Infrastructural Power, Monetary Policy, and the Resilience of European Market-Based Banking’, Online Manuscript, Osf.Io/Preprints/Socarxiv/Nrmt4

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Autonomous Power of the State

The autonomous power of the state : its origins, mechanisms and results Author(s): MICHAEL MANN Source: European Journal of Sociology / Archives Européennes de Sociologie / Europäisches Archiv für Soziologie, Vol. 25, No. 2, Tending the roots : nationalism and populism (1984), pp. 185-213 Published by: Cambridge University Press Stable URL: http://www.jstor.org/stable/23999270 Accessed: 14-09-2017 18:37 UTC JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at http://about.jstor.org/terms Cambridge University Press is collaborating with JSTOR to digitize, preserve and extend access to European Journal of Sociology / Archives Européennes de Sociologie / Europäisches Archiv für Soziologie This content downloaded from 140.180.248.195 on Thu, 14 Sep 2017 18:37:47 UTC All use subject to http://about.jstor.org/terms MICHAEL MANN The autonomous power of the state , its origins, mechanisms and results This essay tries to specify the origins, mechanisms and results of the autonomous power which the state possesses in relation to the major power groupings of 'civil society'. The argument is couched generally, but it derives from a large, ongoing empirical research project into the development of power in human societ ies (i). At the moment, my generalisations are bolder about agrar ian societies ; concerning industrial societies I will be more tentative. -

As Detained for 437 Days in China’S Sprawling New System of Incarceration and Indoctrination

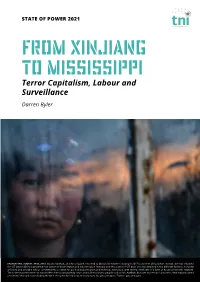

STATE OF POWER 2021 From Xinjiang to Mississippi Terror Capitalism, Labour and Surveillance Darren Byler KAZAKHSTAN, ALMATY, APRIL 2019: Gulzira Auelhan, an ethnic Kazakh, returned to China’s far western Xinjiang in 2017 to visit her ailing father. Instead, she was detained for 437 days in China’s sprawling new system of incarceration and indoctrination. Instead, over the course of 437 days, she was detained in five different facilities, including a factory and a middle school converted into a centre for political indoctrination and technical instruction, with several interludes of a form of house arrest with relatives. The Chinese government has said it offers free vocational education and skills training to people such as Ms. Auelhan. But over more than 14 months, “that training lasted one week,” she said, not including the time she spent forced to work in a factory. IG: @noorimages / Twitter: @noorimages The Chinese state within Xinjiang has forged a form of capitalist frontier-making based on data harvesting and unfree human labour that exploits ethno-racial difference in order to generate new forms of capital accumulation and coercive state power. ‘Where is your ID!’ the police contractor yelled at me in Uyghur. I looked up in surprise. I had been avoiding eye contact, trying to attract as little attention as possible. In April 2018, in the tourist areas of Kashgar – where there were checkpoints every 200 metres – the contractors usually recognised a bespectacled white person as a foreigner. But over the years that I had lived and worked as an anthropologist in Northwest China I had often been mistaken for a Uyghur. -

An Assessment of Mexican Political Institutions Since the Merida

Conductive Capacity of The State 1 Conductive Capacity of The State: An Assessment of Mexican Political Institutions Since the Merida Initiative By Jose Pablo Olvera An Applied Research Project Submitted to the Department of Public Administration Texas State University-San Marcos In Partial Fulfillment for the Requirements for the degree of Masters of Public Administration Spring 2017 Dr. Patricia Shields Christopher Brown, JD Ms. Alejandra Pena, MPA Conductive Capacity of The State 2 Abstract The purpose of this applied research paper is to conduct a preliminary assessment of Mexico’s political institutions since the Merida Initiative to evaluate the progress, or lack thereof, in relation to the agreement’s explicit goals of institutionalizing reforms and supporting democratic governance. The project’s framework is structured using three core pillar questions that address Mexican state capacities: coercive, extractive, and conductive capacity. Conductive capacity refers to the state’s ability to effectively channel citizen demands through the state apparatus. First, an assessment of Mexico’s political institutions is performed using a variety of methods, including data, survey-item, and case study analyses. Second, the dimension of conductive capacity is tested against coercive and extractive capacities to evaluate whether an interaction between these exists. The results of the assessment demonstrate that the Mexican state’s coercive and conductive capacities have significantly decreased since the implementation of the Merida Initiative, while demonstrating that coercive and extractive capacities of the state significantly predict conductive capacity dimension variables. Conductive Capacity of The State 3 Acknowledgments I would like to begin by thanking my parents, Alfonso and May, for their sacrifice made when they decided to leave almost everything behind so that my siblings and I could have a chance at a better future. -

Part I INTRODUCTION

Part I INTRODUCTION 99781107029866c01_p1-24.indd781107029866c01_p1-24.indd 1 110/9/20120/9/2012 110:30:380:30:38 PPMM 99781107029866c01_p1-24.indd781107029866c01_p1-24.indd 2 110/9/20120/9/2012 110:30:390:30:39 PPMM 1 Republics of the Possible State Building in Latin America and Spain Miguel A. Centeno and Agust í n E. Ferraro Introduction Latin American republics were among the fi rst modern political entities designed and built according to already tried and seemingly successful institutional mod- els. During the wars of independence and for several decades thereafter, pub- lic intellectuals, politicians, and concerned citizens willingly saw themselves confronted with a sort of void, a tabula rasa. Colonial public institutions and colonial ways of life had to be rejected, if possible eradicated, in order for new political forms and new social mores to be established in their stead. However, in contrast to the French or American revolutions, pure political utopias did not play a signifi cant role for Latin American institutional projects. The American Revolution was a deliberate experiment; the revolutionar- ies fi rmly believed that they were creating something new, something never attempted before. The French revolutionaries dramatically signaled the same purpose by starting a whole new offi cial calendar from year one. In contrast, Latin American patriots assumed that proven and desirable institutional mod- els already existed, and not just as utopic ideals. The models were precisely the state institutions of countries that had already undergone revolutions or achieved independence, or both: Britain , the United States, France, and others such as the Dutch Republic . -

The Social Origins of State Power in China by Daniel Christopher

The Social Origins of State Power in China by Daniel Christopher Mattingly A dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in Political Science in the Graduate Division of the University of California, Berkeley Committee in charge: Professor Kevin J. O'Brien, Chair Professor Ruth Berins Collier Professor Peter L. Lorentzen Professor Noam Yuchtman Summer 2016 The Social Origins of State Power in China Copyright 2016 by Daniel Christopher Mattingly 1 Abstract The Social Origins of State Power in China by Daniel Christopher Mattingly Doctor of Philosophy in Political Science University of California, Berkeley Professor Kevin J. O'Brien, Chair This dissertation investigates the origins of state power and political accountability. How do states exercise political control over their populations and implement policies that have clear winners and losers? Do democratic institutions in combination with a strong civil society strengthen political accountability? I examine these questions in the context of rural China, which combines limited local democracy and vibrant non-state groups such as kinship associations, temples, and neighborhood groups. Many argue that strong civil society institutions and local elections can curb the power of the state and hold government officials accountable. However, in this dissertation I argue that in China, strong civil society groups and village elections have expanded state power and helped officials confiscate wealth. The first part of the dissertation develops my theory of state power. Drawing on new data from rural China, I show that citizens distrust the ruling Chinese Communist Party (CCP) and believe that local party cadres do not represent their interests. -

SOAS-AKS Working Papers in Korean Studies

School of Oriental and African Studies University of London SOAS-AKS Working Papers in Korean Studies No. 38 The Rhetorical Power of Neo-Liberalism and the Strengthening of the Korean State David Hundt February 2013 http://www.soas.ac.uk/japankorea/research/soas-aks-papers/ SOAS-AKS Working Papers in Korean Studies, No. 38 February 2013 The Rhetorical Power of Neo-Liberalism and the Strengthening of the Korean State NOT FOR CITATION. COMMENTS AND FEEDBACK WELCOME. David Hundt Deakin University [email protected] © 2013 http://www.soas.ac.uk/japankorea/research/soas-aks-papers/ The Rhetorical Power of Neo-Liberalism and the Strengthening of the Korean State Abstract: This article tests the assumption that neo-liberalism inevitably detracts from state strength by analysing the power of the Korean state since the Asian economic crisis. Despite expectations to the contrary, the state has retained its influential position as economic manager, thanks to a combination of two types of power: the repressive powers of the developmental state, and crucially, powers stemming from neo-liberalism itself. The Korean state used both these resources, which amount to the full spectrum of what Michael Mann refers to as infrastructural power, in its social and political struggle with civil society over economic policy. Rather than being a disempowering force, neo-liberal reform enhanced the political position of the Korean state, which presented itself as an agent capable of resolving long-standing economic problems, defending law and order, and attracting the support of democratic forces. Our findings suggest that neo-liberalism offers some states the opportunity to remain weighty economic actors, and developmental states may be particularly adept at co-opting elements of civil society into governing alliances. -

Infrastructural Exclusion and the Fight for the City: Power, Democracy, and the Case of America’S Water Crisis

\\jciprod01\productn\H\HLC\53-2\HLC208.txt unknown Seq: 1 29-OCT-18 9:18 Infrastructural Exclusion and the Fight for the City: Power, Democracy, and the Case of America’s Water Crisis K. Sabeel Rahman* TABLE OF CONTENTS INTRODUCTION .................................................. 533 I. INFRASTRUCTURAL EXCLUSION ............................ 536 R A. The Flint water crisis ................................ 536 R B. Mechanisms of infrastructural exclusion ............... 538 R II. TOWARD A POLITICAL THEORY OF INFRASTRUCTURE: POWER, DEMOCRACY, AND THE PUBLIC UTILITY TRADITION .......... 541 R III. CONSTRUCTING INCLUSIVE INFRASTRUCTURE: WATER AND BEYOND ................................................. 547 R A. Mandating water equity .............................. 548 R B. Restoring public (and democratic) utilities ............ 551 R C. Public oversight over the broader water infrastructure ....................................... 554 R 1. The importance of strategic and system-wide public oversight ........................................ 554 R 2. Institutionalizing strategic enforcement ............ 557 R IV. CONCLUSION ............................................ 560 R INTRODUCTION In 2013, government officials in Flint, Michigan, which had been placed under state-appointed emergency management following a long- standing budget crisis, imposed a variety of cost-cutting measures. One of these measures included switching the city’s water supply temporarily to the Flint River. Another decision was made not to spend scarce dollars on treat- ing the water with anti-corrosion agents. The result was a severe erosion of * Assistant Professor of Law, Brooklyn Law School; Fellow, Roosevelt Institute. I am grateful to the editors of the Harvard Civil Rights-Civil Liberties Law Review for inviting me to contribute to this special issue. This paper was first drafted in December 2016. It draws on previous works including Rahman, THE NEW UTILITIES: PRIVATE POWER, SOCIAL INFRASTRUC- TURE, AND THE REVIVAL OF THE PUBLIC UTILITY CONCEPT, 30 CARDOZO L. -

Michael Mann the Sources of Social Power, Volume 3 Chapter 1: Introduction

Michael Mann The Sources of Social Power, Volume 3 Chapter 1: Introduction The third volume of my history of power in human society concerns the period of history leading up to 1945. But I cannot put a precise starting-date on this period since two different time-scales are involved. My second volume, on the advanced industrializing countries, ended in 1914, so I here resume their domestic stories in 1914, though I go back a little further in the cases of the US and Japan. But I am also concerned here with global empires, which I neglected in my second volume. This involves the second, much longer time-scale, starting well before 1914. We will also see that the years 1914 to 1945 must not be seen as a period quite apart, an island of chaos amid a sea of tranquility. Its crises were the culmination of long-standing structural tendencies of modern Western civilization. The main story in both periods is that globalizations were well under way. Note the plural: there was more than one process of globalization. As I have argued throughout my volumes, human societies form around four distinct power sources – ideological, economic, military and political – which have a relative degree of autonomy from each other (this is my IEMP model of power). So what is generally called globalization (singular) actually involved the plural extension of relations of ideological, economic, military and political power across the world. Around these sources congeal the major power organizations of human societies. In this period the most fundamental were capitalism, empires and nation-states. -

State Infrastructural Power and Nationalism: Comparative Lessons from Mexico and Argentina

State infrastructural power and nationalism: Comparative lessons from Mexico and Argentina Matthias vom Hau October 2007 Brooks World Poverty Institute BWPI Working Paper 11 [email protected] Brooks World Poverty Institute The University of Manchester Humanities Bridgeford Street Building Oxford Road Manchester, M13 9PL U.K. Creating and sharing knowledge to help end poverty Brooks World Poverty Institute ISBN 978-1-906518-10-3 www.manchester.ac.uk/bwpi Abstract This paper focuses on the nexus between state infrastructural power and legitimacy. A comparative case study of nationalism in mid-20th century Mexico and Argentina provides the basis for theorising the impact of state infrastructural power on transformations of official national ideology. Both countries experienced a transition from liberal to popular nationalism. Yet, the extent to which popular nationalism became a regular product of state organisations varied between the two cases, depending on the timing of state development. The temporal congruence between the expansion of state infrastructural power and ideological change, as exemplified by Mexico under Cárdenas, facilitated the full institutionalisation of the new official ideology, whereas a disjuncture between state development and ideological change, as exemplified by Argentina under Perón, inhibited such a comprehensive transformation of nationalism. Keywords: Mexico, Argentina, nationalism, institutionalisation, education, schooling, state formation, state capacity, teachers Matthias vom Hau is a Lewis-Gluckman Postdoctoral Research Fellow at the Brooks World Poverty Institute, The University of Manchester. Acknowledgements This research was supported by an IDRF fellowship from the Social Science Research Council (SSRC) and by the German Academic Exchange Service (DAAD). A previous version was presented at the 2007 Annual Meeting of the American Political Science Association in Chicago. -

The French Revolution in Germany and the Origins of Sociology

HISTORICKÁ SOCIOLOGIE 1/2018 The French Revolution in Germany and the Origins of Sociology ERIC R. LYBECK* Francouzská revoluce v Německu a počátky sociologie Abstract: The French Revolution was central to the emergence of modern society, and by exten- sion, modern social science. However, not only French scientists contributed to the invention of sociology, nor for that matter did sciences necessarily begin by emulating natural science. Instead, this paper argues for a different origin of sociology from the professional faculty of Law. This trajectory emerged in early nineteenth century Germany, not in emulation of the French Revolu- tion, but as part of a broader conservative reaction to French rationalism and imperial hypocrisy. Understanding these origins not only help us better understand the familiar sociology of Max Weber, or even Marx and Durkheim who were trained in this legal scientific tradition; this his- torical understanding reveals an important relationship between sociology and the State as well as conservative politics. Keywords: Germany; Sociology; Law; Legal Science; Civil Service; Weber; Savigny DOI: 10.14712/23363525.2018.37 Introduction The French Revolution is undoubtedly a central event in the history of modern soci- ety, and, consequently, within sociology, the academic discipline occupied with studying modern societies. As Krause [2016] notes, the revolution remains one of many “privi- leged research objects” within the Western sociological canon, particularly within com- parative-historical studies of radical social change [Skocpol 1979; Sewell 1985; Tilly 1968; Moore 1966]. Particularly in the wake of the Atlanticist historical tradition that emerged in the postwar era [Palmer 2014; Black 2001; Haller 2007], the revolution figures as the origin of several constitutional elements of modern society: popular elections; meritocracy and the removal of inherited privileges; nationalism; and rational, specialized administration. -

STATE CAPACITY AS POWER: a CONCEPTUAL FRAMEWORK Johannes Lindvall and Jan Teorell Lund University April 7, 2017

STATE CAPACITY AS POWER: A CONCEPTUAL FRAMEWORK Johannes Lindvall and Jan Teorell Lund University April 7, 2017 Abstract: In reviewing existing definitions and theories of state capacity, we find most to be too teleological, too inductive, and too closely tailored to explaining particular outcomes. We argue that this limits the concept’s applicability arbitrari- ly and impedes theory development. This paper proposes a new conceptualization of state capacity, defined as the strength of the causal relationship between the po- licies that states adopt and the outcomes they intend to achieve. We show that un- der this definition, a state’s capacity can be conceptually distinguished from its autonomy (i.e., its regime). We then develop a theoretical argument about the re- lationship between the resources that states deploy when they implement policies – especially financial resources, human capital, and information – and the three main instruments that states rely on when they control territories and populations: coercion, economic incentives, and propaganda. We end by outlining the contours of a new research agenda on the state and its making that follows from this theory. We are grateful to Jens Bartelson, Michael Bernhard, John Gerring, Anna Grzy- mala-Busse, Sören Henn, Jane Mansbridge, Jørgen Møller, Pippa Norris, and se- minar participants at Boston University, Harvard University, Lund University, and the University of Gothenburg for their thoughtful comments on earlier drafts of this paper. I. Introduction State capacity has become a major research topic in the social sciences. A large and growing literature now argues that if we wish to explain long-run political changes and enduring differences in economic and political development among countries, we first need to understand how states become able to control their territories, raise revenue, establish effective bureaucracies, and deliver public services.1 We argue that the existing literature on state capacity suffers from three related weaknesses. -

Infinite Money and Infrastructural Power: Analyzing the Fiscal Determinants of English State Building, 1689–1789

University of Denver Digital Commons @ DU Josef Korbel Journal of Advanced International Studies Josef Korbel School of International Studies Summer 2013 Infinite Money and Infrastructural Power: Analyzing the Fiscal Determinants of English State Building, 1689–1789 John Louis Boston College Follow this and additional works at: https://digitalcommons.du.edu/advancedintlstudies Part of the International and Area Studies Commons Recommended Citation John Louis, “Infinite Money and Infrastructural Power: Analyzing the Fiscal Determinants of English State Building, 1689-1789,” Josef Korbel Journal of Advanced International Studies 5 (Summer 2013): 59-81 This Article is brought to you for free and open access by the Josef Korbel School of International Studies at Digital Commons @ DU. It has been accepted for inclusion in Josef Korbel Journal of Advanced International Studies by an authorized administrator of Digital Commons @ DU. For more information, please contact [email protected],[email protected]. Infinite Money and Infrastructural Power: Analyzing the Fiscal Determinants of English State Building, 1689–1789 This article is available at Digital Commons @ DU: https://digitalcommons.du.edu/advancedintlstudies/3 Infinite Money and Infrastructural Power ANALYZING THE FISCAL DETERMINANTS OF ENGLISH STATE BUILDING, 1689- 1789 JOHN LOUIS Boston College PhD Candidate, Political Science Geographically limited with a small population and few resources, how did England achieve great power status by the close of the 18th century? Scholars have debated whether debt or taxes were the primary determinants of English state building. Using data from the European State Finance database this paper provides a systematic statistical study designed to disentangle the causal relationship between war, debt and taxes as determinants of English state building.