Annual Report 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DXE Liquidity Provider Registered Firms

DXE Liquidity Provider Program Registered Securities European Equities TheCboe following Europe Limited list of symbols specifies which firms are registered to supply liquidity for each symbol in 2021-09-28: 1COVd - Covestro AG Citadel Securities GCS (Ireland) Limited (Program Three) DRW Europe B.V. (Program Three) HRTEU Limited (Program Two) Jane Street Financial Limited (Program Three) Jump Trading Europe B.V. (Program Three) Qube Master Fund Limited (Program One) Societe Generale SA (Program Three) 1U1d - 1&1 AG Citadel Securities GCS (Ireland) Limited (Program Three) HRTEU Limited (Program Two) Jane Street Financial Limited (Program Three) 2GBd - 2G Energy AG Citadel Securities GCS (Ireland) Limited (Program Three) Jane Street Financial Limited (Program Three) 3BALm - WisdomTree EURO STOXX Banks 3x Daily Leveraged HRTEU Limited (Program One) 3DELm - WisdomTree DAX 30 3x Daily Leveraged HRTEU Limited (Program One) 3ITLm - WisdomTree FTSE MIB 3x Daily Leveraged HRTEU Limited (Program One) 3ITSm - WisdomTree FTSE MIB 3x Daily Short HRTEU Limited (Program One) 8TRAd - Traton SE Jane Street Financial Limited (Program Three) 8TRAs - Traton SE Jane Street Financial Limited (Program Three) Cboe Europe Limited is a Recognised Investment Exchange regulated by the Financial Conduct Authority. Cboe Europe Limited is an indirect wholly-owned subsidiary of Cboe Global Markets, Inc. and is a company registered in England and Wales with Company Number 6547680 and registered office at 11 Monument Street, London EC3R 8AF. This document has been established for information purposes only. The data contained herein is believed to be reliable but is not guaranteed. None of the information concerning the services or products described in this document constitutes advice or a recommendation of any product or service. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Corporate Non-Financial Reporting in Germany

Copyright © Development International e.V., 2019 ISBN: 978-3-9820398-1-7 Authors: Chris N. Bayer, PhD Gisella Vogel Sarah Kaltenhäuser Katherine Storrs Jiahua (Java) Xu, PhD Juan Ignacio Ibañez, LL.M. Title: A New Responsibility for Sustainability: Corporate Non-Financial Reporting in Germany Date published: May 6, 2019 Funded by: iPoint-systems gmbh www.ipoint-systems.com Executive Summary Germany's economy is the fourth-largest in the world (by nominal GDP), and with 28% of the euro area market, it represents the largest economy in Europe.1 Considering the supply chains leading to its economy, Germany's cumulative environmental, social and governance performance reverberates globally. The EU Non-Financial Reporting Directive (NFRD) is the impetus behind this study – a new regulation that seeks to “increase the relevance, consistency and comparability of information disclosed by certain large undertakings and groups across the Union.”2 Large undertakings in EU member states are not only required to report on their financial basics, now they are also required by Article 1 of the Directive to account for their non- financial footprint, including adverse impacts they have on the environment and supply chains. In accordance with the Directive, the German transposition stipulates that the non-financial declaration must state which reporting framework was used to create it (or explain why no framework was applied), as well as apply non-financial key performance indicators relevant to the particular business. These requirements are our point of departure: We systematically assess the degree of non-financial transparency and performance reporting for 2017 applying an ex-post assessment framework premised on the Global Reporting Initiative (GRI), the German Sustainability Code (Deutscher Nachhaltigkeitskodex, DNK) and the United Nations Global Compact (UNGC). -

The Financialisation of Big Tech

Engineering digital monopolies The financialisation of Big Tech Rodrigo Fernandez & Ilke Adriaans & Tobias J. Klinge & Reijer Hendrikse December 2020 Colophon Engineering digital monopolies The financialisation of Big Tech December 2020 Authors: Rodrigo Fernandez (SOMO), Ilke Editor: Marieke Krijnen Adriaans (SOMO), Tobias J. Klinge (KU Layout: Frans Schupp Leuven) and Reijer Hendrikse (VUB) Cover photo: Geralt/Pixabay With contributions from: ISBN: 978-94-6207-155-1 Manuel Aalbers and The Real Estate/ Financial Complex research group at KU Leuven, David Bassens, Roberta Cowan, Vincent Kiezebrink, Adam Leaver, Michiel van Meeteren, Jasper van Teffelen, Callum Ward Stichting Onderzoek Multinationale The Centre for Research on Multinational Ondernemingen Corporations (SOMO) is an independent, Centre for Research on Multinational not-for-profit research and network organi- Corporations sation working on social, ecological and economic issues related to sustainable Sarphatistraat 30 development. Since 1973, the organisation 1018 GL Amsterdam investigates multinational corporations The Netherlands and the consequences of their activities T: +31 (0)20 639 12 91 for people and the environment around F: +31 (0)20 639 13 21 the world. [email protected] www.somo.nl Made possible in collaboration with KU Leuven and Vrije Universiteit Brussel (VUB) with financial assistance from the Research Foundation Flanders (FWO), grant numbers G079718N and G004920N. The content of this publication is the sole responsibility of SOMO and can in no way be taken to reflect the views of any of the funders. Engineering digital monopolies The financialisation of Big Tech SOMO Rodrigo Fernandez, Ilke Adriaans, Tobias J. Klinge and Reijer Hendrikse Amsterdam, December 2020 Contents 1 Introduction .......................................................................................................... -

Global Voting Activity Report to March 2019

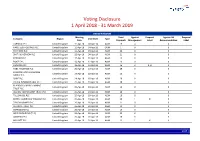

Voting Disclosure 1 April 2018 - 31 March 2019 UNITED KINGDOM Meeting Total Against Proposal Against ISS Proposal Company Region Vote Date Type Date Proposals Management Label Recommendation Label CARNIVAL PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 19 0 0 HANSTEEN HOLDINGS PLC United Kingdom 11-Apr-18 04-Apr-18 OGM 1 0 0 RIO TINTO PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 22 0 0 SMITH & NEPHEW PLC United Kingdom 12-Apr-18 04-Apr-18 AGM 21 0 0 PORVAIR PLC United Kingdom 17-Apr-18 10-Apr-18 AGM 15 0 0 BUNZL PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 19 0 0 HUNTING PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 16 2 3, 8 0 HSBC HOLDINGS PLC United Kingdom 20-Apr-18 13-Apr-18 AGM 29 0 0 LONDON STOCK EXCHANGE United Kingdom 24-Apr-18 18-Apr-18 AGM 26 0 0 GROUP PLC SHIRE PLC United Kingdom 24-Apr-18 18-Apr-18 AGM 20 0 0 CRODA INTERNATIONAL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 18 0 0 BLACKROCK WORLD MINING United Kingdom 25-Apr-18 19-Apr-18 AGM 15 0 0 TRUST PLC ALLIANZ TECHNOLOGY TRUST PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 10 0 0 TULLOW OIL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 16 0 0 BRITISH AMERICAN TOBACCO PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 20 1 8 0 TAYLOR WIMPEY PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 21 0 0 ALLIANCE TRUST PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 13 0 0 SCHRODERS PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 19 0 0 WEIR GROUP PLC (THE) United Kingdom 26-Apr-18 20-Apr-18 AGM 23 0 0 AGGREKO PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 20 0 0 MEGGITT PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 22 1 4 0 1/47 -

DWS Equity Funds Semiannual Reports 2010/2011

DWS Investment GmbH DWS Equity Funds Semiannual Reports 2010/2011 ■ DWS Deutschland ■ DWS Investa ■ DWS Aktien Strategie Deutschland ■ DWS European Opportunities ■ DWS Intervest ■ DWS Akkumula : The DWS/DB Group is the largest German mutual fund company according to assets under management. Source: BVI. As of: March 31, 2011. 4/2011 DWS Deutschland DWS Investa DWS Aktien Strategie Deutschland DWS European Opportunities DWS Intervest DWS Akkumula Contents Semiannual reports 2010/2011 for the period from October 1, 2010, through March 31, 2011 (in accordance with article 44 (2) of the German Investment Act (InvG)) TOP 50 Europa 00 General information 2 Semiannual reports 2010 DWS Deutschland 4 DWS Investa 10 2011 DWS Aktien Strategie Deutschland 16 DWS European Opportunities 22 DWS Intervest 28 DWS Akkumula 36 1 General information Performance ing benchmarks – if available – are also b) any taxes that may arise in connec- The investment return, or performance, presented in the report. All financial tion with administrative and custodial of a mutual fund investment is meas - data in this publication is as of costs; ured by the change in value of the March 31, 2011. c) the costs of asserting and enforcing fund’s units. The net asset values per the legal claims of the investment unit (= redemption prices) with the addi- Sales prospectuses fund. tion of intervening distributions, which The sole binding basis for a purchase are, for example, reinvested free of are the current versions of the simpli- The details of the fee structure are set charge within the scope of investment fied and the detailed sales prospec - forth in the current detailed sales accounts at DWS, are used as the basis tuses, which are available from DWS, prospectus. -

Volume IX, Issue 1 Logistics Solutions for Telecom Professionals

Volume IX, Issue 1 walkerfirst.com/skinny-wire Logistics Solutions for Telecom Professionals Supercharged Ethernet Services Comprehensive Carrier Ethernet Solutions that Strike the Right Balance Fujitsu Carrier Ethernet solutions combine our FLASHWAVE® 5300 Ethernet Access and Aggregation Devices with the FLASHWAVE 7120 packet optical platform and the NETSMART 1200 Management System. The result is a truly efficient, economical Ethernet growth path, balanced with seamless operation and management. But that’s not all. These solutions offer dramatically increased service velocity, together with carrier- grade reliability and performance. If you’re planning to service high-value SLAs or 4G/LTE mobile backhaul, ask your Walker representative about supercharging your network with profitable Ethernet services using Fujitsu FLASHWAVE-based MEF-compliant Ethernet platforms. FLASHWAVE 5300 SERIES • GbE and 10 GbE interfaces • MEF E-Line, E-LAN and E-Access services • Class of service differentiation, shaping and policing • Performance monitoring with ITU-T Y.1731 • Ethernet ring protection with ITU-T G.8032 • Link Aggregation with IEEE 802.3ad • VLAN Push, Pop and translate • Service and Link OAM and fault management • Single or dual tag switching, S and C tag switching, QinQ Fujitsu Network Communications • 2801 Telecom Parkway, Richardson, TX 75082 Tel: 888.362.7763 • us.fujitsu.com/telecom © Copyright 2015 Fujitsu Network Communications, Inc. FUJITSU (and design)® and “shaping tomorrow with you” are trademarks of Fujitsu Limited in the United States and other countries. All Rights Reserved. 2 In This Issue . Feature Articles Science fiction has always been a fascinating world where 4 Everything Broadband, Broadband Everywhere the technology to support gadgetry and ability required By Timothy Downs no explanation or sound logic. -

Google, Bing, Yahoo!, Yandex & Baidu

Google, bing, Yahoo!, Yandex & Baidu – major differences and ranking factors. NO IMPACT » MAJOR IMPACT 1 2 3 4 TECHNICAL Domains & URLs - Use main pinyin keyword in domain - Main keyword in the domain - Main keyword in the domain - Main keyword in the domain - Easy to remember Keyword Domain 1 - As short as possible 2 - As short as possible 2 - As short as possible 11 - As short as possible - Use main pinyin keyword in URL - Main keyword as early as possible - Main keyword as early as possible - Main keyword as early as possible - Easy to remember Keyword in URL Path 3 - One specific keyword 3 - One specific keyword 3 - One specific keyword 11 - As short as possible - As short as possible - As short as possible - As short as possible - No filling words - No filling words - As short as possible Length of URL 2 2 2 22 - URL directory depth as brief as possible - No repeat of terms - No repeat of terms - Complete website secured with SSL -No ranking boost from HTTPS - No active SSL promotion - Complete website secured with SSL HTTPS 3 - No mix of HTTP and HTTPS 2 -Complete website secured with SSL 1 - Mostly recommended for authentication 22 - HTTPS is easier to be indexed than HTTP Country & Language - ccTLD or gTLD with country and language directories - ccTLD or gTLD with country and language directories - Better ranking with ccTLD (.cn or .com.cn) - Slightly better rankings in Russia with ccTLD .ru Local Top-Level Domain 3 - No regional domains, e.g. domain.eu, domain.asia 3 - No regional domains, e.g. -

18 November 2020

DEUTSCHE BÖRSE CASH MARKET Deutsches Eigenkapitalforum Online 16 – 18 November 2020 Programme overview Platinum Partners CONNECTING COMPANIES WITH INVESTORS Gold Partners Silver Partner Supporters Media Partners ICF BANK Monday, 16 November 09:00 Online check in Time for online networking and opportunity to visit the virtual exhibition Plenary session I – Mainstage/Venturestage 09:30 Welcome address and opening remarks * Dr Thomas Book, Executive Board, Deutsche Börse AG 10:00 Keynote speech: “After the virus: How different will the world be?” Shorter supply chains, more debt, more government intervention and a faster dispersion of Speaker: cutting-edge technologies in a more fractured world: the pandemic is reinforcing trends that Dr Holger Schmieding, had started to unfold before. How much of a difference could this make to growth, inflation Chief Economist, and markets trends? The keynote will offer some tentative answers to these questions. Berenberg Analysts’ conferences I 10:30 6 simultaneous streams (London, Madrid, Milan, Oslo, Paris, Zurich) 12:00 Break Time for online networking and opportunity to visit the virtual exhibition Plenary session II – Mainstage/Venturestage 13:00 Panel discussion: “IPO in volatile times: success factors for the IPO season 2021” * Chair: Speakers: Patrick Kalbhenn, Dr Martin Steinbach, Head of IPO and Listing Services, EY Spokesman, Renata Bandov, Director Pre-IPO & Capital Markets, Deutsche Börse AG Deutsche Börse AG Dr Joachim von der Goltz, Head Equity Capital Markets Northern Europe, Credit Suisse -

Broadband Access Equipment

COMMUNICATIONS ENGINEERING JFM ‘07 BROADBAND ACCESS EQUIPMENT Foreword Convergence is becoming a reality in the heart of service provider networks, but in the access network it's more a case of divergence, as service providers seek to offer broadband services over an increasing variety of access technologies, so that customers can get connected wherever they are. That raises a number of challenges for carriers, which are beginning to rethink their network infrastructures to address the heightened bandwidth requirements of services like IPTV and HDTV. Not only do they need to ramp up bandwidth to run these services, but they need to control the quality of user experience. At the same time, they need to devise strategies for supporting legacy, circuit-based services over new packet-based access infrastructure. And all this needs to happen in a way that permits the technology to be deployed and changed easily, cheaply, and rapidly. The telecom operators and their suppliers are addressing these challenges by developing new technologies such IMS (IP Multimedia Subsystem), carrier-class Ethernet, and pseudowire encapsulation. They're also working together in associations such as the DSL Forum to establish new standards and architectures. And all of this is resulting in a plethora of new products hitting the market -- a market that represents a huge opportunity for vendors. It's sometimes said that for every dollar carriers spend in the core of their networks they spend $10 on metro equipment and $100 on access networking. Broadband access is evolving at a rapid rate as subscriber rates around the world continue to soar. -

Determinants and Value of Enterprise Risk Management: Empirical Evidence from Germany

Determinants and Value of Enterprise Risk Management: Empirical Evidence from Germany Philipp Lechner, Nadine Gatzert Working Paper Department of Insurance Economics and Risk Management Friedrich-Alexander University Erlangen-Nürnberg (FAU) Version: February 2017 1 DETERMINANTS AND VALUE OF ENTERPRISE RISK MANAGEMENT: EMPIRICAL EVIDENCE FROM GERMANY Philipp Lechner, Nadine Gatzert* This version: February 21, 2017 ABSTRACT Enterprise risk management (ERM) has become increasingly relevant in recent years, espe- cially due to an increasing complexity of risks and the further development of regulatory frameworks. The aim of this paper is to empirically analyze firm characteristics that deter- mine the implementation of an ERM system and to study the impact of ERM on firm value. We focus on companies listed at the German stock exchange, which to the best of our knowledge is the first empirical study with a cross-sectional analysis for Germany and one of the first for a European country. Our findings show that size, international diversifica- tion, and the industry sector (banking, insurance, energy) positively impact the implementa- tion of an ERM system, and financial leverage is negatively related to ERM engagement. In addition, our results confirm a significant positive impact of ERM on shareholder value. Keywords: Enterprise risk management; firm characteristics; shareholder value JEL Classification: G20; G22; G32 1. INTRODUCTION In recent years, enterprise risk management (ERM) has become increasingly relevant, espe- cially against the background of an increasing complexity of risks, increasing dependencies between risk sources, more advanced methods of risk identification and quantification and information technologies, the consideration of ERM systems in rating processes, as well as stricter regulations in the aftermath of the financial crisis, among other drivers (see, e.g., Hoyt and Liebenberg, 2011; Pagach and Warr, 2011). -

The Calling Card of Russian Digital Antitrust✩ Natalia S

Russian Journal of Economics 6 (2020) 258–276 DOI 10.32609/j.ruje.6.53904 Publication date: 25 September 2020 www.rujec.org The calling card of Russian digital antitrust✩ Natalia S. Pavlova a,b,*, Andrey E. Shastitko a,b, Alexander A. Kurdin b a Russian Presidential Academy of National Economy and Public Administration, Moscow, Russia b Lomonosov Moscow State University, Moscow, Russia Abstract Digital antitrust is at the forefront of all expert discussions and is far from becoming an area of consensus among researchers. Moreover, the prescriptions for developed countries do not fit well the situation in developing countries, and namely in BRICS: where the violator of antitrust laws is based compared to national firms becomes an important factor that links competition and industrial policy. The article uses three recent cases from Russian antitrust policy in the digital sphere to illustrate typical patterns of platform conduct that lead not just to a restriction of competition that needs to be remedied by antitrust measures, but also to noteworthy distribution effects. The cases also illustrate the approach taken by the Russian competition authority to some typical problems that arise in digital markets, e.g. market definition, conduct interpretation, behavioral ef- fects, and remedies. The analysis sheds light on the specifics of Russian antitrust policy in digital markets, as well as their interpretation in the context of competition policy in developing countries and the link between competition and industrial policies. Keywords: digital antitrust, competition policy, industrial policy, platforms, multi-sided markets, essential facilities, consumer bias. JEL classification: K21, L41. 1. Introduction Russian antitrust as a direction of economic policy has a relatively short history, but a rich experience in the application of antitrust laws in areas that are considered digital.