Current Situation in Corporate Accounting Systems

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Basic Policy Regarding Selection of Accounting Standards”

Analysis of Disclosure in “Basic Policy Regarding Selection of Accounting Standards” Tokyo Stock Exchange, Inc. 1 I. Background Jun. 24, 2014 Japan Revitalization Strategy (Revised in 2014) 4) Promoting of an increase in the number of companies voluntarily adopting IFRS Tokyo Stock Exchange will encourage listed companies to explain to investors their basic views on the selection of accounting standards (for example, whether they are considering adopting IFRS). Nov. 11, 2014 Revision of Guidelines for Financial Results Request description on “Basic Policy Regarding Selection of Accounting Standards” in Financial Results <Guidelines for Financial Results> ・Please describe basic policy regarding selection of accounting standards. ・For example, whether you are considering the adoption of IFRS. (stage of consideration, scheduled adoption date) Adoption from Financial Results for FY-ended Mar. 31, 2015 (early adoption possible) Jun. 30, 2015 Japan Revitalization Strategy (Revised in 2015) 4) Further promotion of an increase in the number of companies voluntarily adopting IFRS Listed companies disclose their progress in considering the adoption of IFRS in “Basic Policy Regarding Selection of Accounting Standards” of the financial results. The government will analyze this together with Tokyo Stock Exchange and disseminate the state of IFRS adoption to contribute to efforts among listed companies to consider transitioning to IFRS. 2 II. Scope of Analysis Coverage:3,194 companies TSE-listed companies that provided description in Basic Policy Regarding Selection of Accounting Standards (hereinafter ”Basic Policy”) of financial results:3,193 companies FY ended March 2015:2,308 companies FY ended April 2015 ~ FY ended December 2015:885 companies Other companies that have adopted IFRS (FY ended January 2016 ~ FY ended February 2016):1 company 3 Ⅲ. -

Mizuho BK Custody and Proxy Board Lot Size List OCT 27, 2020 21LADY

Mizuho BK Custody and Proxy Board Lot Size List OCT 27, 2020 Board Lot Stock Name (in Alphabetical Order) ISIN Code QUICK Code Size 21LADY CO.,LTD. 100 JP3560550000 3346 3-D MATRIX,LTD. 100 JP3410730000 7777 4CS HOLDINGS CO.,LTD. 100 JP3163300001 3726 A DOT CO.,LTD 100 JP3160590000 7063 A-ONE SEIMITSU INC. 100 JP3160660001 6156 A.D.WORKS GROUP CO.,LTD. 100 JP3160560003 2982 A&A MATERIAL CORPORATION 100 JP3119800005 5391 A&D COMPANY,LIMITED 100 JP3160130005 7745 A&T CORPORATION 100 JP3160680009 6722 ABALANCE CORPORATION 100 JP3969530009 3856 ABC-MART,INC. 100 JP3152740001 2670 ABHOTEL CO.,LTD. 100 JP3160610006 6565 ABIST CO.,LTD. 100 JP3122480001 6087 ACCESS CO.,LTD. 100 JP3108060009 4813 ACCESS GROUP HOLDINGS CO.,LTD. 100 JP3108190004 7042 ACCRETE INC. 100 JP3108180005 4395 ACHILLES CORPORATION 100 JP3108000005 5142 ACMOS INC. 100 JP3108100003 6888 ACOM CO.,LTD. 100 JP3108600002 8572 ACRODEA,INC. 100 JP3108120001 3823 ACTCALL INC. 100 JP3108140009 6064 ACTIVIA PROPERTIES INC. 1 JP3047490002 3279 AD-SOL NISSIN CORPORATION 100 JP3122030004 3837 ADASTRIA CO.,LTD. 100 JP3856000009 2685 ADEKA CORPORATION 100 JP3114800000 4401 ADISH CO.,LTD. 100 JP3121500007 7093 ADJUVANT COSME JAPAN CO.,LTD. 100 JP3119620007 4929 ADTEC PLASMA TECHNOLOGY CO.,LTD. 100 JP3122010006 6668 ADVAN CO.,LTD. 100 JP3121950004 7463 ADVANCE CREATE CO.,LTD. 100 JP3122100005 8798 ADVANCE RESIDENCE INVESTMENT CORPORATION 1 JP3047160001 3269 ADVANCED MEDIA,INC. 100 JP3122150000 3773 ADVANEX INC. 100 JP3213400009 5998 ADVANTAGE RISK MANAGEMENT CO.,LTD. 100 JP3122410008 8769 ADVANTEST CORPORATION 100 JP3122400009 6857 ADVENTURE,INC. 100 JP3122380003 6030 ADWAYS INC. 100 JP3121970002 2489 AEON CO.,LTD. 100 JP3388200002 8267 AEON DELIGHT CO.,LTD. -

Transparency Report 2017 1

23.974Transparency mm Report 2017 2017 9 ______年 月 www.kpmg.com/jp/azsa © 2017 KPMG AZSA LLC, a limited liability audit corporation incorporated under the Japanese Certified Public Accountants Law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Transparency Report 2017 1 1. Message from the Local Senior Partner As a member of the KPMG network,KPMG AZSA LLC shares a common Purpose-to Inspire Confidence,Empower Change–with member firms around the globe.Based on this Purpose,we aim to establish the reliability of information through auditing and accounting services and support the change of companies and society towards sustainable growth. KPMG AZSA's system of quality control is in line with the KPMG Audit Quality Framework applicable to KPMG network firms globally.This Transparency Report 2017 explains our quality control system in performing audit,based on the framework,and the systems of quality control for each of the key drivers and KPMG network arrangements.We also published AZSA Quality 2017 in September 2017 to address mainly our recent efforts regarding quality control that serves as the basis for KPMG AZSA’s Audit Quality,governance structure and policies of human resource development. 2. Network arrangements As a member firm of KPMG International,KPMG AZSA LLC provides clients with a consistent set of professional services globally through a network in 155 countries.KPMG network arrangements,including legal structure,responsibilities and obligations of member firm are described more detail in the following sections of this report. -

Crystal Technology: Smart Innovation

Crystal Technology: Smart Innovation ANNUAL REPORT 2013 Report for the Fiscal Year Ended March 31, 2013 A LEADER IN THE FIELD OF QUARTZ CRYSTAL ELECTRONIC COMPONENTS NIHON DEMPA KOGYO PROFILE Nihon Dempa Kogyo Co., Ltd. (NDK), was founded in 1948 as a company spe- cializing in the manufacture of quartz crystal devices, based on its business philosophy of “contributing to the prosperity of society and world peace through our service to customers.” The NDK Group supplies crystal devices that serve as indispensable “oscil- lation sources with superior stability” in a wide range of products, including telecommunications devices, such as smartphones, audiovisual/office-automa- tion equipment, and car electronics products. Through these business activi- ties, the NDK Group has developed top-class technological capabilities and has earned one of the top global market shares in its industry. To maintain the high levels of trust of its stakeholders, the NDK Group man- ages its businesses soundly and with a high level of transparency. As evidence of this, the Group has become the first company in Japan to adopt the International Financial Reporting Standards (IFRS) in the preparation of its financial statements. As a company striving for excellence in manufacturing based on the slogan of “quality first,” the NDK Group is also taking active initia- tives to promote the growth of its business activities, by assisting its customers in the development of their businesses and to contribute to the building of afflu- ent societies. The NDK Group’s Global Network The NDK Group has 19 sales bases and 8 manufacturing plants around the world. -

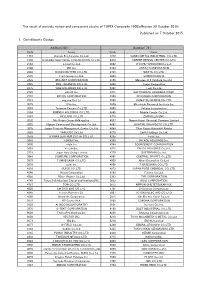

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

Transparency Report 2019

Transparency Report 2019 2018 9 ______年 月 www.kpmg.com jp / / © 2019 KPMG AZSA LLC, a limited liability audit corporation incorporated under the Japanese Certified Public Accountants Law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Transparency Report 2019 1 1. Message from the local Senior Partner As a member of the KPMG network, KPMG AZSA LLC shares a common purpose - to Inspire Confidence, Empower Change – with member firms around the globe. Based on this purpose, we aim to establish the reliability of information through auditing and accounting services and support the change of companies and society towards sustainable growth. AZSA Quality 2019 introduces efforts at KPMG AZSA LLC to improve audit quality, the foundation of which is KPMG’s globally consistent audit quality. In this transparency report, we will additionally introduce KPMG’s system for ensuring audit quality. 2. Who we are 2.1 Our business 2.2 Our strategy KPMG AZSA LLC, a member firm of KPMG International, comprises Our firm’s mission is to ensure the reliability of information by approximately 6,000 people in major cities in Japan, providing audit, providing quality audit and accounting services as well as to attestation, and advisory services such as accounting advisory contribute to the realization of a fair society and healthy services, financial advisory services, IT advisory service and other development of our economy by empowering change. In order to advisory services for initial public offerings and the public sector. execute our firm’s mission, we have following vision: We also offer highly specialized professional services that address To be ‘The Clear Choice’ for our clients, people and society. -

JASIS 2019 Exhibitors

JASIS 2019 Exhibitors Elemental Scientic, Inc. A Elementar Japan K.K. a priori Inc. ELGA LabWater A&D Company, Limited ELIONIX INC. ACTAC.CO.,LTD Emerging Technologies Corporation. Acumentech Co., Ltd. entex inc. AD Science Inc. Eppendorf Co., Ltd. Advanced Energy Japan K.K. ERECTA International Corporation Advantec Toyo Kaisha, Ltd. ESPEC CORP. ADVANTEST CORPORATION ESPEC MIC CORP. Agilent Technologies Japan,Ltd. ETRI AINEX CO., LTD. Excimer,inc AIRIX Corp. Airtech Corporation AIVS Corporation F Alpha M.O.S. Japan K.K. Filgen, Inc. AMETEK Co, Ltd FLON CHEMICAL INC. AMR, Inc. FLON INDUSTRY CO., LTD. analytica-Messe Muenchen ForDx, Inc. Analytik Jena Japan Co., Ltd. Forum for Innovative Regenerative Medicine(FIRM) ANRITSU METER CO., LTD. FUJIKIN Incorporated Anton Paar Japan K.K. Fujitsu Limited Aomori Prefecture Quantum Science Center FUKUSHIMA INDUSTRIES CORP. APRO Science Institute, Inc. FUSO Co., Ltd. ARAM CORPORATION FUTA-Q,Ltd. AS ONE CORPORATION ASAHI KOHSAN Co.,Ltd Asahi Lab Commerce, Inc. G ASAHI LIFE SCIENCE CO.,LTD GASTEC CORPORATION ASAHI RUBBER INC. GC INSTRUMENTS ASAHI TECHNEION CO., LTD. GE Healthcare Japan Corporation ASCH JAPAN CO.,LTD GERSTEL K.K. ASI-AURORA GL Sciences Inc. ASICON Tokyo Ltd. Glass Expansion Pty. Ltd. Association for structure characterization Global Facility Center,HOKKAIDO UNIVERSITY ASTECH CORPORATION GTR TEC CORPORATION ATAGO CO., LTD. GVS Japan K.K. B H BAS Inc. hagataya.co.ltd BD Consulting L.L.C. Hakuto Co., Ltd. BeatSensing co.,ltd. HAMAMATSU PHOTONICS K.K. Beckman Coulter K.K. Hamilton Company Japan K.K. BEIJING LINGGONG TECHNOLOGY CO.,LTD Hanaichi UltraStructure Research Institute BETHL Co.,Ltd. -

Basic Policy Regarding Selection of Accounting Standards”

Analysis of Disclosure in “Basic Policy Regarding Selection of Accounting Standards” Tokyo Stock Exchange, Inc. 1 I. Background Jun. 24, 2014 Japan Revitalization Strategy (Revised in 2014) 4) Promoting of an increase in the number of companies voluntarily adopting IFRS Tokyo Stock Exchange will encourage listed companies to explain to investors their basic views on the selection of accounting standards (for example, whether they are considering adopting IFRS). Nov. 11, 2014 Revision of Guidelines for Financial Results Request description on “Basic Policy Regarding Selection of Accounting Standards” in Financial Results <Guidelines for Financial Results> ・Please describe basic policy regarding selection of accounting standards. ・For example, whether you are considering the adoption of IFRS. (stage of consideration, scheduled adoption date) Adoption from Financial Results for FY-ended Mar. 31, 2015 (early adoption possible) Jun. 30, 2015 Japan Revitalization Strategy (Revised in 2015) 4) Further promotion of an increase in the number of companies voluntarily adopting IFRS Listed companies disclose their progress in considering the adoption of IFRS in “Basic Policy Regarding Selection of Accounting Standards” of the financial results. The government will analyze this together with Tokyo Stock Exchange and disseminate the state of IFRS adoption to contribute to efforts among listed companies to consider transitioning to IFRS. 2 II. Scope of Analysis Coverage:3,507 companies Basic Policy Regarding Selection of Accounting Standards (hereinafter ”Basic Policy”) of financial results that have been described by TSE-listed companies FY ended April 2015 ~ FY ended December 2015 : 895 companies FY ended January 2016 ~ FY ended February 2016 : 246 companies FY ended March 2016 (include irregular accounting period) : 2,366 companies 3 Ⅲ. -

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only. -

NIKKEI JAPAN 1000 Constituents (As of March 25, 2005)

NIKKEI JAPAN 1000 Constituents (as of March 25, 2005) Tokyo Stock Exchange 1st 2580 COCA-COLA CENTRAL JAPAN 1332 NIPPON SUISAN 2590 DYDO DRINCO 1334 MARUHA GROUP 2591 CALPIS 1377 SAKATA SEED 2593 ITO EN 1379 HOKUTO 2594 KEY COFFEE 1601 TEIKOKU OIL 2595 KIRIN BEVERAGE 1662 JAPAN PETROLEUM EXPLORATION 2602 NISSHIN OILLIO GROUP 1720 TOKYU CONSTRUCTION 2607 FUJI OIL 1721 COMSYS HOLDINGS 2613 J-OIL MILLS 1722 MISAWA HOMES HOLDINGS 2651 LAWSON 1801 TAISEI 2664 CAWACHI 1802 OBAYASHI 2670 ABC-MART 1803 SHIMIZU 2678 ASKUL 1808 HASEKO 2681 GEO 1812 KAJIMA 2685 POINT 1820 NISHIMATSU CONSTRUCTION 2692 ITOCHU-SHOKUHIN 1821 SUMITOMO MITSUI CONSTRUCTION 2730 EDION 1824 MAEDA 2731 NIWS 1833 OKUMURA 2768 SOJITZ HOLDINGS 1860 TODA 2779 MITSUKOSHI 1878 DAITO TRUST CONSTRUCTION 2784 ALFRESA HOLDINGS 1881 NIPPO 2801 KIKKOMAN 1883 MAEDA ROAD CONSTRUCTION 2802 AJINOMOTO 1885 TOA 2809 Q.P. 1893 PENTA-OCEAN CONSTRUCTION 2810 HOUSE FOODS 1924 PANAHOME 2811 KAGOME 1925 DAIWA HOUSE INDUSTRY 2815 ARIAKE JAPAN 1928 SEKISUI HOUSE 2871 NICHIREI 1941 CHUDENKO 2873 KATOKICHI 1942 KANDENKO 2874 YOKOHAMA REITO 1946 TOENEC 2875 TOYO SUISAN 1951 KYOWA EXEO 2897 NISSIN FOOD PRODUCTS 1959 KYUDENKO 2908 FUJICCO 1961 SANKI ENGINEERING 2914 JAPAN TOBACCO 1963 JGC 3001 KATAKURA INDUSTRIES 1969 TAKASAGO THERMAL ENGINEERING 3002 GUNZE 1970 HITACHI PLANT ENGINEERING 3101 TOYOBO 1973 NEC SYS. INTEGRA. & CONST. 3103 UNITIKA 1979 TAIKISHA 3105 NISSHINBO INDUSTRIES 1982 HIBIYA ENGINEERING 3106 KURABO INDUSTRIES 2001 NIPPON FLOUR MILLS 3110 NITTO BOSEKI 2002 NISSHIN SEIFUN GROUP 3116 TOYOTA -

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

CEATEC JAPAN 2006 Exhibition Report

CONTENTS CEATEC JAPAN 2006 JAPAN CEATEC 1. SHOW INFORMATION 01 2. CHAIRMAN'S COMMENTS 02 3. OPENING EVENTS 03 4. EXHIBITION CONFIGURATION 04 5. EXHIBITION SITE 05 6. EXHIBITION TRENDS 06 7. SPONSORS PROJECTS AND SPECIAL EXHIBITS 13 8. CONFERENCE 15 9. EXHIBITORS 16 10. NUMBERS AND ANALYSIS OF VISITORS 19 11. ADVERTISING AND PUBLICITY 22 12. CEATEC JAPAN OFFICIAL WEB SITE 24 00 1. SHOW INFORMATION CEATEC JAPAN 2006 JAPAN CEATEC NAME CEATEC JAPAN 2006 (Combined Exhibition of Advanced TEChnologies-Providing Image, Information and Communications) OBJECTIVES 1.To allow visitors to experience the newest technologies, products, systems and software for the digital network age, and the convergence of communications, information and imaging technologies 2.To function as a highly specific exhibition capturing the interest and responding to the needs of users by presenting the industries' latest achievements and trends 3.As Asia's largest interactive exhibition of information on the communications, information and imaging fields, to present the achievements, trends and vitality of these industries to the world 4.To gather industry organizations to present clear social messages, thereby supporting industrial development and contributing to lifestyles, economies and society in the digital network age DURATION Tuesday, October 3-Saturday, October 7, 2006 (5 days), from 10:00 a.m.-5:00 p.m. Premiere Time: Tuesday, October 3, 10:00 a.m.-12:00 p.m. LOCATION Makuhari Messe 2-1 Nakase, Mihama-ku, Chiba, Japan ADMISSION Registration required Visitors Pre-registered on the Web: Free entry Visitors registering at the Gate: General: 1,000 (Students: 500) Note: Groups of 20 or more students and children under 12 years of age were admitted free of charge.