Office Sprawl: the Evolving Geography of Business Robert E

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fuori Le Mura: the Productive Compartmentaliztion of the Megalopolis

Fuori le Mura: The productive compartmentaliztion of the megalopolis Joshua Stein Woodbury University Fuori le Mura is a radical speculative proposal provoking inquiry into right- sizing the contemporary megalopolis. Through a size comparison of vari- ous urban configurations with strictly defined perimeter boundaries, from the Italian city-state to the urban growth boundaries exemplified in con- temporary cities like Portland, OR, a cohesive urban identity and scale is The Walled City defined. Could “walled” mega-enclaves (scaled to match the ideal city size Medieval Siena’s wall operates as more than a simple fortification against the outside of Portland) create manageable urban nodes with a territory of free experi- world. Instead it fosters a complex negotiation between the extra-urban activities still very much networked to those inside the walls. mentation replacing suburbia. Fuori le Mura—Outside the Walls—is a proposal for Los Angeles that draws a dividing line between two complementary modes of living, rein- stating the historical concept of Urbs vs. Rure. No longer prolonging the corrosive dynamic between City and Suburb, where the suburb is simul- taneously culturally subservient to the city and parasitic in its consump- tion of resources, Fuori le Mura instead proposes two different modes of sustainable development and resource management that operate in par- allel. Outside the walls the ultimate fantasy of “no government” prevails— the obvious repercussions being the lack of infrastructure or utilities. The only dictates outside the walls are proscriptive: no impact/no emissions. Beyond this anything is possible. Within the walls infrastructure and utili- ties are heavily regulated, providing inhabitants with easy, prescriptive models for sustainable living. -

The Hub's Metropolis: a Glimpse Into Greater Boston's Development

James C. O’Connell, “The Hub’s Metropolis: Greater Boston’s Development” Historical Journal of Massachusetts Volume 42, No. 1 (Winter 2014). Published by: Institute for Massachusetts Studies and Westfield State University You may use content in this archive for your personal, non-commercial use. Please contact the Historical Journal of Massachusetts regarding any further use of this work: [email protected] Funding for digitization of issues was provided through a generous grant from MassHumanities. Some digitized versions of the articles have been reformatted from their original, published appearance. When citing, please give the original print source (volume/ number/ date) but add "retrieved from HJM's online archive at http://www.wsc.ma.edu/mhj. 26 Historical Journal of Massachusetts • Winter 2014 Published by The MIT Press: Cambridge, MA, 7x9 hardcover, 326 pp., $34.95. To order visit http://mitpress.mit.edu/books/hubs-metropolis 27 EDITor’s choicE The Hub’s Metropolis: A Glimpse into Greater Boston’s Development JAMES C. O’CONNELL Editor’s Introduction: Our Editor’s Choice selection for this issue is excerpted from the book, The Hub’s Metropolis: Greater Boston’s Development from Railroad Suburbs to Smart Growth (Cambridge, MA: The MIT Press, 2013). All who live in Massachusetts are familiar with the compact city of Boston, yet the history of the larger, sprawling metropolitan area has rarely been approached as a comprehensive whole. As one reviewer writes, “Comprehensive and readable, James O’Connell’s account takes care to orient the reader in what is often a disorienting landscape.” Another describes the book as a “riveting history of one of the nation’s most livable places—and a roadmap for how to keep it that way.” James O’Connell, the author, is intimately familiar with his topic through his work as a planner at the National Park Service, Northeast Region, in Boston. -

Satellite Towns

24 Satellite Towns Introduction 'Satellite town' was a term used in the year immediately after the World War I as an alternative to Garden City. It subsequently developed a much wider meaning to include any town that is closely related to or dependent on a larger city. The first specific usage of the word ‘satellite town’ was in 1915 by G.R. Taylor in ‘ Satellite Cities’ referring to towns around Chicago, St. Louis and other American cities where industries had escaped congestion and crafted manufacturer’s town in the surrounding area. The new town is planned and built to serve a particular local industry, or as a dormitory or overspill town for people who work in and nearby metropolis. Satellite Town, can also be defined as a town which is self contained and limited in size, built in the vicinity of a large town or city and houses and employs those who otherwise create a demand for expansion of the existing settlement, but dependent on the parent city to some extent for population and major services. A distinction is made between a consumer satellite (essentially a dormitory suburb with few facilities) and a production satellite (with a capacity for commercial, industrial and other production distinct from that of the parent town, so a new town) town or satellite city is a concept of urban planning and referring to a small or medium-sized city that is near a large metropolis, but predates that metropolis suburban expansion and is atleast partially independent from that metropolis economically. CITIES, URBANISATION AND URBAN SYSTEMS 414 Satellite and Dormitory Towns The suburb of an urban centre where due to locational advantage the residential, industrial and educational centres are developed are known as "satellite or dormitory towns." It has a benefit of providing clean environment and spacious ground for residential and industrial expansion. -

![City Against Suburb: the Culture Wars in an American Metropolis [Book Review]](https://docslib.b-cdn.net/cover/5978/city-against-suburb-the-culture-wars-in-an-american-metropolis-book-review-285978.webp)

City Against Suburb: the Culture Wars in an American Metropolis [Book Review]

Haverford College Haverford Scholarship Faculty Publications Political Science 2001 City Against Suburb: The Culture Wars in an American Metropolis [book review] Stephen J. McGovern Haverford College, [email protected] Follow this and additional works at: https://scholarship.haverford.edu/polisci_facpubs Repository Citation McGovern, Stephen. City Against Suburb: The Culture Wars in an American Metropolis, Joseph A. Rodriguez, Pacific Historical Review, 70(2): 332-334, May 2001. This Book Review is brought to you for free and open access by the Political Science at Haverford Scholarship. It has been accepted for inclusion in Faculty Publications by an authorized administrator of Haverford Scholarship. For more information, please contact [email protected]. Reviews of Books Pacific Historical Review, Vol. 70, No. 2 (May 2001), pp. 304-351 Published by: University of California Press Stable URL: http://www.jstor.org/stable/10.1525/phr.2001.70.2.304 . Accessed: 29/03/2013 12:19 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. University of California Press is collaborating with JSTOR to digitize, preserve and extend access to Pacific Historical Review. http://www.jstor.org This content downloaded from 165.82.168.47 on Fri, 29 Mar 2013 12:19:39 PM All use subject to JSTOR Terms and Conditions Reviews of Books The World That Trade Created: Society, Culture, and the World Economy, 1400 to the Present . -

MEGALOPOLIS MEGALOPOLIS Megalopolis at Night

3/7/2013 MEGALOPOLIS • Term used to describe any large urban Regional Landscapes of the area created by the growth toward each United States and Canada other and eventual merging of two or MEGALOPOLIS more cities. • The French geographer Jean Gottman Prof. Anthony Grande adopted the term in 1961 for the title of his ©AFG 2013 book, “Megalopolis: The Urbanized Northeastern Seaboard of the United States.” Megalopolis Megalopolis at Night When used with a capital “M”, the term denotes the almost unbroken urban Megalopolis development that extends extends over 500 from north of Boston, MA miles from the to counties south of Wash- northern fringe of ington, DC (from Portsmouth, the Boston metro Boston NH approaching Richmond, VA). area (in NH) to Washington, DC New York City metro area. With a lower case “m” the Philadelphia term is applied to any string Some people have of adjoining very large it extending to Baltimore cities. Richmond, VA. Washington Richmond 4 LANDSCAPES of Megalopolis From the beginning: SETTLEMENT Includes large cities, small towns and rural areas where most of the A place where one people reside in an urban place. person or a group of people live. Settlements are differentiated on the basis of size = number of people present spacing = distance from each other function = reason for people grouping there 6 1 3/7/2013 HIERARCHY of SETTLEMENT HIERARCHY of SETTLEMENT The smallest settlements are greatest in number As the number of settlers (people) and located relatively close to each other. They increase from the single provide residents with basic necessities. dwelling (house ) to hamlet (group The larger settlements (cities) are more complicated, offer variety of goods and services of houses) to village to town to and are located at greater distances from each city, a hierarchy of form and other. -

Located in Downtown Narberth Picturesque Suburb Environment Ideally Located Within Walking Distance to Many, Restaurants, Shops

274 SF - Single Office 1,053 SF - 3 Private Offices, Private Bathroom 1,200 SF - 2 Private Offices, Large Open Office, Private Bathroom, Deck site 1,419 SF - 1 Private Office, Fully Furnished Open Office, Private Bathroom Located in downtown Narberth Picturesque Suburb Environment Ideally located within walking distance to many, restaurants, shops and local business Septa’s Paoli/Thorndale line located just 350 ft. away. Easily accessible to I-76, 476, the PA Turnpike and 422 Michael Willner 33 Rock Hill Road, Suite 350 Phone: (610) 658-7070 Bala Cynwyd, PA 19004 E-Mail: [email protected] The Best Little Office Buildings in Narberth are located on Forrest Avenue in Narberth Borough. It encompasses a string of four historic buildings that were converted into offices. There are various sized suites available with each being unique. These offices are ideal for the entrepreneur looking to service main line residents or a larger scale operation looking for up to 2,500 SF on one floor. Parking is available but is limited due to the nature of the downtown. Narberth Borough is located within Lower Merion Township in Montgomery County. It' s on the western edge of the City of Philadelphia on the Main Line, a sequence of picturesque suburbs that extend from Philadelphia along the Pennsylvania Railroad. Montgomery Avenue runs along the borough's northern border making it easily accessible to I-76, 476, the PA Turnpike and 422. Septa' s Paoli/ Thorndale line services Narberth with a train station located in the center of Town. By utilizing the train, patrons can access center city Philadelphia within 19 minutes. -

Alpha ELT Listing

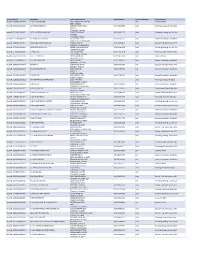

Lienholder Name Lienholder Address City State Zip ELT ID 1ST ADVANTAGE FCU PO BX 2116 NEWPORT NEWS VA 23609 CFW 1ST COMMAND BK PO BX 901041 FORT WORTH TX 76101 FXQ 1ST FNCL BK USA 47 SHERMAN HILL RD WOODBURY CT 06798 GVY 1ST LIBERTY FCU PO BX 5002 GREAT FALLS MT 59403 ESY 1ST NORTHERN CA CU 1111 PINE ST MARTINEZ CA 94553 EUZ 1ST NORTHERN CR U 230 W MONROE ST STE 2850 CHICAGO IL 60606 GVK 1ST RESOURCE CU 47 W OXMOOR RD BIRMINGHAM AL 35209 DYW 1ST SECURITY BK WA PO BX 97000 LYNNWOOD WA 98046 FTK 1ST UNITED SVCS CU 5901 GIBRALTAR DR PLEASANTON CA 94588 W95 1ST VALLEY CU 401 W SECOND ST SN BERNRDNO CA 92401 K31 360 EQUIP FIN LLC 300 BEARDSLEY LN STE D201 AUSTIN TX 78746 DJH 360 FCU PO BX 273 WINDSOR LOCKS CT 06096 DBG 4FRONT CU PO BX 795 TRAVERSE CITY MI 49685 FBU 777 EQUIPMENT FIN LLC 600 BRICKELL AVE FL 19 MIAMI FL 33131 FYD A C AUTOPAY PO BX 40409 DENVER CO 80204 CWX A L FNCL CORP PO BX 11907 SANTA ANA CA 92711 J68 A L FNCL CORP PO BX 51466 ONTARIO CA 91761 J90 A L FNCL CORP PO BX 255128 SACRAMENTO CA 95865 J93 A L FNCL CORP PO BX 28248 FRESNO CA 93729 J95 A PLUS FCU PO BX 14867 AUSTIN TX 78761 AYV A PLUS LOANS 500 3RD ST W SACRAMENTO CA 95605 GCC A/M FNCL PO BX 1474 CLOVIS CA 93613 A94 AAA FCU PO BX 3788 SOUTH BEND IN 46619 CSM AAC CU 177 WILSON AVE NW GRAND RAPIDS MI 49534 GET AAFCU PO BX 619001 MD2100 DFW AIRPORT TX 75261 A90 ABLE INC 503 COLORADO ST AUSTIN TX 78701 CVD ABNB FCU 830 GREENBRIER CIR CHESAPEAKE VA 23320 CXE ABOUND FCU PO BX 900 RADCLIFF KY 40159 GKB ACADEMY BANK NA PO BX 26458 KANSAS CITY MO 64196 ATF ACCENTRA CU 400 4TH -

Office Space Wav Files Download Office Space Wav Files Download

office space wav files download Office space wav files download. To download as a ringtone put the URL below into your cell phone's browser: (Not all cell phones support this feature.) To use as ringtone on your iPhone open the m4r audio file with iTunes and it will automatically be put in the "Ringtones" folder. Then sync your phone. You may need to check the "Sync ringtones" box under the "Ringtones" tab in iTunes for your iPhone. (Unfortunately if the sound clip is over 40 seconds it will not work because iTunes puts a limit on it.) What Are WAV and WAVE Files (and How Do I Open Them)? Brady Gavin has been immersed in technology for 15 years and has written over 150 detailed tutorials and explainers. He's covered everything from Windows 10 registry hacks to Chrome browser tips. Brady has a diploma in Computer Science from Camosun College in Victoria, BC. Read more. A file with the .wav or .wave file extension is a Waveform Audio File Format. It’s a container audio file that stores data in segments. It was created by Microsoft and IBM and has become the standard PC audio file format. Note: WAVE and WAV files (or the .wav and .wave extension) are the same thing. Throughout this article, we’ll be referring to them as WAV files to save a few words. What Is a WAV File? A WAV file is a raw audio format created by Microsoft and IBM. The format uses containers to store audio data, track numbers, sample rate, and bit rate. -

APPENDIX B Cultural Resources Assessment

APPENDIX B Cultural Resources Assessment 3700 Riverside Drive Mixed-Use Project Cultural Resources Assessment prepared for City of Burbank 150 North Third Street Burbank, California 91502 Contact: Daniel Villa, Senior Planner prepared by Rincon Consultants, Inc. 250 East 1st Street, Suite 301 Los Angeles, California 90012 August 2020 Please cite this report as follows: Madsen, A., M. Strother, B. Campbell-King, S. Treffers, and S. Carmack 2020 Cultural Resources Assessment for the 3700 Riverside Drive Mixed Use Project, City of Burbank, Los Angeles County, California. Rincon Consultants Project No. 19-08998. Report on file at the South Central Coastal Information Center, California State University, Fullerton. Table of Contents Table of Contents Executive Summary ................................................................................................................................ 1 Unanticipated Discovery of Cultural Resources ............................................................................. 1 Unanticipated Discovery of Human Remains ................................................................................ 2 1 Introduction ................................................................................................................................... 3 Project Location and Description ........................................................................................ 3 Personnel ........................................................................................................................... -

Representations of Masculinity in Contemporary Hollywood Comedies a Thesis Presented to the Facult

In the Company of Modern Men: Representations of Masculinity in Contemporary Hollywood Comedies A thesis presented to the faculty of the College of Fine Arts of Ohio University In partial fulfillment of the requirements for the degree Master of Arts Nicholas D. Bambach August 2016 © 2016 Nicholas D. Bambach. All Rights Reserved. 2 This thesis titled In the Company of Modern Men: Representations of Masculinity in Contemporary Hollywood Comedies by NICHOLAS D. BAMBACH has been approved for the School of Film and the College of Fine Arts by Ofer Eliaz Assistant Professor of Film Elizabeth Sayrs Interim Dean, College of Fine Arts 3 ABSTRACT BAMBACH, NICHOLAS D., M.A., August 2016, Film In the Company of Modern Men: Representations of Masculinity in Contemporary Hollywood Comedies Director of Thesis: Ofer Eliaz This thesis discusses the increasing visibility of masculine identity in contemporary Hollywood comedies. I examine how shifting developments in economic, societal, cultural, and gender relations impacted the perception of cinematic masculinity. The men, more specifically white and heterosexual, in these films position themselves as victims and, as a result, turn to alternative outlets to ease their frustrations and anxieties. In order to broadly survey the genre of the past two decades, I focus on three consistently popular character tropes in Hollywood comedies: slackers, office workers, and bromantic friendships. All the male characters discussed throughout the thesis are plagued by their innermost anxieties and desires that compromise their gendered identities. However, these films resort to a regressive understanding of masculinity and functions within the dominant heteronormative structures. This thesis demonstrates how Hollywood comedies present a contradictory and multifaceted image of modern masculinity. -

Contractor List

Active Licenses DBA Name Full Primary Address Work Phone # Licensee Category SIC Description buslicBL‐3205002/ 28/2020 1 ON 1 TECHNOLOGY 417 S ASSOCIATED RD #185 cntr Electrical Work BREA CA 92821 buslicBL‐1684702/ 28/2020 1ST CHOICE ROOFING 1645 SEPULVEDA BLVD (310) 251‐8662 subc Roofing, Siding, and Sheet Met UNIT 11 TORRANCE CA 90501 buslicBL‐3214602/ 28/2021 1ST CLASS MECHANICAL INC 5505 STEVENS WAY (619) 560‐1773 subc Plumbing, Heating, and Air‐Con #741996 SAN DIEGO CA 92114 buslicBL‐1617902/ 28/2021 2‐H CONSTRUCTION, INC 2651 WALNUT AVE (562) 424‐5567 cntr General Contractors‐Residentia SIGNAL HILL CA 90755‐1830 buslicBL‐3086102/ 28/2021 200 PSI FIRE PROTECTION CO 15901 S MAIN ST (213) 763‐0612 subc Special Trade Contractors, NEC GARDENA CA 90248‐2550 buslicBL‐0778402/ 28/2021 20TH CENTURY AIR, INC. 6695 E CANYON HILLS RD (714) 514‐9426 subc Plumbing, Heating, and Air‐Con ANAHEIM CA 92807 buslicBL‐2778302/ 28/2020 3 A ROOFING 762 HUDSON AVE (714) 785‐7378 subc Roofing, Siding, and Sheet Met COSTA MESA CA 92626 buslicBL‐2864402/ 28/2018 3 N 1 ELECTRIC INC 2051 S BAKER AVE (909) 287‐9468 cntr Electrical Work ONTARIO CA 91761 buslicBL‐3137402/ 28/2021 365 CONSTRUCTION 84 MERIDIAN ST (626) 599‐2002 cntr General Contractors‐Residentia IRWINDALE CA 91010 buslicBL‐3096502/ 28/2019 3M POOLS 1094 DOUGLASS DR (909) 630‐4300 cntr Special Trade Contractors, NEC POMONA CA 91768 buslicBL‐3104202/ 28/2019 5M CONTRACTING INC 2691 DOW AVE (714) 730‐6760 cntr General Contractors‐Residentia UNIT C‐2 TUSTIN CA 92780 buslicBL‐2201302/ 28/2020 7 STAR TECH 2047 LOMITA BLVD (310) 528‐8191 cntr General Contractors‐Residentia LOMITA CA 90717 buslicBL‐3156502/ 28/2019 777 PAINTING & CONSTRUCTION 1027 4TH AVE subc Painting and Paper Hanging LOS ANGELES CA 90019 buslicBL‐1920202/ 28/2020 A & A DOOR 10519 MEADOW RD (213) 703‐8240 cntr General Contractors‐Residentia NORWALK CA 90650‐8010 buslicBL‐2285002/ 28/2021 A & A HENINS, INC. -

Glib, Funny Office Space: Take This Job and Love It

PAGE22 THE RETRIEVER WEEKLY FEATURES March 2, 1999 Glib, Funny Office Space: Take This Job and Love It 20th Century Fox JAMIE PECK Cubicle Couple: Jennifer Retriever Weekly Staff Writer Aniston and Ron Livingston star in Mike Judge's Office Space, "Beavis and Butt-Head" and "King of the she as a waitress fed up with Hill" creator Mike Judge -goes live-action in chain regulations and he as a 1 Office Space (*** 12 out of four), and the white-collar software designer end result is more animated than either of his who gets a sudden case of the respectively overhyped and overrated TV don't-cares. projects. It could be that Judge's shrewd sense of social satire feels more at home has a lot of fun as Peter's evil over played out by actual people instead of seer, peppering his lines with hilari crudely-rendered doodles, or perhaps it's just ously absent-minded yeeeeahs and that Office's hook is a can't-miss ribbing of mm-hms, while Jennifer Aniston of the daily occupational grind - something "Friends" is adorable as the object of that almost everybody everywhere can relate Peter's affection, an oft-scolded wait to. Whatever the ultimate reason, this lively ress at a T.G.I. Friday's-like eatery. gutbuster appears to indicate a promising for Their romance is largely superfluous, mat change for the occasionally lauded (and but Office Space does use theAniston occasionally controversial) auteur. It's ironic role to observe the parallel travails of to note, then, that the film is based on the those in the service industry.