WPP 2020 Interim Results Morning Teleconference Transcript

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE NEW WPP December 11, 2018

THE NEW WPP December 11, 2018 WPP plc Forward looking statement In order to utilize the ‘safe harbour’ provisions of the United States Private Securities Litigation Reform Act of 1995 (the ‘PSLRA’), WPP plc is providing the following cautionary statement. This presentation contains certain forward-looking statements – that is, statements related to future, not past events and circumstances – which may relate to one or more of the financial condition, results of operations and businesses of WPP plc and certain of the plans and objectives of WPP with respect to these items. These statements are generally, but not always, identified by the use of words such as ‘will’, ‘expects’, ‘is expected to’, ‘aims’, ‘should’, ‘may’, ‘objective’, ‘is likely to’, ‘intends’, ‘believes’, ‘anticipates’, ‘plans’, ‘we see’ or similar expressions. Actual results may differ from those expressed in such statements, depending on a variety of factors including the risk factors set forth in our most recent Annual Report and Form 20-F under “Risk factors” and in any of our more recent public reports. Nothing in this presentation is intended as a forecast, nor should it be taken as such. Our most recent Annual Report and Form 20-F and other period filings are available on our website at www.wpp.com, or can be obtained from the SEC by calling 1-800-SEC-0330 or on its website at www.sec.gov. WPP plc AGENDA OUR STRATEGY OUR VISION AND OFFER A SIMPLER STRUCTURE TECHNOLOGY CULTURE, LEADERSHIP AND TALENT WPP plc TECHNOLOGY IS FUNDAMENTALLY RESHAPING OUR INDUSTRY MEDIA PROLIFERATION -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Printmgr File

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F (Mark One) ‘ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR È ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended 31 December 2020 OR ‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ‘ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report For the transition period from to Commission file number 001-38303 WPP plc (Exact Name of Registrant as specified in its charter) Jersey (Jurisdiction of incorporation or organization) Sea Containers, 18 Upper Ground London, United Kingdom, SE1 9GL (Address of principal executive offices) Andrea Harris Group Chief Counsel Sea Containers, 18 Upper Ground, London, United Kingdom, SE1 9GL Telephone: +44(0) 20 7282 4600 E-mail: [email protected] (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Trading Symbol (s) Name of each exchange on which registered Ordinary Shares of 10p each WPP London Stock Exchange American Depositary Shares, each WPP New York Stock Exchange representing five Ordinary Shares (ADSs) Securities registered or to be registered pursuant to Section 12(g) of the Act. Not applicable (Title of Class) Not applicable (Title of Class) Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. -

Annual Report & Accounts 2017

Annual Report & Accounts 2017 Accounts & Report Annual Annual Report & Accounts 2017 Report &Annual Accounts Visit us online Annual Report wpp.com/annualreport2017 Pro bono work 2017 wpp.com/probono/2017 You can sign up to receive WPP’s public monthly online news bulletin at wpp.com/subscriptions Follow us on Twitter twitter.com/wpp Become a fan on Facebook facebook.com/wpp Watch us on YouTube youtube.com/wpp Connect with us on LinkedIn linkedin.com/company/wpp This year, our Annual Report takes its visual cue from commissioned work created especially for us by illustrator Christopher Corr. The brief was simple. Convey in images the global creative strength that distinguishes WPP – with its unrivalled repertory of talent, a global team of 203,000 people, possessing between them every skill required to launch, defend, reimagine and expand clients’ businesses. More information on the artist, see inside back cover. Contents The big picture How we behave and how we’re rewarded 2 The fast read 81 Letter from the Chairman of the Company 4 Who we are 83 Review of the Company’s governance and 6 What we do the Nomination and Governance Committee 8 Where we are 86 Review of the Audit Committee 89 Letter from the Chairman of the How we’re doing Compensation Committee 90 Performance at a glance 11 Financial summary 92 Compensation Committee Report 14 Strategic report to share owners 105 Implementation of reward policy for 16 Geographic performance management outside the Board 18 Sector performance 20 Financial commentary About share ownership 24 -

This Is the Message

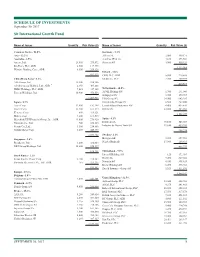

SCHEDULE OF INVESTMENTS September 30, 2017 Sit International Growth Fund Name of Issuer Quantity Fair Value ($) Name of Issuer Quantity Fair Value ($) Common Stocks - 96.0% Germany - 5.3% Asia - 22.2% Allianz SE 2,000 449,171 Australia - 2.5% Aurelius SE & Co. 4,160 273,564 Amcor, Ltd. 23,400 279,872 Siemens AG 3,900 550,324 Rio Tinto, PLC, ADR 2,500 117,975 1,273,059 Westpac Banking Corp., ADR 8,300 209,326 Ireland - 1.8% 607,173 CRH, PLC, ADR 5,800 219,588 China/Hong Kong - 6.2% Medtronic, PLC 2,700 209,979 AIA Group, Ltd. 32,200 238,386 429,567 Alibaba Group Holding, Ltd., ADR * 2,350 405,868 HSBC Holdings, PLC, ADR 7,025 347,105 Netherlands - 10.5% Tencent Holdings, Ltd. 10,900 476,556 ASML Holding NV 1,700 291,040 Galapagos NV * 3,725 379,717 1,467,915 ING Groep NV 34,900 643,285 Japan - 8.7% Koninklijke Philips NV 6,500 267,800 Asics Corp. 12,900 192,398 LyondellBasell Industries NV 4,400 435,820 Daicel Corp. 13,400 161,574 RELX NV 22,800 485,033 Keyence Corp. 600 319,121 2,502,695 Makita Corp. 4,200 169,515 Mitsubishi UFJ Financial Group, Inc., ADR 43,000 276,920 Spain - 4.1% Nintendo Co., Ltd. 700 258,113 Iberdrola SA 70,100 545,069 Secom Co., Ltd. 3,500 254,886 Industria de Diseno Textil SA 11,650 439,205 Suzuki Motor Corp. 8,400 440,875 984,274 2,073,402 Sweden - 2.1% Singapore - 2.6% Hexagon AB 5,200 257,962 Broadcom, Ltd. -

WPP AUNZ 2019 Annual Report

ANNUAL REPORT 2019 CONTENTS 2 CHAIRMAN’S LETTER 4 CEO’S WELCOME 6 OUR FOOTPRINT 8 OUR BRANDS 10 AT A GLANCE 11 OUR SOLUTIONS PILLARS 12 COMMUNICATIONS 22 EXPERIENCE 32 COMMERCE 38 TECHNOLOGY 44 SECRETS & LIES 46 TECHNOLOGY AND DATA 48 OUR CULTURE AND VALUES 50 SUSTAINABILITY 54 SOCIAL INVESTMENT 56 OUR PEOPLE 60 THE BOARD OF DIRECTORS 63 DIRECTORS’ REPORT 66 OPERATING AND FINANCIAL REVIEW 71 AUDITOR’S INDEPENDENCE DECLARATION 73 OUR REMUNERATION CHAIR’S LETTER 74 REMUNERATION REPORT 94 FINANCIAL STATEMENTS We bring together the most 156 DIRECTORS’ DECLARATION 157 INDEPENDENT AUDITOR’S REPORT creative minds, strategic thinkers 162 ASX ADDITIONAL INFORMATION and technology capabilities, to 164 CORPORATE DIRECTORY reshape and support the future of businesses and the public sector. WPP AUNZ ANNUAL REPORT 2019 CHAIRMAN’S LETTER Dear Shareholders which includes experience, commerce proceeds of $158.7 million have enabled and technology. us to reduce gearing to below the This past year has seen the start of a current target gearing ratio of 1.5 - 2.0 transformation for WPP AUNZ as we We are driving collaboration across our times net debt / EBITDA and ensure we finalised an extensive global search for a strong brands, investing in technology have capacity to support our new new CEO with the appointment of Jens capabilities and leveraging our existing strategic plan. Monsees in October 2019. Jens’ track knowledge and experience, to capture record of successfully transforming new opportunities that better serve our The Board is confident that, following the leading brands and companies, and his clients and their customers. -

Notice of Annual General Meeting BHP Billiton

BHP Billiton Plc Notice of Meeting 2015 This document is important and requires your immediate attention. Please read it straight away. If you are in any doubt as to any aspect of the proposals referred to in this document or as to the action you should take, you should immediately consult your stockbroker, solicitor, accountant or other professional adviser authorised under the Financial Services and Markets Act 2000. If you have sold or transferred all your shares in BHP Billiton Plc, please send this document, together with accompanying documents, at once to the purchaser or transferee, or to the stockbroker, bank or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Our Charter We are BHP Billiton, Our purpose is to create long-term shareholder value a leading global through the discovery, acquisition, development and resources company. marketing of natural resources. Our strategy is to own and operate large, long-life, low-cost, expandable, upstream assets diversified by commodity, geography and market. Our Values Sustainability Putting health and safety first, being environmentally responsible and supporting our communities. Integrity Doing what is right and doing what we say we will do. Respect Embracing openness, trust, teamwork, diversity and relationships that are mutually beneficial. Performance Achieving superior business results by stretching our capabilities. Simplicity Focusing our efforts on the things that matter most. Accountability Defining and accepting responsibility and delivering on our commitments. We are successful when: Our people start each day with a sense of purpose and end the day with a sense of accomplishment. -

360 Security Technology Inc 3Sbio Inc 3I Group PLC Abbott Laboratories

Aandelen Obligaties 360 Security Technology Inc 3SBio Inc 3i Group PLC Abbott Laboratories 3M Co AbbVie Inc 3SBio Inc ABN AMRO Bank NV 51job Inc Acadia Healthcare Co Inc 58.com Inc adidas AG AAC Technologies Holdings Inc ADLER Real Estate AG ABB Ltd ADO Properties SA Abbott Laboratories Aegon NV AbbVie Inc AES Corp/VA ABIOMED Inc African Development Bank ABN AMRO Bank NV Aggregate Holdings SA Aboitiz Equity Ventures Inc Air France-KLM Absa Group Ltd Air Transport Services Group I Accell Group NV Airbus SE Accenture PLC Akamai Technologies Inc Accor SA Aker BP ASA Acer Inc Albertsons Investor Holdings L ACS Actividades de Construccio Alcoa Corp Activision Blizzard Inc Alibaba Group Holding Ltd Acuity Brands Inc Allergan PLC Adaro Energy Tbk PT Alliander NV Adecco Group AG Allianz SE adidas AG Ally Financial Inc Adobe Inc Almirall SA Advance Auto Parts Inc Altice USA Inc Advanced Info Service PCL Amazon.com Inc Advanced Micro Devices Inc America Movil SAB de CV Advantech Co Ltd American Axle & Manufacturing Aegon NV American International Group I AES Corp/VA Amgen Inc Affiliated Managers Group Inc ams AG Agilent Technologies Inc ANA Holdings Inc AIA Group Ltd Anglian Water Group Ltd Air Liquide SA Anglo American PLC Air Products & Chemicals Inc Anheuser-Busch InBev SA/NV AirAsia Group Bhd Antero Resources Corp Airbus SE APA Group Aisino Corp APERAM SA Akamai Technologies Inc Aphria Inc Aker BP ASA Apollo Global Management LLC Akzo Nobel NV Apple Inc Alcon Inc Aptiv PLC Alexandria Real Estate Equitie Arab Republic of Egypt Alfa Laval AB Arconic -

Securities at Value BT WALDEN INTL EQUITY FD 31-Aug-21

Securities At Value BT WALDEN INTL EQUITY FD 31-Aug-21 Ticker Description Shares/Par Market Value SDR LN SCHRODERS PLC 16,300.0000 847,290.74 SN/ LN SMITH & NEPHEW 34,200.0000 654,962.57 BMO CN BANK OF MONTREAL 11,200.0000 1,114,761.79 BNS CN BANK OF NOVA SCO 19,000.0000 1,177,051.13 CNR CN CAN NATL RAILWAY 11,500.0000 1,352,833.93 GWO CN GREAT-WEST LIFEC 19,284.0000 596,634.58 MG CN MAGNA INTL 7,400.0000 584,432.82 MRU CN METRO INC 11,100.0000 565,514.86 RY CN ROYAL BANK OF CA 13,000.0000 1,335,552.91 TD CN TORONTO-DOM BANK 20,700.0000 1,344,392.39 MKS LN MARKS & SPENCER 318,860.0000 787,220.79 NXT LN NEXT PLC 5,900.0000 641,823.84 ITV LN ITV PLC 388,000.0000 617,956.67 OR FP L'OREAL 2,400.0000 1,124,939.73 FRE GR FRESENIUS SE & C 12,955.0000 673,618.09 PUB FP PUBLICIS GROUPE 12,400.0000 812,170.81 HNR1 GR HANNOVER RUECK S 2,800.0000 515,243.13 MRK GR MERCK KGAA 4,400.0000 1,045,160.93 JPMORGAN US GOVT MMKT 3,944,243.1000 3,944,243.10 SGSN SW SGS SA-REG 340.0000 1,067,761.33 SU FP SCHNEIDER ELECTR 6,700.0000 1,199,394.27 SAP GR SAP AG 9,606.0000 1,445,144.55 HEN GR HENKEL AG & CO K 8,300.0000 746,542.93 ALV GR ALLIANZ SE-VINK 2,900.0000 681,092.55 MUV2 GR MUENCHENER RUE-R 1,800.0000 525,687.71 BB FP SOCIETE BIC SA 8,443.0000 561,605.75 WKL NA WOLTERS KLUWER 9,300.0000 1,071,015.19 HMB SS HENNES & MAURI-B 33,400.0000 670,816.46 COLR BB COLRUYT SA 9,700.0000 542,665.60 VPK NA VOPAK 17,400.0000 752,887.80 GIVN SW GIVAUDAN-REG 240.0000 1,205,211.29 ZURN VX ZURICH INSURANCE GROUP AG 1,400.0000 615,093.20 101 HK HANG LUNG PROPER 302,000.0000 -

MOTI Vaneck Vectors Morningstar International Moat ETF Reconstitution

September 17, 2021 MOTI® VanEck Morningstar International Moat ETF VanEck Morningstar International Moat ETF seeks to track, before fees and expenses, the price and yield performance of the Morningstar® Global ex-US Moat Focus IndexSM. The index provides exposure to companies with Morningstar® Economic MoatTM ratings of Wide or Narrow that are trading at the lowest current market price to fair value ratios. The index has a staggered rebalance in which it is divided into two sub-portfolios, each with 50 stocks. One sub-portfolio reconstitutes in December and June; the other in March and September. The information here pertains only to the sub-portfolio being reconstituted. Reconstituted Index Sub-portfolio Name Ticker Country Moat Rating Price/Fair Value Subportfolio Weight % 1 Imperial Brands Plc IMB United Kingdom Wide 0.54 2.00 2 Dassault Aviation AM France Narrow 0.58 2.00 3 Continental AG CON Germany Narrow 0.61 2.00 4 Bayer Motoren Werke AG (BMW) BMW Germany Narrow 0.61 2.00 5 China Gas Holdings Ltd. 384 China Narrow 0.62 2.00 6 Danske Bank A/S DANSKE Denmark Narrow 0.63 2.00 7 BOC Hong Kong (Holdings) Ltd. 2388 China Narrow 0.66 2.00 8 Anheuser Busch Inbev NV ABI Belgium Wide 0.66 2.00 9 Vodafone Group VOD United Kingdom Narrow 0.66 2.00 10 SK Telecom Co Ltd 17670 South Korea Narrow 0.71 2.00 11 Win Semiconductors Corp 3105 Taiwan Narrow 0.72 2.00 12 Link Administration Holdings Limited LNK Australia Narrow 0.72 2.00 13 WPP Plc WPP United Kingdom Narrow 0.74 2.00 14 Yum China Holdings Inc YUMC China Wide 0.74 2.00 15 Sun Hung Kai Properties Ltd. -

Annual Report & Accounts 2019

ANNUAL REPORT & ACCOUNTS 2019 WHO WE ARE WPP IS A CREATIVE TRANSFORMATION COMPANY. WE USE THE POWER OF CREATIVITY TO BUILD BETTER FUTURES FOR OUR PEOPLE, CLIENTS AND COMMUNITIES. STRATEGIC REPORT Covid-19 2 Chief Executive’s statement 3 At a glance 8 Our business model 9 Investment case 10 Where we are 12 The market 14 Our strategy 16 Delivering on our strategy 18 Jeremy Bullmore’s essay 48 Remembering two industry greats 50 Financial review 52 Sustainability 58 Assessing and managing our risks 80 CORPORATE GOVERNANCE Chairman’s letter 94 Our Board 96 Our Executive Committee 98 Corporate governance report 100 Sustainability Committee report 107 Nomination and Governance Committee report 108 Audit Committee report 109 Compliance with the Code 112 Compensation Committee report 114 FINANCIAL STATEMENTS Accounting policies 140 Consolidated financial statements 147 Notes to the consolidated financial statements 152 Company financial statements 182 Notes to the Company financial statements 185 Independent auditor’s report 187 ADDITIONAL INFORMATION Taskforce on Climate-related Financial Disclosures 196 Other statutory information 198 Five-year summary 201 Information for shareholders 202 To learn more see Financial glossary 204 wpp.com Where to find us 206 WPP ANNUAL REPORT 2019 1 STRATEGIC REPORT COVID-19 The coronavirus pandemic has touched all our lives. At WPP our first priority is the wellbeing of our people and doing what we can to limit the impact of the virus on society. Our second is continuity of service for our clients. We have thrown ourselves into achieving both objectives. To ensure the safety of employees and We have also modelled a range of revenue When we come through the current to help reduce transmission, we moved declines resulting from the pandemic and, situation, the world will have been changed to a global policy of managed remote in the most extreme scenarios tested, in ways that we cannot fully anticipate yet. -

WPP ESG Investor Event

WPP ESG Investor Event Transcript Wednesday, 30th June 2021 WPP ESG Investor Event 30 June 2021 Disclaimer By reading this transcript you agree to be bound by the following conditions. You may not disseminate this transcript, in whole or in part, without our prior consent. Information in this communication relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments. This communication does not constitute an offering of securities or otherwise constitute an invitation or inducement to any person to underwrite, subscribe for or otherwise acquire or dispose of securities in any company within the WPP Group. Non-IFRS Measures Certain Non-IFRS measures included in this communication have been derived from amounts calculated in accordance with IFRS but are not themselves IFRS measures. They should not be viewed in isolation as alternatives to the equivalent IFRS measure, rather they should be read in conjunction with the equivalent IFRS measure. These include constant currency, pro-forma (‘like-for-like’), headline PBIT (Profit Before Interest and Taxation), headline PBT (Profit Before Taxation), headline EBITDA (Earnings before Interest, Taxation, Depreciation and Amortisation), billings, estimated net new billings, free cash flow and net debt and average net debt, which we define, explain the use of and reconcile to the nearest IFRS measure in the WPP Annual Report & Accounts 2020 for the year ended December 31, 2020. Management believes that these measures are both useful and necessary to present herein because they are used by management for internal performance analyses; the presentation of these measures facilitates comparability with other companies, although management’s measures may not be calculated in the same way as similarly titled measures reported by other companies; and these measures are useful in connection with discussions with the investment community.