Trends Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

00030-147377.Pdf (249.74

America’s MLSs are Making the Market Work™ On April 5, 2018, the Federal Trade Commission (FTC) and Department of Justice (DOJ) announced they would hold a joint workshop on June 5, 2018, to “explore competition issues in the residential real estate brokerage industry. As part of the workshop, the FTC and DOJ are seeking public comment.” The Council of Multiple Listing Services (CMLS) provides this paper as input to the FTC, DOJ, and interested industry participants about the critical pro-competitive role of Multiple Listing Services (MLSs) in the American residential real estate industry. 2017 CMLS | Copyright 2018 CMLS | Edition 1 CMLS | Data and Choices Breed Competition Table of Contents MLSs play a critical pro-competitive role ................................................................................... 1 MLSs are critical conduits, offering an array of choices to access listing data content ........... 2 Consumers have unprecedented access to listing content, thanks in part to MLSs ............... 2 The industry is embracing standards without regulatory pressure ......................................... 3 Listing data content represents valuable intellectual property of brokers and others ............... 4 Broker and seller choice is critical to protect data content, listing brokers, and sellers ............. 4 MLSs support seller and listing broker decision-making about distribution ........................... 4 Independent broker and seller decision-making is pro-competitive ...................................... 5 Past -

2021-Swanepoel-Trends-Report-Trend-01-Real-Estate-In-A-Post-Pandemic-'New-Normal'.Pdf

REAL ESTATE Swanepoel Trends Report, 16th Edition TRENDS OFFICIAL EXTRACT TREND 1: REAL ESTATE IN A POST-PANDEMIC ‘NEW NORMAL’ (PAGES 190-215) 2021 A Market Intelligence Report by T3 Sixty, LLC “Comprehensive research and strategic planning are indispensable for future real estate success. The Swanepoel Trends Report represents the gold standard for third party independent scholarship pertaining to this all-important process.” Gino Blefari, CEO, HSF Affiliates “The Swanepoel Trends Report is ‘the’ go-to book on what is happening within the industry, a great source of real information to help brokers and brands plan for what lies ahead. I have been a subscriber since inception. It gets better and better every year.” Sherry Chris, President & CEO, Realogy Expansion Brands “It’s the best consolidated market intel available and a great tool to use to ponder change, innovation and the industry.” Matthew Consalvo, CEO, Arizona Regional MLS “The Swanepoel Trends Report refines the way I view the industry It’s required reading for my entire board of directors.” Art Carter, CEO, CRMLS “The Swanepoel Trends Report is one of my ‘go to’ reference guides regarding future trends in the real estate vertical. Truly a phenom- enal resource and one that provides great insight and value.” Bob Goldberg, CEO, National Association of REALTORS® “Every month during our Executive Strategy Group Meeting, our executive team selects one trend from the Swanepoel Trends Report to talk through. We discuss this trend and identify a positive opportunity we want to pursue -

Proptech 3.0: the Future of Real Estate

University of Oxford Research PropTech 3.0: the future of real estate PROPTECH 3.0: THE FUTURE OF REAL ESTATE WWW.SBS.OXFORD.EDU PROPTECH 3.0: THE FUTURE OF REAL ESTATE PropTech 3.0: the future of real estate Right now, thousands of extremely clever people backed by billions of dollars of often expert investment are working very hard to change the way real estate is traded, used and operated. It would be surprising, to say the least, if this burst of activity – let’s call it PropTech 2.0 - does not lead to some significant change. No doubt many PropTech firms will fail and a lot of money will be lost, but there will be some very successful survivors who will in time have a radical impact on what has been a slow-moving, conservative industry. How, and where, will this happen? Underlying this huge capitalist and social endeavour is a clash of generations. Many of the startups are driven by, and aimed at, millennials, but they often look to babyboomers for money - and sometimes for advice. PropTech 2.0 is also engineering a much-needed boost to property market diversity. Unlike many traditional real estate businesses, PropTech is attracting a diversified pool of talent that has a strong female component, representation from different regions of the world and entrepreneurs from a highly diverse career and education background. Given the difference in background between the establishment and the drivers of the PropTech wave, it is not surprising that there is some disagreement about the level of disruption that PropTech 2.0 will create. -

Graduation Ceremonies December 2019

GRADUATION CEREMONIES DECEMBER 2019 CONTENTS Morning Ceremony – Thursday 12 December at 10h00............................................................……...3 Faculties of Health Sciences 1 and Law Afternoon Ceremony – Thursday 12 December at 15h00 ………..............….........…………………22 Faculties of Engineering & the Built Environment and Science Morning Ceremony – Friday 13 December at 09h00 …………................……................…………..48 Faculty of Humanities Afternoon Ceremony – Friday 13 December at 14h00 …….....…………..............................………66 Faculty of Commerce Evening Ceremony – Friday 13 December at 18h00 …………................……................…………..78 Faculty of Health Sciences 2 NATIONAL ANTHEM Nkosi sikelel’ iAfrika Maluphakanyisw’ uphondolwayo, Yizwa imithandazo yethu, Nkosi sikelela, thina lusapho lwayo. Morena boloka etjhaba sa heso, O fedise dintwa la matshwenyeho, O se boloke, O se boloke setjhaba sa heso, Setjhaba sa South Afrika – South Afrika. Uit die blou van onse hemel, Uit die diepte van ons see, Oor ons ewige gebergtes, Waar die kranse antwoord gee, Sounds the call to come together, And united we shall stand, Let us live and strive for freedom, In South Africa our land. 2 FACULTIES OF HEALTH SCIENCES (CEREMONY 1) AND LAW ORDER OF PROCEEDINGS Academic Procession. (The congregation is requested to stand as the procession enters the hall) The Presiding Officer will constitute the congregation. The National Anthem. The University Dedication will be read by a member of the SRC. Musical Item. Welcome by the Master of Ceremonies. The Master of Ceremonies will present Peter Zilla for the award of a Fellowship. The graduands and diplomates will be presented to the Presiding Officer by the Deans of the faculties. The Presiding Officer will congratulate the new graduates and diplomates. The Master of Ceremonies will make closing announcements and invite the congregation to stand. -

![Mortgage Technology July 2018 Mortgage Technology July 2018 Sector Dashboard [4]](https://docslib.b-cdn.net/cover/3936/mortgage-technology-july-2018-mortgage-technology-july-2018-sector-dashboard-4-993936.webp)

Mortgage Technology July 2018 Mortgage Technology July 2018 Sector Dashboard [4]

Sectorwatch: Mortgage Technology July 2018 Mortgage Technology July 2018 Sector Dashboard [4] Public Basket Performance [5] Operational Metrics [7] Valuation Comparison [10] Recent Deals [13] Appendix [14] 7 Mile Advisors appreciates the opportunity to present this confidential information to the Company. This document is meant to be delivered only in conjunction with a verbal presentation, and is not authorized for distribution. Please see the Confidentiality Notice & Disclaimer at the end of the document. All data cited in this document was believed to be accurate at the time of authorship and came from publicly available sources. Neither 7 Mile Advisors nor 7M Securities make warranties or representations as to the accuracy or completeness of third-party data contained herein. This document should be treated as confidential and for the use of the intended recipient only. Please notify 7 Mile Advisors if it was distributed in error. 2 Overview 7MA provides Investment Banking & Advisory Services to the Business Services and Technology Industries globally. We advise on M&A and private capital transactions, and provide market assessments and benchmarking. As a close knit team with a long history together and a laser focus on our target markets, we help our clients sell their companies, raise capital, grow through acquisitions, and evaluate new markets. We publish our sectorwatch, a review of M&A and operational trends in the industries we focus. Dashboard Valuation Comparison • Summary metrics on the sector • Graphical, detailed comparison of valuation • Commentary on market momentum by multiples for the public basket comparing the most recent 12-month performance against the last 3-year averages. -

Certified Actuarial Analyst (CAA) – a Truly Global Qualification Jane Curtis Institute and Faculty of Actuaries (Ifoa)

Certified Actuarial Analyst (CAA) – a truly global qualification Jane Curtis Institute and Faculty of Actuaries (IFoA) 30 April 2015 Refresher: what is the CAA? • Two IFoA membership categories (CAA and Student Actuarial Analyst - SAA) • 1 entry test (Module 0) and 5 exam modules – technical calculations and bookwork. Module 0 taken by non-members • Modules 0-4 delivered by Computer Based Assessment. Module 5 is a practical exam on spreadsheet modelling • Work based skills and professionalism requirements; ongoing regulation • Generic, not practice-area specific • c2-3 years part time to qualify 2 30 April 2015 Strategy: why did the IFoA develop the CAA? • Market demand: increasingly business models are built around a small number of high level experts supported by a greater number of technically skilled professional analysts • Professionalism: professionalising those working alongside actuaries and in broader financial services • Actuarial capacity building: in markets where there is a desire for industry growth at pace and at manageable cost • Relevance and affordability: Fellowship isn’t always the right choice but is sometimes the only choice • Accessibility: diversification of the profession; non-traditional entry routes 30 April 2015 3 Benefits: why the CAA? For candidates • membership of a globally recognised prestigious body • globally recognised, portable qualification • opens up a wide range of financial career options For employers • professionalises technical and analytical roles, providing additional assurance to clients and -

1 in the United States District Court for The

IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF MISSOURI JOSHUA SITZER, et al., ) ) Plaintiffs, ) ) v. ) Case No. 19-CV-00332-SRB ) THE NATIONAL ASSOCIATION OF ) REALTORS, et al., ) ) Defendants. ) NOTICE OF INTENT TO ISSUE SUBPOENA TO PRODUCE DOCUMENTS Pursuant to Fed. R. Civ. P. 45, Plaintiffs will request non-party witness Southern Missouri Regional MLS LLC to produce at Alaris Litigation; 2422 East Madrid Street; Springfield, Missouri 65804 on or before November 15, 2019 at 9:00 a.m., all documents and things in its possession, custody or control as specified in Exhibit A to the Subpoena. The Subpoena is attached hereto and incorporated herein as Exhibit 1. DATE: October 10, 2019 WILLIAMS DIRKS DAMERON LLC /s/ Matthew L. Dameron Matthew L. Dameron MO # 52093 Eric L. Dirks MO # 54921 Amy R. Jackson MO # 70144 Courtney M. Stout MO # 70375 1100 Main Street, Suite 2600 Kansas City, MO 64105 Tele: (816) 945-7110 Fax: (816) 945-7118 [email protected] [email protected] [email protected] [email protected] Brandon J.B. Boulware MO # 54150 Jeremy M. Suhr MO # 60075 1 Case 4:19-cv-00332-SRB Document 130 Filed 10/10/19 Page 1 of 2 Erin D. Lawrence MO # 63021 BOULWARE LAW LLC 1600 Genessee, Suite 416 Kansas City, MO 64102 Tele: (816) 492-2826 Fax: (816) 492-2826 [email protected] [email protected] [email protected] Attorneys for Plaintiffs CERTIFICATE OF SERVICE I certify that on this 10th day of October 2019, a true and correct copy of the foregoing was filed electronically via the Court’s CM/ECF system which sent electronic notification of such filing to all counsel of record. -

Join Us for an EXCLUSIVE VIDEO PAID PAID PRSRT PRSRT Phila, PA Phila, Phila, PA Phila, PRSRT STD PRSRT FIRST CLASS FIRST U.S

A Publication of Diversified Real Estate Investor Group August 2018 Learn how to Buy, Rehab & Refinance Properties Long Distance Join us for an EXCLUSIVE VIDEO PAID PAID PRSRT PRSRT Phila, PA Phila, Phila, PA Phila, PRSRT STD PRSRT FIRST CLASS FIRST U.S. POSTAGE U.S. Permit No. 5634 5634 No. Permit U.S. POSTAGE U.S. Permit No. 5634 5634 No. Permit BROCHURE POSTCARD IN THIS ISSUE: • NO MAIN MEETING IN AUGUST AT NORTH HILLS CC • IN LIEU OF MEETING EXCLUSIVE DIG VIDEO WITH AUTHOR DAVID GREENE ON “LONG DISTANCE REAL ESTATE INVESTING”. DETAILS ON PG. 6 • TAX BREAKS FOR INVESTING IN LOW-INCOME “OPPORTUNITY ZONES” PG. 20 In This Issue >> EXCLUSIVE VIDEO with David Greene, Author 6| of "Long Distance Real Estate Investing" MEMBER Dear Legislative 9| 19| 20| SPOTLIGHT Dr. DIG News Prepare Now For Slower 7|A Challenge to DIG Members 9| Growth, Consumer Headwinds 11|Upcoming Events 13|DIG Subgroups UPDATED: Online Home Value 17|Steals and Deals 21| Estimates Are NOT Appraisals 26|Unique Tenant Tricks Diversified Investor 3 Meet The Team >> Association Directors President Frank Nestore DIG Office Hours Vice-President Jon Owens Mon - Friday 9am - Noon Treasurer Raymond Lemire 1250 Bethlehem Pike, Ste. #391 Secretary Marc Sherby Hatfield, PA 19440 Executive Director Stephanie Pappas Phone: 215-712-2525 Email: [email protected] Office Administrator Elaine Kochanski Visit us at: www.digonline.org Diversified Real Estate www.diganswerline.org Investor Group is the leading regional association for Real Estate Investors in the Committee Members Metropolitan Philadelphia/ Delaware Valley Area. DIG is a Advertising/Marketplace Elaine Kochanski National REIA Chapter whose Vendors/Benefits Marc Sherby area includes the PA counties of Berks, Bucks, Chester, Education/Programs Don Beck Delaware, Lehigh, Montgomery, Facilities/AV/CD Sales Jon Owens Philadelphia and surrounding Membership Stephanie Pappas counties in South Jersey and Delaware. -

Boston San Francisco Munich London

Internet & Digital Media Monthly August 2018 BOB LOCKWOOD JERRY DARKO Managing Director Senior Vice President +1.617.624.7010 +1.415.616.8002 [email protected] [email protected] BOSTON SAN FRANCISCO HARALD MAEHRLE LAURA MADDISON Managing Director Senior Vice President +49.892.323.7720 +44.203.798.5600 [email protected] [email protected] MUNICH LONDON INVESTMENT BANKING Raymond James & Associates, Inc. member New York Stock Exchange/SIPC. Internet & Digital Media Monthly TECHNOLOGY & SERVICES INVESTMENT BANKING GROUP OVERVIEW Deep & Experienced Tech Team Business Model Coverage Internet / Digital Media + More Than 75 Investment Banking Professionals Globally Software / SaaS + 11 Senior Equity Research Technology-Enabled Solutions Analysts Transaction Processing + 7 Equity Capital Markets Professionals Data / Information Services Systems | Semiconductors | Hardware + 8 Global Offices BPO / IT Services Extensive Transaction Experience Domain Coverage Vertical Coverage Accounting / Financial B2B + More than 160 M&A and private placement transactions with an Digital Media Communications aggregate deal value of exceeding $25 billion since 2012 E-Commerce Consumer HCM Education / Non-Profit + More than 100 public equities transactions raising more than Marketing Tech / Services Financial $10 billion since 2012 Supply Chain Real Estate . Internet Equity Research: Top-Ranked Research Team Covering 25+ Companies . Software / Other Equity Research: 4 Analysts Covering 40+ Companies RAYMOND JAMES / INVESTMENT BANKING OVERVIEW . Full-service firm with investment banking, equity research, institutional sales & trading and asset management – Founded in 1962; public since 1983 (NYSE: RJF) – $6.4 billion in FY 2017 revenue; equity market capitalization of approximately $14.0 billion – Stable and well-capitalized platform; over 110 consecutive quarters of profitability . -

Realogy Holdings Corp

About Realogy Holdings Corp. Realogy Holdings Corp. (NYSE: RLGY) is the leading and most integrated provider of residential real estate services in the U.S. that is focused on empowering independent sales agents to best serve today’s consumers. Realogy delivers its services through its well-known industry brands including Better Homes and Gardens® Real Estate, CENTURY 21®, Climb Real Estate®, Coldwell Banker®, Coldwell Banker Commercial®, Corcoran Group®, ERA®, Sotheby's International Realty® as well as NRT, Cartus®, Title Resource Group and ZapLabs®, an in-house innovation and technology development lab. Realogy’s fully integrated business model includes brokerage, franchising, relocation, mortgage, and title and settlement services. Realogy provides independent sales agents access to leading technology, best-in-class marketing and learning programs, and support services to help them become more productive and build stronger businesses. Realogy’s affiliated brokerages operate around the world with approximately 193,600 independent sales agents in the United States and approximately 106,400 independent sales agents in 112 other countries and territories. Realogy is headquartered in Madison, New Jersey. Realogy Business Units • Realogy Franchise Group, (Madison, N.J.) the leading franchisor of real estate brokerages in the world, with leading brands, including: o Better Homes and Gardens® Real Estate o CENTURY 21® o Coldwell Banker® o ERA® o Sotheby’s International Realty® o Coldwell Banker Commercial® • NRT LLC, (Madison, N.J.) the largest owner and operator of residential real estate brokerages in the United States • Cartus Corporation, (Danbury, Conn.) a global leader in relocation services • Title Resource Group LLC, (Mt. Laurel, N.J.) a provider of title and other settlement services • ZapLabs LLC, (Emeryville, Calif.) innovation and technology development subsidiary Company Leadership Realogy Holdings Corp. -

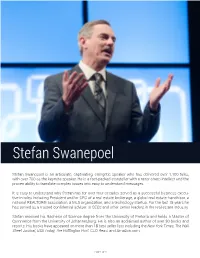

Stefan Swanepoel

Stefan Swanepoel Stefan Swanepoel is an articulate, captivating, energetic speaker who has delivered over 1,100 talks, with over 700 as the keynote speaker. He is a fact-packed storyteller with a razor-sharp intellect and the proven ability to translate complex issues into easy to understand messages. It is easy to understand why Stefan has for over four decades served as a successful business execu- tive in roles including President and/or CEO of a real estate brokerage, a global real estate franchisor, a national REALTOR® association, a MLS organization, and a technology startup. For the last 15 years he has served as a trusted confidential adviser to CEOs and other senior leaders in the real estate industry. Stefan received his Bachelor of Science degree from the University of Pretoria and holds a Master of Commerce from the University of Johannesburg. He is also an acclaimed author of over 30 books and reports. His books have appeared on more than 18 best seller lists including the New York Times, The Wall Street Journal, USA Today, The Huffington Post, CEO Read, and Amazon.com. PAGE 1 OF 3 Speaking Topics Digital Disruption The Technology Transformation of the Real Estate Business 90 Minutes | Large Screen | Opening Sessions Many speakers teach technology but few bring both a dynamic strategic vision of where it’s going along with a practical nuts and bolts understanding of its application and potential in the real estate space as does Swanepoel. This high tech-high touch video rich presentation will keep you at the edge of your chair from beginning to end. -

Competing with New Business Models • Your Job: Clarify the Future • Trends in Property Portals Worldwide • Age of Amazon: Lesson 5 People Vs

COMPLIMENTS OF JUNE 2018 NEWSLETTER Subscribe Today—Free! ACTION PLAN REAL TRENDS COMPETING WITH NEW CONTENT SITE Get information on the BUSINESS MODELS topics you want; when you want it with our new, New business models will keep you on your toes, By Steve Murray, president customized content site. but complaining won’t get you anywhere. Find videos, podcasts, The onslaught of new venture-backed realty that there are at least four private equity insightful trend articles firms entering the industry is somewhat firms—that we are aware of—carefully and more. breathtaking. Along with Redfin, Compass examining investment options in brokerage and eXp, we have Open Door, Offer Pad, and real estate tech. Knock.com, Purple Bricks and others not so To Subscribe: well known. Zillow, Realtor.com, Homes.com It’s not that there are so many new entries and myriad other real estate tech firms have that is causing angina among incumbent CLICK HERE also had an impact. What is less known is realty firms. It’s that they compete by 1-6 FIRST PERSON • Analysis of RT’s Market Leaders Report 30 GLOBAL • Competing with New Business Models • Your Job: Clarify the Future • Trends in Property Portals Worldwide • Age of Amazon: Lesson 5 People vs. • Brokerage Social Responsibility 31-32 TECHNOLOGY Product 22-27 MARKET • The Impact of Technology • Are We Picking Convenience Over • 20 Percent of Homes are Undervalued • Books Worth Reading Security? • CoreLogic Reports Declining Foreclosure Rates • The Value Exchange • Showing Activity at Near-Record Levels 33 PUBLISHER’S 7-21 BROKERAGE 28-29 REGULATORY NOTE • 3 Market Factors Impacting Commissions 1 • Mulvaney Presents His CFPB Vision • Recruit, Develop & Spend Less offering lower costs to consumers, higher costs to recruit and retain agents or both.