The Great Depression As a Historical Problem

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Causes and Remedies for Japan's Long-Lasting Recession

ADBI Working Paper Series Causes and Remedies for Japan’s Long-Lasting Recession: Lessons for the People’s Republic of China Naoyuki Yoshino and Farhad Taghizadeh-Hesary No. 554 December 2015 Asian Development Bank Institute Naoyuki Yoshino is Dean and CEO of the Asian Development Bank Institute. Farhad Taghizadeh-Hesary is Assistant Professor of Economics at Keio University, Tokyo and a research assistant to the Dean of the Asian Development Bank Institute. The views expressed in this paper are the views of the author and do not necessarily reflect the views or policies of ADBI, ADB, its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. Working papers are subject to formal revision and correction before they are finalized and considered published. The Working Paper series is a continuation of the formerly named Discussion Paper series; the numbering of the papers continued without interruption or change. ADBI’s working papers reflect initial ideas on a topic and are posted online for discussion. ADBI encourages readers to post their comments on the main page for each working paper (given in the citation below). Some working papers may develop into other forms of publication. Suggested citation: Yoshino, N., and F. Taghizadeh-Hesary. 2015. Causes and Remedies for Japan’s Long- Lasting Recession: Lessons for the People’s Republic of China. ADBI Working Paper 554. Tokyo: Asian Development Bank Institute. -

The US Economy Since the Crisis: Slow Recovery and Secular Stagnation*

The US economy since the crisis: slow recovery and secular stagnation* Robert A. Blecker Professor of Economics, American University, Washington, DC 20016, USA Revised, March 2016 Abstract: The US economy has experienced a slowdown in its long-term growth and job creation that predates the Great Recession. The stagnation of output growth stems mainly from the depressing effects of rising inequality on aggregate demand, while both increased inequality and the delinkage of employment from output have their roots in profound structural changes to the US industrial structure and international position. Stagnation tendencies were temporarily offset by debt-financed household spending before the financial crisis, after which households became more financially constrained. Meanwhile, fiscal policy has shifted toward austerity while business investment has failed to keep up with the boom in corporate profits in spite of low interest rates. Slower US growth in turn exacerbates the global slowdown as it implies smaller injections of demand into global export markets. Keywords: US economy, secular stagnation, jobless recovery, financial crisis, Great Recession JEL codes: E20, E32, O51 *An earlier version of this paper was presented at the session on ‘Varieties of Stagnation? Europe, Japan and the US’, Conference on ‘The Spectre of Stagnation? Europe in the World Economy’, FMM/IMK/Hans Böckler Foundation, Berlin, Germany, 23 October 2015. Contact email for author: [email protected]. 1 INTRODUCTION The recovery from the Great Recession of 2008–9 has been the slowest and longest of any cyclical upturn in the US economy since the Great Depression of the 1930s. This slow and prolonged recovery was partly a result of the severity of the financial crisis that provoked the recession and the need to repair balance sheets in its aftermath (Koo 2013) as well as inadequate policy responses that failed to provide sufficient stimulus. -

How Secular Is the Current Economic Stagnation?

How secular is the current economic stagnation? Maria Roubtsova ∗ September 30, 2016 Abstract From the burst of the dotcom bubble in 2000, until the global financial crisis that started in August 2007, the global economy was growing. During that phase, macroe- conomics went through an era of general optimism around the idea of having reached a great moderation, with high steady growth and low stable inflation. Central bankers thought they managed to dampen the economic cycles. This era came to an end fol- lowing the meltdown which started with the global financial crisis of 2007. And as among economic agents, macroeconomists’ general state of mind went from optimism to pessimism. Almost ten years since the beginning of the crisis, growth is not back to its pre-crisis trends. Therefore, macroeconomists are debating the notion of a secular stagnation. Is the economy on a long-term stagnation trend, if so, for what reasons, and how to address this situation? This paper offers a critical review of the debates among macroeconomists around this notion of secular stagnation, a concept which was invented by Alvin Hansen following the global economic crisis of the 1930s, and was brought back into the public debate largely by Lawrence Summers since the end of 2013. This literature review starts with a brief synthesis of the original debate about secular stagnation, launched by Hansen in 1938, and ended in the mid-1950s, since these debates inspired contemporary theorists. The second part highlights the main elements of neoclassical explanations for secular stagnation. The third part focuses on the Minskian idea of the end of a debt super-cycle. -

Ebook Download Lectures on Inequality, Poverty and Welfare 1St

LECTURES ON INEQUALITY, POVERTY AND WELFARE 1ST EDITION PDF, EPUB, EBOOK Antonio Villar | 9783319455617 | | | | | Lectures on Inequality, Poverty and Welfare 1st edition PDF Book Arthur Lewis Charles L. There is little doubt that good child care can help children succeed and that one way income support can help children succeed is by enabling their parents to purchase better child care. Cambridge, Massachusetts: Harvard University Press. Economic theory Political economy Applied economics. Presidents of the International Economic Association. Growing evidence shows that low income can have lasting adverse effects on children and that bolstering family income can help poor children catch up in a range of areas. Figure 5. In some ways people had got used to the idea that India was spiritual and religion-oriented. Retrieved 26 April The school had many progressive features, such as distaste for examinations or competitive testing. The key approach consists in linking inequality and poverty measurement with welfare evaluation. Resources, Values, and Development. His influential monograph Collective Choice and Social Welfare , which addressed problems related to individual rights including formulation of the liberal paradox , justice and equity, majority rule, and the availability of information about individual conditions, inspired researchers to turn their attention to issues of basic welfare. In the Bengal famine, rural laborers' negative freedom to buy food was not affected. In order for citizens to have a capacity to vote, they first must have "functionings". In addition to his important work on the causes of famines, Sen's work in the field of development economics has had considerable influence in the formulation of the " Human Development Report ", [15] published by the United Nations Development Programme. -

Capacity Utilization, Inflation and Monetary Policy

Capacity Utilization, Inflation and Monetary Policy: Classicals, post-Keynesians and the New Keynesian Consensus Peter Kriesler and Marc Lavoie1 Abstract The paper looks at the adjustment process towards long run equilibrium within Marxian models, defined in terms of normal rates of capacity utilization. The model is reduced to three essential equations: an IS equation, a Phillips curve equation and an central bank reaction function. It is shown that long run convergence depends on the specific inflation (Phillips curve) equation, and on the central bank setting a zero inflationary target. When these conditions are relaxed, the results are shown to accord more closely with post-Keynesian results. The Marxian model is then contrasted with New Consensus models, which only varies in its inflation/Phillips curve equation. Post-Keynesian criticisms of both the IS and the Phillips curve equation are considered, and suggestions for a post-Keynesian alternative are made. Keywords: monetary policy, central bank, inflation, capacity utilization, post-Keynesian, New- Keynesian JEL classification: E12, E40, E52, E58 In an extremely interesting paper, Duménil and Lévy (Duménil and Lévy 1999) explore the adjustment mechanism of an economy towards a long run equilibrium with capacity utilization at normal levels − a fully adjusted position as the Sraffians would call it, or a classical long-term equilibrium as Duménil and Lévy have it. Short run equilibrium within their model is of the Keynes/Kalecki type, with variability in levels of capacity utilization. One distinctive feature of their model is that it is not the forces of competition which push the economy to a fully adjusted position, but rather aspects of the macro economy coupled with the behaviour of the central bank. -

The Institutionalist Reaction to Keynesian Economics

Journal of the History of Economic Thought, Volume 30, Number 1, March 2008 THE INSTITUTIONALIST REACTION TO KEYNESIAN ECONOMICS BY MALCOLM RUTHERFORD AND C. TYLER DESROCHES I. INTRODUCTION It is a common argument that one of the factors contributing to the decline of institutionalism as a movement within American economics was the arrival of Keynesian ideas and policies. In the past, this was frequently presented as a matter of Keynesian economics being ‘‘welcomed with open arms by a younger generation of American economists desperate to understand the Great Depression, an event which inherited wisdom was utterly unable to explain, and for which it was equally unable to prescribe a cure’’ (Laidler 1999, p. 211).1 As work by William Barber (1985) and David Laidler (1999) has made clear, there is something very wrong with this story. In the 1920s there was, as Laidler puts it, ‘‘a vigorous, diverse, and dis- tinctly American literature dealing with monetary economics and the business cycle,’’ a literature that had a central concern with the operation of the monetary system, gave great attention to the accelerator relationship, and contained ‘‘widespread faith in the stabilizing powers of counter-cyclical public-works expenditures’’ (Laidler 1999, pp. 211-12). Contributions by institutionalists such as Wesley C. Mitchell, J. M. Clark, and others were an important part of this literature. The experience of the Great Depression led some institutionalists to place a greater emphasis on expenditure policies. As early as 1933, Mordecai Ezekiel was estimating that about twelve million people out of the forty million previously employed in the University of Victoria and Erasmus University. -

Employment and Capacity Utilization Over the Business Cycle

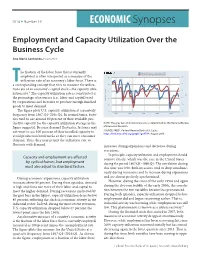

2016 n Number 19 ECONOMIC Synopses Employment and Capacity Utilization Over the Business Cycle Ana Maria Santacreu, Economist he fraction of the labor force that is currently Capacity Utilization: Total Industry (left) 100-Civilian Unemployment Rate (right) 98 employed is often interpreted as a measure of the 90 utilization rate of an economy’s labor force. There is 96 T 85 a corresponding concept that tries to measure the utiliza- tion rate of an economy’s capital stock—the capacity utili- 94 80 zation rate.1 The capacity utilization rate is constructed as 100-% 92 the percentage of resources (i.e., labor and capital) used 75 Percent of Capacity by corporations and factories to produce enough finished 90 goods to meet demand. 70 88 The figure plots U.S. capacity utilization at a quarterly 65 frequency from 1967:Q1–2016:Q1. In normal times, facto- 1970 1980 1990 2000 2010 ries tend to use around 80 percent of their available pro- fred.stlouisfed.org myf.red/g/6ZXZ ductive capacity (as the capacity utilization average in the NOTE: The gray bars indicate recessions as determined by the National Bureau figure suggests). Because demand fluctuates, factories may of Economic Research. SOURCE: FRED®, Federal Reserve Bank of St. Louis; not want to use 100 percent of their installed capacity to https://fred.stlouisfed.org/graph/?g=6TA4; August 2016. avoid production bottlenecks so they can meet consumer demand. Thus, they may permit the utilization rate to fluctuate with demand. increases during expansions and decreases during recessions. In principle, capacity utilization and employment should Capacity and employment are affected comove closely, which was the case in the United States by cyclical factors, but employment during the period 1967:Q1–1990:Q1. -

Imbalance Game 2.0: a Tale of Two Productivities

NEW THINKING Imbalance Game 2.0: A Tale of Two Productivities Michael Craig, CFA Vice President & Director Haining Zha, CFA Vice President September 2017 Almost nine years after the financial crisis, the global economy remains mired in low growth. Low productivity growth is certainly a key contributing factor, but our research shows that current productivity measures don’t tell the whole story. In this article, we propose a fundamental change to how people should examine productivity: we believe the supply and demand sides should be viewed separately to obtain more robust insights. Taking this approach allows us to differentiate supply-side progress from demand-side malaise and shows that the economy may be more promising than commonly thought. In addition, it highlights large supply-side divergences within and across different sectors of the economy, which are not reflected in the aggregate productivity measure – potentially leading to a distorted economic picture. Viewing productivity through this new lens, we believe that: • Nominal economic growth will remain low • Inflation will remain subdued • Interest rates will stay lower for longer • Technology-driven progress and persistent supply-side divergence will create investment risks and opportunities in equity markets In the investment world, economic growth is a big deal. We believe investment returns across asset classes can ultimately be traced back to one source: economic growth. Occasionally, asset prices can deviate from fundamentals, but over the long term, the relationship between returns and growth is very strong. That’s why it is critical to have a better understanding of the low growth phenomenon and key contributing factors, such as productivity. -

Off to a Good Start: the Nber and the Measurement of National Income

NBER WORKING PAPER SERIES OFF TO A GOOD START: THE NBER AND THE MEASUREMENT OF NATIONAL INCOME Hugh Rockoff Working Paper 26895 http://www.nber.org/papers/w26895 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 March 2020 Many thanks are due to Katharine Abraham who discussed a previous draft when it was presented at the 2020 annual meeting of the American Economic Association in a session celebrating the 100th anniversary of the Bureau, and to Claudia Goldin for many helpful comments. The remaining errors are mine. The views expressed herein are those of the author and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2020 by Hugh Rockoff. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Off to a Good Start: The NBER and the Measurement of National Income Hugh Rockoff NBER Working Paper No. 26895 March 2020 JEL No. B0,N12 ABSTRACT The creation of the National Bureau of Economic Research was a response to the bitter controversies over the distribution of income that roiled the United States during the Progressive Era. Thanks to Malcolm Rorty, a business economist, and Nahum I. Stone, an independent socialist economist, a “Committee on the Distribution of Income” was created; what might be considered the first name of the Bureau. -

Efficiency Wages, Insiders and Outsiders, and the Great Depression’

EFFICIENCY WAGES, INSIDERS AND OUTSIDERS, AND THE GREAT DEPRESSION’ Ranjit S. Dighe State University ofNew York at Oswego ABSTRACT This paper uses available quantitative and qualitative evidence from the I 930s to evaluate two prominent explanations of the wage explosion of the New Deal years of 1933—41: efficiency wages and insider-outsider models. The quantitative evidence includes various data on wage changes, hours, turn over, and strikes. Economically-based efficiency-wage models and the in sider-outsider model are found wanting as explanations of 1 930s labor mar kets. Efficiency-wage theories that emphasize worker morale fare better. This paper explains the 1930s wage burst as an interaction between New Deal policies and efforts by employers to maintain worker morale and productiv icy in a climate of growing union strength. The Great Depression, as the ultimate example of a persistent labor market disequi librium in American macroeconomic history; is inevitably seen by many as the ultimate case of sticky wages. Whatever importance one attaches to wage stickiness as a causal factor behind the mass unemployment of the 1930s, the failure ofthat unemployment to exert greater downward pressure on wages is striking. The downward rigidity ofwages in the Great Contraction of 1929—33 seems to receive the most attention from economic historians, but nearly all of the lasting increase in real wages came during the New Deal years of 1933_41.2 (See Figure.) From 1929 to June 1933, the average hourly earnings (AHE) offactory workers, measured against wholesale prices, rose just 4.5% in real product terms. (In nominal terms, they fell 23.7%, from $.590 to $.450.) From June 1933 when Congress passed the National Industrial Recovery Act (NIRA), the centerpiece of Presi dent Franklin D. -

Lee G. Branstetter

Lee G. Branstetter Carnegie Mellon University • H. John Heinz III College • School of Public Policy and Management 5000 Forbes Avenue Pittsburgh, PA 15213 • TEL (412) 268-4649 • [email protected] CURRENT ACADEMIC APPOINTMENTS Carnegie Mellon University Pittsburgh, PA Heinz College and Department of Social and Decision Sciences Director, Future of Work Initiative, 2016-present Professor of Economics and Public Policy, 2014-present Associate Professor of Economics and Public Policy (with tenure), 2006-2013 National Bureau of Economic Research Cambridge, MA Research Associate, 2006-present Faculty Research Fellow, 1996-2006 Affiliated with the Program on Productivity, Innovation, and Entrepreneurship and the Program on International Trade and Investment. Peterson Institute for International Economics Washington, DC Nonresident Senior Fellow, 2013-present ____________________________________________________________________________________________________ PREVIOUS APPOINTMENTS Council of Economic Advisers Washington, DC Executive Office of the President of the United States Senior Economist for International Trade and Investment, 2011-2012 Journal of International Economics Associate Editor, 2003-2011 Columbia Business School New York, NY Daniel Stanton Associate Professor of Business, 2004 – 2006 Director, International Business Program, 2002 – 2006 Associate Professor of Finance and Economics, 2001 – 2006 University of California, Davis Davis, CA Director, East Asian Studies Program, 1999 – 2001 Assistant Professor of Economics, 1996 -

Speech--Chairman Ben S. Bernanke

For release on delivery 9:30 a.m. EDT May 8, 2010 Commencement Address: The Economics of Happiness Remarks by Ben S. Bernanke Chairman Board of Governors of the Federal Reserve System at the University of South Carolina Columbia, South Carolina May 8, 2010 I want to begin by thanking the Board of Trustees of the University of South Carolina, President Pastides, and this year’s graduates for the great honor of addressing this commencement ceremony. Although I was born just across the border in Augusta, Georgia, I considered South Carolina my home from early childhood until I married and took my first academic job after graduate school. During most of that time, my family lived in Dillon, a couple of hours’ drive from here. I have had several occasions to visit Dillon and other places in the Carolinas since I got into government work, and I am both amazed and proud about the remarkable economic and social progress that has occurred since I grew up here. South Carolina, like America, is always reinventing itself, despite new and, it sometimes seems, ever more difficult challenges. I always find it difficult to choose a topic for a commencement talk. I am an economist, but my experience has been that people in a celebratory frame of mind are usually not that interested in an economics lecture. (I can’t quite understand why not.) Instead, they are generally looking for something more personal and inspirational. So I thought I would split the difference between an economics lecture and inspirational remarks and speak briefly about what economics and social science more generally have to say about personal happiness, and what those ideas imply both for economic policymaking and the choices each of you will make as you leave college for other pursuits.