DEAN FOODS CO Form 10-K Annual Report Filed 2019-02-28

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ims List Sanitation Compliance and Enforcement Ratings of Interstate Milk Shippers April 2017

IMS LIST SANITATION COMPLIANCE AND ENFORCEMENT RATINGS OF INTERSTATE MILK SHIPPERS APRIL 2017 U.S. Department of Health and Human Services Public Health Service Food and Drug Administration Rules For Inclusion In The IMS List Interstate milk shippers who have been certified by State Milk sanitation authorities as having attained the milk sanitation compliance ratings are indicated in the following list. These ratings are based on compliance with the requirements of the USPHS/FDA Grade A Pasteurized Milk Ordinance and Grade A Condensed and Dry Milk Products and Condensed and Dry Whey and were made in accordance with the procedures set forth in Methods of Making Sanitation Rating of Milk Supplies. *Proposal 301 that was passed at 2001 NCIMS conference held May 5-10, 2001, in Wichita, Kansas and concurred with by FDA states: "Transfer Stations, Receiving Stations and Dairy Plants must achieve a sanitation compliance rating of 90 or better in order to be eligible for a listing in the IMS List. Sanitation compliance rating scores for Transfer and Receiving Stations and Dairy Plants will not be printed in the IMS List". Therefore, the publication of a sanitation compliance rating score for Transfer and Receiving Stations and Dairy Plants will not be printed in this edition of the IMS List. THIS LIST SUPERSEDES ALL LISTS WHICH HAVE BEEN ISSUED HERETOFORE ALL PRECEDING LISTS AND SUPPLEMENTS THERETO ARE VOID. The rules for inclusion in the list were formulated by the official representatives of those State milk sanitation agencies who have participated in the meetings of the National Conference of Interstate Milk Shipments. -

Dean Foods Company (Exact Name of Registrant As Specified in Its Charter)

The goodness of dairy 2015 Annual Report 42805 Merrill_Cover_A240821.indd 3 3/24/16 11:20 PM Dear Fellow Stockholders: 2015 was a year of substantial success and accomplishments and I’m excited to share with you our progress from the past year. We exited the year with great financial results and entered 2016 with significant momentum. It was a year where we accomplished several of our previous goals and we continue to sharpen our focus. Financially, 2015 was a year of opportunity. • We experienced significant improvement • We returned approximately $79 million in our P&L. in cash to our shareholders in the form of • We improved our liquidity, extended debt dividends and share repurchases. maturities and increased flexibility with • We generated strong free cash flow of modified debt facilities providing up to approximately $246 million. $1 billion in liquidity. • We invested approximately $163 million in • We fortified our balance sheet with total our business through capital expenditures. leverage declining over two full turns in 2015 to 1.89 net debt to EBITDA. DairyPure® was the big news of the year. The April 2015 launch of our national white milk brand is off to a great start. Consumers are telling us they’re asking for DairyPure by name and that the 5 Point Purity Promise™ is important to them when making their choice for their family’s milk. We expect great things from DairyPure and are looking forward to sharing more news with you next year. Expansion of the DairyPure brand With the successful launch of DairyPure, one national brand endorsed by our local brands, Dean Foods is embarking on the expansion of DairyPure products: • School milk has transitioned to DairyPure, allowing our youngest consumers to have the daily opportunity to drink our milk at school. -

EXHIBIT ITEM 1 SMA010 Proponent Cooperatives

EXHIBIT ITEM 1 SMA010 Proponent Cooperatives February 2004 Arkansas Dairy Cooperative Association, Inc. Floyd Wiedower, Manager P.O. Box 507 Damascus, Arkansas 72039 501-335-7204 501-335-7705 fax Dairy Farmers of America, Inc. Gary Hanman, Pres. & CEO P.O. Box 909700 Kansas City, Missouri 64190 816-801-6422 816-801-6423 fax Dairymen's Marketing Cooperative, Inc. Don Allen, General Manager 421 East State Street Mountain Grove, Missouri 65711 417-962-7460 417-962-6159 fax Lone Star Milk Producers, Inc. Jim Baird, Manager Route 1, Box 59B Windthorst, Texas 76389 940-378-2311 940-378-2751 fax Maryland & Virginia Milk Producers Cooperative Association, Inc. Jay Bryant, General Manager 1985 Isaac Newton Square West Reston, Virginia 20190 703-742-6800 703-742-7459 fax Southeast Milk, Inc. Calvin Covington, CEO P.O. Box 3790 Belleview, Florida 34421 352-245-2~,37 352-245-9434 fax EXHIBIT ITEM 2 SMA020 Producer Milk Deliveries Proponent Cooperatives and Others November 2003 F.O. 5 F.O. 7 Combined Total Order Producer Milk 507,412,336 593,836,792 1,101,249,128 Member Producer Milk Arkansas Dairy Coop. 13,933,382 13,933,382 Dairy Farmers of America 222,978,642 319,174,550 542,153,192 Dairymen's Marketing Coop. 6,235,057 6,235,057 Lone Star Milk Prod. 16,453,108 34,839,125 51,292,233 MD & VA Milk Prod. 80,473,502 22,119,702 102,593,204 / Southeast Milk 17,401,087 17,401,087 Tota___/I 319,905,252 413,702,903 733,608,155 Percent of Order Total 63.046% 69.666% 66.616% Other Cooperative Producer Milk Marketed Arkansas Dairy Coop. -

Federal Milk Order Distributing Plant Information for 2019 NOTE: "DIP" Indicates Debtor in Possession

Federal Milk Order Distributing Plant Information For 2019 NOTE: "DIP" indicates debtor in possession Pool Distributing Plants State County Plant Name City State ZipCode FIPS FIPS Cl. I Dftl. Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Agropur Grand Rapids MI 49548 26 081 1.80 33 33 33 33 33 33 33 33 33 33 33 33 Agropur Maplewood MN 55113 27 123 1.70 30 30 30 30 30 30 30 30 30 30 Alpenrose Dairy Portland OR 97298 41 051 1.90 124 124 124 124 124 124 124 124 124 124 124 124 Andersen Dairy Battle Ground WA 98604 53 011 1.90 124 124 124 124 124 124 124 124 124 124 124 124 Anderson-Erickson Dairy Des Moines IA 50317 19 153 1.80 32 32 32 32 32 32 32 32 32 32 32 32 Aurora Organic Dairy Platteville CO 80651 08 123 2.45 32 32 32 32 32 32 32 32 32 32 32 32 Blue Kingfisher dba Walmart Fort Wayne IN 46819 18 003 1.80 33 33 33 33 33 33 33 33 33 33 33 33 Boice Brothers Dairy Kingston NY 12401 36 111 2.80 1 1 1 1 1 1 1 1 Borden Dairy Cowarts AL 36321 01 069 4.30 7 7 7 7 7 7 7 7 7 7 7 7 Borden Dairy Miami FL 33164 12 025 6.00 6 6 6 6 6 6 6 6 6 6 6 6 Borden Dairy Winter Haven FL 33881 12 105 5.40 6 6 6 6 6 6 6 6 6 6 6 6 Borden Dairy London KY 40743 21 125 2.90 5 5 5 5 5 5 5 5 5 5 5 5 Borden Dairy Lafayette LA 70596 22 055 3.80 7 7 7 7 7 7 7 7 7 7 7 7 Borden Dairy Hattiesburg MS 39404 28 035 3.80 7 7 7 7 7 7 7 7 7 7 7 7 Borden Dairy Cincinnati OH 45215 39 061 2.20 33 33 33 33 33 33 33 33 33 33 33 33 Borden Dairy Cleveland OH 44111 39 035 2.00 33 33 33 33 33 33 33 33 33 33 33 33 Borden Dairy Charleston SC 29419 45 019 4.30 5 5 5 5 5 5 5 5 5 5 5 5 Borden Dairy Austin TX 78702 48 453 3.30 126 126 126 126 126 126 126 126 126 126 126 126 Borden Dairy Conroe TX 77305 48 339 3.60 126 126 126 126 126 126 126 126 126 126 126 126 Borden Dairy Dallas TX 75221 48 113 3.00 126 126 126 126 126 126 126 126 126 126 126 126 Braum's Tuttle OK 73089 40 051 2.60 32 32 32 32 32 32 32 32 32 32 32 32 Broadacre Dairies Powell TN 37849 47 093 3.20 5 5 5 5 5 5 5 5 5 5 5 5 Byrne Dairy Syracuse NY 13220 36 067 2.50 1 1 1 1 1 1 1 1 1 1 1 C. -

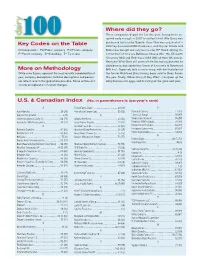

Key Codes on the Table More on Methodology Where Did They

Where did they go? Three companies depart the list this year, having been ac- quired early enough in 2007 to not be listed. Alto Dairy was Key Codes on the Table purchased last year by Saputo, Cass Clay was acquired at in 2007 by Associated Milk Producers, and Crystal Cream and C=Cooperative Pu=Public company Pr=Private company Butter was bought out early last year by HP Hood. Joining the P=Parent company S=Subsidiary T= Tie in rank list for the first time are BelGioso Cheese (No. 75), Ellsworth Creamery (84) and Roth Kase USA (96) all from Wisconsin. Next year Winn-Dixie will come off the list, having divested its dairy processing capabilities (some of it recently to Southeast More on Methodology Milk Inc.). Supervalu tells a similar story, with the final plant of While sales figures represent the most recently completed fiscal the former Richfood Dairy having been sold to Dean Foods year, company descriptions, facilities descriptions and person- this year. Finally, Wilcox Dairy of Roy, Wash., has given up the nel reflect recent changed where possible. Some entries will dairy business for eggs, and its listing will be gone next year. include an explanation of recent changes. U.S. & Canadian Index (No. in parentheses is last year’s rank) A Foster Farms Dairy ....................................... 50 (48) P Agri-Mark Inc. .............................................. 29 (29) Friendly Ice Cream Corp. ...............................55 (56) Parmalat Canada .........................................12 (13) Agropur Cooperative .........................................6 (9) G Perry’s Ice Cream ........................................ 97 (97) Anderson Erickson Dairy Co. ......................... 66 (71) Glanbia Foods Inc. ........................................ 23 (32) Plains Dairy Products ....................................95 (99) Associated Milk Producers Inc. -

Milkweed May 2006 Salvage

The Milkweed “Float like a butterfly, Dairy’s best information and insights sting like a bee.” Issue No. 475 • February 2019 This issue mailed on February 13 — Muhammad Ali Lost Export Markets Boost U.S. Cheese Inventories & Erode Prices by Jan Shepel focus on American-style cheeses, which include Cheese inventories in warehouses across the Cheddar – dairy’s price-setting benchmark variety. United States were being lowered in the early part of American cheese inventories started last year 2018, but after retaliatory tariffs were imposed by below 2017 levels – a perceived good indicator for trading partners late in 2018’s second quarter, those rising milk prices in the country. American cheese inventories jumped to levels significantly above year- inventories climbed less dramatically than in the pre- earlier levels. vious year, up to a July peak. American cheese in- The critical data for cheese inventories must ventories then dipped in August, before rising significantly above 2017 levels through November, Table 1 which is the last month for which data was available. Inventory numbers for 2014, 2015 and 2016 Cheese Inventories Versus were well below both 2017 and 2018 for the entire Exports After Tariffs year. In terms of total U.S. cheese production, 2018 data shows the numbers to be higher throughout the 2017 2018 year than all of those preceding years. But that’s not (Mill. lbs) (Mill. lbs) necessarily a a problem – due to solid, demand-driven output gains posted by Mozzarella and pizza cheese Jan. 752 740 during 2018. Comparing total January production in Roundup® herbicide’s active ingredient is Feb. -

APPALACHIAN MARKETING AREA Federal Order No. 5 HANDLERS and PLANTS SUBJECT to FEDERAL ORDER NO

TABLE 19 APPALACHIAN MARKETING AREA Federal Order No. 5 HANDLERS AND PLANTS SUBJECT TO FEDERAL ORDER NO. 5 - 2003 Pool Distributing Plants - Sec. 1005.7(a) JFMAMJJASOND Broadacre Dairies P.O. Box 650 xxxxxxxxxxxx Powell, TN 37849 Chattanooga Dairy, LLC 3411 Vinewood Ave. xx Chattanooga, TN 37416 Coburg Dairy, LLC P.O. Box 63448 xxxxxxxxxxxx Charleston, SC 29419-3448 Dairy Fresh, LLC P.O. Box 4009 xxxxxxxxxxxx Winston-Salem, NC 27115-4009 Dean Foods Company 4420 Bishop Lane xxxxxxxxxxxx Louisville, KY 40218-4506 Flav-O-Rich, Inc. P.O. Box 40 xxxxxxxxxxxx London, KY 40743-0040 Golden Gallon, LLC P. O. Box 181600 xxxxxxxxxx Chattanooga, TN 37416-7600 Hoosier Dairy, Inc. P. O. Box 70 xxxxxxxxxxxx Holland, IN 47541-0070 Hunter Farms, Inc. 1900 North Main St. xxxxxxxxxxxx High Point, NC 27262 Ideal American Dairy P. O. Box 4038 xxxxxxxxxxxx Evansville, IN 47724-0038 Land-O-Sun Dairies, Inc. P.O. Box 12860 xxxxxxxxxxxx Florence, SC 29504-2860 Land-O-Sun Dairies, Inc. DBA Pet Dairy xxxxxxxxxxxx P.O. Box 1349 Kingsport, TN 37662-1349 Land-O-Sun Dairies, Inc. DBA Pet Dairy xxxxxxxxxxxx P.O. Box 4527, Station B Spartanburg, SC 29305-4527 Land-O-Sun Dairies, Inc. 103 North Cherry St. xxxxxxxxxxxx Wilkesboro, NC 28697 Maola Milk and Ice Cream Co. P.O. Drawer S xxxxxxxxxxxx New Bern, NC 28560-3113 JFMAMJJASOND Mayfield Dairy Farms, Inc. P.O. Box 310 xxxxxxxxxxxx Athens, TN 37371-0310 Milkco, Inc. P.O. Box 16160 xxxxxxxxxxxx Asheville, NC 28816-0160 Regis Milk Co. 578 Meeting St. xxxxxxxxxxxx Charleston, SC 29403-4537 Southern Belle Dairy, Inc. -

Handlers and Plants Subject to Federal Order No

TABLE 19 APPALACHIAN MARKETING AREA Federal Order No. 5 HANDLERS AND PLANTS SUBJECT TO FEDERAL ORDER NO. 5 - 2006 Pool Distributing Plants - Sec. 1005.7(a) JFMAMJJASOND Broadacre Dairies P.O. Box 650 xxxxxxxxxxxx Powell, TN 37849-0650 Chattanooga Dairy, LLC 3411 Vinewood Drive xxxxx Chattanooga, TN 37406 Coburg Dairy, LLC P.O. Box 63448 xxxxxxxxxxxx North Charleston, SC 29419-3448 Dairy Fresh 2221 Patterson Avenue xxxxxxxxxxxx Winston-Salem, NC 27105-6036 Dairy Fresh 1350 West Fairfield Road xxxxxxxx High Point, NC 27264 Dean Foods Company 4420 Bishop Lane xxxxxxxxxxxx Louisville, KY 40218-4506 Flav-O-Rich, Inc. P.O. Box 40 xxxxxxxxxxxx London, KY 40743-0040 Homestead Creamery P.O. Box 506 xxxxxxxxxxxx Wirtz, VA 24184 Hoosier Dairy, Inc. P. O. Box 70 xxxxxxxxxxxx Holland, IN 47541-0070 Hunter Farms, Inc. P.O. Box 5148 xxxxxxxxxxxx High Point, NC 27262 Land-O-Sun Dairies, Inc. P.O. Box 12860 xxxxxxxxxxxx Florence, SC 29504-2860 Land-O-Sun Dairies, Inc. DBA Pet Dairy xxxxxxxxxxxx P.O. Box 1349 Kingsport, TN 37662-1349 Land-O-Sun Dairies, Inc. DBA Pet Dairy xxxxxxxxxxxx P.O. Box 4527, Station B Spartanburg, SC 29305-4527 Maola Milk and Ice Cream Co. P.O. Drawer S xxxxxxxxxxxx New Bern, NC 28560-3113 Mayfield Dairy Farms, Inc. P.O. Box 310 xxxxxxxxxxxx Athens, TN 37371-0310 Appalachian Marketing Area - 1 - JFMAMJJASOND Milkco, Inc. P.O. Box 16160 xxxxxxxxxxxx Asheville, NC 28816-0160 Regis Milk Co. 578 Meeting St. xxxxxxxxxxxx Charleston, SC 29403-4537 Southern Belle Dairy, Inc. P. O. Box 1020 xxxxxxxxxxxx Somerset, KY 42502-1020 U. -

Dairy 100 Table.Qxp

dairy SALES SALES COMPANY LOCATION DAIRY EXECUTIVE TYPE PARENT CO./SUBSIDIARIES FY END ‘05 ‘04 1. Dean Foods Co. Dallas, TX Gregg Engles, Chairman/CEO Pu S-Dean Dairy Group, WhiteWave Foods 12/31/05 10,106 9835^ Brands: Alta Dena, Barbe's, Barbers, Berkeley Farms, Borden (licensed), Broughton, Brown's, Country Charm, Country Churn, Country Delite, Country Fresh, Country Love, Creamland, Dairy Fresh, Dean's, Foremost (licensed), Fieldcrest, Garelick Farms, Gandy's, Hershey’s (licensed), Horizon Organic, Hygeia, Imo, International Delight, Kohler, Land O'Lakes (licensed), Lehigh Valley, Louis Trauth, Maplehurst, Mayfield, McArthur, Meadowbrook, Meadow Gold, Melody Farms, Mile High, Model, Mountain High, Nature's Pride, Oak Farms, PET (licensed), Price's, Purity, Reiter, Robinson, Saunders, Sealtest (licensed), Schenkel's All Star, Schepps, Shenandoah's Pride, Silk, Skinny Cow, Sealtest (licensed), Stroh's, Swiss, Swiss Premium, The Organic Cow, TG Lee, Tuscan, Verifine, Viva, Wengert's, White Wave. Plants (104): (by state): Alabama: Barber Dairy, Birmingham (milk); Mayfield Dairy Farms, Birmingham (novelties); Milk Products of Alabama, Decatur, (milk, ice cream and shake mixes); California: Dean Foods, Buena Park (multiple products); City of Industry; Gustine (Morningstar); Alta Dena Dairy, City of Industry (milk, juice/drinks ice cream); Fullerton Cultured Specialties, Fullerton (yogurt); Berkeley Farms, Hayward (milk, cream, fresh whipped cream) Swiss Dairy, Riverside (juice/drinks); Tulare Cultured Specialties, Tulare (cultured); Colorado: Meadow Gold, Englewood, Denver, Delta, Greeley (multiple products); Mile High Ice Cream, Denver (ice cream); Robinson Dairy, Denver (multiple products); Connecticuit: Kohler, Newington; Florida: McArthur Dairy, Miami (fluid); TG Lee, Orange City (juice/drinks, yogurt); TG Lee, Orlando (milk); Ryan Foods, Jacksonville. -

End User List a Brand of Max-Air Technology

End User List A Brand of Max-Air Technology. Food & Beverage Industry 21st Century Foods Cherrydale Farms Glades Pike Winery Mar-Key Foods Poland Springs Water Ventura Foods Absopure Water Co. Chiquita Goetze Candy Co. Maui Pineapple Co. Prairie Farms Vermont Pure Springs ACH Foods Classic Caramel Gold Kist Maxfield Candy Co. Preferred Meal Systems Vitality Beverage Co. Adair Food Co. Clausen Koch Golden Farm Foods Mayfield Dairy Premium Beverage Company Vitasoy Adell Whey Cliffstar Foods Golden State Foods McCall Farms Progresso Quality Foods Walden Springs Water Co. Advanced Food Products Clover Club Bottling Golden Valley Microwave McCormick Distillers Purity Dairy Wallaby Yogurt Co. Advanced Meats Clover Farms Dairy Co. Golden West Foods McDonald Dairy Division Quaker Oats Wayne Farms Advantage Nutritional Clovervale Foods Goldenberg Candy Co. McKesson Water Products Quality Baking Company Weaver Popcorn Agri Mark Dairy Coca-Cola Gonnelia Baking Co. Meijer Central Kitchen Quantum Foods Wengert’s Dairy Albertville Quality Foods Coloma Frozen Food Good Foods Menu Foods Quest Flavors International Western Country Pie Ale-8-One Colteryahn Dairy Good Humor – Breyers Miceli Dairy Products Ralston Foods White Wave, Inc. Algood Foods Co. Con Agra Dairy Foods Graceland Fruit Inc. Michael Foods Reckitt-Benckiser Wick’s Pies Allen Canning Co. Con Agra Food Ingredients Great Lakes Brewing Co. Michigan City Baking Red Giant Foods Wilburn Chocolate Alpha Baking Co. Con Agra Foods Great Lakes Cheese Michigan Milk Products Assoc. Red Gold Wild Coyote Foods Alpine Cheese Co. Con Agra Frozen Foods Guggisberg Cheese Milk Products of Alabama Reiter Dairy Wildwood Harvest America’s Kitchen Con Agra Grocery Products H.B. -

DEAN FOODS COMPANY Last Updated:01/30/2017 - 02:06:30 AM

Created on : 01/30/2017 04:58:14 PM © FEDMINE™ All Rights Reserved FEDMINE™ Prime Contractor Company Profile - DEAN FOODS COMPANY Last Updated:01/30/2017 - 02:06:30 AM Note 1: If a Parent company for this enty is reported, click the link on its Parent DUNS number below to see its consolidated Profile. Parent subsidiary relaonships are no longer provided due to the Federal Government's agreement with D&B, and therefore, some relaonships may not reflect the most current status in our system. Note 2: All O BLIGATED DO LLARS PERTAIN TO PRIME CO NTRACTING DO LLARS O NLY. IF PURCHASED SEPARATELY SUBCO NTRACTS DATA IS INCLUDED IN ALL PRO FILES. View Profile by subsidiaries Contract Awards in Last 30 Days Contracts by Place of Performance Contracts By Contracng Off. FedBizOpps Awards Contracts by NAICS Codes Contracts by PSC Codes Contracts by Categories Contracts By Socio Economic Status Contracts By SetAside Type Contracts By Pricing Type Contracts By Extent of Compeon ORGANIZATION DETAILS COMPARATIVE 8 - YEAR FEDERAL PRIME CONTRACTS VIEW DUNS: 929182210 Expenditures By year Parent DUNS: NONE 40 Fedmine ID: F060256623 Address: 2711 N HASKELL AVE STE 3400 30 DALLAS TX 75204-2928 USA 20 County Code: 113 Cong. District: 32 10 Metro Area Code: 0000 Organizaon Type: CORPORATE ENTITY (NOT TAX EXEMPT) 0 2010 2011 2012 2013 2014 2015 2016 2017 2L fedmine.us Incorporaon: TX Top Federal Agencies (2010-2017) Legal Structure: Business Type: 2X - For-Profit Organizaon LJ - Limited Liability Company MF - Manufacturer of Goods VW - Contracts and Grants Employees: -

Compilation of Statistical Material and Requested Data

COMPILATION OF STATISTICAL MATERIAL AND REQUESTED DATA FEDERAL MILK ORDER NO. 1 NORTHEAST MARKETING AREA Prepared by: For Use in Public Hearing Market Administrator’s Office Docket No. AO-14-A70; DA-02-01 30 Winter Street Alexandria, VA Boston, MA 02108 September 2002 TABLE OF CONTENTS Northeast Marketing Area–Federal Order 1 Page No. Receipts of Producer Milk, by State, 2000–2002..............................................................................................................1 Number of Producers, by State, 2000–2002.....................................................................................................................2 Daily Average Output of Producer Milk per Farm, by State, 2000–2002..........................................................................3 Producer Prices and Producer Production Summary, January 2000–July 2002..............................................................4 Producer Receipts, by Classification, January 2000–July 2002.......................................................................................5 Class I, II, III, and IV Prices and Advanced Pricing Factors at Suffolk County, MA (Boston), January 2000–September 2002 ...................................................................................................................................6 Plant Classification Information, January 2000–July 2002 ...............................................................................................7 Cooperatives with Producers Pooled on the Northeast Order, July 2002 ......................................................................19