Orange PL – Telecom Offers Wholesale Fiber Access to T-Mobile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Raport Zintegrowany 2018 Orange Polska 1 Raport Zintegrowany 2018 Orange Polska Spis Treści

Raport Zintegrowany 2018 Orange Polska 1 Raport Zintegrowany 2018 Orange Polska Spis treści 4 Wprowadzenie 8 Firma i jej interesariusze O firmie Nasi interesariusze 14 Model biznesowy i tworzenie wartości Kluczowe zasoby Model biznesowy Otoczenie zewnętrzne Otoczenie wewnętrzne 38 Strategia Pytania do Prezesa Nasza strategia 50 Wyniki Pytania do Członka Zarządu ds. Finansów Wyniki modelu biznesowego Wyniki finansowe 78 Zarządzanie ryzykiem 86 Ład korporacyjny Nasze podejście do ładu korporacyjnego Struktura zarządzania 134 Wybrane dane finansowe 144 Załączniki Tabela GRI Metodologia Słownik 2 3 Wprowadzenie 4 5 Wprowadzenie Słowo wstępu O raporcie Szanowni Państwo! Podejście do raportów rocznych te zagadnienia, które są najważniejsze dla różnych grup interesariuszy. Raport zawiera także informacje o pośrednim Zapraszam do lektury naszego raportu rocznego – trzeciego, wpływie Orange Polska na łańcuch wartości poprzez budowanie w którym wyniki Orange Polska prezentujemy w zintegrowanej for- Orange Polska ma przyjemność zaprezentować trzeci relacji z dostawcami, organami państwowymi oraz partnerami mie. Łącząc fi nansowe i pozafi nansowe aspekty naszej działalnoś- zintegrowany raport roczny. Raport publikowany jest co biznesowymi i społecznymi. Poruszona została kwestia wpływu ci, chcemy pokazać Państwu szerszy kontekst naszych działań, roku. Poprzedni raport zintegrowany opublikowany został na gospodarkę, społeczności lokalne i środowisko. W raporcie a w szczególności sposób reagowania na zmiany w zewnętrznym w kwietniu 2018 roku. Kontynuujemy -

Orange Partners with APG for the Deployment of an Additional 1.7M FTTH Plugs in Poland Through a 50-50 Joint Venture Valued at 605 Million Euros

Press release Paris, 12 April 2021 Orange partners with APG for the deployment of an additional 1.7m FTTH plugs in Poland through a 50-50 joint venture valued at 605 million euros Orange Polska announced today the creation of a FiberCo co-owned (50-50) with APG. This joint venture aims to support the rollout of fiber in Poland, in areas where access to very high-speed broadband infrastructure is limited or inexistent. The FiberCo integrates 2.4 million lines, including 1.7 million households that will be deployed over the next five years. This transaction values the joint venture at 2,748 million PLN (605 million euros) following a competitive process aimed at seeking out a long-term partner. As a result, Orange Polska will receive 1,374 million PLN (303 million euros) from APG, of which 65% will be transferred on closing and the rest between 2022 and 2026 as the deployment plan advances. This project will allow Orange Polska to pursue its ambitious fiber-optic rollout strategy by sharing investment costs. Click here for further details. This announcement follows other Orange Group announcements including the creation of Orange Concessions in January 2021 and the outline of the European Towerco Totem in February 2021. As such, Orange continues to deploy its infrastructure strategy as set-out in its Engage 2025 plan. Commenting on the partnership in Poland, Mari-Noëlle Jégo-Laveissière, Deputy CEO of Orange in charge of European Operations (outside France), said: “This partnership with APG is excellent news for Orange Polska. APG is a global leader in infrastructure management and will provide us with the financial backing necessary to achieve our ambitious five-year fiber roll-out program in Poland. -

Prezentacja Programu Powerpoint

Cyfrowy Polsat IR Newsletter 10 – 16 February 2020 Press review Biznes.pap.pl Netia’s network with the data transfer speed up to 1 Gbps reaches over 1.4 million households 10 February 2020 By kuc/ ana/ The upgraded Netia’s network with data transfer speed up to 1 Gbps reaches over 1.4 million households, informed Tomasz Dakowski a Member of the Management Board, while stating that due to the dynamics of the investment process, the company “had already moved passed" the biggest growth of the network coverage. Since 2016 Netia has carried out an investment into the fiber-optic network which should consume the total of PLN 418 million. Under the network upgrade, Netia intends to cover 2.55 million of households with the fiber-optic network with 1 Gbps data transfer speed. The operator plans to complete the work related to the network upgrade by the end of the first quarter of 2020 at the latest, and the investment shall be finally settled by the end of 2020. On Friday, the company informed about a new offer of bundled services. A bundle for PLN 60 will be the basic package offered to customers; currently the main offer of the Company is the package for PLN 50 per month. However, a new, more expensive basic package will include two additional services. Similar changes have been introduced to the remaining packages with higher data transfer rates and bigger number of TV channels. Dakowski informed that the company was currently providing Internet access services to 380-400 thousand retail customers on its own network, while simultaneously half of them also use television services offered by the company. -

Ubezpieczenie Sprzętu Elektronicznego Raport Rzecznika

UBEZPIECZENIE SPRZĘTU ELEKTRONICZNEGO RAPORT RZECZNIKA FINANSOWEGO Warszawa, listopad 2016 r. Spis treści Wstęp ……… ............................................................................................................................................. 2 Rozdział I. Istota produktu ubezpieczeniowego ................................................................................. 10 1. Zarządzanie i cykl życia produktu ubezpieczeniowego ................................................................ 11 2. Kompozycja marketingowa .......................................................................................................... 14 3. Różnice pomiędzy instytucjami ubezpieczenia, gwarancji ubezpieczeniowej a rękojmi i gwarancji producenta i sprzedawcy ........................................................................... 21 4. Przedmiot ubezpieczenia .............................................................................................................. 30 5. Zakres ubezpieczenia .................................................................................................................... 32 6. Zawarcie i przystąpienie do umowy ubezpieczenia ..................................................................... 40 7. Pozostałe elementy ubezpieczenia .............................................................................................. 43 Rozdział II. Sprzedaż ubezpieczeń sprzętu elektronicznego ............................................................... 52 1. Dystrybucja ubezpieczeń ............................................................................................................. -

GUD) Do Świadczenia Usługi Sprzedaży Energii Elektrycznej Na Obszarze Działania Innogy Stoen Operator Sp

innogy Stoen Operator Sp. z o.o. adres do korespondencji: ul. Nieświeska 52 03-867 Warszawa T +48 22 821 31 31 F +48 22 821 31 32 E [email protected] I www.innogystoenoperator.pl Lista przedsiębiorstw obrotu energią elektryczną , upoważnionych na mocy Generalnej Umowy Dystrybucyjnej (GUD) do świadczenia usługi sprzedaży energii elektrycznej na obszarze działania innogy Stoen Operator Sp. z o.o. (w kolejności podpisywania GUD). Data aktualizacji: 15.04.2019 r. 1. TAURON Sprzedaż GZE Sp. z o.o. 2. PKP Energetyka S.A. 3. innogy Polska S.A. - Sprzedawca z urzędu (*) (**) 4. Veolia Energia Polska S.A. 5. ENERGA-OBRÓT S.A. 6. CEZ Trade Polska Sp. z o.o. 7. PGE Energia Cieplna S.A. 8. FITEN S.A. 9. TAURON Sprzedaż Sp. z o.o. 10. PGE Obrót S.A. 11. Enea Elektrownia Połaniec S.A. 12. Slovenské Elektrárne, a.s. Spółka Akcyjna Oddział w Polsce 13. Alpiq Energy Spółka europejska Oddział w Polsce 14. Tauron Polska Energia S.A. 15. Przedsiębiorstwo Energetyczne ESV S.A. 16. Elektrix Sp. z o.o. 17. 3 WINGS Sp. z o.o. 18. Energia dla Firm S.A. (***) 19. ENIGA Edward Zdrojek 20. POWERPOL Sp. z o.o. (***) 21. Elektrociepłownia Andrychów Sp. z o.o. 22. ProPower 21 Sp. z o.o. 23. Energetyczne Centrum S.A. (***) 24. Fortum Marketing and Sales Polska S.A. 25. ERGO ENERGY Sp. z o.o. 26. Inter Energia sp. z o.o. 27. TRADEA Sp. z o.o. 28. GOEE ENERGIA Sp. z o.o. (***) 29. POLENERGIA OBRÓT S.A. -

20% Więcej Za Doładowanie Cykliczne

Regulamin promocji doładowań „20% więcej za doładowanie cykliczne” obowiązuje od dnia 18 września 2015 r. do odwołania. „20% więcej za doładowanie cykliczne” („Promocja”) to promocja doładowań umożliwiająca Abonentom taryf: Nowe Orange Go, Orange POP, Orange One oraz Orange Yes na kartę w Orange oraz Abonentom sieci Orange korzystającym z ofert Mix („Abonenci”) uzyskanie dodatkowych środków za doładowanie konta. jak skorzystać: 1. Warunkiem skorzystania z Promocji jest zdefiniowanie w serwisie bankowym doładowania dla numeru telefonu Abonenta poprzez usługę doładowania cyklicznego kwotą 10, 30, 40, 50, 100 lub 200 zł. 2. Promocja dostępna jest w serwisach transakcyjnych iPKO oraz Inteligo prowadzonych przez PKO Bank Polski S.A. 3. Doładowania, o których mowa w pkt 1 należy dokonać nie wcześniej niż o godzinie 00:01 dnia 18 września 2015 r. jak korzystać? 4. Do każdego doładowania wykonanego zgodnie z pkt 1 – 3 w ramach Promocji przyznane zostaną dodatkowe jednostki taryfowe („Bonus”) o wartości: . 2 zł za doładowanie nominałem 10 zł . 6 zł za doładowanie nominałem 30 zł . 8 zł za doładowanie nominałem 40 zł . 10 zł za doładowanie nominałem 50 zł . 20 zł za doładowanie nominałem 100 zł . 40 zł za doładowanie nominałem 200 zł 5. Bonus wpłynie na konto promocyjne Abonenta w ciągu maksimum 24 godzin od momentu doładowania konta, o którym mowa w pkt 1, a o wpłynięciu bonusu Abonent zostanie poinformowany wiadomością SMS. 6. Środki przyznane w ramach Bonusu gromadzą się na koncie promocyjnym Abonenta i mogą być wykorzystane zgodnie z regulaminem usługi „Konto promocyjne”. 7. Termin ważności środków w ramach Bonusu wynosi 14 dni. 8. Stan i ważność konta promocyjnego (Bonusu) można sprawdzić: - wysyłając SMS-a o treści ILE pod numer 1555 (koszt SMS-a wg planu taryfowego), - dzwoniąc pod numer *500, - logując się na www.orange.pl - poprzez krótki kod *124*# [zadzwoń] ile to kosztuje: 9. -

Cyfrowy Polsat S.A. Capital Group

CYFROWY POLSAT S.A. CAPITAL GROUP Interim Consolidated Report for the six month period ended June 30, 2020 Place and date of publication: Warsaw, August 27, 2020 Place and date of approval: Warsaw, August 26, 2020 Interim Consolidate Report of Cyfrowy Polsat Group for the six-month period ended June 30, 2020 TABLE OF CONTENTS REPORT OF THE MANAGEMENT BOARD ON THE ACTIVITIES OF CYFROWY POLSAT S.A. CAPITAL GROUP FOR THE SIX MONTH PERIOD ENDED JUNE 30, 2020 POLSAT GROUP AT A GLANCE ............................................................................................................................................. 4 DISCLAIMERS ........................................................................................................................................................................... 5 FINANCIAL DATA OVERVIEW ................................................................................................................................................. 6 1. CHARACTERISTICS OF POLSAT GROUP ................................................................................................................. 9 2. SIGNIFICANT EVENTS ............................................................................................................................................... 22 3. OPERATING AND FINANCIAL REVIEW OF POLSAT GROUP ................................................................................ 27 4. OTHER SIGNIFICANT INFORMATION ..................................................................................................................... -

Winter in Prague Tuesday 5 December to Friday 8 December 2017

emerging europe conference Winter in Prague Tuesday 5 December to Friday 8 December 2017 Our 2017 event held over 4 informative and jam-packed days, will continue the success of the previous five years and host almost 3,000 investor meetings, with over 160 companies representing 17 countries, covering multiple sectors. For more information please contact your WOOD sales representative: WOOD & Company Save Warsaw +48 222 22 1530 the Date! Prague +420 222 096 452 conferences 2017 London +44 20 3530 0611 [email protected] Participating companies in 2016 - by country Participating companies in 2016 - by sector Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Asseco Poland AT&S Budapest Stock Exchange Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka AT&S CA Immobilien Magyar Telekom Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim CME Conwert MOL Group Electrica Cimsa Arcelik Banca Transilvania Cyfrowy Polsat S.A. Erste Bank OTP Bank Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Luxoft Immofinanz Wizz Air Hidroelectrica Dogan Holding Atlantic Grupa BGEO Aeroflot Magyar Telekom PORR Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Zachodni WBK Cimsa O2 Czech Republic RHI Kazakhstan OMV Petrom Ford Otosan CCC Bucharest Stock Exchange Ciech Orange Polska Uniqa Insurance Group Steppe Cement Romgaz Garanti Coca-Cola Icecek Budapest Stock Exchange Dogus Otomotiv OTE Vienna -

Current Report 5/2021 Orange Polska S.A., Warsaw, Poland 21 April, 2021

Current Report 5/2021 Orange Polska S.A., Warsaw, Poland 21 April, 2021 Pursuant to Article 17(1) of the Regulation (EU) No. 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC, the Management Board of Orange Polska S.A. hereby provides selected financial and operating data related to the activities of the Orange Polska Capital Group (“the Group”, “Orange Polska”) for 1Q 2021. Disclosures on performance measures, including information on data restatements are presented in the Note 2 and 4 to Condensed IFRS Quarterly Consolidated Financial Statements of the Orange Polska Group for the 3 months ended 31 March 2021 (available at https://www.orange-ir.pl/results-center/). The accounting policies changed by the Group in 2020 relate to the determination of the lease term of cancellable lease. In 1Q 2021 Orange Polska reports strong financial results in line with full-year plans, and solid commercial performance despite pandemic restrictions key figures 1Q 2021 1Q 2020 Change (PLN million) restated Revenue 2,918 2,804 +4.1% EBITDAaL 709 673 +5.3% EBITDAaL margin 24.3% 24.0% +0.3p.p. operating income 116 88 +31.8% net income/(loss) 39 -38 +77m eCapex 445 343 +29.7% organic cash flow 198 -78 +276m 1 KPI (‘000) 1Q 2021 1Q 2020 Change convergent customers (B2C) 1,503 1,387 +8.4% mobile accesses (SIM cards) 15,800 15,436 +2.4% post-paid 11,017 -

Alior, JSW, Orange Polska, Pgnig

Dziennik 20 lutego 2019 r. Najważniejsze informacje: Indeksy GPW zmiana WIG otw. 59 571,2 -0,6% Alior - Alior ocenia, że efekt kapitałowy wdrożenia AMA może być większy niż 37 pb na Tier1 WIG zam. 59 477,3 -0,2% JSW - ME zaskoczone planami potencjalnej emisji akcji JSW - Tobiszowski obrót (mln PLN) 683,8 28,3% Orange Polska - Jean-Francois Fallacher prezesem Orange Polska na kolejną kadencję WIG 20 otw. 2 324,7 -0,7% WIG 20 zam. 2 322,4 -0,1% PGNiG - PGNiG wydobyło 3,8 mld m sześc. gazu w '18, z sukcesem zakończyło prawie 85% FW20 otw. 2 329,0 high wierceń FW20 zam. 2 330,0 0,0% PKN Orlen - PKN Orlen porozumiał się ze związkami zawodowymi ws. wzrostu wynagrodzeń i mWIG40 otw. 4 085,2 -0,4% nagród mWIG40 zam. 4 077,1 -0,2% Sektor energetyczny - Odkrywka Złoczew nie stoi w sprzeczności z ewentualną budową atomu w okolicy Bełchatowa Największe wzrosty kurs zmiana Ambra - Ambra przewiduje ok. 5% wzrost rynku wina w Polsce w kolejnych latach Eurocash 19,52 3,0% Alior Bank 59,35 2,8% Braster - Braster ma umowę z dystrybutorem na rynek indyjski Asseco Poland 53,85 2,6% Izostal, Stalprofil - Oferta konsorcjum za 121,3 mln PLN netto najkorzystniejsza w przetargu Telekom Austria AG 6,38 2,4% Gaz-Systemu Grupa Azoty 46,28 1,9% MLP Group - MLP Group planuje w tym roku rozpocząć budowę parku logistycznego w pobliżu Lublina Największe spadki kurs zmiana Novaturas - Strata netto Novaturas w IV kw. 2018 r. wyniosła 0,2 mln euro BGŻ BNP Paribas 48,50 -4,9% Trakcja - Trakcja liczy, że do połowy '19 zamknie proces związany z refinansowaniem i emisją Dom Development 72,00 -4,5% ZE PAK 7,95 -2,7% Ursus - Konsorcjum Ursusa jedyne w projekcie bezemisyjnego transportu publicznego na Forte 24,10 -2,2% ponad 1 tys. -

Warsaw, December 17, 2020 Konrad Księżopolski, Head of Research

Warsaw, December 17, 2020 Konrad Księżopolski, Head of Research, Haitong Bank Haitong Bank in a report from December 14 (08:00) updates recommendations on Polish TMT companies: • Cyfrowy Polsat (BUY, FV PLN 32.3) • Orange Polska (NEUTRAL, FV PLN 7) • Play Communications (NEUTRAL, FV PLN 37.3) • Netia (NEUTRAL, FV PLN 4.9) • Asseco Poland (BUY, FV PLN 78.1) • Comarch (BUY, FV PLN 226.7) • LiveChat (BUY, FV PLN 126.6) • Ten Square Games (BUY, FV PLN 690) • Wirtualna Polska (NEUTRAL, FV PLN 82.8) Valuation Methodology Cyfrowy Polsat We value Cyfrowy Polsat using a DCF and peer multiples. Using a DCF we arrive at PLN 30.4/sh while our peer valuation yields PLN 34.2/sh. Our final fair value is PLN 32.3/sh, implying 16% potential upside. Orange Polska We value Orange Polska using a DCF and peer multiples where DCF and peers have a 50% weight each. As Orange Polska does not pay dividends, we stopped valuing the stock using the DDM method. Using a DCF, we derive a fair value of PLN 7.7 and using peers of PLN 6.2. Our fair value is PLN 7.0, implying 7% upside potential to the current share price Play Communications We value Play using a DCF, DDM and peer multiples. Using a DCF, we derive a fair value of PLN 34.6; using DDM we arrive at PLN 33.5 and peers of PLN 43.9. Applying an equal weighting to each valuation method we obtain a fair value of PLN 37.3, implying 3% downside potential to the current share price. -

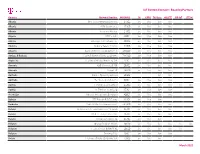

Iot Custom Connect - Roaming Partners

IoT Custom Connect - Roaming Partners Country Column1 Network Provider Column2MCCMNCColumn10 Column32G Column4GPRS Column53G Data Column64G/LTE Column7NB-IoT LTE-M Albania One Telecommunications sh.a 27601 live live live live Albania ALBtelecom sh.a. 27603 live live live live Albania Vodafone Albania 27602 live live live live Algeria ATM Mobilis 60301 live live live live Algeria Wataniya Telecom Algerie 60303 live live live live Andorra Andorra Telecom S.A.U. 21303 live live live live Anguilla Cable and Wireless (Anguilla) Ltd 365840 live live live live Antigua & Barbuda Cable & Wireless (Antigua) Limited 344920 live live live live Argentina Telefónica Móviles Argentina S.A. 72207 live live live live Armenia VEON Armenia CJSC 28301 live live live live Armenia Ucom LLC 28310 live live live live Australia SingTel Optus Pty Limited 50502 live live Australia Telstra Corporation Ltd 50501 live live live live Austria T-Mobile Austria GmbH 23203 live live live live live live Austria A1 Telekom Austria AG 23201 live live live live Azerbaijan Bakcell Limited Liable Company 40002 live live live live Bahrain STC Bahrain B.S.C Closed 42604 live live live Barbados Cable & Wireless Barbados Ltd. 342600 live live live live Belarus Belarusian Telecommunications Network 25704 live live live live Belarus Mobile TeleSystems JLLC 25702 live live live live Belarus Unitary Enterprise A1 25701 live live live Belgium Orange Belgium NV/SA 20610 live live live live live live Belgium Telenet Group BVBA/SPRL 20620 live live live live live Belgium Proximus PLC 20601 live live live live Bolivia Telefonica Celular De Bolivia S.A. 73603 live live live March 2021 IoT Custom Connect - Roaming Partners Country Column1 Network Provider Column2MCCMNCColumn10 Column32G Column4GPRS Column53G Data Column64G/LTE Column7NB-IoT LTE-M Bosnia and Herzegovina PUBLIC ENTERPRISE CROATIAN TELECOM Ltd.