206 90 19.0 21.0 1033226 100.0 All BBC Radio Q 34945 64 9.9 15.5 539982 52.3 All BBC Radio 15-44 Q 14249 56 5.7 10.2 144999 38.0 All BBC Radio 45+ Q 20696 71 13.6 19.1 394983 60.6 All BBC Network Radio1 Q 32136 59 8.5 14.5 464642 45.0 BBC Local Radio Q 8632 16 1.4 8.7 75340 7.3 All Commercial Radio Q 35881 66 8.5 13.0 464812 45.0 All Commercial Radio 15-44 Q 18510 73 8.8 12.0 222329 58.3 All Commercial Radio 45+ Q 17371 60 8.3 14.0 242483 37.2 All National Commercial1 Q 19905 37 3.2 8.7 172369 16.7 All Local Commercial (National TSA) Q 27277 50 5.4 10.7 292443 28.3 Other Radio Q 3903 7 0.5 7.3 28431 2.8 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 3rd August 2017 information for the purposes of the Criminal Justice Act 1993. -

Small Scale DAB Licensing Consultation: Responses Received

Small Scale DAB Licensing consultation: Responses received October 2018 1 List of respondents A total of 87 responses were received from members of the public, and individuals and organisations working within a variety of sectors. Of the respondents, one has requested anonymity and therefore has not been listed. 1. Neil Kipling 46. Muxco 2. Iain Gowers 47. Tone FM 3. Rodney Maxwell 48. John Goodman 4. Paul Holmes 49. Celador 5. Peter Allridge 50. Global 6. Colin Marks 51. Mark O’Reilly 7. David Dbs 52. Niocast Digital 8. Steve Fox 53. Services Sound and Vision (SSVC) 9. Alec Thomas 54. Colonel J G Robinson Brigade of 10. Martin James Gurkhas 11. Penistone Community Radio 55. Buchan Radio 12. Graham Phillips 56. Resonance FM 13. Takeover Radio 57. Quidem Radio Group 14. Dave Hurford 58. The Flash 15. Radio Verulam 59. Bauer Media Group 16. Phonic FM 60. Alternative Broadcast Company 17. Chris Dawson 61. KMFM 18. Biggles FM 62. Nation Broadcasting 19. Maxxwave 63. DigiLink Connect 20. Moss Media 64. Wireless Group 21. Coast Digital Radio 65. DC Thomson Media 22. UKRD 66. 100% Media Group 23. BBC 67. Brighton and Hove Radio Ltd 24. Heart of Nation Broadcasting 68. Radiate ideas 25. 6 Towns Radio 69. Radiocentral24 26. The Source FM 70. Daniel Rose 27. Martin Steers 71. UDAB 28. Uckfield FM 72. Future Digital Norfolk 29. Seahaven FM 73. Radio Reverb 30. Marc Webber 74. Radiocentre 31. Kingdom FM 75. Arqiva 32. Digital Radio Mondiale Consortium 76. Community Media Association 33. Lincs FM Group 77. MKFM 34. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 23Rd June 2019

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 23rd June 2019 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 55,032,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48788 89 18.4 20.8 1014982 100.0 All BBC Radio Q 34080 62 9.1 14.7 500172 49.3 All BBC Radio 15-44 Q 13333 53 4.8 9.2 122149 34.2 All BBC Radio 45+ Q 20748 70 12.7 18.2 378023 57.5 All BBC Network Radio1 Q 31474 57 8.0 14.0 440318 43.4 BBC Local Radio Q 7593 14 1.1 7.9 59855 5.9 All Commercial Radio Q 36147 66 8.9 13.5 487215 48.0 All Commercial Radio 15-44 Q 17965 71 8.8 12.3 221568 62.0 All Commercial Radio 45+ Q 18182 61 8.9 14.6 265647 40.4 All National Commercial1 Q 22656 41 3.8 9.3 211650 20.9 All Local Commercial (National TSA) Q 25762 47 5.0 10.7 275565 27.1 Other Radio Q 3927 7 0.5 7.0 27595 2.7 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 1st August 2019 information for the purposes of the Criminal Justice Act 1993. -

Town FM Application

General information (a) Name of Applicant, Address, Telephone and E-mail Note for new applicants: This must be a single legal entity: either a body corporate or a named individual person. If the former, a copy of the certificate of incorporation must be included with the application. Town FM Limited Address: 12 Alpha Business Park White House Road Ipswich IP1 5LT Telephone: 01603 703300 E-mail: [email protected] (b) Main Contact (For Public Purposes) Please nominate at least one individual to deal with any press or public enquiries, stating: Name: Phil Caborn Telephone (daytime): 01603 703300 Address: 12 Alpha Business Park, White House Road, Ipswich, IP1 5LT E-mail: [email protected] (c) Station Name (if decided) Town FM (d) Main Contact (For Ofcom Purposes) Please nominate one individual to whom questions of clarification and/or amplification should be sent, stating: Name: Richard Johnson Address: Celador Radio, County Gates, Ashton Road, Bristol, BS3 2JH E-mail: [email protected] This information may be submitted in confidence, separately from the other responses in this section. 1 Section 105(A): Ability to maintain proposed service 1. Ownership and control of company which will operate the licence (a) Board of Directors i) Provide the name, occupation, other directorships, other media interests, and, if not a director of an existing Ofcom radio licensee, the relevant media experience, of each director (executive and non-executive), including the proposed chairperson. Town FM – a local station underpinned by experience and passion For a small station, we recognise this is a big board. It is the board of Celador Radio with the addition of two local directors. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 17Th December 2017

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 17th December 2017 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 54,466,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48860 90 19.1 21.3 1038816 100.0 All BBC Radio Q 35019 64 10.1 15.7 548937 52.8 All BBC Radio 15-44 Q 13938 55 5.5 9.9 138350 36.5 All BBC Radio 45+ Q 21081 72 14.1 19.5 410588 62.3 All BBC Network Radio1 Q 32242 59 8.7 14.7 472924 45.5 BBC Local Radio Q 8297 15 1.4 9.2 76013 7.3 All Commercial Radio Q 35466 65 8.4 13.0 459392 44.2 All Commercial Radio 15-44 Q 17977 71 8.9 12.6 225773 59.5 All Commercial Radio 45+ Q 17489 60 8.0 13.4 233620 35.4 All National Commercial1 Q 20254 37 3.3 8.8 177508 17.1 All Local Commercial (National TSA) Q 26532 49 5.2 10.6 281885 27.1 Other Radio Q 3815 7 0.6 8.0 30486 2.9 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 8th February 2018 information for the purposes of the Criminal Justice Act 1993. -

Bauer Radio Stations in the South and West of England Request to Modify Approved Areas

Bauer Radio stations in the south and west of England Request to modify approved areas CONSULTATION: Publication Date: 25 September 2020 Closing Date for Responses: 23 October 2020 Contents Section 1. Overview 1 2. Details and background information 2 3. Consideration of the requests 5 Annex Responding to this consultation 6 Ofcom’s consultation principles 8 Consultation coversheet 9 Consultation question 10 Bauer Radio’s request relating to the south and west of England 11 Bauer Radio stations in the south and west of England – request to modify an approved area 1. Overview Most local analogue commercial radio stations are required to produce a certain number of hours of locally-made programming. Under legislation passed in 2010, these stations are not only able to broadcast their locally-made hours from within their licence area, but may instead broadcast from studios that are based within a larger area approved by Ofcom. These wider areas are known as ‘approved areas’. Stations can also share their local hours of programming with other stations located in the same approved area. Ofcom has approved an area for every local radio licence in the UK, to give stations more flexibility in their broadcasting arrangements. However, a licensee can ask Ofcom to approve a bespoke area, since the statutory framework allows for an approved area in relation to each local analogue service. What we are consulting on – in brief Bauer Radio has asked Ofcom to move the Shaftesbury local FM licence from the existing ‘South West England (Bauer)’ approved area into the ‘South of England (Bauer)’ approved area.