Integrated Reporting As a Driver for Integrated Thinking?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View Annual Report

Cautionary note with regard to “forward-looking statements” Some statements in this Annual Report are “forward-looking statements”. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that may occur in the future. These forward-looking statements involve known and unknown risks, uncertainties and other factors that are beyond PostNL’s control and impossible to predict and may cause actual results to differ materially from any future results expressed or implied. These forward-looking statements are based on current expectations, estimates, forecasts, analyses and projections about the industries in which PostNL operates and PostNL management’s beliefs and assumptions about future events. You are cautioned not to put undue reliance on these forward-looking statements, which only speak as of the date of this Annual Report and are neither predictions nor guarantees of future events or circumstances. PostNL does not undertake any obligation to release publicly any revisions to these forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws. Table of Contents 1 We are PostNL 3 2 Message from Herna Verhagen 11 24 hours in PostNL Business Report 3 How we create long-term value 15 4 Our strategy 22 5 What sets us apart 31 6 Mail in the Netherlands 42 7 Parcels 48 8 International 55 9 Performance 2017 and outlook 2018 -

DSM's Integrated Annual Report 2015

Royal DSM Integrated Annual Report 2015 WorldReginfo - c41a4efa-17eb-497c-8f68-03022dabfb88 WorldReginfo - c41a4efa-17eb-497c-8f68-03022dabfb88 DSM at a glance Nutrition DSM Resins & Functional Materials is a global player in developing, manufacturing and marketing high-quality resins The Nutrition cluster comprises DSM Nutritional Products and solutions for paints, industrial coatings and fiber-optic coatings. DSM Food Specialties.These businesses serve the global Continuous innovation means that customers can meet industries for animal feed, food and beverage, pharmaceutical, regulatory needs and respond better to consumer demands for infant nutrition, dietary supplements and personal care. more sustainable materials. DSM Nutritional Products is one of the world’s leading Innovation Center producers of essential nutrients such as vitamins, carotenoids, nutritional lipids and other ingredients to the feed, food, DSM Innovation Center serves as an enabler and accelerator pharmaceutical and personal care industries. Among its of innovation within DSM as well as providing support to the customers are the world’s largest food and beverage clusters. With its Emerging Business Areas, the Business companies. DSM is uniquely positioned thanks to the Incubator and DSM Venturing & Licensing, the DSM Innovation combination of its broad portfolio of active ingredients, maximum Center has a general business development role, focusing on differentiation through formulation, local presence, a global areas outside the current scope of the business groups. premix network, and a strong focus on innovation. DSM Nutritional Products consists of the following business units: DSM’s Emerging Business Areas provide strong long-term growth platforms based on the company’s core competences Animal Nutrition & Health addresses the nutritional additives in life sciences and materials sciences. -

Royal DSM N.V. Annual Report 2006

Royal DSM N.V. Annual Report 2006 Brighter Wider Better Together DSM Profile DSM is active worldwide in nutritional and pharma ingredients, performance materials and industrial chemicals. The company develops, produces and sells innovative products and services that help improve the quality of life. DSM’s products are used in a wide range of end-markets and applications, such as human and animal nutrition and health, personal care, pharmaceuticals, automotive and transport, coatings and paint, housing and electrics & electronics (E&E). DSM’s strategy, named Vision 2010 – Building on Strengths, focuses on accelerating profitable and innovative growth of the company’s specialties portfolio. The key drivers of this strategy are market-driven growth and innovation plus an increased presence in emerging economies. The group has annual sales of over €8 billion and employs some 22,000 people worldwide. DSM ranks among the global leaders in many of its fields. The company is headquartered in the Netherlands, with locations in Europe, Asia, Africa, Australia and the Americas. More information about DSM can be found at www.dsm.com. Annual Report 2005 www.dsm.com DSM at a glance DSM’s activities have been grouped into business groups representing coherent product / market combinations. The business group directors report directly to the Managing Board. Nutrition Pharma €2,407m €916m DSM Nutritional Products DSM Pharmaceutical Products DSM Nutritional Products is the world’s largest supplier of nutri- DSM Pharmaceutical Products is one of the world’s leading tional ingredients, such as vitamins, carotenoids (anti-oxidants providers of high quality global custom manufacturing services and pigments), other biochemicals and fine chemicals, and to the pharmaceutical, biotech and agrochemical industries. -

Remuneration Report

REMUNERATION REPORT The first part of this report outlines the remuneration policy REMUNERATION POLICY for the Board of Management as it has been adopted over The main objective of Fugro’s remuneration policy is to time, while the second part contains details of the attract, motivate and retain qualified management that is remuneration in 2015 of the members of the Board of needed for a global company of the size and complexity of Management and of the Supervisory Board. Fugro. The members of the Board of Management are More information on remuneration and on option and share rewarded accordingly. Variable remuneration is an important ownership of members of the Board of Management is part of the total package. The remuneration policy aims at available in note 5.64.2 of the financial statements in this compensation in line with the median of the labour market annual report. This remuneration report is also available reference group. The current remuneration policy was on Fugro’s website. adopted by the AGM on 6 May 2014 and took effect retroactively as from 1 January 2014. As mentioned above, This report has been prepared by the remuneration the policy was amended in the AGM on 30 April 2015. Within committee of the Supervisory Board. The main function of the framework of the remuneration policy, compensation for this committee is to prepare the decision-making of the the Board of Management is determined by the Supervisory Supervisory Board regarding the remuneration policy for the Board on the advice of the remuneration committee. Board of Management and the application of this policy to the remuneration of the individual members of the Board of Labour market reference group Management. -

Integrated Reporting and Investor Clientele

Integrated Reporting and Investor Clientele The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Serafeim, George. "Integrated Reporting and Investor Clientele." Harvard Business School Working Paper, No. 14-069, February 2014. (Revised April 2014.) Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:12111355 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Open Access Policy Articles, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#OAP Integrated Reporting and Investor Clientele George Serafeim Working Paper 14-069 April 4, 2014 Copyright © 2014 by George Serafeim Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author. Integrated Reporting and Investor Clientele George Serafeim Harvard Business School Abstract In this paper, I examine the relation between Integrated Reporting (IR) and the composition of a firm’s investor base. I hypothesize and find that firms that practice IR have a more long-term oriented investor base with more dedicated and fewer transient investors. This result is more pronounced for firms with high growth opportunities, not controlled by a family, operating in ‘sin’ industries, and exhibiting more stable IR practice over time. I find that the results are robust to the inclusion of firm fixed effects, controls for the quantity of sustainability disclosure, and alternative ways of measuring IR. -

Implementing Integrated Reporting

Implementing Integrated Reporting PwC’s practical guide for A new business language PwC | Implementing Integrated Reporting | 1 Despite an increase in the volume and frequency of The imperative to build a long-term business model that information made available by companies, access to takes cognisance of the impacts, risks and opportunities in “more data for public equity investors has not necessarily “relation to the environmental, social and economic contexts translated into more comprehensive insight into within which an organisation operates, is increasingly companies. Integrated reporting addresses this problem becoming part of the licence to operate for companies the by encouraging companies to integrate both their world over. Investors also progressively recognise that they financial and ESG performance into one report that can no longer ignore these elements when performing includes only the most salient or material metrics. fundamental analysis, and evidence is mounting that Al Gore and David Blood companies who integrate broader sustainability A Manifesto for Sustainable Capitalisma considerations into their value proposition, clearly position themselves for better performance in the longer term. JSE (Johannesburg Stock Exchange) maintains a ‘report-or- explain basis’ when dealing with integrated reporting. JSE Johannesburg Stock Exchanged Financial capital is disproportionate in the way in which a Corporate reporting is of the utmost importance to company is valued. Social and environmental impacts investors. Long-term investors are already well known to “are not recognised to the extent they need to be in “look beyond the financial facts and figures only. investment and capital allocation decisions. Integrated Integrated reporting is a logical and necessary next step Reporting is also about giving credit where credit is due. -

Annual Report 2007 FUGRO NV

ANNUAL REPORT 2007 FUGRO N.V. FUGRO 2007 REPORT ANNUAL FUGRO N.V. Annual Report 2007 GEOTECHNIEK MILIEU ONDERZOEK MARINER Colophon Fugro N.V. Veurse Achterweg 10 2264 SG Leidschendam The Netherlands Telephone: +31 (0)70 3111422 Fax: +31 (0)70 3202703 Concept and realisation: C&F Report Amsterdam B.V. Photography: Fugro N.V., Picture Report, Amsterdam. Fugro has endeavored to fulfil all legal requirements related to copyright. Anyone who, despite this, is of the opinion that other copyright regulations could be applicable should contact Fugro. Text: Boogaard Communications Consultancy (BCC) v.o.f. This annual report is a translation of the official report published in the Dutch language. The annual report is also available on our website www.fugro.com. For complete information, see www.fugro.com Fugro N.V. Veurse Achterweg 10 P.O. Box 41 Cautionary Statement regarding Forward-Looking Statements 2260 AA Leidschendam This annual report may contain forward-looking statements. Forward-looking statements are statements that are not historical facts, including The Netherlands (but not limited to) statements expressing or implying Fugro N.V.’s beliefs, expectations, intentions, forecasts, estimates or predictions (and the Telephone: +31 (0)70 3111422 assumptions underlying them). Forward-looking statements necessarily involve risks and uncertainties. The actual future results and situations Fax: +31 (0)70 3202703 may therefore differ materially from those expressed or implied in any forward-looking statements. Such differences may be caused by various E-mail: [email protected] factors (including, but not limited to, developments in the oil and gas industry and related markets, currency risks and unexpected operational www.fugro.com setbacks). -

1994 Foundation of Nutreco

‘11 CONTENTS CONTENTS Overview Operations and and strategy 2 business performance 32 OVERVIEW AND STRATEGY OPERATIONAL DEVELOPMENTS Our track record and ambitions 2 Premix and Feed Specialties 34 Statement by the Chief Executive Officer 4 Fish Feed 36 Profile & financial highlights 6 Animal Nutrition Canada 38 Key figures 8 Compound Feed Europe 40 Report of the Executive Board 10 Meat and Other 42 Operating result 13 Strategic agenda 2012 14 Innovation 46 Strategy 17 Sustainability 56 Strategic objectives and highlights 24 Human Resources 60 Information about the Nutreco share 27 OPERATIONS GOVERNANCE OVERVIEW AND AND BUSINESS AND FINANCIAL STRATEGY PERFORMANCE COMPLIANCE STATEMENTS 1 Governance Financial and compliance 64 statements 91 Risk management 64 FINANCIAL STATEMENTS Management review and reporting 73 Corporate governance 74 Consolidated financial statements 92 Remuneration Report 79 Notes to the consolidated financial statements 98 Report of the Supervisory Board 85 Company’s financial statements 182 Notes to the company’s financial statements 183 Other information 185 Independent auditor’s report 186 Ten years of Nutreco 188 ADDENDUM Executive Board 190 Supervisory Board 191 Business Management & corporate staff 193 Participations of Nutreco N.V. 194 2 OUR TRACK RECORD AND AMBITIONS Our track record and ambitions AquaVision and Agri Vision Annual international conference organised by Nutreco since 1996, Sustainability bringing multiple stakeholders together • First Sustainability Report in 2000. at a professional, non-political forum to • Establishment of Innovation and discuss challenges and opportunities Sustainability Committee in in agriculture and aquaculture. About Supervisory Board in 2009 and 5,000 delegates have attended. performance targets on sustainability for top management since 2010. -

Annual Report Capturing Growth, Delivering Value How to Read This Report

Annual Report Capturing growth, delivering value How to read this report Management summary Readers looking for the highlights of 2020 are advised to read chapter 1 until 6, and the first pages of chapter 7 until 10. Report of the Board of Management The report of the Board of Management consists of the following sections: • Introduction • Business Report • Governance, chapter 16 until 19 Forward-looking statements This Annual Report contains forward-looking statements. Readers should not put undue reliance on these statements. These provide a snapshot on the publication date of this report. In addition, future actual events, results and outcomes likely differ from these statements made. Chapter ‘Non-financial statements’, section ‘Safeguarding report quality’ provides more information on forward-looking statements. Contents 8 Message from Herna Verhagen 24 How we create value 30 Our strategy 72 Financial value Introduction Governance 1 At a glance 4 12 Board of Management 92 2 Message from Herna Verhagen 8 13 Supervisory Board 94 3 Our operating context 12 14 Report of the Supervisory Board 96 4 Impact of Covid-19 20 15 Remuneration report 102 16 Corporate governance 110 17 Our tax policy and principles 120 Business Report 18 PostNL on the capital markets 122 5 How we create value 24 19 Statements of the Board of Management 126 6 Our strategy 30 7 Customer value 40 8 Social value 54 Performance statements 9 Environmental value 64 20 Financial statements 129 10 Financial value 72 21 Non-financial statements 213 11 Risk and opportunity -

Abn Amro Bank Nv

7 MAY 2020 ABN AMRO ABN AMRO BANK N.V. REGISTRATION DOCUMENT constituting part of any base prospectus of the Issuer consisting of separate documents within the meaning of Article 8(6) of Regulation (EU) 2017/1129 (the "Prospectus Regulation") 250249-4-270-v18.0 55-40738204 CONTENTS Page 1. RISK FACTORS ...................................................................................................................................... 1 2. INTRODUCTION .................................................................................................................................. 26 3. DOCUMENTS INCORPORATED BY REFERENCE ......................................................................... 28 4. SELECTED DEFINITIONS AND ABBREVIATIONS ........................................................................ 30 5. PRESENTATION OF FINANCIAL INFORMATION ......................................................................... 35 6. THE ISSUER ......................................................................................................................................... 36 1.1 History and recent developments ............................................................................................. 36 1.2 Business description ................................................................................................................ 37 1.3 Regulation ............................................................................................................................... 40 1.4 Legal and arbitration proceedings .......................................................................................... -

Dorien Fransens, Secretary General, Europeanissuers

5+ aitbl - ivzw RucBelliard 4 6 Tel| +32(012 289 25 70 info@europeafi issuers,eu 8-1040BRUSSEIs Fax:+32 (0)2 512 l5 60 wM/w.€uropeanitsuers,eu U.S.Securftles and Exchange Commission Tothe att. of Ms.Nancv M. Morris Secretary1.00 F Street, NE washington,D.c. 20549-9303 U5A r.iFcH!l/HD MAY13 2008 Brussels,8 May 2008 Re: Commentson ProposedAmendments to RulesRelating to ForeignPrivate lssuer Reportingunder the SecuritiesExchange Act of 1934 FileNo. 57-05-08 DearMs. Morris, We are submittingthis letter in responseto the requestof the Securitiesand Exchange Commission(the "Commission") for commentson the Commission'sproposal to amendthe rulesand forms that governreporting by foreignprivate issuers under the Securities ExchangeAct of 1934,as amended(the "ExchangeAct"). The proposalis discussedin ReleaseNo. 33-8900; 34-57409i International series Release No. 1308; File No. 57-05-08 (the "Release"), Europeanlssuers'has for severalyears supported the effortsof the Commissionto review the applicationof the U.S.securities laws and regulations to non-U.S.issuers. These efforts haveresulted in substantialimprovements to the U.S.regulatory regime in the pastfew years,including the modernizationof the rulesgoverning deregistration and the elimination of U.S.GAAP reconciliation for companiesthat publishIFRS financialstatements. Unfortunately,we cannotsupport the Commission'sproposal to requirelarge non-U.S. issuersto file their annualreports on Form20-F within 90 daysof the end of their fiscal years. We regardthis proposalas a step in the oppositedirection compared to the I Europeanlssuersis a pan Europeanorganisation that representsthe vast majority of publicly quoted companiesin Europe. Europeanlssuerswas formed when EALIq the EuropeanAssociation of Listed Companies,and UNIQUE, the Unionof lssuersQuoted in Europe,combined their organisations in early 2008. -

CFD Type IB Symbol Product Description Symbol Currency Share

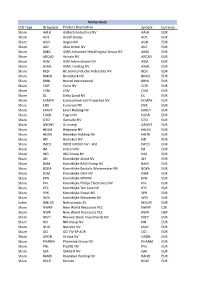

Netherlands CFD Type IB Symbol Product Description Symbol Currency Share AALB Aalberts Industries NV AALB EUR Share AO1 Accell Group AO1 EUR Share AGN Aegon NV AGN EUR Share AKZ Akzo Nobel NV AKZ EUR Share AMG AMG Advanced Metallurgical Group NV AMG EUR Share ARCAD Arcadis NV ARCAD EUR Share ASM ASM International NV ASM EUR Share ASML ASML Holding NV ASML EUR Share BESI BE Semiconductor Industries NV BESI EUR Share BINCK BinckBank NV BINCK EUR Share BRNL Brunel International BRNL EUR Share COR Corio NV COR EUR Share CSM CSM CSM EUR Share DL Delta Lloyd NV DL EUR Share ECMPA Eurocommercial Properties NV ECMPA EUR Share ENX Euronext NV ENX EUR Share EXACT Exact Holding NV EXACT EUR Share FUGR Fugro NV FUGR EUR Share GTO Gemalto NV GTO EUR Share GRONT Grontmij GRONT EUR Share HEIJM Heijmans NV HEIJM EUR Share HEHN Heineken Holding NV HEHN EUR Share HEI Heineken NV HEI EUR Share IMCD IMCD GROUP NV - W/I IMCD EUR Share IM Imtech NV IM EUR Share ING ING Groep NV ING EUR Share AH Koninklijke Ahold NV AH EUR Share BAM Koninklijke BAM Groep NV BAM EUR Share BOKA Koninklijke Boskalis Westminster NV BOKA EUR Share DSM Koninklijke DSM NV DSM EUR Share KPN Koninklijke KPN NV KPN EUR Share PHI Koninklijke Philips Electronics NV PHI EUR Share KTC Koninklijke Ten Cate NV KTC EUR Share VPK Koninklijke Vopak NV VPK EUR Share WES Koninklijke Wessanen NV WES EUR Index IBNL25 Netherlands 25 IBNL25 EUR Share NWRP New World Resources PLC NWRP CZK Share NWR New World Resources PLC NWR GBP Share NISTI Nieuwe Steen Investments NV NISTI EUR Share NN NN Group NV