Chapter 3 Market Demand and Economic Opportunities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bankruptcy Forms

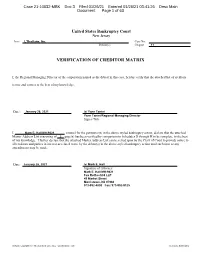

Case 21-10632-MBK Doc 3 Filed 01/26/21 Entered 01/26/21 03:41:26 Desc Main Document Page 1 of 63 United States Bankruptcy Court New Jersey In re L'Occitane, Inc. Case No. Debtor(s) Chapter 11 VERIFICATION OF CREDITOR MATRIX I, the Regional Managing Director of the corporation named as the debtor in this case, hereby verify that the attached list of creditors is true and correct to the best of my knowledge. Date: January 26, 2021 /s/ Yann Tanini Yann Tanini/Regional Managing Director Signer/Title I, Mark E. Hall MH-9621 , counsel for the petitioner(s) in the above-styled bankruptcy action, declare that the attached Master Address List consisting of 2 page(s) has been verified by comparison to Schedules D through H to be complete, to the best of my knowledge. I further declare that the attached Master Address List can be relied upon by the Clerk of Court to provide notice to all creditors and parties in interest as related to me by the debtor(s) in the above-styled bankruptcy action until such time as any amendments may be made. Date: January 26, 2021 /s/ Mark E. Hall Signature of Attorney Mark E. Hall MH-9621 Fox Rothschild LLP 49 Market Street Morristown, NJ 07960 973-992-4800 Fax: 973-992-9125 Software Copyright (c) 1996-2020 Best Case, LLC - www.bestcase.com Best Case Bankruptcy Case 21-10632-MBK Doc 3 Filed 01/26/21 Entered 01/26/21 03:41:26 Desc Main Document Page 2 of 63 Creditor Matrix Name Attention Address 1 Address 2 Address 3 City State Zip Country #0257-004865 Broughton Street Partn PO Box 742939 Atlanta GA 30374-2939 #339475 GGP Ala Moana L.L. -

2019 Property Portfolio Simon Malls®

The Shops at Clearfork Denver Premium Outlets® The Colonnade Outlets at Sawgrass Mills® 2019 PROPERTY PORTFOLIO SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME 2 THE SIMON EXPERIENCE WHERE BRANDS & COMMUNITIES COME TOGETHER SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME 2 ABOUT SIMON Simon® is a global leader in retail real estate ownership, management, and development and an S&P 100 company (Simon Property Group, NYSE:SPG). Our industry-leading retail properties and investments across North America, Europe, and Asia provide shopping experiences for millions of consumers every day and generate billions in annual sales. For more information, visit simon.com. · Information as of 12/16/2019 3 SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME More than real estate, we are a company of experiences. For our guests, we provide distinctive shopping, dining, and entertainment. For our retailers, we offer the unique opportunity to thrive in the best retail real estate in the best markets. From new projects and redevelopments to acquisitions and mergers, we are continuously evaluating our portfolio to enhance the Simon experience—places where people choose to shop and retailers want to be. 4 LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME WE DELIVER: SCALE A global leader in the ownership of premier shopping, dining, entertainment, and mixed-use destinations, including Simon Malls®, Simon Premium Outlets®, and The Mills® QUALITY Iconic, irreplaceable properties in great locations INVESTMENT Active portfolio management increases productivity and returns GROWTH Core business and strategic acquisitions drive performance EXPERIENCE Decades of expertise in development, ownership, and management That’s the advantage of leasing with Simon. -

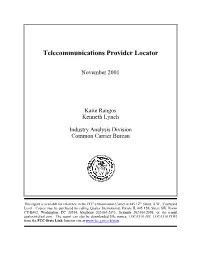

Telecommunications Provider Locator

Telecommunications Provider Locator November 2001 Katie Rangos Kenneth Lynch Industry Analysis Division Common Carrier Bureau This report is available for reference in the FCC’s Information Center at 445 12th Street, S.W., Courtyard Level. Copies may be purchased by calling Qualex International, Portals II, 445 12th Street SW, Room CY-B402, Washington, DC 20554, telephone 202-863-2893, facsimile 202-863-2898, or via e-mail [email protected]. The report can also be downloaded [file names: LOCAT01.ZIP, LOCAT01.PDF] from the FCC-State Link Internet site at www.fcc.gov/ccb/stats. Telecommunications Provider Locator This report lists the contact information and the types of services sold by 5,679 telecommunications providers operating as of December 31, 2000. All information in this report is drawn from providers’ April 1, 2001 filing of the Telecommunications Reporting Worksheet (FCC Form 499-A). This report can be used by customers to identify and locate telecommunications providers, by telecommunications providers to identify and locate others in the industry, and by equipment vendors to identify potential customers. Virtually all providers of telecommunications must file FCC Form 499-A each year.1 These forms are not filed directly with the FCC but rather with the Universal Service Administrative Company (USAC), which serves as the data collection agent. The worksheets were due April 1, 2001, but some providers filed late or updated their filing after that date. By October 1, 2001, the database contained contact information and revenue data from 5,679 filers. Information from filings received after October 1 and from filings that were incomplete has been excluded from the tables. -

Transportation Air Quality Conformity Analysis for the Amended Plan Bay

The Final Transportation-Air Quality Conformity Analysis for the Amended Plan Bay Area 2040 and the 2021 Transportation Improvement Program February 2021 Bay Area Metro Center 375 Beale Street San Francisco, CA 94105 (415) 778-6700 phone [email protected] e-mail www.mtc.ca.gov web Project Staff Matt Maloney Acting Director, Planning Therese Trivedi Assistant Director Harold Brazil Senior Planner, Project Manager 2021 Transportation Improvement Program Conformity Analysis Page | i Table of Contents I. Summary of Conformity Analysis ...................................................................................................... 1 II. Transportation Control Measures .................................................................................................... 7 History of Transportation Control Measures .............................................................................. 7 Status of Transportation Control Measures................................................................................ 9 III. Response to Public Comments ...................................................................................................... 12 IV. Conformity Findings ...................................................................................................................... 13 Appendix A. List of Projects in the 2021 Transportation Improvement Program Appendix B. List of Projects in Amended Plan Bay Area 2040 2021 Transportation Improvement Program Conformity Analysis Page | ii I. Summary of Conformity Analysis The -

Halo 3 ODST Midnight Openings

Store # Address City State Phone 318 800 East Dimond Boulevard #3-118 Anchorage AK (907) 522-1254 6139 1118 N Muldoon Rd Suite 165 Anchorage AK (907) 332-0000 1833 32 College Rd. Fairbanks AK (907) 474-4550 3219 419 Merhar Ave., Suite A Fairbanks AK (907) 456-5700 6140 1867 E George Parks Way Vasilla AK (907) 357-5775 5601 300 Colonial Promenade Pkwy, Ste 3100 Alabaster AL (205) 621-3131 3915 229 French Farm Blvd Unit M Athens AL (256) 233-3167 2989 977 Gilbert Ferry Rd. SE Attalia AL (256) 538-2397 3917 4933 Promenade Parkway Ste 147 Bessemer AL (205) 425-4985 1595 5964 Chalkville Mountain Rd Birmingham AL (205) 661-6010 3693 1632 Montclair Blvd Shops A-8 Birmingham AL (205) 957-2600 5059 4507 Riverview Pkwy, Ste 107 Birmingham AL (205) 981-2121 2771 2200 Hwy. 431, Suite F Boaz AL (256) 840-0491 2792 1850 Cherokee Ave. SW, Suite A Cullman AL (256) 739-0432 4850 6880 Us Hwy 90, Suite 6 Daphne AL (251) 625-2724 5359 1605 Beltline Rd Sw, Ste D4 Decatur AL (256) 351-9771 5723 2812 Spring Ave SW Decatur AL (256) 552-7525 3858 4521 Montgomery Hwy Suite 2 Dothan AL (334) 671-8223 3867 3255 S. Oates St Dothan AL (334) 792-6534 3506 600 Boll Weevil Circle Enterprise AL (334) 347-0018 324 301 Cox Creek Parkway #1026 Florence AL (256) 764-8141 5512 366 Cox Creek Pkwy, Unit D Florence AL (256) 740-0655 3032 2108 S. McKenzie St., Unit 5 Foley AL (251) 943-8925 6824 Building 9214 Hutto Plaza 5th Avenue Fort Rucker AL (334) 598-1467 5331 300 E Meighan Blvd Gadsden AL (256) 546-1818 3896 3800 Gulf Shores Parkway Hwy 59 and CR 4 Gulf Shores AL (251) 967-3896 3030 1199 Hwy. -

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 Gamestop Dimond Center 80

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 GameStop Dimond Center 800 East Dimond Boulevard #3-118 Anchorage AK 99515 665 1703 (907) 272-7341 GameStop Anchorage 5th Ave. Mall 320 W. 5th Ave, Suite 172 Anchorage AK 99501 665 6139 (907) 332-0000 GameStop Tikahtnu Commons 11118 N. Muldoon Rd. ste. 165 Anchorage AK 99504 665 6803 (907) 868-1688 GameStop Elmendorf AFB 5800 Westover Dr. Elmendorf AK 99506 75 1833 (907) 474-4550 GameStop Bentley Mall 32 College Rd. Fairbanks AK 99701 665 3219 (907) 456-5700 GameStop & Movies, Too Fairbanks Center 419 Merhar Avenue Suite A Fairbanks AK 99701 665 6140 (907) 357-5775 GameStop Cottonwood Creek Place 1867 E. George Parks Hwy Wasilla AK 99654 665 5601 (205) 621-3131 GameStop Colonial Promenade Alabaster 300 Colonial Prom Pkwy, #3100 Alabaster AL 35007 701 3915 (256) 233-3167 GameStop French Farm Pavillions 229 French Farm Blvd. Unit M Athens AL 35611 705 2989 (256) 538-2397 GameStop Attalia Plaza 977 Gilbert Ferry Rd. SE Attalla AL 35954 705 4115 (334) 887-0333 GameStop Colonial University Village 1627-28a Opelika Rd Auburn AL 36830 707 3917 (205) 425-4985 GameStop Colonial Promenade Tannehill 4933 Promenade Parkway, Suite 147 Bessemer AL 35022 701 1595 (205) 661-6010 GameStop Trussville S/C 5964 Chalkville Mountain Rd Birmingham AL 35235 700 3431 (205) 836-4717 GameStop Roebuck Center 9256 Parkway East, Suite C Birmingham AL 35206 700 3534 (205) 788-4035 GameStop & Movies, Too Five Pointes West S/C 2239 Bessemer Rd., Suite 14 Birmingham AL 35208 700 3693 (205) 957-2600 GameStop The Shops at Eastwood 1632 Montclair Blvd. -

YPN Member List – As of 2/14/2018

Carissa Abazia Juan Alvarez Pinnacle Capital Mortgage - Jake Wade Viavi Solutions 70 Stony Point Road, Suite C 2789 Northpoint Parkway Santa Rosa, CA 95401 Santa Rosa, CA 95407 (707) 721-5655 (707) 545-6440 http://www.jakewadeloans.com www.viavisolutions.com Rachel Adams Nathan Andreassen George Petersen Insurance Agency American River Bank 175 W. College Avenue 90 South E Street, Ste #110 Santa Rosa, CA 95401 Santa Rosa, CA 95404 (707) 525-4150 (707) 528-6300 www.gpins.com www.americanriverbank.com Jessica Adams Jose Anyay Vintners Inn New York Life Insurance 4350 Barnes Road 740 Fourth Street Santa Rosa, CA 95403 Santa Rosa, CA 95404 (707) 575-7350 (707) 542-3462 www.vintnersinn.com Aura Aguilar Nicole Arnone Redwood Hill Farm & Creamery/Green Valley Organic Cipolla Financial and Insurance Services 2064 Gravenstein Hwy No., Bldg. 1, Suite 50 Santa Rosa Avenue, Suite 110 Sebastopol, CA 95472 Santa Rosa, CA 95404 (707) 823-8250 (707) 569-7134 www.cipollafis.com Able Aguilar Kelly Baker Signarama Sutter Health 915 Piner Road, Suite C 30 Mark West Springs Road Santa Rosa, CA 95403 Santa Rosa, CA 95403 (707) 523-0606 (707) 576-4000 signarama.com/ca-santa-rosa www.suttersantarosa.org Mandy R Alvarado Danielle Baker W Real Estate Sonoma Clean Power 500 Bicentennial Way Ste 310 50 Santa Rosa Avenue, 5th Floor Santa Rosa, CA 95403 Santa Rosa, CA 95404 (707) 591-0570 (707) 978-3468 www.wrealestate.net http://www.sonomacleanpower.org YPN Member List – as of 2/14/2018 Dora Barrera Katie Behrhorst Sonoma Clean Power The Press Democrat 50 Santa Rosa -

State Store Hours State Store Hours Al Brookwood

ALL HOURS APPLY TO LOCAL TIME ZONES STATE STORE HOURS STATE STORE HOURS AL BROOKWOOD VILLAGE 5-9pm MO NORTHPARK (MO) 5-9pm AL RIVERCHASE GALLERIA 5-9pm MO THE SHOPPES AT STADIUM (MO) 5-9pm AZ SCOTTSDALE FASHION SQUARE 5-9pm MT BOZEMAN GALLATIN VALLEY (MT) 5-9pm AZ BILTMORE FASHION PARK 5-9pm MT HELENA NORTHSIDE CENTER (MT) 5-9pm AZ ARROWHEAD TOWNE CENTER 5-9pm NC CRABTREE VALLEY 5-9pm AZ CHANDLER FASHION CENTER 5-9pm NC STREETS AT SOUTHPOINT 5-9pm AZ PARADISE VALLEY (AZ) 5-9pm NC CROSS CREEK (NC) 5-9pm AZ TUCSON MALL 5-9pm NC FRIENDLY CENTER 5-9pm AZ TUCSON PARK PLACE 5-9pm NC NORTHLAKE (NC) 5-9pm AZ SANTAN VILLAGE 5-9pm NC SOUTHPARK (NC) 5-9pm CA CONCORD 5-9:30pm NC TRIANGLE TOWN CENTER 5-9pm CA CONCORD SUNVALLEY 5-9pm NC CAROLINA PLACE (NC) 5-9pm CA WALNUT CREEK BROADWAY PLAZA 5-9pm NC HANES 5-9pm CA SANTA ROSA PLAZA 5-9pm NC WENDOVER 5-9pm CA FAIRFIELD SOLANO 5-9pm ND WEST ACRES (ND) 5-9pm CA NORTHGATE (CA) 5-9pm ND COLUMBIA (ND) 5-9pm CA PLEASANTON STONERIDGE 5-9pm NH MALL OF NEW HAMPSHIRE 5-9:30pm CA MODESTO VINTAGE FAIR 5-9pm NH BEDFORD (NH) 5-9pm CA NEWPARK 5-9pm NH MALL AT ROCKINGHAM PARK 5-9:30pm CA STOCKTON SHERWOOD 5-9pm NH FOX RUN (NH) 5-9pm CA FRESNO FASHION FAIR 5-9pm NH PHEASANT LANE (NH) 5-9:30pm CA SHOPS AT RIVER PARK 5-9pm NJ MENLO PARK 5-9:30pm CA SACRAMENTO DOWNTOWN PLAZA 5-9pm NJ WOODBRIDGE CENTER 5-9:30pm CA ROSEVILLE GALLERIA 5-9pm NJ FREEHOLD RACEWAY 5-9:30pm CA SUNRISE (CA) 5-9pm NJ MONMOUTH 5-9:30pm CA REDDING MT. -

Napa, California

NAPA, CALIFORNIA PROPERTY OVERVIEW NAPA PREMIUM OUTLETS® NAPA, CA MAJOR METROPOLITAN AREA SELECT TENANTS San Francisco: 50 miles south Ann Taylor Factory Store, Banana Republic Factory Store, Brooks Brothers Factory Store, Calvin Klein, Coach, Cole Haan Outlet, Gap RETAIL Outlet, GUESS Outlet, Gymboree Outlet, J.Crew Factory, Max Studio, Michael Kors Outlet, Nike Factory Store, Polo Ralph Lauren Factory GLA (sq. ft.) 179,000; 50 stores Store, Talbots, Tommy Hilfiger Company Store, Under Armour OPENING DATES TOURISM / TRAFFIC Opened November 1994 Over 4.5 million people per year are drawn to the Napa Valley region to Expanded 2002 vacation in the vineyards and enjoy the sumptuous restaurants and elegant spas. Highway 29: 52,000 ADT. PARKING RATIO NAPA LOCATION / DIRECTIONS PREMIUM OUTLETS 5.22:1 NAPA, CA California SR 29 and First Street in the heart of Napa Valley’s renowned wine country, 40 minutes north of San Francisco, California. RADIUS POPULATION 15 miles: 339,740 — From San Francisco: Hwy. 101 to Hwy. 37E to Hwy. 121N toward 30 miles: 1,904,248 Sonoma. Continue on 121N toward Napa/First Street turnoff. 45 miles: 4,612,100 Left turn over freeway to traffic signal. Turn left onto Freeway Drive, then right into Napa Premium Outlets. AVERAGE HH INCOME 30 miles: $97,947 Information as of 5/1/17. Source: SPG Research; trade area demographic information per STI: PopStats (2016). MASTER PLAN FREEWAY DR. TO 1ST ST. & SR 29 GAP OUTLET POLO RALPH LAUREN FACTORY STORE CALVIN KLEIN KILBURN AVE. SR 29 FREEWAY DR. NORTH NIKE FACTORY STORE AERIAL OVERVIEW LAUREL ST. -

Store Address City State Zip Muscle Beach - S.M

Store Address City State Zip Muscle Beach - S.M. 1633 Ocean Front Santa Monica CA 90401 Westfield Fox Hills 6000 S. Sepulveda Blvd #2286 Culver City CA 90230 Santa Maria Town Center 197 Santa Maria Town Center East Santa Maria CA 93454 Westfield Parkway 713 Parkway Plaza El Cajon CA 92020 Glendale Galleria 1146 Glendale Galleria Glendale CA 91210 Vintage Fair Maill 3401 Dale Road, #443 Modesto CA 95356 Puente Hills Mall 1600 S. Azusa Avenue, Unit #169G City Of Industry CA 91748-1617 The Oaks Shopping Center 382 W. Hillcrest Drive, Suite 6 Thousand Oaks CA 91360 The Shops at Mission Viejo 1005 The Shops at Mission Viejo, Sp. VC-05 Mission Viejo CA 92691 South Bay Pavilion at Carson 463 Carson Mall Carson CA 90746 Westfield Plaza Bonita 3030 Plaza Bonita Road, Space FC-9 National City CA 91950 Santa Rosa Plaza 2103 Santa Rosa Plaza Santa Rosa CA 95401 Serramonte Center 80-B Serramonte Center Daly City CA 94015 Brea Mall 2153 Brea Mall Brea CA 92821 Westfield Palm Desert 72-840 Highway 111, Space 357 Palm Desert CA 92260 The Galleria at South Bay 1815 Hawthorne Boulevard, #309 Redondo Beach CA 90278 Southland Mall 13 Southland Mall Dr. Hayward CA 94545 Montebello Town Center 1644 Montebello Town Center Montebello CA 90640 Montclair Plaza 2022 Montclair Plaza Lane Montclair CA 91763 Fashion Fair Mall 521 East Shaw Avenue, #101 Fresno CA 93710 Westfield North County 200 Via Rancho Parkway, Space #435 Escondido CA 92025 Los Cerritos Center 121 Los Cerritos Center Cerritos CA 90703 NewPark Mall #2073 NewPark Mall Newark CA 94560 The Mall at Victor -

Effective 5/4/08 Macy's West SMALL TICKET DEPARTMENTS Store/DC List As of May 4, 2008

Macy's West SMALL TICKET DEPARTMENTS Store/DC List as of May 4, 2008 Current Current New New DC Division Store Division Store DC Alpha Effective Name Number Name Number Name Code Mall Name / Store Name Address City State Zip Date Macy's Northwest 0001 MCW 0301 Tukwila TU SEATTLE (DOWNTOWN) Third and Pine Seattle WA 98181 5/4/2008 Macy's Northwest 0002 MCW 0302 Tukwila TU NORTHGATE (WA) 401 NE Northgate Way Space 602 Seattle WA 98125 5/4/2008 Macy's Northwest 0003 MCW 0303 Tukwila TU TACOMA 4502 South Steele #700 Tacoma WA 98409 5/4/2008 Macy's Northwest 0004 MCW 0304 Tukwila TU WENATCHEE VALLEY 445 Valley Mall Pkwy E. Wenatchee WA 98802 5/4/2008 Macy's Northwest 0005 MCW 0305 Tukwila TU BELLIS FAIR (BELLINGHAM) 50 Bellis Fair Pkwy Bellingham WA 98226 5/4/2008 Macy's Northwest 0006 MCW 0306 Tukwila TU SPOKANE (DOWNTOWN) Main and Wall St Spokane WA 99201 5/4/2008 Macy's Northwest 0008 MCW 0308 Tukwila TU SOUTH CENTER (WA) 500 Southcenter Mall Tukwila WA 98188 5/4/2008 Macy's Northwest 0009 MCW 0309 Tukwila TU THREE RIVERS 331 Three Rivers Dr Kelso WA 98626 5/4/2008 Macy's Northwest 0010 MCW 0310 Tukwila TU WALLA WALLA (DOWNTOWN) 54 East Main St Walla Walla WA 99362 5/4/2008 Macy's Northwest 0011 MCW 0311 Tukwila TU COLUMBIA CENTER (WA) 1321 N.Columbia Center BLVD. Suite 400 Kennewick WA 99336 5/4/2008 Macy's Northwest 0012 MCW 0312 Tukwila TU NORTHTOWN (WA) N. -

EYEXAM of CALIFORNIA Office Directory

EYEXAM of California, Inc., Revised February 2016 EYEXAM OF CALIFORNIA P.O. Box 2756 Mission Viejo, CA 92690 Office Directory 1-888-439-3392 Phone, 949-364-1289 TDD www.eyexamofca.com *All Offices Accepting New Patients *All Providers are Optometrists Licensed by the California State Board of Optometry *All Providers are DPA and TPA certified by the California State Board of Optometry *Language Assistance Available at all Offices *Additional Provider Information Available on Request at EYEXAM of California Offices *Information Subject to Change without Notice EYEXAM of California Northern California Facilities County Address City Zip Phone Doctors Languages Spoken Erica Wu, O.D., Managing Optometrist English, Clinical Spanish, Vietnamese Alameda #5774 2202F Southshore Alameda 94501-8026 (510) 521-2734 Judy Wong, O.D., Associate Optometrist Sally Melendez, O.D., Managing Optometrist English, Gujurati, Spanish, Mandarin Alameda #0489 5707 Christie Ave Emeryville 94608-2412 (510) 547-8926 Christopher Ng O.D., Associate Optometrist Jessica Liu O.D., Associate Optometrist Monica Liou, O.D., Managing Optometrist English, Tagalog, Vietnamese Alameda #0059 500 Southland Mall Hayward 94545-2148 (510) 887-2803 M.Chishty-Qawan, O.D., Associate Optometrist Noorie Dong, O.D., Managing Optometrist English, Hindi. Cantonese Alameda #0195 1115 New Park Mall Newark 94560-5246 (510) 792-6776 Jackie Tran, O.D., Associate Optometrist Carole Gee, O.D., Managing Optometrist English, Hindi Alameda #5775 2180 Contra Costa Blvd. Pleasant Hill 94523-3742 (925) 691-5055 Emily Lyn, O.D, Associate Optometrist Bei Zhang, O.D., Managing Optometrist English, Cantonese, Mandarin, Vietnamese, Alameda #0098 1104A Stoneridge Mall Road Pleasanton 94588-3219 (925) 463-3521 Aaron Neufield, O.D., Associate Optometrist Clinical Spanish Judy Wong, O.D., Associate Optometrist Tim Miller, O.D., Managing Optometrist English Contra Costa #5612 2565 Sand Creek Road, Ste.