The Beginning of The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Luminant 101 WHO WE ARE WHAT WE DO

Luminant 101 www.Luminant.com WHO WE ARE WHAT WE DO Luminant is the largest competitive Luminant’s generating power generation company in Texas. capacity consists of a Our activities include power plant, diverse mix of plants. mining, wholesale marketing and trading, • Nuclear- and and development operations. coal-fueled plants generate the bulk • We have more than 15,400 megawatts of of the energy and existing electric generation in Texas, including generally operate 2,300 MW fueled by nuclear power and continuously at 8,000 MW fueled by coal. capacity. They are • Almost 2,200 MW of our coal fleet is new high performing in safety and efficiency. generation. • Natural gas units help meet variable consumption • We have restored more than 73,000 acres as because they can more readily be ramped up or part of our lignite coal mining operations and down as demand warrants. planted more than 33 million trees. • We are a leading purchaser of wind-generated Our Generating Capacity 1 electricity in Texas and the United States. Total: 15,427 MW • We are a subsidiary of Energy Future Nuclear Holdings Corp. EFH is a Dallas-based 15% Coal energy holding company. For more 52% information, visit www.Luminant.com or www.energyfutureholdings.com. Natural Gas 33% Our 2012 Energy Production2 Total: 70,490 GWh Nuclear 28% FORT WORTH DALLAS TYLER Natural Gas Coal MIDLAND 2% 70% ODESSA WACO LUFKIN BRYAN/COLLEGE STATION AUSTIN HOUSTON SAN ANTONIO 1 Includes four mothballed units (1,655 MW) not currently available for dispatch 2 Excludes purchased power Mines Power Plants Gas Coal Nuclear Updated March 2013 Luminant 101 Our mining operations supply a portion of the fuel for the coal-fueled generation plants from more than 1,000 million tons of owned or leased Texas lignite coal reserves. -

Luminant a - Coastal Site

Comanche Peak Nuclear Power Plant, Units 3 & 4 COL Application Part 3 - Environmental Report CHAPTER 9 ALTERNATIVES TO THE PROPOSED ACTION TABLE OF CONTENTS Section Title Page 9.0 ALTERNATIVES TO THE PROPOSED ACTION ....................................................... 9.0-1 9.1 NO-ACTION ALTERNATIVE ...................................................................................... 9.1-1 9.1.1 IMPLICATIONS AND EFFECTS OF TAKING NO ACTION.................................. 9.1-1 9.2 ENERGY ALTERNATIVES......................................................................................... 9.2-1 9.2.1 ALTERNATIVES NOT REQUIRING NEW GENERATING CAPACITY ............... 9.2-1 9.2.1.1 Power Purchases ............................................................................................ 9.2-2 9.2.1.2 Plant Reactivation or Extended Service Life ................................................... 9.2-2 9.2.1.3 Conservation (Energy Efficiency) .................................................................... 9.2-3 9.2.1.4 Combination of Alternatives ............................................................................ 9.2-3 9.2.2 ALTERNATIVES REQUIRING NEW GENERATING CAPACITY ........................ 9.2-4 9.2.2.1 Wind ................................................................................................................ 9.2-7 9.2.2.2 Solar Thermal Power and Photovoltaic Cells ................................................ 9.2-10 9.2.2.3 Hydropower.................................................................................................. -

Energy Future Holdings and Mining Reclamation Bonds in Texas (Pdf)

Energy Future Holdings and Mining Reclamation Bonds in Texas By Tom Sanzillo Director of Finance Institute for Energy Economics and Financial Analysis A Report Prepared For: The Sierra Club Public Citizen Austin, Texas October, 2013 1 EXECUTIVE SUMMARY Energy Future Holdings (EFH) Company is publicly reported to be on the brink of a major financial reorganization. The financial problems of EFH and its subsidiaries stem from an ill-conceived buyout of TXU Corporation (the predecessor company) by the EFH management. The debt incurred for the buyout far exceeded the ability of the assets to pay for it. The company has stated that its top priority is debt management and most of its actions appear to be concerned with payment of debt service. 1 Energy Future Competitive Holdings (EFCH) is a subsidiary of EFH, which in turn has various subsidiaries that create a complex corporate structure. EFCH subsidiary Luminant Mining Company LLC, using Luminant Generation, also known as GENCO, as a third party insurer, has utilized a provision in Texas law that allows for a third party entity to guarantee the performance bond of the mining company. Luminant Mining and Luminant Generation have made multiple applications for such proposals amounting to $1.01 billion in self-bonding authority. 2 This report presents the case that recent applications made by Luminant Mining, using Luminant Generation as a third party guarantor to the Railroad Commission of Texas (RRC) for self- bonding authority, creates a misleading impression regarding Luminant Generation’s financial condition. Luminant Mining and Luminant Generation are subsidiaries of EFCH and EFH. -

Declaration of Ken Smith, Vice President of Construction Management, Luminant Generation Company LLC

Case: 16-60118 Document: 00513405270 Page: 63 Date Filed: 03/03/2016 Declaration of Ken Smith, Vice President of Construction Management, Luminant Generation Company LLC 60 Case: 16-60118 Document: 00513405270 Page: 64 Date Filed: 03/03/2016 DECLARATION OF KEN SMITH 1. I am vice president of construction management at Luminant, a competitive power generation subsidiary of Energy Future Holdings Corp. I will use “Luminant” in this declaration to refer to all Luminant entities that are petitioners in this matter. I make this declaration in support of Luminant’s motion to stay the Texas regional haze rule issued by the U.S. Environmental Protection Agency. See Approval and Promulgation of Implementation Plans; Texas and Oklahoma; Regional Haze State Implementation Plans; Interstate Visibility Transport State Implementation Plan To Address Pollution Affecting Visibility and Regional Haze; Federal Implementation Plan for Regional Haze, 81 Fed. Reg. 296 (Jan. 5, 2016) (“Final Rule”). This declaration is based on my personal knowledge and opinions which I am qualified to provide based on my education, training, and extensive experience in the power generation industry as discussed below. 2. As discussed in more detail below, the Final Rule, if not stayed by the Court, will cause immediate and irreparable harm to Luminant. The Final Rule imposes a massive build-out requirement on the majority of Luminant’s coal-fueled electric generating units. The harm from the Final Rule includes unrecoverable costs and expenditures, in the hundreds of millions of dollars, which Luminant would incur in the near term in order to begin work on the additional equipment and upgrades that EPA is requiring at Luminant’s generating units. -

2018 Annual Sustainability Report CONTENTS

2018 Annual Sustainability Report CONTENTS Our People ..................................................................................................2 Environmental Sustainability ...............................................................6 Our Products............................................................................................. 11 Our Governance ......................................................................................14 Our Headquarters and Regional Offices ....................................... 17 United Nations’ Sustainable Development Goals ...................... 18 Our Possibilities ...................................................................................... 19 Vistra Energy Power Plants* Natural Gas Coal Nuclear Solar / Batteries Oil Batteries (under development) Retail Operations Plant Operations Retail and Plant Operations Regional Office Company Headquarters *Note: Does not include plants previously announced to be retired. CEO’S MESSAGE As an integrated energy company, Vistra Energy operates an innovative, customer-centric retail business and a generation fleet focused on safely, reliably, and efficiently generating power in the communities we serve. Electricity is an irreplaceable product that is critical to everyday life, whether it be for residences or businesses. We understand and take very seriously our role to provide cost-effective, reliable power to our customers and help fuel the economy. We also understand and take very seriously that our business has an environmental footprint. -

Luminant 101 WHO WE ARE WHAT WE DO

Luminant 101 www.Luminant.com WHO WE ARE WHAT WE DO Luminant is the largest competitive Luminant’s generating power generation company in Texas. capacity consists of a Our activities include power plant, diverse mix of plants. mining, wholesale marketing and trading, • Nuclear- and and development operations. coal-fueled plants generate the bulk • We have more than 13,700 megawatts of of the energy and existing electric generation in Texas, including generally operate 2,300 MW fueled by nuclear power and continuously at 8,000 MW fueled by coal. capacity. They are • Almost 2,200 MW of our coal fleet is new high performing in safety and efficiency. generation. • Natural gas units help meet variable consumption • We have restored more than 73,000 acres as because they can more readily be ramped up or part of our lignite coal mining operations and down as demand warrants. planted more than 33 million trees. • We are a leading purchaser of wind-generated Our Generating Capacity 1 electricity in Texas and the United States. Total: 15,427 MW • We are a subsidiary of Energy Future Nuclear Holdings Corp. EFH is a Dallas-based 15% Coal energy holding company. For more 52% information, visit www.Luminant.com or www.energyfutureholdings.com. Natural Gas 33% Our 2012 Energy Production2 Total: 70,490 GWh Nuclear 28% FORT WORTH DALLAS TYLER Natural Gas Coal MIDLAND 2% 70% ODESSA WACO LUFKIN BRYAN/COLLEGE STATION AUSTIN HOUSTON SAN ANTONIO 1 Includes four mothballed units (1,655 MW) not currently available for dispatch 2 Excludes purchased power Mines Power Plants Gas Coal Nuclear Updated July 2015 Luminant 101 Our mining operations supply a portion of the fuel for the coal-fueled generation plants from more than 1,000 million tons of owned or leased Texas lignite coal reserves. -

News Release for IMMEDIATE RELEASE

News Release FOR IMMEDIATE RELEASE Luminant Announces Facility Closures, Job Reductions in Response to EPA Rule Company Forced to Take Difficult Steps; Files Suit to Protect Jobs, Reliability DALLAS – September 12, 2011 – In employee meetings today across its Texas operations, Luminant leadership announced the need to close facilities to comply with the Environmental Protection Agency’s Cross-State Air Pollution Rule, which will cause the loss of approximately 500 jobs. The rule, which the EPA released earlier this summer, requires Texas power generators to make dramatic reductions in emissions beginning January 1, 2012. While Luminant is making preparations to meet the rule’s compliance deadline, this morning it also filed a legal challenge in an effort to protect facilities and employees, and to minimize the harm this rule will cause to electric reliability in Texas. To meet the rule’s unrealistic deadline and requirements, Luminant reluctantly must take the difficult steps of idling two generating units and ceasing mining Texas lignite at three mines. Luminant will also implement several other actions to reduce emissions, including making substantial investments in its facilities. Luminant supports continued efforts to improve air quality across the state and nation. Since 2005, for example, Luminant has achieved a 21 percent reduction in SO2 emissions, while at the same time increasing generation by 13 percent. CEO Statement “As always, Luminant is committed to complying fully with EPA regulations. We have spent the last two months identifying all possible options to meet the requirements of this new rule, and we are launching a significant investment program to reduce emissions across our facilities,” said David Campbell, Luminant’s chief executive officer. -

Environmental Review ABOUT LUMINANT

2012 Environmental Review ABOUT LUMINANT GENERATING PLANTS AND MINES UNITS CAPACITY (MW) COUNTY NUCLEAR Comanche Peak 2 2,300 Somervell COAL Big Brown 2 1,150 Freestone Big Brown Freestone Among the most beautiful and prized birds, wood Turlington Freestone ducks were on the verge of extinction. Today, Martin Lake 3 2,250 Rusk they are a success story of proper protection and Beckville Panola/Rusk management. Luminant’s restored wildlife habitat, Oak Hill Rusk which includes nesting boxes and extensive water resources, helps the ducks thrive, and Tatum Panola their presence is a great indicator of sound land Monticello 3 1,880 Titus management and a healthy habitat. Thermo Hopkins Winfield Titus/Franklin Oak Grove 2 1,600 Robertson Kosse Limestone/Robertson Luminant, a subsidiary of Sandow 2 1,137 Milam Three Oaks Lee/Bastrop Energy Future Holdings Corp. NATURAL GAS1 competitive power generation DeCordova 4 CTs 260 Hood business, including mining, Graham 2 630 Young wholesale marketing and Lake Hubbard 2 921 Dallas trading,A and development operations, Morgan Creek 6 CTs 390 Mitchell Luminant has more than 15,400 Permian Basin 1, 5 CTs 865 Ward megawatts of generation in Texas, Stryker Creek 2 685 Cherokee including 2,300 MW fueled by Trinidad 1 244 Henderson nuclear power and 8,000 MW fueled Valley 3 1,115 Fannin by coal. The company is also one NUCLEAR COAL MINES NATURAL GAS CTs COMBUSTION TURBINES of the largest purchasers of wind- generated electricity in Texas and the nation. EFH is a Dallas-based energy holding company that has a portfolio GENERATION SUMMARY of competitive and regulated energy FUEL TYPE CAPACITY (MW) PLANTS UNITS subsidiaries, primarily in Texas. -

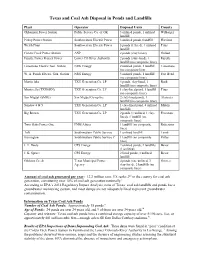

Texas and Coal Ash Disposal in Ponds and Landfills

Texas and Coal Ash Disposal in Ponds and Landfills Plant Operator Disposal Units County Oklaunion Power Station Public Service Co. of OK 3 unlined ponds, 1 unlined Wilbarger landfill Pirkey Power Station Southwestern Electric Power 3 unlined ponds,1landfill Harrison Welsh Plant Southwestern Electric Power 3 ponds (1 lined), 1 unlined Titus landfill Coleto Creek Power Station ANP 2 ponds (clay liners) Goliad Fayette Power Project Power Lower CO River Authority 2 ponds (clay-lined), 1 Fayette landfill (no composite liner) Limestone Electric Gen. Station NRG Energy 2 unlined ponds, 1 landfill Limestone (no composite liner W. A. Parish Electric Gen. Station NRG Energy 5 unlined ponds, 1 landfill Fort Bend (no composite liner) Martin lake TXU Generation Co. LP 4 ponds, clay-lined, 1 Rusk landfill (no composite liner) Monticello (TXUGEN) TXU Generation Co. LP 1 clay-lined pond, 1 landfill Titus (no composite liner) San Miguel (SMIG) San Miguel Co-op Inc. 2 clay-lined ponds, 1 Atascosa landfill (no composite liner) Sandow 4 & 5 TXU Generation Co. LP 1 clay-lined pond, 4 unlined Milam landfills Big Brown TXU Generation Co. LP 2 ponds (1 unlined, 1 clay- Freestone lined), 1 landfill (no composite liner) Twin Oaks Power One PNM Altura 1 landfill (no composite Robertson liner) Tolk Southwestern Public Service 1 unlined landfill Lamb Harrington Southwestern Public Service C 1 landfill (no composite Potter liner) J. T. Deely CPS Energy 2 unlined ponds, 2 landfills Bexar (1 unlined) J. K. Spruce CPS Energy 2 lined ponds, 1 unlined Bexar landfill Gibbons Creek Texas Municipal Power 4 ponds (one unlined, 3 Grimes Agency clay-lined), 2 landfills (no composite liner) Amount of coal ash generated per year: 12.2 million tons. -

Power Plant and Mine

Oak Grove Power Plant and Mine Economic Impact Oak Grove Power Plant and Kosse Mine are proud to be an integral part of the communities in which our employees work and live. In 2015, Luminant paid tens of millions of dollars statewide in property taxes. The company is the largest taxpayer by a wide margin in virtually all the communities where it operates plants, including Oak Grove. Community Benefit We take pride in being a good neighbor through community contributions and volunteerism. The plant and mines give tens of thousands of dollars to worthwhile projects and community organizations, such as the Robertson County Basic Facts Boys and Girls Club and area chambers of commerce. Fuel source: Lignite Employees at Oak Grove also give back to their Operating capacity and homes powered: communities through volunteerism, supporting 1,600 MW — enough to power the Robertson County Science Fair and Franklin about 800,000 homes in normal ISD mentoring programs, among others. conditions and about 320,000 homes in periods of peak demand Awards and Recognition Year began operation: Unit 1–2010; Unit 2–2010 Throughout the years, Oak Grove has been recognized as a community and corporate leader. A few significant awards include: Location: Robertson County, • Interstate Mining Compact Commission’s National Mine Reclamation Award Limestone County 2014 (Luminant) Supporting mine: Kosse • Railroad Commission of Texas’ Coal Mining Reclamation Award 2014 (Luminant) • Employee Recipients of the Brazos Valley Regional Advisory Council Lifesaving Award 2011 DALLAS Environmental Responsibility WACO Oak Grove TEMPLE Luminant is proud of its strong track record of meeting or outperforming all environmental laws, rules and regulations. -

Luminant and Subsidiaries

Comanche Peak Nuclear Power Plant Units 3 and 4 COL Application Part 1 Administrative and Financial Information Revision 0 (Non-Proprietary Version) Comanche Peak Nuclear Power Plant, Units 3 & 4 COL Application Part 1, General and Financial Information TABLE OF CONTENTS 1.0 INTRODUCTION ................................................................................................................... 3 1.1 LICENSE ACTIONS REQUESTED ....................................................................................... 3 1.2 GENERAL INFORMATION 1.2.1 Applicants.................................................................................................................. 4 1.2.2 Ownership of the Applicants ..................................................................................... 5 1.2.3 Description of Business or Occupation ..................................................................... 7 1.2.4 Organization and Management................................................................................. 7 1.2.5 Regulatory Agencies with Jurisdiction over Rates and Services............................... 10 1.2.6 Trade and News Publications ................................................................................... 11 1.3 FINANCIAL QUALIFICATIONS............................................................................................. 11 1.4 DECOMMISSIONING FUNDING ASSURANCE ................................................................... 13 1.5 FOREIGN OWNERSHIP OR CONTROL.............................................................................. -

Texas and Coal Ash Disposal in Ponds and Landfills Summary:1

Texas and Coal Ash Disposal in Ponds and Landfills Summary:1 Oklaunion Power Station Public Service Co. of 3 Ponds Wilbarger Oklahoma Pirkey Power Station Southwestern Electric Power 6 Ponds/landfill* Harrison Co. Welsh Plant Southwestern Electric Power 3 Ponds/landfill* Titus Co Coleto Creek Power Station ANP 2 Ponds Goliad Fayette Power Project Power Lower Colorado River 1 Ponds Fayette Station Authority Limestone Electric Generating NRG Energy 3 Ponds/landfill* Limestone Station W. A. Parish Electric Generating NRG Energy 8 Ponds/landfill* Fort Bend Station Martin lake TXU Generation Co. LP landfill* Rusk Monticello (TXUGEN) TXU Generation Co. LP landfill* Titus San Miguel (SMIG) San Miguel Co-op Inc. data indeterminate Atascosa Sandow 4 & 5 TXU Generation Co. LP landfill* Milam Big Brown TXU Generation Co. LP landfill* Freestone Twin Oaks Power One PNM Altura landfill* Robertson Tolk Southwestern Public Service data indeterminate Lamb Co. Harrington Southwestern Public Service data indeterminate Potter Co. J. T. Deely CPS Energy landfill* Bexar Sandow Station Alcoa U.S. landfill* Milam J. K. Spruce CPS Energy landfill* Bexar Gibbons Creek Texas Municipal Power landfill* Grimes Agency AES Deepwater AES NUGs data indeterminate Harris Odessa Ector Generating Station PSEG Global data indeterminate Ector Guadalupe Generating Station PSEG Global data indeterminate Guadalupe *indicates one or more coal ash landfills.2 Amount of coal ash generated per year: 13.1 million tons. TX ranks 2nd in the country for coal ash generation.3 The U.S. EPA has not yet gathered information on coal ash disposal in landfills, so a detailed breakdown is not yet available.