Security Analysis and Portfolio Management DCOM504/DMGT511

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

29:390:470:01 & 02 COURSE TITLE: Security Analysis

Department of Finance and Economics COURSE NUMBER: 29:390:470:01 & 02 COURSE TITLE: Security Analysis COURSE MATERIALS Lecture notes and assignments will be distributed via Blackboard. Required Textbooks: 1) “Value Investing – from Graham to Buffett and Beyond”, Bruce Greenwald, Judd Kahn, Paul Sonkin and Michael Biema. Wiley Finance. ISBN 0-471-46339-6 2) “The Warren Buffett Way”, 3rd Edition, Robert Hagstrom, Wiley Other readings (buy used copies): 3) “The Intelligent Investor”, Benjamin Graham. Revised Edition 2006 by Harper Collins Publishers. ISBN-10 0-06-055566-1 4) “Security Analysis”, 1951 Edition”, Benjamin Graham & David L. Dodd by McGraw Hill. ISBN 0-07-144820-9 5) “The Essays of Warren Buffett: Lessons for Corporate America”, First Revised Edition, by Lawrence A. Cunningham, ISBN-10: 0-9664461-1-9 6) “Investment Banking: Valuation, Leveraged Buyouts, and Mergers and Acquisitions”, Joshua Rosenbaum, Joshua Pearl and Joseph R. Perella (Wiley Finance) 2009. ISBN 978-0-470-44220-3 FINAL GRADE ASSIGMENT Grades Mid-Term: 40% Equity Challenge competition: 60% (team work) Teams: Each student must be part of a team of 4 members. Please take advantage of student diversity in your class. Your team is expected to work on class assignments and the equity challenge competition. 1 Department of Finance and Economics (29:390:470) COURSE SCHEDULE Course Outline Week 1: Principles of Security Analysis Lectures 1A & 1B Buying a business Lecture 1C Read Accounting Clinic 1 Appendix 1 Week 2: Balance Sheet, Income Statement Lectures 2A & 2B Appendix -

FM-404 Subject : Management of Financial Services

: 1 : Class : MBA Updated by : Dr. M.C. Garg Course Code : FM-404 Subject : Management of Financial Services LESSON-1 FINANCIAL SYSTEMS AND MARKETS STRUCTURE 1.0 Objective 1.1 Introduction 1.2 Concept of Financial System 1.3 Financial Concepts 1.4 Development of Financial System in India 1.5 Weaknesses of Indian Financial System 1.6 Summary 1.7 Keywords 1.8 Self Assessment Questions 1.9 Suggested Readings 1.0 OBJECTIVE After reading this lesson, you should be able to: (a) Understand the various concepts of financial system (b) Highlight the developments and weakness of financial system in India 1.1 INTRODUCTION A system that aims at establishing and providing a regular, smooth, efficient and cost effective linkage between depositors and investors is known as financial system. The functions of financial system are to channelise the funds from the surplus units to the deficit units. An efficient financial system not only encourages savings and investments, : 2 : it also efficiently allocates resources in different investment avenues and thus accelerates the rate of economic development. The financial system of a country plays a crucial role of allocating scare resources to productive uses. Its efficient functioning is of critical importance to the economy. 1.2 CONCEPT OF FINANCIAL SYSTEM Financial system is one of the industries in an economy. It is a particularly important industry that frequently has a far reaching impact on society and the economy. But if its occult trappings are stripped it is like any industry, a group of firms that combine factors of production (land, labour and capital) under the general direction of a management team and produce a product or cluster of products for sale in financial market. -

Ba7021 Security Analysis and Portfolio Management 1 Sce

BA7021 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT A Course Material on SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT By Mrs.V.THANGAMANI ASSISTANT PROFESSOR DEPARTMENT OF MANAGEMENT SCIENCES SASURIE COLLEGE OF ENGINEERING VIJAYAMANGALAM 638 056 1 SCE DEPARTMENT OF MANAGEMENT SCIENCES BA7021 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT QUALITY CERTIFICATE This is to certify that the e-course material Subject Code : BA7021 Subject : Security Analysis and Portfolio Management Class : II Year MBA Being prepared by me and it meets the knowledge requirement of the university curriculum. Signature of the Author Name : V.THANGAMANI Designation: Assistant Professor This is to certify that the course material being prepared by Mrs.V.THANGAMANI is of adequate quality. He has referred more than five books amount them minimum one is from abroad author. Signature of HD Name: S.Arun Kumar SEAL 2 SCE DEPARTMENT OF MANAGEMENT SCIENCES BA7021 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT CONTENTS CHAPTER TOPICS PAGE NO INVESTMENT SETTING 1.1 Financial meaning of investment 1.2 Economic meaning of Investment 7-25 1 1.3 Characteristics and objectives of Investment 1.4 Types of Investment 1.5 Investment alternatives 1.6 Choice and Evaluation 1.7 Risk and return concepts. SECURITIES MARKETS 2.1 Financial Market 2.2 Types of financial markets 2.3 Participants in financial Market 2.4 Regulatory Environment 2 2.5 Methods of floating new issues, 26-64 2.6 Book building 2.7 Role & Regulation of primary market 2.8 Stock exchanges in India BSE, OTCEI , NSE, ISE 2.9 Regulations of stock exchanges 2.10 Trading system in stock exchanges 2.11 SEBI FUNDAMENTAL ANALYSIS 3.1 Fundamental Analysis 3.2 Economic Analysis 3.3 Economic forecasting 3.4 stock Investment Decisions 3.5 Forecasting Techniques 3 3.6 Industry Analysis 65-81 3.7 Industry classification 3.8 Industry life cycle 3.9 Company Analysis 3.10Measuring Earnings 3.11 Forecasting Earnings 3.12 Applied Valuation Techniques 3.13 Graham and Dodds investor ratios. -

Security Analysis: an Investment Perspective

Security Analysis: An Investment Perspective Kewei Hou∗ Haitao Mo† Chen Xue‡ Lu Zhang§ Ohio State and CAFR LSU U. of Cincinnati Ohio State and NBER March 2020¶ Abstract The investment CAPM, in which expected returns vary cross-sectionally with invest- ment, profitability, and expected growth, is a good start to understanding Graham and Dodd’s (1934) Security Analysis within efficient markets. Empirically, the q5 model goes a long way toward explaining prominent equity strategies rooted in security anal- ysis, including Frankel and Lee’s (1998) intrinsic-to-market value, Piotroski’s (2000) fundamental score, Greenblatt’s (2005) “magic formula,” Asness, Frazzini, and Peder- sen’s (2019) quality-minus-junk, Buffett’s Berkshire Hathaway, Bartram and Grinblatt’s (2018) agnostic analysis, and Penman and Zhu’s (2014, 2018) expected return strategies. ∗Fisher College of Business, The Ohio State University, 820 Fisher Hall, 2100 Neil Avenue, Columbus OH 43210; and China Academy of Financial Research (CAFR). Tel: (614) 292-0552. E-mail: [email protected]. †E. J. Ourso College of Business, Louisiana State University, 2931 Business Education Complex, Baton Rouge, LA 70803. Tel: (225) 578-0648. E-mail: [email protected]. ‡Lindner College of Business, University of Cincinnati, 405 Lindner Hall, Cincinnati, OH 45221. Tel: (513) 556-7078. E-mail: [email protected]. §Fisher College of Business, The Ohio State University, 760A Fisher Hall, 2100 Neil Avenue, Columbus OH 43210; and NBER. Tel: (614) 292-8644. E-mail: zhanglu@fisher.osu.edu. ¶For helpful comments, -

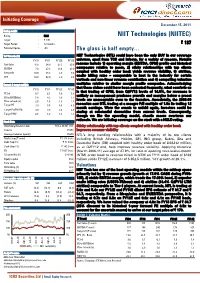

NIIT Technologies (NIITEC) Target : | 170 Target Period : 12 Months | 187 Potential Upside : -9% the Glass Is Half Empty…

Initiating Coverage December 15, 2011 Rating matrix Rating : Hold NIIT Technologies (NIITEC) Target : | 170 Target Period : 12 months | 187 Potential Upside : -9% The glass is half empty… YoY Growth (%) NIIT Technologies (NTL) could have been the only BUY in our coverage FY10 FY11 FY12E FY13E universe, apart from TCS and Infosys, for a variety of reasons. Notable Net Sales -6.8 34.9 27.3 20.9 reasons include 1) operating margin (EBITDA, OPM) profile and historical EBITDA 7.0 27.3 13.4 20.0 composure relative to peers, 2) sticky relationships with top clients Net profit 10.0 44.3 3.8 9.8 coupled with healthy order book yields revenue visibility, 3) attrition, EPS 10.0 42.9 3.0 9.8 onsite billing rates – comparable to best in the industry for certain verticals and non-linear revenue contribution and 4) compelling valuation Current & target multiple multiples relative to similar margin profile companies. Acknowledging that these claims could have been contested frequently, what comforts us FY10 FY11 FY12E FY13E is that trading of OPM, from Q2FY12 levels of 14.8%, for revenues is PE (x) 8.7 6.1 5.9 5.4 unlikely as management prudence prevails and margins below a preset EV to EBITDA(x) 5.4 4.3 3.8 3.1 levels are unacceptable even to the founders. Anecdotally, the 2008-09 Price to book (x) 2.0 1.6 1.3 1.1 recession saw NTL trading at a meagre P/E multiple of 1.9x its trailing 12 Target PE 7.9 5.5 5.4 4.9 month earnings. -

Notes from Security Analysis Sixth Edition Hardcover

Ronald R. Redfield CPA, PFS Notes to book “Security Analysis” 6th edition Written by: Benjamin Graham and David Dodd I thought these quotes from Security Analysis Sixth Edition Hardcover might be food for thought. Benjamin Graham and David Dodd first wrote security Analysis in 1934. The first edition was described by Graham as a “book that is intended for all those who have a serious interest in securities values.” The book was not designed for the investment novice. One must have an intermediate to advanced understanding of financial statements, accounting and finance for the book to be understood. The book emphasizes logical reasoning. Graham wrote, “It is the conservative investor who will need most of all to be reminded constantly of the lessons of 1931 –1933 and of previous collapses.” On Page [xiv] Seth Klarman wrote: ”Losing money, as Graham noted, can also be psychologically unsettling. Anxiety from the financial damage caused by recently experienced loss or the fear of further loss can significantly impede our ability to take advantage of the next opportunity that comes along. If an undervalued stock falls by half while the fundamentals – after checking and rechecking – are confirmed to be unchanged, we should relish the opportunity to buy significantly more “on sale.” But if our net worth has tumbled along with the share price, it may be psychologically difficult to add to the position.” On Page [xviii] Klarman wrote: ”Skepticism and judgment are always required.” “Because the value of a business depends on numerous variables, -

Value Investing Program Student Information Session

Value Investing Program Student Information Session February 20, 2020 ⧫ 12:30 p.m. Uris 301 ………………………………………………………………………………………………………………………………………… Agenda • Introduction to the Heilbrunn Center • Center Overview • Our Team • Our Courses • The Value Investing Program • Overview of the Program • Application Process • Debunking Myths • Testimonials: Q&A with current Value Investing Program students ………………………………………………………………………………………………………………………………………… 2 Heilbrunn Center: Overview ………………………………………………………………………………………………………………………………………… 3 Heilbrunn Center: Our Team Tano Santos Meredith Trivedi David L. and Elsie M. Dodd Managing Director Professor of Finance Julia Kimyagarov Caroline Reichert Director Associate Director ………………………………………………………………………………………………………………………………………… 4 Heilbrunn Center Courses (2020) Spring 2020 Tentative Fall 2020 Course Name Professor Course Name Professor Accounting for Value ~* Stephen Penman Advanced Investment Research #* Kian Ghazi Advanced Investment Research ^* Kian Ghazi Applied Value Investing #* Mark Cooper/Jonathon Luft Applied Security Analysis ~* Anuroop Duggal Applied Value Investing ~* Eric Almeraz/ David Horn Applied Value Investing #* T. Charlie Quinn Applied Value Investing (EMBA) ~+ Tom Tryforos Applied Value Investing #* Rishi Renjen/Kevin Oro-Hahn Art of Forecasting (B Term) ~* Ellen Carr Applied Value Investing #* Scott Hendrickson/ Matt Fixler Compounders *^ Anouk Dey/ Jeff Mueller Applied Value Investing ~* Anuroop Duggal Distressed Value Investing #~*+ Dan Krueger Art of Forecasting (B Term) ~* Ellen -

Pricing and Performance of Initial Public Offerings in the United States 1St Edition Pdf, Epub, Ebook

PRICING AND PERFORMANCE OF INITIAL PUBLIC OFFERINGS IN THE UNITED STATES 1ST EDITION PDF, EPUB, EBOOK Arvin Ghosh | 9781351496759 | | | | | Pricing and Performance of Initial Public Offerings in the United States 1st edition PDF Book Financial Times. Your Money. Your review was sent successfully and is now waiting for our team to publish it. Industrial and Commercial Bank of China. In particular, merchants and bankers developed what we would today call securitization. The Internet Bubble. However, due to transit disruptions in some geographies, deliveries may be delayed. Gregoriou, Greg Private shareholders may hold onto their shares in the public market or sell a portion or all of them for gains. In the US, clients are given a preliminary prospectus, known as a red herring prospectus , during the initial quiet period. In this timely volume on newly emerging financial mar- kets and investment strategies, Arvin Ghosh explores the intriguing topic of initial public offerings IPOs of securities, among the most significant phenomena in the United States stock markets in recent years. Although IPO offers many benefits, there are also significant costs involved, chiefly those associated with the process such as banking and legal fees, and the ongoing requirement to disclose important and sometimes sensitive information. Role of the Underwriters. In some situations, when the IPO is not a "hot" issue undersubscribed , and where the salesperson is the client's advisor, it is possible that the financial incentives of the advisor and client may not be aligned. View all volumes in this series: Quantitative Finance. Retrieved 4 March Literature Review and Data Source. -

Security Analysis and Investment Management

M.B.A IV Semester Course 406 FM-02 SECURITY ANALYSIS AND INVESTMENT MANAGEMENT LESSONS 1 TO 6 INTERNATIONAL CENTRE FOR DISTANCE EDUCATION AND OPEN LEARNING HIMACHAL PRADESH UNIVERSITY, GYAN PATH, SUMMERHILL, SHIMLA-171005 Contents Sr. No. Topoc Page No. LESSON-1 STOCK MARKET 1 LESSON-2 NEW ISSUE MARKET 15 LESSON-3 VALUATION OF SECURITIES 26 LESSON-4 FUNDAMENTAL ANALYSIS 37 LESSON-5 TECHNICAL ANALYSIS 58 LESSON-6 PORTFOLIO MANAGEMENT 80 LESSON-1 STOCK MARKET Structure 1.0 Learning Objectives 1.1 Introduction 1.2 Financial Market 1.3 Components of Financial Market 1.4 Stock Exchange 1.5 Nature and Characteristics of Stock Exchange 1.6 Function of Stock Exchange 1.7 Advantages of Stock Exchange 1.8 Organisation of Stock Exchange in India 1.9 Operational Mechanism of Stock Exchanges 1.10 Listing of Securities 1.11 Self-check Questions 1.12 Summary 1.13 Glossary 1.14 Answers: Self-check Questions 1.15 Terminal Questions 1.16 Suggested Readings 1.0 Learning Objectives After going through this lesson the learners should be able to: 1. Understand the financial market. 2. Discuss the components of financial market. 3. Understand the function of stock market. 4. Describe the operational mechanism of the stock exchange. 1.1 Introduction Stock market or secondary market is a place where buyer and seller of listed securities come together. This market is one of the important components of financial markets. In order to understand stock markets in detail, we shall understand the structure of financial market in an economy. Sections of this unit explain briefly the financial markets, components of financial markets, nature and functions of stock market, its Organization and statutory regulations for listing securities on stock markets. -

Security Analysis by Benjamin Graham and David L. Dodd

PRAISE FOR THE SIXTH EDITION OF SECURITY ANALYSIS “The sixth edition of the iconic Security Analysis disproves the adage ‘’tis best to leave well enough alone.’ An extraordinary team of commentators, led by Seth Klarman and James Grant, bridge the gap between the sim- pler financial world of the 1930s and the more complex investment arena of the new millennium. Readers benefit from the experience and wisdom of some of the financial world’s finest practitioners and best informed market observers. The new edition of Security Analysis belongs in the library of every serious student of finance.” David F. Swensen Chief Investment Officer Yale University author of Pioneering Portfolio Management and Unconventional Success “The best of the past made current by the best of the present. Tiger Woods updates Ben Hogan. It has to be good for your game.” Jack Meyer Managing Partner and CEO Convexity Capital “Security Analysis, a 1940 classic updated by some of the greatest financial minds of our generation, is more essential than ever as a learning tool and reference book for disciplined investors today.” Jamie Dimon Chairman and CEO JPMorgan Chase “While Coca-Cola found it couldn’t improve on a time-tested classic, Seth Klarman, Jim Grant, Bruce Greenwald, et al., prove that a great book can be made even better. Seth Klarman’s preface should be required reading for all investors, and collectively, the contributing editors’ updates make for a classic in their own right. The enduring lesson is that an understand- ing of human behavior is a critical part of the process of security analysis.” Brian C. -

Security Analysis (B8368-01) Spring 2020- Bidding Syllabus

Security Analysis (B8368-01) Spring 2020- Bidding Syllabus PROFESSOR: Michael J. Mauboussin TEACHING ASSISTANT: TBD Phone: 917-617-0950 Phone: TDB E-mail: [email protected] E-mail: TBD Classroom Location: TBD Wednesdays: 5:45 – 9:00 pm Office Hours: By appointment Communications from professor and teaching assistants about the course will take place through Canvas. Students should make sure they regularly check for announcements and messaging notifications. COURSE DESCRIPTION The course has two parts. The first part (14 to 16 lectures) develops the essential tools that a security analyst needs to come to a thoughtful investment recommendation. These tools include basic capital market concepts, analysis of competitive advantage, valuation methods, and techniques for proper decision making. The second part (8 sessions) allows the students to apply these lessons by presenting an analysis of a company and an investment conclusion regarding the shares of the company. A senior executive of a corporation will join the class toward the end of the first section to discuss competitive advantage. This session will give students the opportunity to question a management team directly on all facets of corporate strategy. Further, accomplished portfolio managers will attend student presentations to provide constructive feedback, to share their insights into the security analysis process, and to answer questions. The learning objective of the course is to combine various analytical frameworks and mental models into an investment recommendation. Further, students will learn to make a clear and persuasive presentation based on well-reasoned analysis. This course will be of most value to students who intend to pursue a career in investment management. -

A Leader of Value Investing in Asia

A Leader of Value Investing in Asia Value Partners is a leading Why Value Partners? Experienced and stable team We have one of the largest asset management Pioneer value investor in Asia on-the-ground investment teams We were one of the first fund with around 40 professionals firm in Asia. Since its managers in Asia to apply strict conducting in-depth company value investing principles in the early research and analysis. Many of establishment in 1993, 90s, and started investing in the them have been working together and under the leadership China domestic market when it had for more than 10 years. just begun to open up. of its Chairman and co-CIO Strong operational support and Greater China expertise stringent risk management Mr. Cheah Cheng Hye, the We are Greater China specialists Our clients are supported by a with extensive investment experience strong business operation team of company has successfully and in-depth local knowledge. over 100 professionals as well as As part of our research process, solid risk management systems. developed from a start-up our team conducted a large number boutique into one of of company visits every year. Asia’s most respected Proven track record and investment process asset managers. Over the years, we have delivered robust risk-adjusted absolute returns while maintaining low volatility throughout different market cycles. “Our employees pledge to put clients’ interest first and put our pride, not our ego, into our work.” Our product suite Value Partners offers a wide spectrum of investment solutions, ranging from actively managed products to passively traded index funds.