Stoxx® Global 3000 Energy Index

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Buy Kunlun Energy

23 August 2017 Utilities Kunlun Energy Deutsche Bank Markets Research Rating Company Date Buy Kunlun Energy 23 August 2017 Results Asia China Reuters Bloomberg Exchange Ticker Price at 21 Aug 2017 (HKD) 7.45 Utilities 0135.HK 135 HK HSI 0135 Price target - 12mth (HKD) 8.50 Utilities 52-week range (HKD) 7.95 - 5.55 HANG SENG INDEX 27,155 Core profit growth in line; robust volume with slightly lower margin Valuation & Risks Kunlun's 1H17 core net profit rose by 14% yoy to Rmb2.7bn, in line with our Hanyu Zhang expectations and accounting for 58/62% of DBe/consensus full year forecast. Research Analyst Volume was as strong as expected with 12-184% yoy growth in four gas related +852-2203 6207 segments. Similar with gas utilities peers, Kunlun recorded a Rmb2cents/cm Michael Tong, CFA yoy (flat hoh) decline in EBITDA margin for gas sales segment due to market competition and failure to pass through PetroChina's winter citygate price hike. Research Analyst Mgmt expect the volume momentum to continue and margins to recover a bit +852-2203 6167 HoH in 2H17. Kunlun is the beneficiary of China's structural growth in both piped gas and the LNG value chain and is trading at an undemanding valuation of 11x Price/price relative 2018E P/E. Maintain Buy. 10 7.5 By segment results review 5 Kunlun's 1H17 reported net profit was flat yoy at Rmb2.4bn. If adding back 2.5 Rmb325mn attributable impairment loss, core net profit rose by 14% yoy to Jan '16 Jul '16 Jan '17 Jul '17 Rmb2.7bn. -

Middle East Oil Pricing Systems in Flux Introduction

May 2021: ISSUE 128 MIDDLE EAST OIL PRICING SYSTEMS IN FLUX INTRODUCTION ........................................................................................................................................................................ 2 THE GULF/ASIA BENCHMARKS: SETTING THE SCENE...................................................................................................... 5 Adi Imsirovic THE SHIFT IN CRUDE AND PRODUCT FLOWS ..................................................................................................................... 8 Reid l'Anson and Kevin Wright THE DUBAI BENCHMARK: EVOLUTION AND RESILIENCE ............................................................................................... 12 Dave Ernsberger MIDDLE EAST AND ASIA OIL PRICING—BENCHMARKS AND TRADING OPPORTUNITIES......................................... 15 Paul Young THE PROSPECTS OF MURBAN AS A BENCHMARK .......................................................................................................... 18 Michael Wittner IFAD: A LURCHING START IN A SANDY ROAD .................................................................................................................. 22 Jorge Montepeque THE SECOND SPLIT: BASRAH MEDIUM AND THE CHALLENGE OF IRAQI CRUDE QUALITY...................................... 29 Ahmed Mehdi CHINA’S SHANGHAI INE CRUDE FUTURES: HAPPY ACCIDENT VERSUS OVERDESIGN ............................................. 33 Tom Reed FUJAIRAH’S RISE TO PROMINENCE .................................................................................................................................. -

Natural Gas Energy

Annual Report 2006 Contents - PROFILE, MISSION, VISION 2015, VALUES AND CONDUCT - HIGHLIGHTS - MESSAGE FROM THE CEO - OIL MARKET OVERVIEW - CORPORATE STRATEGY - BUSINESSES Exploration and Production Refining and Commercialization Petrochemicals Transportation Distribution Natural Gas Energy - INTERNATIONAL ACTIVITIES - SOCIAL AND ENVIRONMENTAL RESPONSIBILITY Human Resources Health, Safety and the Environment Social, Environmental, Cultural and Sports Sponsorship - INTANGIBLE ASSETS Technological Capital Organizational Capital Human Capital Relationship Capital - BUSINESS MANAGEMENT Business Performance Capital Markets Risk Management Corporate Governance Annual Report 2006 2 Profile Petrobras is a publicly listed company that operates on an integrated and specialized basis in the following segments of the oil, gas and energy sector: exploration and production; refining, commercialization, transportation and petrochemicals; the distribution of oil products; natural gas and energy. Founded in 1953, Petrobras is now the world’s 14 th largest oil company, according to the publication Petroleum Intelligence Weekly . The leader in the Brazilian hydrocarbons sector, the company has been expanding, in order to become an integrated energy business with international operations, and the leader in Latin America. Mission To operate safely and profitably, in a socially and environmentally responsible manner, within the oil, gas and energy sector, both domestically and abroad, supplying products and services that meet the needs of the customers, thereby -

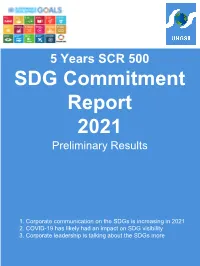

SDG Commitment Report 2021 Preliminary Results

Powered by: 5 Years SCR 500 SDG Commitment Report 2021 Preliminary Results 1. Corporate communication on the SDGs is increasing in 2021 2. COVID-19 has likely had an impact on SDG visibility 3. Corporate leadership is talking about the SDGs more Over 95% of companies now discussing SDGs in annual report Share of comapnies mentioning SDGs 100% 98% 96% 94% 92% 90% 88% 86% 84% 82% 80% 2017 2018 2019 2020 2021 Huge increase in share of chairmen discussing the SDGs Share of chairmen discussing SDGs 35% 30% 25% 20% 15% 10% 5% 0% 2017 2018 2019 2020 2021 Slight increase in share of CEOs discussing the SDGs Share of CEOs discussing SDGs 60% 50% 40% 30% 20% 10% 0% 2017 2018 2019 2020 2021 Most companies are discussing the SDGs more than last year ASML HSBC Holdings BMW Banpu Vonovia Increase in Andritz AG Iceland Air number of ABB Abbott Laboratories SDG Allianz Accenture statements in Barloworld BASF 2021 vs. 2020 Facebook Apple Remgro ABN Amro Tesco Air Canada Adidas Best Buy Fannie Mae Swatch Group Intel Bank of Montreal Whirlpool Adobe Tyson Foods Disney Freddie Mac Coach Aviva Deere JM Smucker Costco Live Nation Shoprite Haseko George Weston Carnival Comcast Hormel FedEx Conagra Walmart Sysco Boeing Medtronic Starbucks Decrease in Distell Hershey number of Citigroup Fifth Third SDG Telefonica IBM statements in Humana Astral Foods 2021 vs. 2020 Visa British American Tobacco Eskom -1500 -1000 -500 0 500 1000 1500 2000 2500 3000 5 Increase in visibility of almost all SDGs in 2021; decreases not statistically significant SDG8 Decent Work SDG16 Peace & Justice Increase in SDG9 Industry & Innovation number of SDG SDG12 Responsible Consumption statements in SDG3 Good Health 2021 vs. -

Energy Investments in a Zero-Carbon World

Investment Management ENERGY INVESTMENTS IN A ZERO-CARBON WORLD The energy sector is controversial. It faces a perfect (usually in the single to low double digits), whereas storm due to the short-term demand shock caused by the iron-ore and copper reserves are often measured in COVID-19 pandemic and the longer-term risk from the decades or even centuries. This means that at current reduction in society’s carbon footprint to combat climate production rates, under all scenarios for future oil change. Considering this uncertainty and the collapse demand, it is impossible for upstream reserves to in valuations in the sector, we are confronted with dual become obsolete due to inadequate demand for oil. scenarios: whether the sector presents an exceptional • With respect to new competitors, US shale has investment opportunity or is destined for obsolescence. We emerged as a powerful new supply source over believe the key questions are: the past few years. But we estimate that US shale 1. What is the risk that energy companies will be left with production requires an oil price of $60 per barrel or material stranded assets in a carbon-neutral world? more to be economical, underscoring the limits as to how much disruption shale can cause. 2. How will the coming energy transition impact the sustainability of energy companies? MULTI-DECADE DEMAND FOR OIL AND GAS This note focuses on the risks and opportunities presented It bears repeating that there is no scenario under by the upcoming transition for the energy sector. We which the demand for oil and gas will disappear in address company-specific issues as part of our research the next few decades. -

Empresas Copec S.A. Consolidated Financial

EMPRESAS COPEC S.A. CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2018 IFRS - International Financial Reporting Standards IAS - International Accounting Standards NIFCH - Chilean Financial Reporting Standards IFRIC - International Financial Reporting Interpretations Committee US$ - United States dollars ThUS$ - Thousands of US dollars MUS$ - Millions of US dollars MCh$ - Millions of Chilean Pesos COP$ - Colombian pesos S./ - Peruvian nuevo sol WorldReginfo - d6a34cd4-9970-4f3e-9bfb-af0f71482286 INDEPENDENT AUDITORS' REPORT Santiago, March 8, 2019 Dear Shareholders and Directors Empresas Copec S.A. We have audited the accompanying consolidated financial statements of Empresas Copec S.A. and affiliates, which comprise a consolidated statement of financial position as of December 31, 2018 and 2017, the corresponding consolidated statements of income by function, consolidated comprehensive income, consolidated changes in equity and consolidated cash flow for the years ending on these dates, and the corresponding notes to the consolidated financial statements. Management's responsibility for the consolidated financial statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards (IFRS). This responsibility includes the design, implementation and maintenance of relevant internal controls for the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether -

Credit Trend Monitor: Earnings Rising with GDP; Leverage Trends Driven by Investment

CORPORATES SECTOR IN-DEPTH Nonfinancial Companies – China 24 June 2021 Credit Trend Monitor: Earnings rising with GDP; leverage trends driven by investment TABLE OF CONTENTS » Economic recovery drives revenue and earnings growth; leverage varies. Rising Summary 1 demand for goods and services in China (A1 stable), driven by the country's GDP growth, Auto and auto services 6 will benefit most rated companies this year and next. Leverage trends will vary by sector. Chemicals 8 Strong demand growth in certain sectors has increased investment requirements, which in Construction and engineering 10 turn could slow some companies’ deleveraging efforts. Food and beverage 12 Internet and technology 14 » EBITDA growth will outpace debt growth for auto and auto services, food and Metals and mining 16 beverages, and technology hardware. As a result, leverage will improve for rated Oil and gas 18 companies in these sectors. A resumption of travel, outdoor activities and business Oilfield services 20 operations, with work-from-home options, as the coronavirus pandemic remains under Property 22 control in China will continue to drive demand. Steel, aluminum and cement 24 Technology hardware 26 » Strong demand and higher pricing will support earnings growth for commodity- Transportation 28 related sectors. These sectors include chemicals, metals and mining, oil and gas, oilfield Utilities 30 services, steel, aluminum and cement. Leverage will improve as earnings increase. Carbon Moody's related publications 32 transition may increase investments for steel, aluminum and cement companies. But List of rated Chinese companies 34 rated companies, which are mostly industry leaders, will benefit in the long term because of market consolidation. -

Energy on the Move Annual Report and Accounts 2014

Energy on the move Annual Report and Accounts 2014 Energy on the move Annual Report and Accounts 2014 www.galpenergia.com This translation of the Portuguese document was made only for the convenience of non-Portuguese speaking interested parties. For all intents and purposes, the Portuguese version shall prevail. ENERGY ON THE MOVE To evolve is to become adapted to the challenges of our surroundings, it is to adjust to new realities and to find ways to overcome our goals. It is for this reason that we can today think of Galp Energia as a living organism, where concepts such as resilience, adaptation, adjustment, involvement and joint construction allow for continuous evolution. Exploration & Production Refining & Marketing Gas & Power Galp Energia + + = Annual Report and Accounts 2014 01 Galp Energia 8 1.1 Galp Energia in the world 10 1.2 Statement of the Board of Directors 12 1.3 Strategy 16 1.4 Main indicators 18 02 Activities 20 2.1 Market environment 21 2.2 Exploration & Production 25 2.3 Refining & Marketing 37 2.4 Gas & Power 41 03 Financial performance 44 3.1 Executive summary 45 3.2 Results analysis 45 3.3 Capital expenditure 47 3.4 Cash flow 47 3.5 Financial debt 48 04 Risk management 49 4.1 Risk management model 50 4.2 Internal control system 51 4.3 Main risks 52 05 Commitment to stakeholders 59 5.1 Corporate governance 60 5.2 Human capital 67 5.3 Research and technology 69 5.4 Health, safety and environment 70 5.5 Quality 72 5.6 Local community development 73 06 Appendices 74 6.1 Proposed allocation of net profit 75 6.2 Additional information 75 6.3 Consolidated financial statements 78 6.4 Reports and opinions 170 6.5 Glossary and acronyms 177 This page is intentionally left blank. -

MINUTA Petrobras Distribuidora SA Companhia Aberta De Capital

MINUTA Petrobras Distribuidora S.A. Companhia Aberta de Capital Autorizado – CVM nº 24295 Rua Correia Vasques 250, Cidade Nova, CEP 20211-140, Rio de Janeiro, RJ CNPJ n.º 34.274.233/0001-02 – NIRE 33.3.0001392-0 – Código ISIN BRBRDTACNOR1 Código de Negociação das Ações na B3 S.A. – Brasil, Bolsa, Balcão ("B3"): "BRDT3" PEDIDO DE RESERVA PARA INVESTIDORES NÃO INSTITUCIONAIS PARA PAGAMENTO À VISTA DE AÇÕES ORDINÁRIAS DE EMISSÃO DE PETROBRAS DISTRIBUIDORA S.A. N.º Pedido de reserva ("Pedido de Reserva") relativo à oferta pública de distribuição secundária de 436.875.000 ações ordinárias, nominativas, escriturais e sem valor nominal de emissão de Petrobras Distribuidora S.A. ("Companhia"), livres e desembaraçadas de quaisquer ônus ou gravames ("Ações"), de titularidade de Petróleo Brasileiro S.A. – Petrobras, sociedade de economia mista com registro de emissor de valores mobiliários perante a Comissão de Valores Mobiliários ("CVM"), com sede na Cidade do Rio de Janeiro, Estado do Rio de Janeiro, na Avenida República do Chile 65, inscrita no Cadastro Nacional da Pessoa Jurídica do Ministério da Economia ("CNPJ") sob o n.º 33.000.167/0001-01 ("Acionista Vendedor"), na qualidade de acionista vendedor e ofertante. As Ações serão ofertadas no Brasil, sob a coordenação de Banco Morgan Stanley S.A. ("Coordenador Líder"), Bank of America Merrill Lynch Banco Múltiplo S.A. ("Bank of America"), Citigroup Global Markets Brasil, Corretora de Câmbio, Títulos e Valores Mobiliários S.A. ("Citi"), Goldman Sachs do Brasil Banco Múltiplo S.A. ("Goldman Sachs"), Banco Itaú BBA S.A. ("Itaú BBA"), Banco J.P. Morgan S.A. -

China and IMO 2020

December 2019 China and IMO 2020 OIES PAPER: CE1 Michal Meidan The contents of this paper are the author’s sole responsibility. They do not necessarily represent the views of the Oxford Institute for Energy Studies or any of its members. Copyright © 2019 Oxford Institute for Energy Studies (Registered Charity, No. 286084) This publication may be reproduced in part for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgment of the source is made. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the Oxford Institute for Energy Studies. ISBN : 978-1-78467-154-9 DOI: https://doi.org/10.26889/9781784671549 2 Contents Contents ................................................................................................................................................. 3 Introduction ........................................................................................................................................... 2 I. Background: IMO 2020 .................................................................................................................. 3 II. China: Tough government policies to tackle shipping emissions… ....................................... 5 III. ...but a relatively muted response from refiners ..................................................................... 7 a. A tale of two bunker markets ....................................................................................................... -

Capital Increase Presentation

Enel Américas Capital Increase February 27th, 2019 Table of Contents Our Track Record Transaction Rationale Transaction Structure Closing Remarks 2 Our Track Record 3 Proposed Equity Capital Increase Facilitates Pursuit of Proven Growth Strategy Formation of Successful Up to US$ 3.5 Bn Continued the Largest Delivery of Capital Increase Growth Private Utility Growth and Capital Structure Strategy & Company in Shareholder Optimization to Consolidation LatAm Value Unlock Growth Created Americas- Organic Facilitates execution of Minority investors buyout focused growth vehicle growth strategy with leading market Captured efficiencies Privatization and position Cash flow optimization consolidation Expanded Free Market Unlocked efficiencies and Enel X segments Credit enhancement Enel X expansion Simplified structure Inorganic Higher market capitalization, float and Reduced leakage Acquired Enel Dx São liquidity Paulo and Enel Dx Goiás evidencing strong value creation capabilities 4 Our Track Record Sustainability, Growth, Efficiencies and Value Creation 2016 2018 I&N(3) End users MM 14.1 24.5 EBITDA US$ Bn 2.4 3.4 Growth Net Income US$ Bn 1.0 1.7 CAPEX US$ Bn 1.2 1.7 Group simplification Number of companies 43 32(4) Opex reduction Cumulated efficiencies(1,5) US$ MM ~ 130 ~ 420 Shareholder return Total Dividends US$ Bn 0.3 0.5 Value creation People benefited(1) MM (cumulated) 1.4 2.7 Sustainability commitment Index Member Number of indexes 0 4(2) Notes: 3. Infrastructure & Networks 5 1. Base year 2015 4. Not including acquired -

The Petrobras Zero Hunger Program Invests R$ 303 Million to Fight Social

www.petrobras.com.br 2003 reportsocial responsibility HIGHLIGHTS Partnership with society The Petrobras Zero Hunger With its strong economic and social involvement in the regions where the company is Program invests R$ 303 million to located, Petrobras supports and participates in the preparation, execution and refinement of fight social exclusion and bring comprehensive public policies. Much of this work is a result of partnerships with universities, NGOs and public bodies. about development with citizenship Suppliers are encouraged Petrobras is widely recognized for its strong to do their bit commitment towards social values and the Petrobras encourages its company, since 2003, has been aligning its suppliers to strive for standards activities in the social area with public of operational safety, envi- policies to fight social exclusion and misery. ronmental protection and This is the spirit underlying the Petrobras attention to health similar to Zero Hunger Program, which is helping to those prevailing in its own transform the situation of the country’s activities. poorest communities. Between now and Ombudsperson ensures 2006, a total of R$ 303 million will be transparent relations invested in projects that will have a positive The corporate ombudsperson impact in the areas of education, pro- is the principal means of fessional training, the generation of income ensuring transparency in and employment for adolescents and adults, Petrobras’ relations with its protecting children and teenagers’ rights, workers, customers, suppliers social undertakings and voluntary work. and society in general. With the Petrobras Zero Hunger Program, Petrobras upholds the company has redirected its social policy biodiversity and and focused its activities towards achieving environmental protection development with citizenship, which should The company has developed benefit some 4 million people throughout programs for the protection Brazil.