Press Release Cadila Pharmaceuticals Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gujara T Terce Laboratories Limited

GUJARAT TERCE LABORATORIES LIMITED Date: 17.04.201 9 To, Corporate Relations Department, Bombay Stock Exchange Limited, 2"* Floor, P.J Towers, Dalal Street, Mumbai-400 001 Scrip Code: 524314 Dear Sir, Subject: Certificate under Regulation 74(5) of SEBl (Depositories and Participants) Regulations, 2018 for the quarter ended 3IstMarch, 2019 This is to certify that the details of securities dematerialized/rematerialized during the quarter ended 3Ist March, 2019, as required under Regulation 74(5) of SEBl (Depositories and Participants) Regulations, 2018, have been furnished to all the stock exchanges where the shares of the Company are listed. The letter confirming this from our RTA - MIS. Bigshare Services Private Limited dated 05" April, 2019 is enclosed for your reference. We request you to kindly take this on your record and oblige. Thanking you, Yours faithfullv. Yours faithfuiiy, Gujarat Terce Laboratories Limited company Secretary & Corn Encl.: as above CC: 1. National Securities Depository Ltd 4th & 5th Floor, A Wing, Tradeworld, Senapati Bapat Marg, Near Kamla Mills Compound, Lower Parel, Mumbai - 40001 3 CC: 2. Central Depository Services (India) Limited Marathon Futurex, A-Wing, 25th Floor, NM Joshi Marg, Lower Pare), Mumbai - 400013 Regd. Oflice & Factory : 12212 Ravi Estate, Bileshwarpura, Admn. Office : Dl801 & 802, The First, Behind Keshavbaug Party Plot, Chhatral, Ta. : Kalol, Dist. : Gandhinagar (Guj.) INDIA. Near Shivalik High-street, Vastrapur, Ahmedabad-380015 Gujarat.(lNDIA) Ph.: 079-48933701 Ph.: 02764-233182 E.mail : [email protected] E.mail : [email protected] Web. : www.gujaratterce.com CIN : L23112GJ1985PLC007753 I GTLL_SAC_CDSL.txt BIGSHARE SERVICES PVT. LTD. ANNEXURE 1 UNIT : GUJARAT TERCE LABORATORIES LTD List of Demat request received in previous quarter & confirmed in this quarter 01/01/2019 to 31/03/2019 CDSL ----------------------------------------------------------------------------------------------------------------- ----------------------------- SrNo DRN Req. -

Of 11 BEFORE the ADJUDICATING OFFICER SECURITIES AND

BEFORE THE ADJUDICATING OFFICER SECURITIES AND EXCHANGE BOARD OF INDIA [ADJUDICATION ORDER NO. IVD-ID9/RDB/AO/DRK-AKS/EAD3-494 -496 /38 - 40 /2014] __________________________________________________ UNDER SECTION 15 I OF SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992 READ WITH RULE 5(1) OF SECURITIES AND EXCHANGE BOARD OF INDIA (PROCEDURE FOR HOLDING INQUIRY AND IMPOSING PENALTIES BY ADJUDICATING OFFICER) RULES, 1995 In respect of: BMD Exports Pvt. Ltd. Shri Jitendrabhai Ramanbhai Patel Shri Madhavlal Bechardas Patel 22-A,Suraksha Society Visnagar, Mehsana Gujarat - 384315 FACTS IN BRIEF 1. Securities and Exchange Board of India (hereinafter referred to as ‘ SEBI ’) conducted an investigation of the Initial Public Offer (hereinafter referred to as ‘IPO ’) of RDB Rasayans Ltd. (herein after referred to as ‘RDB ’) and its subsequent trading on and around the listing day as the scrip of RDB witnessed wide fluctuations in the price on Bombay Stock Exchange Ltd. (hereinafter referred to as ‘ BSE ’). RDB came out with an IPO of 45,00,000 equity shares of ` 10 per share at an issue price of ` 79 each and the issue was opened on 21.09.2011 and closed on 23.09.2011. The post issue equity share capital of the company is 1,77,14,800 shares. APPOINTMENT OF ADJUDICATING OFFICER 2. I was appointed as the Adjudicating Officer under Section 15 I of the Securities and Exchange Board of India Act, 1992 (hereinafter referred to as ‘SEBI Act ’), read with Rule 3 of Securities and Exchange Board of India (Procedure for Holding Inquiry and Imposing Penalties by Adjudicating Officer) Rules, 1995 (hereinafter referred to as ‘ Adjudication Rules’ ) to Page 1 of 11 inquire into and adjudge under Sections 15 HA and 15 HB of the SEBI Act the violations of Sections 12A (a), (b) and (c) of the SEBI Act read with Regulations 3 (a), (b), (c), (d), 4 (1), 4 (2) (a), (d) and (e) of SEBI (Prohibition of Fraudulent and Unfair Trade Practices Relating to Securities Market) Regulations, 2003 (hereinafter referred to as ‘ PFUTP Regulations ’) alleged to have been committed by BMD Exports Pvt. -

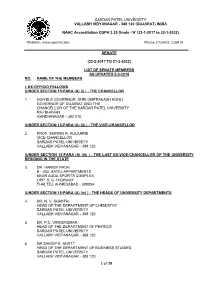

SENATE FINAL LIST AS on 5-3-2018 New.Pdf

SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120 (GUJARAT) INDIA NAAC Accreditation CGPA 3.25 Grade -'A' (23-1-2017 to 22-1-2022) Website : www.spuvvn.edu Phone: (02692) 226819 SENATE (22-2-2017 TO 21-2-2022) LIST OF SENATE MEMBERS AS UPDATED 5-3-2018 NO. NAME OF THE MEMBERS I. EX-OFFICIO FELLOWS (UNDER SECTION 15-PARA (A) (i) ) - THE CHANCELLOR 1. HON’BLE GOVERNOR. SHRI OMPRAKASH KOHLI GOVERNOR OF GUJARAT AND THE CHANCELLOR OF THE SARDAR PATEL UNIVERSITY RAJ BHAVAN GANDHINAGAR - 382 010. (UNDER SECTION 15-PARA (A) (ii) ) - THE VICE-CHANCELLOR 2. PROF. SHIRISH R. KULKARNI VICE-CHANCELLOR SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. (UNDER SECTION 15-PARA (A) (iii) ) - THE LAST EX-VICE-CHANCELLOR OF THE UNIVERSITY RESIDING IN THE STATE 3. DR. HARISH PADH B - 303, SATEJ APPARTMENTS NEAR AUDA SPORTS COMPLEX OPP. S. G. HIGHWAY THALTEJ, AHMEDABAD - 380054 (UNDER SECTION 15-PARA (A) (iv) ) - THE HEADS OF UNIVERSITY DEPARTMENTS 4. DR. N. V. SHASTRI HEAD OF THE DEPARTMENT OF CHEMISTRY SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. 5. DR. P.C. VINODKUMAR HEAD OF THE DEPARTMENT OF PHYSICS SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. 6. DR.SANDIP K. BHATT HEAD OF THE DEPARTMENT OF BUSINESS STUDIES, SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. 1 of 29 7. DR. DAYASHANKAR TRIPATHI HEAD OF THE DEPARTMENT OF HINDI SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. 8. DR. R. K. MANDALIYA HEAD OF THE DEPARTMENT OF ENGLISH SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. 9. DR. NIRANJANKUMAR PUNAMCHAND PATEL HEAD OF THE DEPARTMENT OF SANSKRIT SARDAR PATEL UNIVERSITY VALLABH VIDYANAGAR - 388 120. -

Pragati Sahakari Bank Ltd

To find your name press ctrl + F and type your name and press enter PRAGATI SAHAKARI BANK LTD. Unclaimed Deposit Amount Transfer to the Depositer Education and Awareness Fund Scheme 2014 (DEAF – 2015) on 30.09. -

Pragati Sahakari Bank Ltd

To find your name press ctrl + F and type your name and press enter PRAGATI SAHAKARI BANK LTD. Unclaimed Deposit Amount Transfer to the Depositer Education and Awareness Fund Scheme 2014 on 30 Septmber 2018 NAME ADDRESS P & P PROPERTY P LTD. 203 STERLING CENTER,R C DUTT ROAD,,VADODARA P D CONSTRUCTION 16.SATKAR SOC.,B/H.GHELANI PETROLPUMP,NIZAMPURA,VADODARA P D MEHTA 48, VIJAY SOC.,,,VADODARA P K CHATTERJEE 33, SHREYNAGAR SOC,SUBHANPURA,,VADODARA P K M ENTERPRISE KALAKUNJ SOCIETY,WATER TANK,KARELIBAUG,VADODARA,VADODARA P N ENTERPRISE 27/B SITABAUG SOT,MANJALPUR,,VADODARA P. JOSEPH GERALD MARKETING DIV.,A.C.W LTD,,VADODARA PABLA RAJINDER SINGH SARUP SINGH 10/10.GUJARAT REFINARY,POWNSHIP JAWAHARNAGAR,,VADODARA PADMA N KURLEKAR A/1,NIRMAN PARK,VISHWAMITRY RD,MANJALPUR,VADODARA PADMABEN AMRUTLAL SHAH FA/25, AL. COLONY,,,VADODARA PADMAKAR BALCHANDRA PATVARDHAN RAMJI MANDIR POLE,KOTHI, RAOPURA,,VADODARA PADMAKAR BHALCHANDRA PATWARDHAN A/7,MIRA SOC.NEAR HATHIBHAI-,-NBAGAR, DIWALIPURA,,VADODARA PADMARAI MURALI MISTRY RAJIV NAGAR,SAIYAD VASANA,,VADODARA PAHLAJ KHANCHAND MALKANI G/3, VIKRAM APPARTMENT,FATEHGANJ,,VADODARA PALAK PARESHBHAI PATEL BRHAMAN FALIYA,GORWA,,VADODARA PALAK PINAKIN PATEL 29, ASHOKNAGAR -1,OPP. LIONS HALL, RACE COURSE,,VADODARA PALAK S JOSHI A/18,SUNMOON PARK SOCIETY,NEAR AKOTA GARDEN,PRODUCTIVITY ROAD,VADODARA PALAK U PATEL B\54, ALEMBIC COLONY,,,VADODARA PALANILKUNNATHIL K SHASHI GOVT.POULTRY FARM,ALE.ROAD,,VADODARA PALASH CONSTRUCTION A\22,LAXMIKUNJ SOCIETY,NEW SAMA ROAD,NR.AYAPA TEMPLE,,VADODARA PALIDEVI RAMPURA YADAV -

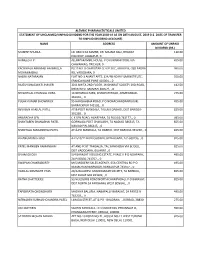

Name Address Amount of Unpaid Dividend (Rs.) Mukesh Shukla Lic Cbo‐3 Ka Samne, Dr

ALEMBIC PHARMACEUTICALS LIMITED STATEMENT OF UNCLAIMED/UNPAID DIVIDEND FOR THE YEAR 2018‐19 AS ON 28TH AUGUST, 2019 (I.E. DATE OF TRANSFER TO UNPAID DIVIDEND ACCOUNT) NAME ADDRESS AMOUNT OF UNPAID DIVIDEND (RS.) MUKESH SHUKLA LIC CBO‐3 KA SAMNE, DR. MAJAM GALI, BHAGAT 110.00 COLONEY, JABALPUR, 0 HAMEED A P . ALUMPARAMBIL HOUSE, P O KURANHIYOOR, VIA 495.00 CHAVAKKAD, TRICHUR, 0 KACHWALA ABBASALI HAJIMULLA PLOT NO. 8 CHAROTAR CO OP SOC, GROUP B, OLD PADRA 990.00 MOHMMADALI RD, VADODARA, 0 NALINI NATARAJAN FLAT NO‐1 ANANT APTS, 124/4B NEAR FILM INSTITUTE, 550.00 ERANDAWANE PUNE 410004, , 0 RAJESH BHAGWATI JHAVERI 30 B AMITA 2ND FLOOR, JAYBHARAT SOCIETY 3RD ROAD, 412.50 KHAR WEST MUMBAI 400521, , 0 SEVANTILAL CHUNILAL VORA 14 NIHARIKA PARK, KHANPUR ROAD, AHMEDABAD‐ 275.00 381001, , 0 PULAK KUMAR BHOWMICK 95 HARISHABHA ROAD, P O NONACHANDANPUKUR, 495.00 BARRACKPUR 743102, , 0 REVABEN HARILAL PATEL AT & POST MANDALA, TALUKA DABHOI, DIST BARODA‐ 825.00 391230, , 0 ANURADHA SEN C K SEN ROAD, AGARPARA, 24 PGS (N) 743177, , 0 495.00 SHANTABEN SHANABHAI PATEL GORWAGA POST CHAKLASHI, TA NADIAD 386315, TA 825.00 NADIAD PIN‐386315, , 0 SHANTILAL MAGANBHAI PATEL AT & PO MANDALA, TA DABHOI, DIST BARODA‐391230, , 0 825.00 B HANUMANTH RAO 4‐2‐510/11 BADI CHOWDI, HYDERABAD, A P‐500195, , 0 825.00 PATEL MANIBEN RAMANBHAI AT AND POST TANDALJA, TAL.SANKHEDA VIA BODELI, 825.00 DIST VADODARA, GUJARAT., 0 SIVAM GHOSH 5/4 BARASAT HOUSING ESTATE, PHASE‐II P O NOAPARA, 495.00 24‐PAGS(N) 743707, , 0 SWAPAN CHAKRABORTY M/S MODERN SALES AGENCY, 65A CENTRAL RD P O 495.00 -

Cadila Healthcare Limited Annual Report 2016-17 Contents

Cadila Healthcare Limited Annual Report 2016-17 Contents Management Business Directors’ Report Our culture Chairman’s Highlights of Discussion and Responsibility & relevant in a story Address Operations 2016-17 Analysis - 2016-17 Report Annexures 04 -11 12-15 16-17 18-32 33-40 41-73 Corporate Auditors’ Balance Statement of Cash Flow Statement of Governance Report Report Sheet Profit and Loss Statement Change in Equity 74-89 90-95 96 97 98-99 100 Notes to the Consolidated Notice of Financial Consolidated Financial Section 129 (3) Annual General Statements Auditors’ Report Statements Statement Meeting 101-164 165-169 170-239 240-241 242-256 Corporate Information Founder Board of Directors Directors Chief Financial Late Ramanbhai B. Patel Pankaj R. Patel Mukesh M. Patel Officer Chairman & Managing Director Humayun R. Dhanrajgir Nitin D. Parekh Dr. Sharvil P. Patel Nitin R. Desai Joint Managing Director Dharmishta N. Rawal Company Apurva S. Diwanji* Secretary *[w.e.f. May 13, 2016] Registered and Corporate Office Statutory Auditors Upen H. Shah “Zydus Tower”, Satellite Cross Roads, Mukesh M. Shah & Co. Sarkhej-Gandhinagar Highway, Chartered Accountants Zydus Research Centre Ahmedabad 380 015. Ahmedabad Survey No. 396 / 403, Sarkhej-Bavla N.H. No. 8A, Moraiya, Ahmedabad 382 213. Registrar and Share Transfer Agents Works Formulation Units API Units Topical Unit Link Intime India Private Limited Survey No. 417, 419 & 420, Block No. 265/266, Village: Plot No. 254-255, Opp. Laxmi Narayan 506-508, Amarnath Business Centre-1 Sarkhej-Bavla N.H. No. 8A, Changodar, Sarkhej-Bavla N.H. Petrol Pump, Sarkhej-Bavla N.H. No. -

Dr. Aliasgar J Kundawala Designation

Department Name : Pharmaceutics and Pharmaceutical Technology Name : Dr. Aliasgar J Kundawala Designation : Associate Professor and Head of Dept. Chairman, Board of studies, Faculty of Pharmaceutical Sciences, CVMU- Vallabh Vidyanagar. Email ID : [email protected] Qualification : M. Pharm., Ph. D. Specialization : Pharmaceutics Date of Joining : 1st November 2006 Research interest: . Drug delivery to lungs and brain.(Nano emulsion/ NLC/ Dry Powder Inhalers etc.) . Nanoparticulate and Microparticulate Drug delivery systems. Oral Controlled Release drug delivery systems (Matrix/ Osmotic pressure controlled) . Mouth dissolving Drug delivery systems. Publications: Shyamala Baskaran, Toutesh G and Kundawala A, A review: Zeta potential, The Pharma Review. Patel MR, Parikh JR, Patel RB, Kundawala AJ, Bhatt KK.: “Microemulsion: As novel Drug delivery Vehicle”:Pharminfo.net A. J. Kundawala S. Suresh, Narendra C., D. Maheshwari. “Formulation and Evaluation of Liposomes Containing Antitubercular Drugs by Taguchi’s Orthogonal Array design” Acta Pharmaceutica Sciencia. 52: 79-88 (2010) Kundawala A, Patel VA, Bhatt NV, Makwana JH, Patel HV. “Formulation and in- vitro evaluation of Clomipramine hydrochloride sustained release tablets”. Indian pharmacist, 2009,8, 63-69. A J Kundawala, V.A. Patel, R.S.R. Murthy and H.V.Patel, “Effect of Solvent and Non- Solvent Composition on Physical Characters of Mefloquine Hydrochloride Microsphers”. Int. J. of Pharam. Research. 2009, 1(4), 68-73. Page 1 of 7 Dhagla ram choudhary, Vishnu A Patel, Harsha V Patel, Aliasgar J Kundawala, “Formulation and Evaluation of Quick Dissolving Film of Levocetirizine Dihydrochloride”. Int. J of Pharm and Tech 2011, 3, 1740-49. Dhagla ram choudhary, Vishnu A Patel, Usmangani K Chhalotiya, Harsha V Patel, Aliasgar J Kundawala, “Formulation and Evaluation of quick Dissolving Film of Ondansetron hydrochloride”. -

Date of AGM(DD-MON-YYYY) 25-Jul-2016

Note: This sheet is applicable for uploading the particulars related to the unclaimed and unpaid amount pending with company. Make sure that the details are in accordance with the information already provided in e-form IEPF-2 CIN/BCIN L29199GJ1974PLC002574 Prefill Company/Bank Name EIMCO ELECON (INDIA ) LIMITED Date Of AGM(DD-MON-YYYY) 25-Jul-2016 Sum of unpaid and unclaimed dividend 294490.00 Sum of interest on matured debentures 0.00 Sum of matured deposit 0.00 Sum of interest on matured deposit 0.00 Sum of matured debentures 0.00 Sum of interest on application money due for refund 0.00 Sum of application money due for refund 0.00 Redemption amount of preference shares 0.00 Sales proceed for fractional shares 0.00 Validate Clear Proposed Date of Investor First Investor Middle Investor Last Father/Husband Father/Husband Father/Husband Last DP Id-Client Id- Amount Address Country State District Pin Code Folio Number Investment Type transfer to IEPF Name Name Name First Name Middle Name Name Account Number transferred (DD-MON-YYYY) A C AAIYAMPEROMA A C ARUNACHALAM 224 TEPPAM NORTH VIRUDHUNAGAINDIA Tamil Nadu 626001 EIMC0000000000001337 Amount for unclaimed and un 750.00 12-Aug-2022 A R RAMCHANDRAIH A R RAMCHANRAIH 49/1 APPAJ, ROA LANE C T STREET CINDIA Karnataka 560002 EIMC0000000000010516 Amount for unclaimed and un 500.00 12-Aug-2022 AARTI CHOUDHARY MANOJ KUMAR 3535/2 GALI NO 6 RAJA PARK RANI BINDIA Delhi 110034 EIMC0000000000004130 Amount for unclaimed and un 500.00 12-Aug-2022 ADITI AGARWAL ASHOK KUMAR AGARWAL LUCKNOW MILL STORES 24 G B MARINDIA Uttar Pradesh 226018 EIMC0000000000003452 Amount for unclaimed and un 250.00 12-Aug-2022 ADITYA BAFNA PRAKASH CHANDRA D-55 -B ROAD NO 3 LAXMI NAGAR D INDIA Delhi 110092 EIMC0000000000009232 Amount for unclaimed and un 750.00 12-Aug-2022 AHMEDKHAN NAGORI NA C/7 KASHMIRA SOC. -

TORCHBEARERS GG Sanjay Lalbhai Arvind

2SATURDAY, AUGUST 3, 2013 TULSI TANTI: He is the chairman and managing di- MUKESH AMBANI: rector of Pune-based Suzlon Energy, the India’s richest man, business tycoon Mukesh world’s largest supplier of wind tur- Ambani is the chairman and managing bines, a company he built from scratch. director of Reliance Industries Limited (RIL), a Fortune 500 company. Elder son of the legendary entrepreneur Dhirubhai Ambani, he is known for his leadership qualities and for putting Gujarat on the global map by setting up the largest refinery in the world at Jamnagar in the state. UDAY KOTAK: He is the vice chairman and man- aging director of Kotak Mahin- dra Bank in which he owns 50% “Gujaratis stake. In a recent interview, he stressed that solutions to India’s problems are not in running after are fun-loving” US dollars but fixing the manu- NITIN SHAH, Chairman and Managing facturing sector in the country. Director of Allied Digital shares his journey and his love for Gujarat in conversation with Rashmi Sanzgiri ILLUSTRIOUS : HOW HAS YOUR JOURNEY opportunities. I have my business QBEEN, FROM EMPLOYEE TO across the state and provide IT- EMPLOYER? service to bluechip companies like PIRUZ KHAMBATTA: MicroInfra, Torrent, Reliance and PERSONALITIES : After passing BE (Electronics) many other companies here. Afrom VJTI in 1977, I got a job in Gujarat is very close to my heart. He leads India’s largest and most CMC where I worked for six years. My roots are in Gujarat and I am India is home to some of the finest and most popular soft drink concentrate While I was there, I got a chance to thankful to the state. -

ZYDUS FAMILY TRUST Administrative Office: “Zydus Corporate Park”, Scheme No

ZYDUS FAMILY TRUST Administrative Office: “Zydus Corporate Park”, Scheme No. 63, Survey No. 536, Khoraj (Gandhinagar), Near Vaishnodevi Circle, Sarkhej–Gandhinagar Highway, Ahmedabad–382481 Date: May 11, 2020 Listing Department BOMBAY STOCK EXCHANGE LIMITED P J Towers, Dalal Street, Fort, Mumbai–400 001 Listing Department NATIONAL STOCK EXCHANGE OF INDIA LIMITED Exchange Plaza, Bandra Kurla Complex, Bandra (E), Mumbai–400 051 Re.: Disclosure under Regulation 30[1] & 30[2] of SEBI [Substantial Acquisition of Shares & Takeovers] Regulations, 2011 Dear Sir, Please find enclosed disclosure of shares held by Zydus Family Trust in Cadila Healthcare Limited, the Target Company, in the prescribed format as on March 31, 2020, pursuant to Regulation 30[1] & 30[2] of SEBI [Substantial Acquisition of Shares & Takeovers] Regulations, 2011. Please find the same in order and take the same on record. Thanking you, Yours faithfully, For, ZYDUS FAMILY TRUST Sd/‐ PANKAJ R. PATEL TRUSTEE Encl.: As above Copy to: The Company Secretary, Cadila Healthcare Limited DISCLOSURES UNDER REGULATION 30[2] OF SEBI [SUBSTANTIAL ACQUISITION OF SHARES & TAKEOVERS] REGULATIONS, 2011 Part–A–Details of Shareholding 1 Name of the Target Company [TC] Cadila Healthcare Limited 2. Name[s] of the Stock Exchange[s] where 1. National Stock Exchange of India Limited the shares of the TC are listed 2. BSE Limited 3. Particulars of the shareholder a. Name of person whose total holding Zydus Family Trust [including that in the form of shares, warrants, convertible securities and any other instrument that would entitle the holder to receive shares in the target company] is more than 25% of the shares or voting rights of the TC; Or b. -

The Amazing Story of Pankaj Patel

THE PATEL EXPRESS: The amazing story of Pankaj Patel By Ketan Trivedy (Ahmedabad) No, this is not the rags-to-riches story of a successful businessman. This is also not the saga of a man who has come to an unknown city with just bare minimum from his village and makes it big struggling against odds. In short, this is not the tale of an entrepreneur who has created something out of nothing. But wait, do not jump the guns, it is an interesting story nonetheless. It is full of struggles and quite inspiring. It involves the acumen of knowing the challenges in the changing circumstances and facing those challenges from the front. Though this story may not have the ingredients of typical struggle of the old generation for laying the foundation of an edifice of prosperity, it has the story of creating a strong building on a strong pillar. It has the funda of modern times and involves the next generation‟s intrepid entrepreneur‟s insight and subsequent success. This is the story of Pankajbhai Patel, the owner of Ahmedabad-based pharmaceutical company Zydus Cadilla having the market capitalization of Rs. 13308.65 crore. Pankajbhai Patel makes Aten tablet used by most to control their BP or the Sugar Free meant to be used by Diabetic patients or Ever Youth Face Wash used by women. While the threat of Swine Flu is looming large on the nation, this enterprising Patel has taken up the challenge of making H1N1 vaccine for the first time in India which was recently launched in the market.