Assessment of Different Approaches to Implementation of the IPPC Directive and Their Impacts on Competitiveness – Some Evidence from the Steel and Glass Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Home + Housewares Guide in an Industry That Changes Daily, It’S Hard to Keep

2019 Pre-Show Edition home + housewares Guide In an industry that changes daily, it’s hard to keep current. The International Home + Housewares Show is the perfect opportunity to get up-to-date: every year close to 60,000 of the world’s most important professionals gather to do business in Chicago. march 2 - 5 Register for badges: www.housewares.org Show Expos . 2-7 City of Chicago . 14-17 Educational Programs . 8-9 Show Planning . 18 Show Destinations . 10-11 Registration Information . 19 Show Events . 12-13 Welcome to Chicago . 20 Show Expos dine + décor Fashion-forward, innovative homegoods • cook + bakeware • tabletop, kitchen for the kitchen and dining room essentials + accents • gift • home décor The 2018 International Home + Housewares Show was a fantastic experience. I would recommend this to anyone in the business. It SOUTH HALL created an amazing atmosphere to network, engage, learn and grow your business. Excellent turnout with a good list of speakers that will benefit every aspect of retailing, and of course, well curated vendors! Exhibitors include: Regina Bonoan, Merchandising Group Manager cook + bakeware Make Room and More (SSI) All-Clad | BergHOFF International | Philippines Chantal Corp. | Corelle Brands | Cristel | CucinaPro | Cuisipro | De Buyer | Fissler | Groupe SEB | Jean Dubost | KRUPS | Search for all Exhibitors and Brands on L'Atelier Du Vin | Lagostina | Le Creuset | Housewares Connect 365 at Lodge Mfg. | Meyer | Nordic Ware | www.housewares.org/housewaresconnect365 Paderno World Cuisine | Rösle | Scanpan | -

Prelim Appendix H Category 6 Petitions

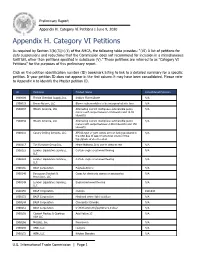

Preliminary Report Appendix H. Category VI Petitions | June 9, 2020 Appendix H. Category VI Petitions As required by Section 3(b)(3)(c)(ii) of the AMCA, the following table provides: “(VI) A list of petitions for duty suspensions and reductions that the Commission does not recommend for inclusion in a miscellaneous tariff bill, other than petitions specified in subclause (V).” These petitions are referred to as "Category VI Petitions” for the purposes of this preliminary report. Click on the petition identification number (ID) bookmark listing to link to a detailed summary for a specific petition. If your petition ID does not appear in the first column it may have been consolidated. Please refer to Appendix A to identify the Master petition ID. ID Petitioner Product Name Consolidated Petitions 1900009 Florida Chemical Supply, Inc. Sodium Fluorosilicate N/A 1900019 Broan-Nutone, LLC Blower subassemblies to be incorporated into fans N/A 1900037 Hitachi America, Ltd. Alternating current multiphase submersible pump N/A motors with output between 3 kilowatts and 14.92 kilowatts 1900038 Hitachi America, Ltd. Alternating current multiphase submersible pump N/A motors with output between 149.2 kilowatts and 150 kilowatts 1900116 Canary Drilling Services, LLC API 6A type of gate valves are not being produced in N/A the USA due to lack of economic source of the type/grade of steel needed 1900117 T.H Furniture Group Inc. Home Mattress,Only use to sleep or rest N/A 1900123 Lumber Liquidators Services, Certain engineered wood flooring N/A LLC 1900124 -

Download New Glass Review 15

eview 15 The Corning Museum of Glass NewGlass Review 15 The Corning Museum of Glass Corning, New York 1994 Objects reproduced in this annual review Objekte, die in dieser jahrlich erscheinenden were chosen with the understanding Zeitschrift veroffentlicht werden, wurden unter that they were designed and made within der Voraussetzung ausgewahlt, daB sie inner- the 1993 calendar year. halb des Kalenderjahres 1993 entworfen und gefertigt wurden. For additional copies of New Glass Review, Zusatzliche Exemplare der New Glass Review please contact: konnen angefordert werden bei: The Corning Museum of Glass Sales Department One Museum Way Corning, New York 14830-2253 Telephone: (607) 937-5371 Fax: (607) 937-3352 All rights reserved, 1994 Alle Rechte vorbehalten, 1994 The Corning Museum of Glass The Corning Museum of Glass Corning, New York 14830-2253 Corning, New York 14830-2253 Printed in Frechen, Germany Gedruckt in Frechen, Bundesrepublik Deutschland Standard Book Number 0-87290-133-5 ISSN: 0275-469X Library of Congress Catalog Card Number Aufgefuhrt im Katalog der Library of Congress 81-641214 unter der Nummer 81 -641214 Table of Contents/lnhalt Page/Seite Jury Statements/Statements der Jury 4 Artists and Objects/Kunstlerlnnen und Objekte 10 Bibliography/Bibliographie 30 A Selective Index of Proper Names and Places/ Ausgewahltes Register von Eigennamen und Orten 58 etztes Jahr an dieser Stelle beklagte ich, daB sehr viele Glaskunst- Jury Statements Ller aufgehort haben, uns Dias zu schicken - odervon vorneherein nie Zeit gefunden haben, welche zu schicken. Ich erklarte, daB auch wenn die Juroren ein bestimmtes Dia nicht fur die Veroffentlichung auswahlen, alle Dias sorgfaltig katalogisiert werden und ihnen ein fester Platz in der Forschungsbibliothek des Museums zugewiesen ast year in this space, I complained that a large number of glass wird. -

New Glass Review 10.Pdf

'New Glass Review 10J iGl eview 10 . The Corning Museum of Glass NewG lass Review 10 The Corning Museum of Glass Corning, New York 1989 Objects reproduced in this annual review Objekte, die in dieser jahrlich erscheinenden were chosen with the understanding Zeitschrift veroffentlicht werden, wurden unter that they were designed and made within der Voraussetzung ausgewahlt, dal3 sie the 1988 calendar year. innerhalb des Kalenderjahres 1988 entworfen und gefertigt wurden. For additional copies of New Glass Review, Zusatzliche Exemplare des New Glass Review please contact: konnen angefordert werden bei: The Corning Museum of Glass Sales Department One Museum Way Corning, New York 14830-2253 (607) 937-5371 All rights reserved, 1989 Alle Rechtevorbehalten, 1989 The Corning Museum of Glass The Corning Museum of Glass Corning, New York 14830-2253 Corning, New York 14830-2253 Printed in Dusseldorf FRG Gedruckt in Dusseldorf, Bundesrepublik Deutschland Standard Book Number 0-87290-119-X ISSN: 0275-469X Library of Congress Catalog Card Number Aufgefuhrt im Katalog der KongreB-Bucherei 81-641214 unter der Nummer 81-641214 Table of Contents/lnhalt Page/Seite Jury Statements/Statements der Jury 4 Artists and Objects/Kunstler und Objekte 10 Bibliography/Bibliographie 30 A Selective Index of Proper Names and Places/ Verzeichnis der Eigennamen und Orte 53 er Wunsch zu verallgemeinern scheint fast ebenso stark ausgepragt Jury Statements Dzu sein wie der Wunsch sich fortzupflanzen. Jeder mochte wissen, welchen Weg zeitgenossisches Glas geht, wie es in der Kunstwelt bewer- tet wird und welche Stile, Techniken und Lander maBgeblich oder im Ruckgang begriffen sind. Jedesmal, wenn ich mich hinsetze und einen Jurybericht fur New Glass Review schreibe (dies ist mein 13.), winden he desire to generalize must be almost as strong as the desire to und krummen sich meine Gedanken, um aus den tausend und mehr Dias, Tprocreate. -

The Glass Industry: Recent Trends and Changes in Working Conditions and Employment Relations

Working Paper No. 310 The glass industry: Recent trends and changes in working conditions and employment relations Nora Wintour Sectoral Policies Department WP 310 The glass industry: Recent trends and changes in working conditions and employment relations Nora Wintour International Labour Office Geneva Working papers are preliminary documents circulated to stimulate discussion and obtain comments Copyright © International Labour Organization 2015 First published 2015 Publications of the International Labour Office enjoy copyright under Protocol 2 of the Universal Copyright Convention. Nevertheless, short excerpts from them may be reproduced without authorization, on condition that the source is indicated. For rights of reproduction or translation, application should be made to ILO Publications (Rights and Licensing), International Labour Office, CH-1211 Geneva 22, Switzerland, or by email: [email protected]. The International Labour Office welcomes such applications. Libraries, institutions and other users registered with a reproduction rights organization may make copies in accordance with the licences issued to them for this purpose. Visit www.ifrro.org to find the reproduction rights organization in your country. ILO Cataloguing in Publication Data Wintour, Nora The glass industry : recent trends and changes in working conditions and employment relations / Nora Wintour ; International Labour Office, Sectoral Policies Department. - Geneva: ILO, 2015 (Working paper ; WP 310) ISBN: 9789221301172; 9789221301189 (web pdf) International Labour -

Homes & Interiors

Homes & Interiors - Ceramics, Glassware, Pictures & Decorative items - Live Online , 1 LG flatscreen television, model number7/04/2021 9:0018 AMUnusual Victorian Derby Porcelain Spill vase in 43UJ634V with remote control £50-80 the form of a Conch shell, supported by a Sea 2 Dyson DC40 vacuum cleaner with paperwork Horse £50-70 £30-50 19 Large Studio pottery charger with white flashes 3 Challenge floor standing electric oscillating fan on a blue ground £20-40 and a boxed Igenix heater (2) £20-40 20 Silver plated three piece teaset with fluted 4 Claude Butler Pine Lake mountain bike £30-50 decoration together with silver plated cutlery and sundries £20-40 5 Good Quality reproduction Ships Half Hull- 21 Extensive collection of Horse Brasses to include Iolanthe, Fitch Beale & Co, 1851, 127 x 30cm RSPCA Merit badges, and others (qty) £60-100 £100-150 22 Antique Copper 2 Gallon measure, together with 6 Good Quality reproduction Ships Half Hull- Iron miniature copper spirit kettles, copper brandy Ship Royale, 1863, 108 x 23cm £60-100 warmers and other antique metalware (qty) £80- 7 Pair of gold velvet interlined curtains, 230cm x 120 190cm approximately £30-50 23 Victorian Rosewood wall bracket with brass 8 Pakistani runner with geometric decoration on inlaid decoration, together with clocks for brown and red ground 236cm x 63cm £30-50 restoration £20-40 9 Eleven Royal Doulton figures - Hilary HN2335, 24 Brass ejector candlestick, together with other Fragrance HN2334, Elegance HN2264, Ashley brass candlesticks, copper and brass items (qty) HN3420, -

Punt Marks Guide Durobor SA

Reference of glass container manufacturing marks Punt Marks Guide Durobor SA ................................................................................................ 65 Table of Contents Elias Valavanis S.A. Glassworks ............................................................... 66 AGI Glaspac (Div. of HSIL, Formerly Associated Glass Industries, Ltd.) . 5 El Farran Glass Industry ........................................................................... 67 Addis Ababa Bottle & Glass Share Company ........................................... 6 El Nasr Glass & Crystal Co. ....................................................................... 68 Al Tajir Glass Industries LLC ....................................................................... 7 Fábrica de Envases de Vidrio - S.A. de C.V. .............................................. 69 Alembic Limited (Yera Glass) ..................................................................... 8 Fabrica Paraguaya de Vidrio (subsidiary of Ambev S.A.) ....................... 70 Allied Glass Containers Ltd. ....................................................................... 9 Formosan Glass Corporation ................................................................... 71 Amcor ........................................................................................................ 10 Gallo Glass Company ............................................................................... 72 Anadolu Cam Sanayii A.S. - SISECAM ..................................................... 11 Gamin Glass -

Download New Glass Review 21

NewG lass The Corning Museum of Glass NewGlass Review 21 The Corning Museum of Glass Corning, New York 2000 Objects reproduced in this annual review Objekte, die in dieser jahrlich erscheinenden were chosen with the understanding Zeitschrift veroffentlicht werden, wurden unter that they were designed and made within der Voraussetzung ausgewahlt, dass sie in- the 1999 calendar year. nerhalb des Kalenderjahres 1999 entworfen und gefertigt wurden. For additional copies of New Glass Review, Zusatzliche Exemplare der New Glass please contact: Review konnen angefordert werden bei: The Corning Museum of Glass Buying Office One Corning Glass Center Corning, New York 14830-2253 Telephone: (607) 974-6479 Fax: (607) 974-7365 E-mail: [email protected] All rights reserved, 2000 Alle Rechte vorbehalten, 2000 The Corning Museum of Glass The Corning Museum of Glass Corning, New York 14830-2253 Corning, New York 14830-2253 Printed in Frechen, Germany Gedruckt in Frechen, Bundesrepublik Deutschland Standard Book Number 0-87290-147-5 ISSN: 0275-469X Library of Congress Catalog Card Number Aufgefuhrt im Katalog der Library of Congress 81-641214 unter der Nummer 81-641214 Table of Contents/In halt Page/Seite Jury Statements/Statements der Jury 4 Artists and Objects/Kunstlerlnnen und Objekte 16 1999 in Review/Ruckblick auf 1999 36 Bibliography/Bibliografie 44 A Selective Index of Proper Names and Places/ Ausgewahltes Register von Eigennamen und Orten 73 Jury Statements Here is 2000, and where is art? Hier ist das Jahr 2000, und wo ist die Kunst? Although more people believe they make art than ever before, it is a Obwohl mehr Menschen als je zuvor glauben, sie machen Kunst, "definitionless" word about which a lot of people disagree. -

Lucy F. Kweskin Matthew A. Skrzynski PROSKAUER ROSE LLP Eleven

20-12097-scc Doc 505 Filed 01/22/21 Entered 01/22/21 18:51:52 Main Document Pg 1 of 186 Hearing Date: February 12, 2021 at 10:00 a.m. (Prevailing Eastern Time) Objection Deadline: February 5, 2021 at 4:00 p.m. (Prevailing Eastern Time) Lucy F. Kweskin Jeff J. Marwil (admitted pro hac vice) Matthew A. Skrzynski Jordan E. Sazant (admitted pro hac vice) PROSKAUER ROSE LLP Brooke H. Blackwell (admitted pro hac vice) Eleven Times Square PROSKAUER ROSE LLP New York, New York 10036 70 West Madison, Suite 3800 Telephone: (212) 969-3000 Chicago, IL 60602 Facsimile: (212) 969-2900 Telephone: (312) 962-3550 Facsimile: (312) 962-3551 Peter J. Young (admitted pro hac vice) PROSKAUER ROSE LLP 2029 Century Park East, Suite 2400 Los Angeles, CA 90067-3010 Telephone: (310) 557-2900 Facsimile: (310) 557-2193 Attorneys for Debtors and Debtors in Possession UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re Chapter 11 CENTURY 21 DEPARTMENT STORES LLC, et al., Case No. 20-12097 (SCC) Debtors.1 (Jointly Administered) NOTICE OF APPLICATION OF DEBTORS FOR ENTRY OF AN ORDER AUTHORIZING THE EMPLOYMENT AND RETENTION OF BERDON LLP AS TAX PREPARER AND CONSULTANT EFFECTIVE AS OF THE PETITION DATE PLEASE TAKE NOTICE that a hearing (the “Hearing”) will be held on the Application of Debtors for Entry of an Order Authorizing the Employment and Retention of Berdon LLP as 1 The Debtors in these chapter 11 cases (the “Chapter 11 Cases”), along with the last four digits of each Debtor’s federal tax identification number, as applicable, are Century 21 Department Stores LLC (4073), L.I. -

Bamfords Auctioneers & Valuers

Bamfords Auctioneers & Valuers The Derby Auction House Chequers Road Derby VICTORIAN, EDWARDIAN AND GENERAL SALE PART 2 Derbyshire DE21 6EN Started Jul 19, 2017 10:30am BST United Kingdom Lot Description 1000 A Hinks patent oil lamp with plated Corinthian column supporting clear cut glass font, later converted to electricity An early 19th Century substantial Named-View Derby campana vase, painted with a view in Wales, green ground, gilt snake handles, 1001 C.1825 (faults) Condition Report: Heavily damaged and poorly restored throughout, large cracks throughout An 18th century Pearlware blue and white bowl, painted with a child riding an Ox with others watching, pagoda, landscape, unmarked, 1002 29.5cm diam, c.1790 1003 A Japanese Pottery figure samurai warrior, green robes, long beard; another Geisha girl (2) 1004 A Japanese shaped circular plate, painted in underglaze blue with flowering peonies, 30cm diam, Miji period A large Royal Dux type model of an Indian elephant, standing with curled trunk, glazed in bronze green and gold tones, 44cm high, 1005 impressed marks (faults) 1006 A Moorcroft triangular ashtray, hibiscus on yellow ground A Victorian oversized Brandy balloon glass, engraved grape and vine Condition Report: A small 1mm chip to inner ring, light surface 1007 scratches throughout, 25cm high 1008 A Royal Worcester snuffer, as a Japanese girl 1009 A 19th century porcelain dog, Boxer 1010 A pair of large green glass bowls on stands 1011 A Goebel glass model Cockerel, painted decoration, engraved marks A late 19th century Staffordshire -

Baltic Glass the Development of New Creative Models Based on Historical and Contemporary Contextualization

Vesele, Anna (2010) Baltic Glass The development of new creative models based on historical and contemporary contextualization. Doctoral thesis, University of Sunderland. Downloaded from: http://sure.sunderland.ac.uk/3659/ Usage guidelines Please refer to the usage guidelines at http://sure.sunderland.ac.uk/policies.html or alternatively contact [email protected]. Baltic Glass The development of new creative models based on historical and contemporary contextualization Anna Vesele A thesis submitted in partial fulfilment of the requirements of the University of Sunderland for the degree of Doctor of Philosophy Faculty of Arts, Design and Media, University of Sunderland April 2010 1 Abstract The aim of this research was to demonstrate the creative potential of a particular type of coloured flat glass. This glass is produced in Russia and is known as Russian glass. The present researcher has refined methods used by Baltic glass artists to create three- dimensional artworks. The examination of the development of glass techniques in Estonia, Latvia and Lithuania was necessary in order to identify these methods and to contextualize the researcher’s personal practice. This study describes for the first time the development of glass art techniques in the Baltic States from the 1950s to the present day. A multi-method approach was used to address research issues from the perspective of the glass practitioner. The methods consisted of the development of sketches, models and glass artworks using existing and unique assembling methods. The artworks underlined the creative potential of flat material and gave rise to a reduction in costs. In conjunction with these methods, the case studies focused on the identification of similarities among Baltic glass practices and similarities of approach to using various glass techniques. -

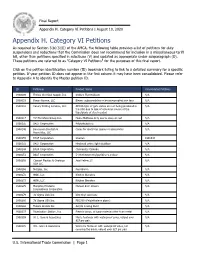

Final Appendix H Category 6 Petitions

Final Report Appendix H. Category VI Petitions | August 10, 2020 Appendix H. Category VI Petitions As required by Section 3(b)(3)(E) of the AMCA, the following table provides a list of petitions for duty suspensions and reductions that the Commission does not recommend for inclusion in a miscellaneous tariff bill, other than petitions specified in subclause (V) and updated as appropriate under subparagraph (D). These petitions are referred to as "Category VI Petitions" for the purposes of this final report. Click on the petition identification number (ID) bookmark listing to link to a detailed summary for a specific petition. If your petition ID does not appear in the first column it may have been consolidated. Please refer to Appendix A to identify the Master petition ID. ID Petitioner Product Name Consolidated Petitions 1900009 Florida Chemical Supply, Inc. Sodium Fluorosilicate N/A 1900019 Broan-Nutone, LLC Blower subassemblies to be incorporated into fans N/A 1900116 Canary Drilling Services, LLC API 6A type of gate valves are not being produced in N/A the USA due to lack of economic source of the type/grade of steel needed 1900117 T.H Furniture Group Inc. Home Mattress,Only use to sleep or rest N/A 1900135 BASF Corporation Polyisobutylene N/A 1900146 Bensussen Deutsch & Cases for electronic games or accessories N/A Associates, LLC 1900155 BASF Corporation Oxoiron 1901843 1900172 BASF Corporation Hindered amine light stabilizer N/A 1900244 BASF Corporation Chloracetyl Chloride N/A 1900251 BASF Corporation 5-(Methoxymethyl)pyridine-2,3-dicar N/A 1900258 Clariant Plastics & Coatings Acid Yellow 23 N/A USA LLC 1900268 Metglas, Inc.