Focused, Solid and Ready for Growth Annual Report 2002

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

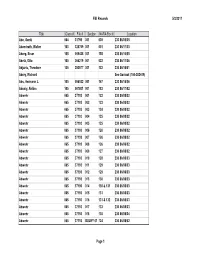

5/3/2011 FBI Records Page 1 Title Class # File # Section NARA Box

FBI Records 5/3/2011 Title Class # File # Section NARA Box # Location Abe, Genki 064 31798 001 039 230 86/05/05 Abendroth, Walter 100 325769 001 001 230 86/11/03 Aberg, Einar 105 009428 001 155 230 86/16/05 Abetz, Otto 100 004219 001 022 230 86/11/06 Abjanic, Theodore 105 253577 001 132 230 86/16/01 Abrey, Richard See Sovloot (100-382419) Abs, Hermann J. 105 056532 001 167 230 86/16/06 Abualy, Aldina 105 007801 001 183 230 86/17/02 Abwehr 065 37193 001 122 230 86/08/02 Abwehr 065 37193 002 123 230 86/08/02 Abwehr 065 37193 003 124 230 86/08/02 Abwehr 065 37193 004 125 230 86/08/02 Abwehr 065 37193 005 125 230 86/08/02 Abwehr 065 37193 006 126 230 86/08/02 Abwehr 065 37193 007 126 230 86/08/02 Abwehr 065 37193 008 126 230 86/08/02 Abwehr 065 37193 009 127 230 86/08/02 Abwehr 065 37193 010 128 230 86/08/03 Abwehr 065 37193 011 129 230 86/08/03 Abwehr 065 37193 012 129 230 86/08/03 Abwehr 065 37193 013 130 230 86/08/03 Abwehr 065 37193 014 130 & 131 230 86/08/03 Abwehr 065 37193 015 131 230 86/08/03 Abwehr 065 37193 016 131 & 132 230 86/08/03 Abwehr 065 37193 017 133 230 86/08/03 Abwehr 065 37193 018 135 230 86/08/04 Abwehr 065 37193 BULKY 01 124 230 86/08/02 Page 1 FBI Records 5/3/2011 Title Class # File # Section NARA Box # Location Abwehr 065 37193 BULKY 20 127 230 86/08/02 Abwehr 065 37193 BULKY 33 132 230 86/08/03 Abwehr 065 37193 BULKY 33 132 230 86/08/03 Abwehr 065 37193 BULKY 33 133 230 86/08/03 Abwehr 065 37193 BULKY 35 134 230 86/08/03 Abwehr 065 37193 EBF 014X 123 230 86/08/02 Abwehr 065 37193 EBF 014X 123 230 86/08/02 Abwehr -

Gravrättsinnehavare Sökes Mölltorp.Pdf

Kungörelse Vid inventering av gravplatser på Mölltorps kyrkogård har följande gravplatser befunnits sakna registrerade gravrättsinnehavare. Gravplats Senast gravsatta Plats Dödsår Uppdaterad 2021-03 G B 3-A-B Gustava Bjerstedt Johansson 1918 G B 5-A-B Karl August Kärrman 1926 G B 9-A-B Manny Hulda Maria Thübeck 1980 G B 10 Johanna Ulrika Rosalia Emilia Ewerts 1929 G B 11-A-B Astrid Matilda Ahlqvist 1974 G B12-A-B Lotta Kajsa Carlsson 1923 G B 13-A-B Malin Teresia Göransson 1916 G C 8-A_B Karolina Rantzén Krogstorp 1925 G C 10-A-B Margit Kristina Berglund Karlsborg 1982 G C 18-A-F Johanna Fredrika Andersdotter Sjövik 1939 G D 3 A-B Svea Hjelmberg 1974 G D 5 A-C-D Anders Fredrik Eriksson ”Ebbetorp” 1927 G D 12 Karolina Torstenson Skäverud 1926 G D 22 A-B Selma Andersson 1923 G E 1 A-B Rut Ingeborg Landelius 1991 G E 4 A-B Anna Karolina Holm 1944 G E 7 A-B Anna Lovisa Holmqvist 1951 G E 16 A-B Carl August Eriksson 1938 G E 18 A-B Karl Johan Jansson 1940 G F 4 A-B Tore Ragnar Lundgren 1990 G G 60 Axel Verner Johansson Älebäcken 1973 G G 106 Maria Sofia Harnesk 1929 G G 109 Karl Karlsson 1928 G G 110-111 Karl Arvid Pettersson 1979 G G 171,172 Frans Oskar Johansson Gräshult 1935 G G 215 Anders Viktor Andersson Gräshult 1931 G G 252,253 Ada Charlotta Persson Furugården 1969 G G 254,255 Jenny Paulina Persson Måsebo 1958 G G 276 Amanda Karolina Lake Furugården 1950 G G 277,278 Karl David Viselius Malm Ingesborg 1984 G G 279 Hulda Gustava Andersson 1963 G G 286 Frans Vilhelm Eriksson 1948 G G 289 Anders Martin Ljung 1967 G G 293 Gerda Hedvig Altea -

Class of 2020

Virtual Celebration and Degree Conferral for the CLASS OF 2020 Saturday, May 16, 2020 Contents Board of Visitors, 2 Administration, 3 Graduates and Degree Candidates* Graduate School of Arts & Sciences, 4 College of Arts & Sciences, 8 School of Medicine, 18 School of Law, 19 School of Engineering & Applied Science, 21 Curry School of Education and Human Development, 26 Darden Graduate School of Business Administration, 30 School of Architecture, 31 School of Nursing, 32 McIntire School of Commerce, 34 School of Continuing & Professional Studies, 36 Frank Batten School of Leadership and Public Policy, 37 School of Data Science, 37 Student and Faculty Awards, 38 Honorary Societies, 39 The Good Old Song, 42 * The degree candidates in this program were applicants for degrees as of May 1, 2020. The August 2019 and December 2019 degree recipients precede the list of May 2020 degree candidates in each section. © 2020 by the Rector and Visitors of the University of Virginia Designed by University of Virginia Printing and Copying Services University of Virginia Board of Visitors James B. Murray, Jr., Rector (Keene, VA) Whittington W. Clement, Vice Rector (Richmond, VA) Robert M. Blue (Richmond, VA) Mark T. Bowles (Goochland, VA) L.D. Britt, M.D., MPH (Suffolk, VA) Frank M. Conner III (Alexandria, VA) Elizabeth M. Cranwell (Vinton, VA) Thomas A. DePasquale (Washington, DC) Barbara J. Fried (Crozet, VA) John A. Griffin (New York, NY) Louis S. Haddad (Suffolk, VA) Robert D. Hardie (Charlottesville, VA) Maurice A. Jones (Norfolk, VA) Babur B. Lateef, M.D. (Manassas, VA) Angela Hucles Mangano (Playa del Rey, CA) C. -

Of Names 91, 92, 95–97 Davies, Brian 13, 49 Adorno, Theodor Wiesengrund 34, 43, 44, 90, Davis, Scott G

Davidson, Donald 9, 10, 15, 33, 59, 63, 66–84, Index of Names 91, 92, 95–97 Davies, Brian 13, 49 Adorno, Theodor Wiesengrund 34, 43, 44, 90, Davis, Scott G. 69, 74 116, 121, 123, 140, 161, 162, 213 Dawkins, Richard 16 Agamben, Giorgio 202, 207, 212 Deleuze, Giles 11, 138, 143, 208 Albinus, Lars 16, 45, 56, 59, 63, 67, 105, 137, Dennett, Daniel 16 153, 177, 179, 196, 198, 199, 202 Derrida, Jacques 15, 16, 21, 22, 152, 207–209, Alston, William 13, 28, 29, 41 212, 215 Ananda Sri G. 102 Detienne, Marcel 91–93, 99, 141 Apel, Karl Otto 15, 50, 51, 58, 169 Doležel, Lubomir 55, 155 Arendt, Hannah 104, 116, 120 Donald, Merlin 57 Aristotle 43, 66, 90–92, 94, 99, 115, 138, 158 Doniger, Wendy 198 Asad, Talal 36 Drury, M. O‘C. 127 Augustine 43, 84, 186 Duns Scotus 215 Bachelard, Gaston 8, 35 Eiland, H. 113, 114, 121, 122, 125, 128, 130 Badiou, Alain 17, 37, 41, 202 Eliade, Mircea 18, 19 Bakhtin, Mikhael M. 98, 202 Engler, Steven 6, 9, 13, 40, 63, 69, 70, 71 Barbour, Ian G. 13, 47 Feyerabend, Ludwig 15 Barnes, Barry 15 Fitzgerald, Timothy 18, 20, 36, 40, 190 Barth, Karl 142 Flood, Gavin 6, 16, 17, 20, 223 Baudelaire, Charles 118, 211 Foucault, Michel 2, 4, 8, 15, 24, 35, 38–40, 48, Bellah, Robert 40, 219 50, 51, 66, 96, 100, 128, 129, 141, 152, 195, Benjamin, Walter 2, 4, 10, 11, 33, 41, 79, 86, 202, 208, 214 89–91, 96–98, 101, 102, 105–107, 111–140, Frankenberry, Nancy 18, 66, 69–71 143–146, 148, 151, 160, 161, 167, 192, 202, Frazer, James George 83–87, 89, 108, 110, 119, 205–207, 210–213, 216–219, 222, 223 130, 132, 133, 135, 183–185, 190, 202, 213 Berger, Peter 7, 15, 80, 91 Freud, Sigmund 13, 182, 206 Bloor, David 15 Frege, Gottlob 32, 62, 144, 145 Bonhoeffer, Dietrich 142 Gabrielli, Paolo 105, 120, 123, 131, 132, 211 Borges, Luis 211, 218, 223 Gadamer, Hans Georg 37, 38, 72, 73, 156, 157 Boyer, Pascal 60, 197 Gardiner, Mark Q. -

3358 the LONDON GAZETTE, 18 JULY, 1947 Meitner, Franz Philipp

3358 THE LONDON GAZETTE, 18 JULY, 1947 Meitner, Franz Philipp. Child of Meitner,, Walter. Meyerhoff, Fritz (known as Fred Meyerhofl); Gei- Meitner, Walter; Austria; Chemist; 198, Wilmslow many; Manufacturer; 24, Colinton Mains Terrace, Road, Manchester 20. 10 June, 1947- Edinburgh 13, Midlothian, Scotland. 13 June, Melcher, Kitty Katherina; Austria; Hosiery Fore- 5947- s.- woman; 16, Portsdown Road, Leicester, Leicester- Meyerhofl, Heinz Julius (known as Henry). Child shire. 6 June, 1947. of Meyerhofl, Fritz (known as Fred Meyerhoff). Mellinger, Lucas Emmanuel Matthias; Germany; Meyerhoff, Henry. See Meyerhofl, Heinz Julius. Student; 37, Emperors Gate, London, S.W-7. 31 Meyerhoff, Peter Adolf Wilhelm; Germany; May, 1947. Economist; 17, Windmill Road, Brentford, Mellinger, Michael Andreas; Germany; Student; 66, Middlesex. 24 June, 1947. Scarsdale Villas, London, W.8. n June, 1947. Meyersohn, Herbert; Germany; Dental Surgeon; *Melzak, Ada; Poland; Supervisor; 44, Wheatlands 8, Harbord Street, London, S.W.6. 19 May, Drive, Bradford, Yorkshire. 29 May, 1947. 1947. Melzer, Leo; Austria; Technical Assistant; 132, Meyerstein, Wilhelm; Germany; Lecturer of Anson Road, London, N.W.2. 20 June, 1947- Physiology; 123, Willow Avenue, Birmingham, Mendel, Rahel Luise; Germany; Student Nurse; Warwickshire. 14 June, 1947. Withington Hospital, Nell Lane, West Didsbury, *Meyns, Christena Winifred Claudia; Germany; Manchester. 2 June, 1947. Housewife; " Ivybank," Fawkham, Kent. n Mendels, Louis Philip; Netherlands; Managing June, 1947. Director; Sea View, 26, Daglands Road, Fowey, Michaelis, Martha; Germany; Social Worker; 51, Cornwall. 20 May, 1947. Fitzjphns Avenue, London, N.W.3- 26 June, Mendelsohn, Heinrich. Child of Mendelsohn, 1947. Johannes. Michel, Stefame Caroline; Germany; Secretary; Mendelsohn, Johannes; Germany; Distiller; 8, Holm- 9, Edmunds Walk, London, N.2. -

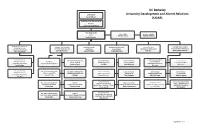

UC Berkeley University Development and Alumni Relations (UDAR)

UC Berkeley Chancellor University Development and Alumni Relations Carol Christ (UDAR) Executive Vice Chancellor & Provost Catherine Koshland Vice Chancellor Chief of Staff Executive Assistant UDAR Kim Kincannon Matthew Weinberg Julie Hooper Assistant Vice Chancellor Associate Vice Chancellor Campaign Director Associate Vice Chancellor Executive Director Associate Vice Chancellor PRINCIPAL GIFTS & CONSTITUENT PROGRAMS FOUNDATION OPERATIONS ADVANCEMENT OPERATIONS STRATEGIC INITIATIVES CAMPAIGN DEVELOPMENT Michelle McClellan Leslie Schibsted Lishelle Blakemore MiHi Ahn Nancy Lubich McKinney Christine Schmidt Executive Director Chief Technology Officer Asst. Dean of Development Executive Director Executive Director Senior Director PRINCIPAL GIFTS & 26 CAMPUS ADVANCEMENT SOCIAL SCIENCES ALUMNI RELATIONS GIFT PLANNING FUND MANAGEMENT STRATEGIC INITIATIVES Chief Development Officers INFORMATION SERVICES Christian Gordon Jay Dillon Randi Silverman Ali De Gros Jenny Cutting Karl Otto Executive Director Asst. Dean of Development Asst. Dean of Development Executive Director Executive Director Senior Director Senior Director PRINCIPAL GIFTS & ARTS & HUMANITIES UNDERGRADUATE STUDIES ANNUAL PROGRAMS MAJOR GIFTS DONOR RECOGNITION GIFT SERVICES STRATEGIC INITIATIVES Lynnette Teti VACANT Howard Heevner Tami Cardenas Katy Galli-Kreps Matthew Weaver Leti Light Executive Director Human Resources Director Asst. Dean of Development Director Executive Director Executive Director EXTERNAL RELATIONS & TALENT MANAGEMENT & BIOLOGICAL SCIENCES PROSPECT DEVELOPMENT STUDENT EXPERIENCE & DIVERSITY FINANCE & ADMINISTRATION MARKETING COMMUNICATIONS WORKFORCE PLANNING Kirsten Swan Terence Kissack Brooke Hendrickson Loraine Binion Colleen Rovetti Ron Coverson Asst. Dean of Development Director Executive Director MATH & PHYSICAL SCIENCES COMMUNICATIONS & OUTREACH FOUNDATION RELATIONS & Maria Hjelm Carolyn Iyoya Irving CORPORATE PHILANTHROPY Sylvia Bierhuis Updated 7/1/21. -

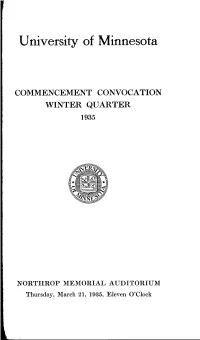

1935-Commencement.Pdf

University of Minnesota COMMENCEMENT CONVOCATION WINTER QUARTER 1935 NORTHROP MEMORIAL AUDITORIUM Thursday, March 21, 1935, Eleven O'Clock PROGRAM President LOTUS D. COFFMAN, Presiding PROCESSIONAL-HMarche de Fete" - Claussmann GEORGE H. FAIRCLOUGH HYMN-HAmerica" My country! 'tis of thee Our fathers' God! to Thee, Sweet land of liberty, Author of Liberty, Of thee I sing; To Thee we sing; Land where my fathers died, Long may our land be bright Land of the Pilgrims' pride, With freedom's holy light; From every mountain side Protect us by Thy might, Let freedom ring! Great God, our King! COMMENCEMENT ADDRESS-"Telescopes, Microscopes, and Politics" THOMAS V. SMITH, Ph.D. Professor of Philosophy, University of Chicago ORGAN SOLO-"Toccata and Fugue in D Minor" Bach (Born March 21, 1685) MR. FAIRCLOUGH CONFERRING OF DEGREES LOTUS D. COFFMAN, Ph.D., LL.D. President of the University 2 SONG-"Hail, Minnesota!" Minnesota, hail to thee! Like the stream that bends to sea Hail to thee, our College dear! Like the pine that seeks the blue I Thy light shall ever be Minnesota, still for thee, A beacon bright and clear; Thy sons are strong and true. Thy sons and daughters true From thy woods and waters fair, Will proclaim thee near and far; From thy prairies waving far, They will guard thy fame At thy call they throng, And adore thy name; With their shout and song, Thou shalt be their Northern Star. Hailing thee their Northern Star. RECESSIONAL-"Finale (Symphony V)" Widor MR. FAIRCLOUGH SMOKING As a courtesy to those attending functions, and out of respect for the character of the building, be it resQlved by the Board of Regents that there be printed in the programs of .11 functions held in the Cyrus Northrup Memorial Auditorium a request that smoking be confined to the outer lobby on the main floor, to the gallery lobbies, and to the lounge rooms. -

ECSC 2018 Program

The 72nd Annual Eastern Colleges Science Conference Ithaca College 21 April 2018 Program Book MEETING WELCOME Welcome to ECSC 2018 and Ithaca College! It’s my great pleasure to welcome you all to Ithaca College for the 72nd Eastern Colleges Science Conference. We are excited to be welcoming students and faculty from nearly 20 colleges and universities, representing dozens of fields in the social and natural sciences. I have been attending ECSC with my own research students since 1989, and I have always found it be an incredibly rewarding experience for both me and for my undergraduate students in psychology. Students are delighted to have the opportunity to share their research with faculty and other students, explaining their findings and answering questions about their methods and the implications of their research for the field. My students have come back from ECSC weekend really jazzed about doing research, and proud of representing their work and Ithaca College. I hope that all of you have the same experience this weekend. I encourage you to attend as many platform presentations and view as many posters as you can – including ones from areas outside your own field. Ask questions, engage in discussions about the implications of the findings, and make connections with students from other colleges and universities. In this era of “fake news” and distrust of facts and news media, scientific thinking is more important than ever before. It is such a privilege and a pleasure to gather together with a large group of scientists (of many ages) to celebrate the work that we do. -

The German Connection for My Daughter ‘Johanna’

~ 1 ~ THE GERMAN CONNECTION FOR MY DAUGHTER ‘JOHANNA’ OTTO AND DISCHER FAMILIES PATERNAL THREAD FOR JOHANNA (This journal is the complete paper trail) THE GOOD SHIP HELENSLEE SAILED FROM LONDON 2 OCTOBER 1869: ARRIVED IN AUCKLAND 18 JANUARY 1870 On board was Johanna’s great, great, great grandfather Friedrich Karl OTTO His daily experiences, written and recorded in a diary aboard the Helenslee during his journey are most interesting. The translated copy of his diary from German to English is held at the Turnbull Library in Wellington ABOVE: FOUR GENERATIONS THE BABY IS MY AUNT MOLLY PULLEN NEE MOLD WITH MY GRANDMOTHER HENRIETTA MOLD NEE WEBB DIRECTLY BEHIND ON THE LEFT IS MY GREAT GRANDMA FREDERICA WEBB NEE OTTO AND TO THE RIGHT IS GREAT, GREAT, GRANDFATHER FREDERIC CHARLES OTTO ~ 2 ~ CHAPTERS CHAPTER ONE FROM THE SEA THEY CAME FROM GERMANY TO ENGLAND TO NEW ZEALAND PAGE 3 CHAPTER TWO GENERATION ONE FOR DISCHER PAGE 28 CHAPTER THREE GENERATION TWO FOR DISCHER PAGE 29 CHAPTER FOUR GENERATION THREE FOR DISCHER PAGE 31 CHAPTER FIVE GENERATION FOUR FOR DISCHER PAGE 33 CHAPTER SIX GENERATION ONE FOR OTTO PAGE 41 CHAPTER SEVEN GENERATION TWO FOR OTTO PAGE 42 CHAPTER EIGHT GENERATION THREE FOR OTTO PAGE 44 CHAPTER NINE GENERATION FOUR FOR OTTO PAGE 49 CHAPTER TEN OTTO FAMILY PHOTOS AND REFERENCES PAGE 51 CHAPTER ELEVEN THE TRANSLATED DIARY OF MR. FREDERIC CHARLES OTTO PAGE 59 CHAPTER TWELVE RECENT PHOTOS AND REFERENCES PAGE 115 ~ 3 ~ 1 FROM THE SEA THEY CAME GERMANY TO ENGLAND TO NEW ZEALAND THE OTTO’S VOYAGES TO NEW ZEALAND MR F. -

A $1.25 Million Chair in Corporate

Tuesday, May /3. /986 Published by the University of Pennsylvania Volume 32. Number 34 in Law Bilke prize for the highest grades in constitu- A $1.25 Million Chair Corporate tional law. He entered the business world after The William B. Johnson Professorship of The Board of Directors of IC Industries several years as an attorney in military and Corporate Law has been established at the Law voted unanimously last week to establish the government service, and joined IC Industries as School through a $1.25 million gift from IC chairin honor ofMr. Johnson's 20th year at the CEO in 1966. Industries in honor oftheirchairman and chief helm of the Chicago-based company, accord- "Bill Johnson has been an excellent student, executive officer, William B. Johnson, ofLaw's ing to a company spokesman. Under Mr. an exemplary lawyer, and an outstanding busi- Class of 1943. Johnson's leadership, IC Industries has grown ness leader. It greatly enhances the Law School The holder ofthe William B. Johnson chair from a $300 million railroad to a $4.5 billion to have a chair in corporatelaw dedicated in his will "teach and, through scholarly research and diversified conglomerate encompassing six honor," said Federal Court of Appeals Judge writing, contribute to the fundamental rethink- major subsidiaries with concentrations in spe- Arlin Adams, a Penn Trustee who is chairman ing of corporate law now taking place in the cialty foods, consumer services, and aerospace of the School's Board of Overseers. courts, legislatures and regulatory agencies," and defense products. Mr. Johnson is also an Overseer, and serves according to Dean Robert H. -

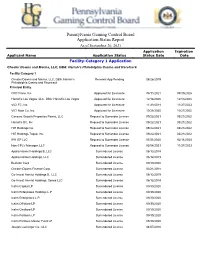

Pennsylvania Gaming Control Board Application Status Report

Pennsylvania Gaming Control Board Application Status Report As of September 26, 2021 Application Expiration Applicant Name Application Status Status Date Date Facility-Category 1 Application Chester Downs and Marina, LLC, DBA: Harrah’s Philadelphia Casino and Racetrack Facility-Category 1 Chester Downs and Marina, LLC, DBA: Harrah’s Renewal App Pending 08/26/2019 Philadelphia Casino and Racetrack Principal Entity CRC Finco, Inc Approved for Licensure 08/11/2021 08/10/2026 Harrah's Las Vegas, LLC, DBA: Harrah's Las Vegas Approved for Licensure 12/16/2020 12/15/2025 VICI FC, Inc. Approved for Licensure 11/28/2018 11/27/2023 VICI Note Co. Inc. Approved for Licensure 10/28/2020 10/27/2025 Caesars Growth Properties Parent, LLC Request to Surrender License 09/22/2021 03/21/2022 Harrah's BC, Inc Request to Surrender License 09/22/2021 03/21/2022 HIE Holdings Inc. Request to Surrender License 09/22/2021 03/21/2022 HIE Holdings Topco, Inc. Request to Surrender License 09/22/2021 03/21/2022 IPH GP LLC Request to Surrender License 07/31/2020 02/11/2025 Non-CPLV Manager, LLC Request to Surrender License 05/04/2021 11/27/2023 Apollo Hamlet Holdings B, LLC Surrendered License 06/12/2019 Apollo Hamlet Holdings, LLC Surrendered License 06/12/2019 Beckton Corp Surrendered License 09/30/2020 Chester Downs Finance Corp. Surrendered License 03/21/2018 Co-Invest Hamlet Holdings B, LLC Surrendered License 06/12/2019 Co-Invest Hamlet Holdings, Series LLC Surrendered License 06/12/2019 Icahn Capital LP Surrendered License 09/30/2020 Icahn Enterprises Holdings L.P. -

Loyola University New Orleans College of Law

LOYOLA UNIVERSITY NEW ORLEANS COLLEGE OF LAW FINANCIAL INSTITUTIONS LAW (LAW L829) FALL 2019 SEMESTER SYLLABUS (Revised---06/17/2019) Instructor’s Name: Professor R. J. Rabalais Eleanor Legier Sarpy Distinguished Professor of Law Office Location: Room 436 7214 St. Charles Avenue (Broadway Campus) New Orleans, LA 70118-3538 Office Hours: Tuesdays--- 5:00 p.m. to 6:00 p.m. Thursdays---5:00 p.m. to 6:00 p.m. (or after class, or by appointment) Office Telephone: (504) 861-5671 Office Email Address: [email protected] Current Term: Fall 2019 Semester Class Meeting Times: Tuesdays ---3:30 p.m. to 4:45 p.m. Thursdays---3:30 p.m. to 4:45 p.m. Course Goals and Objectives: (1) The course will provide students with an introduction to investment management regulation in the United States, where there are currently over $25 trillion in assets under management, involving over 95 million retail investors. (2) The course is designed to provide a solid foundation for students interested in taking the North American Securities Administrators Association (NASAA) Series 65---Uniform Investment Adviser Law Examination, which is administered by the Financial Industry Regulatory Authority (FINRA). 1 Expected Student Learning Outcomes: (1) Knowledge of substantive law and processes, including: knowledge of substantive and procedural rules of law the processes through which law is created, applied and changed the policies underlying laws, and the methods used to resolve disputes. (2) Analysis and reasoning, including: the ability to identify legal issues the ability to apply the rules of law and policy to facts the ability to construct arguments and analyze counter-arguments the ability to adapt arguments as facts change and are discovered the ability to exercise practical judgment, and the ability to use facts, law, and policy to persuade.